|

市场调查报告书

商品编码

1683982

亚太杀菌剂:市场占有率分析、产业趋势与成长预测(2025-2030)Asia Pacific Fungicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

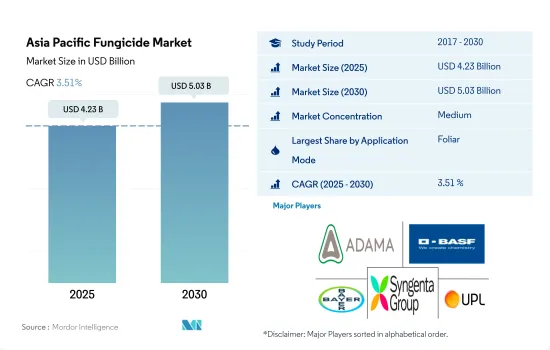

亚太杀菌剂市场规模预计在 2025 年为 42.3 亿美元,预计到 2030 年将达到 50.3 亿美元,预测期内(2025-2030 年)的复合年增长率为 3.51%。

由于气候条件变化,真菌疾病的盛行率不断上升,推动了市场

- 2022年叶面喷布占杀菌剂市场的60.7%,市场规模为23.2亿美元。这种施用方法是优选的,因为它直接针对植物的脆弱部位,保护它们免受真菌疾病的侵害。叶面喷布杀菌剂可有效保护叶子、茎部和地上植物组织。

- 杀菌剂种子处理通常用于在植物发育的早期阶段对抗真菌感染。它们在种子周围形成保护屏障,防止猝倒病、幼苗猝倒病和根腐病等疾病。在亚太杀菌剂市场中,杀菌剂种子处理在 2022 年占据了 13.9% 的显着份额。

- 2022 年化学灌溉市场价值为 4.719 亿美元。由于精准施药、人事费用降低以及田间杀菌剂分配效率更高等因素,预计该市场将进一步成长。预计中国、印度和澳洲等国家越来越多地采用微灌溉系统将推动市场成长。

- 透过将杀菌剂施用于土壤,杀菌剂分子会被植物根部吸收,从而提供对土壤传播的真菌病原体的保护。这些病原体,如枯萎病、黄萎病、疫霉菌根腐病、腐霉菌根腐病和立枯丝核菌根腐病,对该地区种植的各种作物构成重大威胁。土壤中使用杀菌剂可以有效对抗这些毁灭性的疾病。

- 透过利用各种施用方法,农民可以采取有针对性的方法来保护作物免受真菌感染并提高整体生产力。

中国主导亚太杀菌剂市场

- 亚太地区以其多样化的农作物而闻名。米是许多国家的主食,尤其是东南亚国家,例如泰国、越南和印尼。其他重要作物包括小麦、玉米、大豆、甘蔗、水果和蔬菜。中国和印度是多种作物的主要生产国,为区域和全球粮食供应做出重大贡献。

- 中国主导亚太杀菌剂市场,2022 年占 31.5% 的市场占有率。中国主要的杀菌剂类别包括三唑类、甲氧基丙烯酸酯类丙烯酸酯类、苯并咪唑酮、二硫代氨基甲酸和醌类外抑制剂 (QoI)。这些杀菌剂具有不同的作用方式并针对特定的真菌病原体。

- 日本是第二大杀菌剂消费国,2022 年的市场占有率为 16.8%。日本大多数谷物和谷类易受由 Helicobasidium mompa、Roselinia necatrix、Anillaria melea 和 Rhizoctonia solani 引起的严重土传病害的产量,导致重要作物作物减产。预计这些因素将进一步增加日本对化学杀菌剂的需求,预测期内(2023-2029 年)的复合年增长率估计为 3.4%。

- 该地区不断增长的人口,加上对更多作物的需求,促使人们使用杀虫剂来提高作物产量。在东南亚国家和印度,人均可耕地面积正在以惊人的速度下降,杀菌剂的使用在提高每公顷平均作物产量方面发挥关键作用。由于上述原因,预测期内市场复合年增长率预计将达到 3.7%。

亚太地区杀菌剂市场趋势

主要作物受病害影响的加剧以及提高产量的需求将推高每公顷杀菌剂的消费量

- 在亚太地区,病原体的存在造成了农业生产的重大损失,因此需要增加杀菌剂的使用。 2022年日本每公顷杀菌剂消费量将达7.9公斤,高于亚太地区任何其他国家。与 2017 年的资料相比,这些数字显示使用量增加了约 13%。这种增长可以归因于杀菌剂的应用对控制疾病传播的有效性,特别是水稻稻瘟病和大豆銹病等空气传播疾病,这导致每公顷杀菌剂的消费量增加。

- 缅甸已成为继日本之后第二个大幅增加每公顷杀菌剂消费量的国家。推动这一趋势的因素有很多。采用密集耕作方式来提高生产力,以及更高频率地使用杀菌剂来减轻疾病爆发,是每公顷杀菌剂消费量急剧增加的主要因素。由于这些原因,缅甸杀菌剂的使用量显着增加。例如缅甸主要作物水稻的种植。农民严重依赖杀菌剂来有效控制晚疫病和螟蛾。

- 整体来看,除中国和泰国外,该地区杀菌剂消费量持续成长。这一趋势背后有几个因素,包括气候变迁、为提高产量而进行的强化农业实践、频繁爆发的疾病以及减少杀菌剂残留的法规不足。中国、泰国等国积极采取措施减少农药消费量,农药使用量下降。

气候变迁改变了真菌的生存、传染性和宿主的易感性,导致了新疾病的出现。

- Tebuconazole是一种系统性杀菌剂,2022 年的价格为每吨 8,700 美元。Tebuconazole以治疗銹病、纹枯病、叶斑病和炭疽病而闻名。

- Mancozeb是一种广谱接触性杀菌剂,用于控製油籽、油菜籽、生菜、小麦、苹果、番茄、鲜食葡萄、酿酒葡萄、洋葱、胡萝卜、欧洲防风草、红葱和硬粒小麦中的多种真菌疾病,包括炭疽病、腐霉病、叶斑病、白粉病、灰霉病、銹病和频谱。 2022 年Mancozeb的价格为每吨 7,700 美元。

- Azoxystrobin是一种广谱频谱,可有效对抗真菌、子囊菌、真菌和担子菌类病原体。由于镰刀菌和木霉菌等真菌的侵染增加,Azoxystrobin的价格已从 2017 年的每吨 4,000 美元上涨至 2022 年的每吨 4,600 美元。同样,用于控制真菌引起的植物疾病的系统性杀菌剂Metalaxyl2022 年的价格为每公吨 4,400 美元。

- 丙森锌是一种二硫代氨基甲酸接触性杀菌剂,2022 年的价格为每吨 3,500 美元。丙森锌适用于番茄、白菜、黄瓜、芒果、花卉等,用于防治芒果早疫病、晚疫病,白菜炭疽病,马铃薯霜霉病,黄瓜霜霉病,番茄晚疫病。

- Zealam 是一种基本的接触性和叶面性杀菌剂,2022 年的价格为每吨 3,200 美元。主要防治马铃薯/番茄早疫病、晚疫病,攀缘植物和葫芦科植物的霜霉病、黑腐病,苹果黑星病,香蕉叶斑病,柑橘黑变病。

亚太杀菌剂产业概况

亚太杀菌剂市场适度整合,前五大公司占56.43%的市占率。该市场的主要企业有:ADAMA Agricultural Solutions Ltd.、 BASF SE、Bayer AG、Syngenta Group 和 UPL Limited(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 每公顷农药消费量

- 活性成分价格分析

- 法律规范

- 澳洲

- 中国

- 印度

- 印尼

- 日本

- 缅甸

- 巴基斯坦

- 菲律宾

- 泰国

- 越南

- 价值炼和通路分析

第五章 市场区隔

- 应用模式

- 化学喷涂

- 叶面喷布

- 熏蒸

- 种子处理

- 土壤处理

- 作物类型

- 经济作物

- 水果和蔬菜

- 粮食

- 豆类和油籽

- 草坪和观赏植物

- 原产地

- 澳洲

- 中国

- 印度

- 印尼

- 日本

- 缅甸

- 巴基斯坦

- 菲律宾

- 泰国

- 越南

- 其他亚太地区

第六章 竞争格局

- 关键策略趋势

- 市场占有率分析

- 商业状况

- 公司简介(包括全球概况、市场层级概况、主要业务部门、财务状况、员工人数、关键资讯、市场排名、市场占有率、产品和服务、最新发展分析)

- ADAMA Agricultural Solutions Ltd.

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Jiangsu Yangnong Chemical Co. Ltd

- Nufarm Ltd

- Rainbow Agro

- Syngenta Group

- UPL Limited

第七章:CEO面临的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 50001684

The Asia Pacific Fungicide Market size is estimated at 4.23 billion USD in 2025, and is expected to reach 5.03 billion USD by 2030, growing at a CAGR of 3.51% during the forecast period (2025-2030).

The increased infestation of fungal diseases due to changing climatic conditions drives the market

- In 2022, the fungicides market witnessed the dominance of foliar application, holding a significant share of 60.7% with a value of USD 2.32 billion. This application method is preferred due to its ability to directly target and protect vulnerable plant parts from fungal diseases. By applying fungicides through the foliar application, leaves, stems, and above-ground plant tissues may effectively be safeguarded.

- Fungicide seed treatments are commonly used to combat fungal infections during the early stages of plant development. They form a protective barrier on the seeds, preventing diseases such as damping-off, seedling blights, and root rots. In the Asia-Pacific fungicide market, fungicide seed treatments held a substantial share of 13.9% in 2022.

- The market for chemigation was valued at USD 471.9 million in 2022. It is further estimated to grow owing to factors like its precise application, reduced labor costs, and increased efficiency in the distribution of fungicides throughout the field. The increase in the adoption of micro-irrigation systems in countries like China, India, and Australia is expected to aid the market's growth.

- Applying fungicides to the soil allows for the uptake of fungicide molecules by plant roots, protecting against soilborne fungal pathogens. These pathogens, such as Fusarium wilt, verticillium wilt, Phytophthora root rot, Pythium root rot, and Rhizoctonia root rot, pose significant threats to various crop types grown in the region. Soil application of fungicides effectively combats these destructive diseases.

- By utilizing different application methods, farmers may employ targeted approaches to protect their crops from fungal infections and enhance overall productivity.

China dominates the Asia-Pacific fungicide market

- Asia-Pacific is known for its diverse agricultural crops. Rice is a staple food in many countries, particularly in Southeast Asia, such as Thailand, Vietnam, and Indonesia. Other important crops include wheat, corn, soybeans, sugarcane, fruits, and vegetables. China and India are major producers of various crops, contributing significantly to the regional and global food supply.

- China dominated the Asia-Pacific fungicide market, accounting for a market share of 31.5% in 2022. Major fungicide classes in China include triazoles, strobilurins, benzimidazoles, dithiocarbamates, and quinone outside inhibitors (QoIs). These fungicides have different modes of action and target specific fungal pathogens.

- Japan is the second-largest consumer of fungicides, and it had a market share of 16.8% in 2022. Most of the grain and cereal crops in Japan are prone to serious soil-borne diseases that are caused by Helicobasidium mompa, Rosellinia necatrix, Annillaria mellea, and Rhizoctonia solani,which cause serious yield losses in economically important crops. These factors are further expected to increase Japan's demand for chemical fungicides while registering an estimated CAGR of 3.4% during the forecast period (2023-2029).

- The increasing need for food crops due to the region's population increase fueled the use of pesticides to enhance crop yield. In Southeast Asian countries and India, the arable land per person is decreasing at an alarming rate, where the use of fungicides can play an important role in increasing the average crop yields per hectare. Owing to the above reasons, the market is anticipated to record a CAGR of 3.7% during the forecast period.

Asia Pacific Fungicide Market Trends

Increased disease effects on major crops and the need for higher productivity raise the per-hectare fungicide consumption

- In the Asia-Pacific, the presence of pathogens leads to significant losses in agricultural production, necessitating the increased utilization of fungicides. Japan's fungicide consumption per hectare in 2022 stood at 7.9 kg, surpassing other Asia-Pacific countries. This figure illustrates a rise of roughly 13% in usage compared to the recorded data from 2017. This increase may be attributed to the effectiveness of fungicide application in controlling the spread of diseases, particularly airborne diseases like rice blast or soybean rust, which led to increased consumption of fungicide per hectare.

- Myanmar has emerged as the next country to significantly escalate its consumption of fungicides per hectare, following in the footsteps of Japan. Numerous factors contribute to this trend. The adoption of intensive agricultural practices aimed at enhancing productivity, coupled with higher application rates and frequent use of fungicides to mitigate disease outbreaks, stand out as the primary drivers behind the surge in fungicide consumption per hectare. These reasons have contributed to the notable increase in fungicide utilization within Myanmar. For instance, the cultivation of rice, which serves as a major crop in Myanmar. Farmers rely heavily on fungicides to effectively manage blight and false smut.

- Overall, the region is witnessing a consistent rise in fungicide consumption, except in China and Thailand. Several factors contribute to this trend, including climate change, intensified agricultural practices aimed at boosting production, frequent disease outbreaks, and inadequate regulations for reducing fungicidal residues. China and Thailand have taken proactive measures to reduce pesticide consumption, resulting in lower usage in these countries.

Climatic changes altering fungal survivability, infectivity, and host susceptibility are leading to new disease outbreaks

- Tebuconazole, a systematic fungicide, was valued at a price of USD 8.7 thousand per metric ton in 2022. Tebuconazole is known to treat rust fungus, sheath blight, leaf spot, and anthracnose.

- Mancozeb is a broad-spectrum contact fungicide used to control many fungal diseases, such as anthracnose, pythium blight, leaf spot, downy mildew, Botrytis, rust, and scab in oilseeds rapeseeds, lettuce, wheat, apples, tomatoes, table grapes, wine grapes, bulb onions, carrots, parsnips, shallots, and durum wheat. Mancozeb was priced at USD 7.7 thousand per metric ton in 2022.

- Azoxystrobin is a broad-spectrum fungicide active against fungal pathogens belonging to the Oomycetes, Ascomycetes, Deuteromycetes, and Basidiomycetes. Owing to the increase in infestation of fungi like Fusarium and Trichoderma, the price of azoxystrobin increased from USD 4.0 thousand per metric ton in 2017 to USD 4.6 thousand per metric ton by 2022. Similarly, metalaxyl is a systemic fungicide used to control plant diseases caused by Oomycete fungi, which was priced at USD 4.4 thousand per metric ton in 2022.

- Propineb is a dithiocarbamate, a contact fungicide that was priced at USD 3.5 thousand per metric ton in 2022. Propineb is applicable to tomatoes, Chinese cabbages, cucumbers, mangoes, flowers, and other crops. It is used in preventing and treating early late blight of mango, anthracnose of Chinese cabbage, potato downy mildew, cucumber downy mildew, and tomato late blight.

- Ziram is a basic contact and foliar fungicide that was priced at USD 3.2 thousand per metric ton in 2022. It mainly controls early and late blight of potatoes/tomatoes, downy mildew and black rot of vines and cucurbits, scab of apples, Sigatoka of bananas, and citrus melanosis.

Asia Pacific Fungicide Industry Overview

The Asia Pacific Fungicide Market is moderately consolidated, with the top five companies occupying 56.43%. The major players in this market are ADAMA Agricultural Solutions Ltd., BASF SE, Bayer AG, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Indonesia

- 4.3.5 Japan

- 4.3.6 Myanmar

- 4.3.7 Pakistan

- 4.3.8 Philippines

- 4.3.9 Thailand

- 4.3.10 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Myanmar

- 5.3.7 Pakistan

- 5.3.8 Philippines

- 5.3.9 Thailand

- 5.3.10 Vietnam

- 5.3.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd.

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Jiangsu Yangnong Chemical Co. Ltd

- 6.4.7 Nufarm Ltd

- 6.4.8 Rainbow Agro

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

农业杀菌剂市场:依配方、作物类型、有效成分、应用和通路管道划分-2026-2032年全球预测杀菌剂市场:依产品类型、剂型、应用、终端用户产业及通路划分-2026-2032年全球预测溴基杀菌剂市场按用途、化合物类型、物理形态、应用方法和最终用户划分,全球预测(2026-2032年)

农业杀菌剂市场:依配方、作物类型、有效成分、应用和通路管道划分-2026-2032年全球预测杀菌剂市场:依产品类型、剂型、应用、终端用户产业及通路划分-2026-2032年全球预测溴基杀菌剂市场按用途、化合物类型、物理形态、应用方法和最终用户划分,全球预测(2026-2032年) 2026年全球三唑类杀菌剂市场报告2026年全球化学杀菌剂市场报告2026年全球杀菌剂市场报告2026年全球杀菌剂市场报告

2026年全球三唑类杀菌剂市场报告2026年全球化学杀菌剂市场报告2026年全球杀菌剂市场报告2026年全球杀菌剂市场报告 农业杀菌剂市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、作物类型、地区和竞争格局划分,2021-2031年奥沙噻菌灵杀菌剂市场按作物类型、剂型、目标病害、施用方法和销售管道-全球预测(2026-2032 年)植物杀菌剂市场:依杀菌剂类型、作物类型、剂型、作用方式及施用方法划分-2026-2032年全球预测

农业杀菌剂市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、作物类型、地区和竞争格局划分,2021-2031年奥沙噻菌灵杀菌剂市场按作物类型、剂型、目标病害、施用方法和销售管道-全球预测(2026-2032 年)植物杀菌剂市场:依杀菌剂类型、作物类型、剂型、作用方式及施用方法划分-2026-2032年全球预测

▼