|

市场调查报告书

商品编码

1683984

中国除草剂市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030)China Herbicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

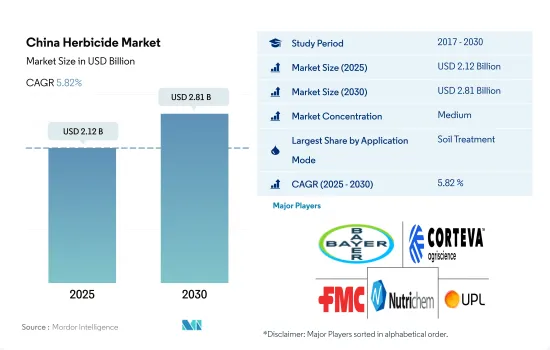

预计 2025 年中国除草剂市场规模为 21.2 亿美元,到 2030 年将达到 28.1 亿美元,预测期内(2025-2030 年)的复合年增长率为 5.82%。

市场受到有效除草剂控制需求的驱动。

- 中国农民使用多种方法来施用除草剂。所有这些方法的总市场规模预计到 2022 年将达到 17.8 亿美元。

- 2022年,土壤治疗方法占最高市场占有率,为8.415亿美元,占整个除草剂市场的47.2%。土壤处理之所以受欢迎,是因为其有效性,特别是使用出苗前除草剂,它可以在作物播种前针对杂草种子并抑制其发芽。叶面喷布除草剂的市场占有率在 2022 年达到 31.9%,为杂草控制带来了许多好处。这样可以实现精确定位,因为除草剂可以直接与杂草叶子接触并透过叶子表面吸收。

- 化学灌溉从2017年的1.994亿美元增加到2022年的3.398亿美元。 2022年主要用于谷物和谷类领域,占市场占有率的52.3%。这是因为微灌系统在这些作物中很普遍,并且非常适合化学灌溉。

- 叶面喷布在杂草控制方面具有多种优势。叶面喷布可使除草剂直接与杂草叶片接触,产生更有针对性的除草效果。

- 熏蒸除草方法不如其他喷洒方法常见,因为熏蒸方法的高度特异性和环境因素限制了其应用范围。但它能有效控制其他方法无法控制的顽固杂草。

- 考虑到每种施用方法对农民的有效性、特殊性及其重要性,除草剂市场预计在预测期内(即 2023-2029 年)的复合年增长率为 6.1%。

中国除草剂市场趋势

采用轮作等替代方案以及除草剂应用技术进步-控制除草剂的使用有助于减少每公顷的消费量

- 由于几个重要因素,中国的除草剂使用量大幅下降。造成这种情况的一个因素是,人们越来越认识到并采用轮作和生物防治作为农业、园艺和景观美化等各个领域有效管理杂草的重要工具。

- 轮作是指在较长时间内在同一块土地上依照特定顺序种植不同作物。不同作物有不同的生长模式和营养需求,有助于打断杂草的生命週期。透过作物,中国农民扰乱了杂草的生长週期,减少了杂草数量,并最大限度地减少了大量使用除草剂的需要。

- 中国农民成功地利用生物防治剂有效管理了多种作物中的杂草,大大减少了除草剂的使用。引入此类生物防治剂非常有益,减少了对各种农业实践中喷洒除草剂的依赖。

- 中国农民正在使用无人驾驶航空器系统(UAS) 影像分析和电脑视觉技术来加强杂草管理。这种方法使我们能够找出哪些行长满了杂草,并有选择地精确施用除草剂,而保留没有杂草的行。这种创新方法避免了不必要的喷洒,有效地减少了除草剂的浪费,从而整体减少了每公顷除草剂的消费量。

- 透过种植基改作物,农民可以最大限度地减少额外投资的需要,并显着减少每公顷除草剂的消费量。

中国是世界上最大的Glyphosate生产国和出口国。

- 杂草是作物生产的主要限制因素,对中国的粮食安全至关重要。 500多种入侵杂草对中国的农业生产和生态系统构成威胁。Atrazine、Paraquat和Glyphosate是中国常用的除草剂。

- Atrazine是一种广泛用于控制多种阔叶杂草和禾本科植物的除草剂。中国每年消耗超过16,000吨的Atrazine(技术上占97%)。Atrazine主要用于控制玉米和甘蔗田的一年生杂草。中国是世界主要的莠Atrazine供应国之一。 2022 年的价格为每吨 13,700 美元。

- Paraquat是克无踪的活性成分,可以控制杂草和草类。它也用于在收穫前干燥棉花等作物。 2022年Paraquat的价格为每吨4,600美元。中国是Paraquat的主要出口国,其80%以上的Paraquat产量出口到世界各国。

- Glyphosate是一种频谱广谱系统性除草剂和作物干燥剂。 2022 年的价格为每吨 1,100 美元。Glyphosate主要用于控制禾本科植物、莎草科植物和阔叶杂草。中国是世界上最大的Glyphosate生产国和出口国。中国Glyphosate产量从2010年的31.6万吨增加至2017年的约50.5万吨。 2017年,中国出口Glyphosate原药超过30万吨,满足了全球一半以上的Glyphosate需求。

- 国家的天气、杂草感染、能源价格和人事费用等因素显着影响活性成分的价格。

中国除草剂产业概况

中国除草剂市场格局适度整合,前五大企业市占率合计为64.14%。该市场的主要企业有:拜耳股份公司、科迪华农业科技、FMC集团、纽奇莫和UPL有限公司(按字母顺序排列)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 每公顷农药消费量

- 活性成分价格分析

- 法律规范

- 中国

- 价值炼和通路分析

第五章 市场区隔

- 执行模式

- 化学喷涂

- 叶面喷布

- 熏蒸

- 土壤处理

- 作物类型

- 经济作物

- 水果和蔬菜

- 粮食

- 豆类和油籽

- 草坪和观赏植物

第六章竞争格局

- 关键策略趋势

- 市场占有率分析

- 商业状况

- 公司简介(包括全球概况、市场层级概况、主要业务部门、财务状况、员工人数、关键资讯、市场排名、市场占有率、产品和服务、最新发展分析)

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Jiangsu Yangnong Chemical Co. Ltd

- Lianyungang Liben Crop Technology Co. Ltd

- Nutrichem Co. Ltd

- Rainbow Agro

- UPL Limited

- Wynca Group(Wynca Chemicals)

第七章:CEO面临的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 50001686

The China Herbicide Market size is estimated at 2.12 billion USD in 2025, and is expected to reach 2.81 billion USD by 2030, growing at a CAGR of 5.82% during the forecast period (2025-2030).

The market is driven by the need for effective control of herbicides

- Farmers in China employ various methods of herbicide application. The market for all these methods was valued at USD 1.78 billion in 2022.

- In 2022, the soil treatment method had the highest market share of USD 841.5 million, accounting for 47.2% of the total herbicide market. The popularity of soil treatment is due to its efficacy in utilizing pre-emergent herbicides, specifically targeting weed seeds, inhibiting their germination before crop sowing. With a market share of 31.9% in 2022, foliar application of herbicides offers numerous benefits in weed control. It provides precise targeting as the herbicides directly contact the weed's foliage, facilitating absorption through the leaf surfaces.

- The chemigation method grew from USD 199.4 million in 2017 to USD 339.8 million in 2022. In 2022, it was predominantly used in the grains and cereals segment, representing 52.3% of the market share. This is due to the prevalence of micro-irrigation systems in these crops, making them well-suited for chemigation.

- The foliar application offers several advantages in weed control. It provides targeted action, as the herbicides come into direct contact with the weed's foliage.

- The fumigation method of weed control is less common than other application methods due to its limited applicability attributed to its high specificity of usage and environmental concerns. However, it effectively controls a few tough weeds that other methods cannot.

- Considering the effectiveness, specificity, and essentiality of each application method for farmers, the market for herbicides is projected to register a CAGR of 6.1% during the forecast period from 2023 to 2029.

China Herbicide Market Trends

Adoption of alternative methods like crop rotation and technical advancements in herbicide application-controlled herbicide application contributes to lower consumption per hectare

- The usage of herbicides in China has reduced significantly due to several key factors. Some factors contributing to this are the growing recognition and adoption of crop rotation and biological controls as essential tools for effective weed management in various sectors, such as agriculture, horticulture, and landscaping.

- Crop rotation is a practice where different crops are grown in a specific sequence on the same land over time. This helps break the lifecycle of weeds, as different crops have different growth patterns and nutritional needs. By alternating crops, Chinese farmers have disrupted weed growth cycles, reduced weed populations, and minimized the need for higher use of herbicides.

- Chinese farmers skillfully employ biocontrol agents to effectively manage weeds in a wide array of crops, thereby leading to a notable decrease in the usage of herbicides. The implementation of these biocontrol agents is highly beneficial, resulting in reduced reliance on herbicide applications throughout various agricultural practices.

- Chinese farmers use unmanned aerial systems (UAS) imagery analysis and computer vision techniques to enhance weed management practices. By employing this approach, they identify weed-infested rows and selectively apply herbicides accurately, leaving non-weed-infested rows untouched. This innovative method effectively minimizes the wastage of herbicides by avoiding unnecessary applications and reducing overall herbicide consumption per hectare.

- Farmers adopt genetically modified organism (GMO) crops to minimize additional investment requirements, resulting in a significant reduction in herbicide consumption per hectare.

China is the world's largest producer and exporter of glyphosate

- Weeds are a major constraint to crop production, which is crucial for food security in China. Over 500 invasive weeds are an increasing threat to agricultural production and ecosystems in China. Atrazine, paraquat, and glyphosate are commonly used herbicides in China.

- Atrazine is an herbicide widely used to control various broadleaved weeds and grasses. China consumes more than 16,000 ton (97% technical) of atrazine annually. Atrazine is mainly used to control annual weeds in corn or sugarcane fields. China is one of the major suppliers of atrazine worldwide. It was priced at USD 13.7 thousand per metric ton in 2022.

- Paraquat is the active ingredient of gramoxone, which controls weeds and grasses. It is also used for desiccating crops, like cotton, before harvest. Paraquat was valued at USD 4.6 thousand per metric ton in 2022. China is a major paraquat export country, and over 80% of its paraquat output is exported to countries worldwide.

- Glyphosate is an organophosphorus broad-spectrum systemic herbicide and crop desiccant. It was priced at USD 1.1 thousand per metric ton in 2022. Glyphosate is mainly used to control weeds like grasses, sedges, and broadleaves. China is the world's largest producer and exporter of glyphosate in the world. The output of glyphosate in China increased from 316,000 ton in 2010 to about 505,000 ton in 2017. In 2017, China exported over 300,000 ton of glyphosate technical, which satisfied more than half of the global glyphosate demand.

- Factors like weather conditions, weed infestation, energy prices, and labor costs in the country majorly influence the prices of active ingredients.

China Herbicide Industry Overview

The China Herbicide Market is moderately consolidated, with the top five companies occupying 64.14%. The major players in this market are Bayer AG, Corteva Agriscience, FMC Corporation, Nutrichem Co. Ltd and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 China

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Bayer AG

- 6.4.3 Corteva Agriscience

- 6.4.4 FMC Corporation

- 6.4.5 Jiangsu Yangnong Chemical Co. Ltd

- 6.4.6 Lianyungang Liben Crop Technology Co. Ltd

- 6.4.7 Nutrichem Co. Ltd

- 6.4.8 Rainbow Agro

- 6.4.9 UPL Limited

- 6.4.10 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

苯氯林市场:依製剂类型、作物类型、施用方法、通路和最终用途划分-2026-2032年全球预测氟米龙市场:按作物类型、製剂类型、施用时间、最终用户和销售管道划分 - 全球预测 2026-2032阿尼罗磷市场:全球预测(2026-2032 年),依製剂类型、作物类型、施用方法、产品等级、通路和最终用途划分

苯氯林市场:依製剂类型、作物类型、施用方法、通路和最终用途划分-2026-2032年全球预测氟米龙市场:按作物类型、製剂类型、施用时间、最终用户和销售管道划分 - 全球预测 2026-2032阿尼罗磷市场:全球预测(2026-2032 年),依製剂类型、作物类型、施用方法、产品等级、通路和最终用途划分 吡咯烷砜市场分析及预测(至2035年):依类型、产品类型、应用、技术、最终用户、形态、产品介绍形式、材料类型及功能划分除草剂市场分析及预测(至2035年):类型、产品类型、用途、剂型、技术、最终用户、模式、功能

吡咯烷砜市场分析及预测(至2035年):依类型、产品类型、应用、技术、最终用户、形态、产品介绍形式、材料类型及功能划分除草剂市场分析及预测(至2035年):类型、产品类型、用途、剂型、技术、最终用户、模式、功能 全球除草剂市场规模、份额、趋势和成长分析报告(2026-2034年)

全球除草剂市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球不织布除草剂市场报告2026年全球除草剂市场报告按作物类型、製剂类型、製剂方式、施用时间和最终用途分類的氧氟芬技术市场,全球预测,2026-2032年

2026年全球不织布除草剂市场报告2026年全球除草剂市场报告按作物类型、製剂类型、製剂方式、施用时间和最终用途分類的氧氟芬技术市场,全球预测,2026-2032年 除草剂市场规模、份额和成长分析(按类型、作物类型和地区划分)-2026-2033年产业预测

除草剂市场规模、份额和成长分析(按类型、作物类型和地区划分)-2026-2033年产业预测

▼