|

市场调查报告书

商品编码

1937433

农业螯合物:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Agricultural Chelates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

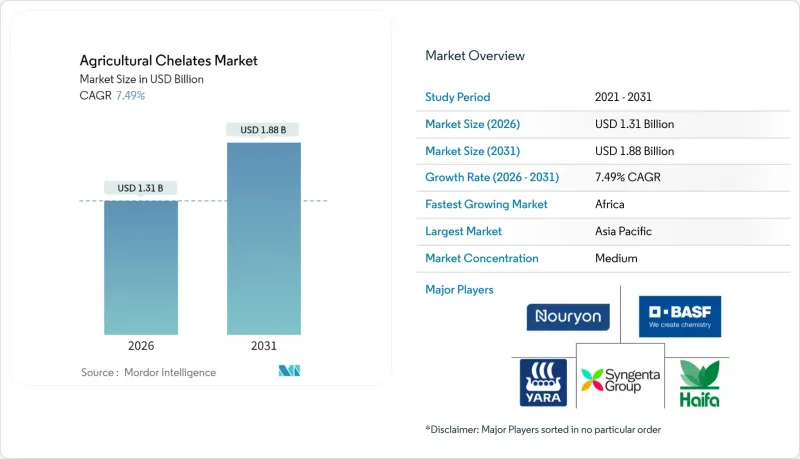

2025 年农业螯合物市场价值 12.2 亿美元,预计到 2031 年将达到 18.8 亿美元,高于 2026 年的 13.1 亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 7.49%。

市场成长的关键驱动因素包括:在耕地面积不断减少的情况下,提高作物产量的压力日益增大;精准施肥系统的日益普及;以及粮食安全需求。主要农业区的农民使用缓释螯合剂来应对锌和铁缺乏症,即使大量营养元素供应充足,锌和铁缺乏症也会导致产量下降高达50%。联合国粮食及农业组织(粮农组织)预测,2050年,灌溉耕地面积将增加3,200万公顷(11%),灌溉耕地收穫面积将扩大17%。这种扩张,尤其是在开发中国家,促使人们更加关注高效率的农业养分输送系统。欧盟对乙二胺四乙酸(EDTA)排放的更严格监管以及美国对高效肥料的45Z税额扣抵政策,正在推动对既能提高产量又能满足环境要求的可生物降解螯合剂的需求。这些监管趋势已将农业螯合物市场确立为现代作物营养策略的关键组成部分。

全球农业螯合物市场趋势及展望

全球粮食安全与耕地减少

根据联合国粮食及农业组织(粮农组织)的数据,到2050年,全球人口预计将超过90亿,届时全球粮食需求需要增加70%,而人均耕地面积却持续减少。为了应对这项挑战,农民正在使用螯合微量元素来最大限度地提高现有土地的产量。研究表明,即使氮、磷、钾供应充足,未被发现的微量元素缺乏也会导致作物减产20%至50%。螯合物透过在不同的pH值下保持金属溶解度来解决这一问题。美国温室农业的扩张推动了对高品质微量元素溶液的需求,尤其是在循环水耕系统。耕地有限、人口成长以及室内农业的扩张预计将持续推动农业螯合物市场的成长。

土壤中微量元素缺乏

土壤调查证实,超过50%的耕地缺锌,约30%的耕地缺铁,尤其是碱性或钙质土壤。在这些pH条件下,传统的硫酸盐肥料容易沉淀,限制了植物对微量金属的吸收。螯合微量元素肥料藉由保护金属离子免于沉淀,在pH 4-9的范围内保持溶解状态。每年因微量元素缺乏造成的作物损失高达150亿至200亿美元,证明了使用螯合产品保护作物产量和品质的必要性。

对合成螯合剂的严格监管

针对合成螯合剂的环境法规限制了市场成长,尤其是传统的EDTA(乙二胺四乙酸)和DTPA(二乙烯三胺五乙酸)製剂,因为它们具有环境持久性和水生毒性。根据欧盟的REACH法规,EDTA被归类为高度持久性物质,其土壤半衰期超过365天,并具有中度慢性水生毒性。加州将于2025年实施针对螯合剂的特定标籤要求,而美国环保署(EPA)的指导方针限制了饮用水中EDTA的浓度。流域监测已检测到径流中EDTA浓度高达261µg/L,导致製造商的合规成本增加。这些监管指导方针正在减少合成产品的销售量,并限制农业螯合剂市场的成长。

细分市场分析

截至2025年,合成螯合剂占农业螯合剂市占率的64.62%。乙二胺四乙酸(EDTA)对多种金属具有亲和性,而乙二胺-N,N'-双(2-羟基苯乙酸)(EDDHA)在碱性土壤中表现良好。二乙烯三胺五乙酸(DTPA)在中性pH值下具有很强的络合作用,是可控环境农业中封闭式灌溉施肥和水耕系统必不可少的螯合剂。

受永续性需求和可再生物质衍生的磺酸盐-胺基酸复合物日益普及的推动,有机螯合剂市场正以7.78%的复合年增长率成长。预计到2031年,这些市场动态将重塑农业螯合剂市场格局,合成螯合剂和有机螯合剂领域都将取得进展。为了满足生态标章标准并获得低碳融资,特种作物种植者愿意为经认证的可生物降解螯合剂支付更高的价格。农业螯合剂市场正从以销售为基础的竞争转向以环境绩效为基础的差异化竞争,这将使那些能够生产永续替代品并在pH值、温度和离子强度范围内保持稳定性的公司受益。

区域分析

预计2025年,亚太地区将占据农业螯合物市场33.45%的份额,稳居领先市场地位。在国家政策的推动下,中国引领着该地区的发展,这些政策将永续农业集约化与水质法规结合。中国地方政府为精准施肥灌溉设备提供补贴,增加了封闭式灌溉系统中对稳定螯合物的需求。印度计划于2024年推出「Agri Stack」数位代金券平台,以优化向小规模农户输送微量元素,预计这将提高预测期内每英亩螯合物的使用量。日本和澳洲凭藉先进的温室设施和出口导向园艺产业,维持对优质螯合物的稳定需求。

预计非洲的复合年增长率将达到9.88%,这主要得益于捐助者支持的土壤健康倡议以及对解决营养缺乏问题的日益重视。尼日利亚的化肥计画正向螯合剂经销商提供优惠贷款,这些分销商主要面向小规模农户;与此同时,南非的商业农场正在实施感测器控制的肥料灌溉系统,以提高用水效率。东非共同体成员国正在藉镜肯亚的数位化农业推广服务模式,培训农民识别营养缺乏症和应用螯合剂的技术。多边资金、教育倡议和扶持政策的共同作用,使非洲成为农业螯合剂市场成长最快的地区。

儘管欧洲农业用地面积较小,但由于其单位面积投入成本高,且对螯合剂的环境法规十分严格,因此仍占据着重要的市场影响力。该地区越来越倾向于选择可生物降解的螯合剂,尤其是磺酸盐和胺基酸製剂。通用农业政策(CAP)对精密农业设备投资的津贴,鼓励了螯合剂在施肥和灌溉领域的应用。有机农产品市场的不断扩张,也为符合认证要求的植物来源螯合剂创造了机会。这些因素使得欧洲即便耕地面积成长有限,仍能维持其在农业螯合剂市场中所占的较大份额。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 全球粮食安全与耕地减少

- 土壤中微量元素缺乏

- 增加营养强化作物的消费

- 一种特殊的螯合剂,特别注重与智慧施肥系统的兼容性。

- 排碳权挂钩的养分利用效率计划

- 扩大可控制环境农业

- 市场限制

- 对合成螯合剂的严格监管

- 与传统微量营养素盐相比,高成本

- 小规模农户意识水平低

- 来自生物刺激剂替代品的竞争

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按类型

- 合成

- EDTA(乙二胺四乙酸)

- EDDHA(乙二胺-N,N'-双(2-羟基苯乙酸))

- DTPA(二乙烯三胺五乙酸)

- IDHA(亚氨基二琥珀酸)

- 其他合成类型(CDTA(环己烷-1,2-二氨基四乙酸)、NTA(次氮基三乙酸)等)

- 有机的

- 磺酸盐

- 胺基酸

- 葡萄糖酸七酯

- 其他有机类型(柠檬酸盐、腐植酸/富里酸复合物等)

- 合成

- 透过使用

- 土壤

- 叶面喷布

- 施肥灌溉

- 其他用途(种子处理/种子披衣、水耕等)

- 按作物类型

- 谷物和谷类

- 豆类和油籽

- 经济作物

- 水果和蔬菜

- 草坪和观赏植物

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 北美其他地区

- 欧洲

- 西班牙

- 英国

- 法国

- 德国

- 俄罗斯

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 亚太其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Nouryon Chemicals Holding BV

- BASF SE

- Yara International ASA

- Haifa Group

- Syngenta Group(Valagro SpA)

- Mitsubishi Chemical Corporation

- BMS Micro-Nutrients NV

- ICL Group Ltd.

- Nufarm Limited

- Protex International

- Shandong IRO Chelating Chemical Co. Ltd.

- Ava Chemicals Private Limited

- Innospec Inc.

- Brandt Consolidated, Inc.

- Shiv Chem Industries

第七章 市场机会与未来展望

The agricultural chelates market was valued at USD 1.22 billion in 2025 and estimated to grow from USD 1.31 billion in 2026 to reach USD 1.88 billion by 2031, at a CAGR of 7.49% during the forecast period (2026-2031).

The market growth is driven by increasing pressure to improve crop yields from diminishing farmland, growing adoption of precision fertigation systems, and food security requirements. Farmers across major agricultural regions are using controlled-release chelate formulations to address zinc and iron deficiencies, which can reduce yields by up to 50% even with sufficient macronutrient availability. The Food and Agriculture Organization (FAO) projects that land equipped for irrigation will increase by 32 million hectares (11%) by 2050, while harvested irrigated land will expand by 17%. This expansion, especially in developing countries, has increased the emphasis on efficient agricultural nutrient delivery systems. The European Union's stricter discharge limits on EDTA (Ethylenediaminetetraacetic Acid) and the United States' 45Z tax credit for nutrient-efficient fertilizers are driving demand for biodegradable chelates that address both productivity and environmental requirements. These regulatory developments position the agricultural chelates market as an essential component of modern crop nutrition strategies.

Global Agricultural Chelates Market Trends and Insights

Global Food Security and Shrinking Arable Land

According to the Food and Agriculture Organization of the United Nations (FAO), global food demand must increase by 70% by 2050 to feed the projected world population of over 9 billion people, while per-capita arable land continues to decline. In response, agricultural producers are implementing chelated micronutrients to maximize yields on available farmland. Research demonstrates that undetected micronutrient deficiencies can reduce grain yields by 20-50%, even with adequate nitrogen, phosphorus, and potassium levels. Chelates address this issue by maintaining metal solubility across various pH levels. The expansion of greenhouse operations in the United States has increased the demand for high-quality micronutrient solutions, particularly for recirculating hydroponic systems. The combination of limited arable land, population growth, and expanding indoor farming operations continues to drive growth in the agricultural chelates market.

Micronutrient Deficiency in Soil

Soil surveys demonstrate zinc deficiencies in more than 50% of cultivated land and iron deficiencies in approximately 30% of farmland, particularly in alkaline or calcareous soils. In these pH conditions, conventional sulfates frequently precipitate, limiting trace metal availability to plants. Chelated micronutrients maintain their solubility across pH levels from 4 to 9 by protecting metal ions from precipitation. The annual crop losses due to micronutrient deficiencies amount to USD 15-20 billion, substantiating the adoption of chelated products to protect crop yields and quality.

Stringent Regulations on Synthetic Chelating Agents

Environmental regulations on synthetic chelating agents are limiting market growth, particularly affecting traditional EDTA (Ethylenediaminetetraacetic Acid) and DTPA (Diethylenetriaminepentaacetic Acid) formulations due to their environmental persistence and aquatic toxicity. The European Union's REACH dossier classifies EDTA as highly persistent, with soil half-lives exceeding 365 days, and indicates moderate chronic aquatic toxicity. California implemented chelate-specific labeling requirements in 2025, while the Environmental Protection Agency (EPA) guidelines restrict EDTA concentrations in drinking water. As watershed monitoring detects EDTA in runoff at concentrations up to 261 µg/L, manufacturers face increasing compliance costs. These regulatory guidelines reduce sales of synthetic products and constrain growth in the agricultural chelates market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Consumption of Nutritionally Fortified Crops

- Compatibility-Driven Specialty Chelates for Smart Fertigation Systems

- Higher Cost Versus Conventional Micronutrient Salts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Synthetic chelates accounted for 64.62% of the agricultural chelates market share in 2025. EDTA (Ethylenediaminetetraacetic Acid) maintains broad metal affinity, while EDDHA (Ethylenediamine-N, N'-bis(2-hydroxyphenylacetic acid)) performs well in alkaline soils. DTPA (Diethylenetriaminepentaacetic Acid) provides strong complexation at neutral pH, making it essential for closed fertigation and hydroponic systems in controlled environment agriculture.

Organic chelates are growing at an 7.78% CAGR, driven by sustainability requirements and increased adoption of lignosulfonate and amino acid complexes from renewable biomass. These market dynamics are projected to transform the agricultural chelates market through 2031, with developments occurring in both synthetic and organic segments. Specialty crop producers are willing to pay higher prices for certified biodegradable chelates to meet eco-label standards and access low-carbon financing. The agricultural chelates market is moving from volume-based competition to environmental performance differentiation, benefiting companies that can produce sustainable alternatives while maintaining stability across pH, temperature, and ionic strength ranges.

The Agricultural Chelates Market Report is Segmented by Type (Synthetic and Organic), by Application (Soil, Foliar, Fertigation, and Other Applications), by Crop Type (Grains and Cereals, Pulses and Oilseeds, Commercial Crops, Fruits and Vegetables, and Turf and Ornamentals), and by Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 33.45% of the agricultural chelates market share in 2025, establishing itself as the primary market for agricultural chelates. China leads the region, driven by national policies that combine sustainable agricultural intensification with water quality regulations. The country's provincial governments offer subsidies for precision fertigation equipment, increasing the demand for stable chelates in closed irrigation systems. India's implementation of the Agri Stack digital voucher platform in 2024 is optimizing micronutrient distribution to small-scale farmers, which is anticipated to increase chelate usage per acre during the forecast period. Japan and Australia maintain consistent premium demand through their advanced greenhouse facilities and export-oriented horticulture.

Africa demonstrates a 9.88% forecast CAGR, driven by donor-supported soil health initiatives and increased focus on addressing nutritional deficiencies. Nigeria's fertilizer program provides concessional loans to chelate distributors serving small-scale farmers, while South African commercial farms implement sensor-guided fertigation to optimize water usage. East African Community members are adopting Kenya's digital extension services model to educate farmers about deficiency identification and chelate application. The combination of multilateral funding, educational initiatives, and supportive policies establishes Africa as the fastest-growing region in the agricultural chelates market.

Europe maintains significant market influence despite its smaller agricultural area, due to high per-hectare input investments and stringent environmental regulations for chelates. The region shows increasing preference for biodegradable options, particularly lignosulfonates and amino acid formulations. The Common Agricultural Policy's investment grants for precision agriculture equipment are driving the adoption of fertigation-specific chelates. The growing organic produce market creates opportunities for plant-based chelation agents that meet certification requirements. These factors help Europe maintain a substantial share in the agricultural chelates market despite limited growth in cultivated area.

- Nouryon Chemicals Holding B.V.

- BASF SE

- Yara International ASA

- Haifa Group

- Syngenta Group (Valagro S.p.A)

- Mitsubishi Chemical Corporation

- BMS Micro-Nutrients NV

- ICL Group Ltd.

- Nufarm Limited

- Protex International

- Shandong IRO Chelating Chemical Co. Ltd.

- Ava Chemicals Private Limited

- Innospec Inc.

- Brandt Consolidated, Inc.

- Shiv Chem Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Global Food Security and Shrinking Arable Land

- 4.2.2 Micronutrient Deficiency in Soil

- 4.2.3 Rising Consumption of Nutritionally Fortified Crops

- 4.2.4 Compatibility-Driven Specialty Chelates for Smart Fertigation Systems

- 4.2.5 Carbon-Credit-Linked Nutrient-Use-Efficiency Programs

- 4.2.6 Expansion of Controlled Environment Agriculture

- 4.3 Market Restraints

- 4.3.1 Stringent Regulations on Synthetic Chelating Agents

- 4.3.2 Higher Cost Versus Conventional Micronutrient Salts

- 4.3.3 Limited Awareness Among Smallholder Farmers

- 4.3.4 Competition from Bio-Stimulant Alternatives

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Synthetic

- 5.1.1.1 EDTA (Ethylenediaminetetraacetic Acid)

- 5.1.1.2 EDDHA (Ethylenediamine-N,N'-bis(2-hydroxyphenylacetic acid))

- 5.1.1.3 DTPA (Diethylenetriaminepentaacetic Acid)

- 5.1.1.4 IDHA (Iminodisuccinic Acid)

- 5.1.1.5 Other Synthetic Types (CDTA (Cyclohexane-1,2-diaminetetraacetic Acid), NTA (Nitrilotriacetic Acid), etc.)

- 5.1.2 Organic

- 5.1.2.1 Lignosulfonates

- 5.1.2.2 Amino acids

- 5.1.2.3 Heptagluconates

- 5.1.2.4 Other Organic Types (Citrates, Humic and Fulvic Acid Complexes, etc.)

- 5.1.1 Synthetic

- 5.2 By Application

- 5.2.1 Soil

- 5.2.2 Foliar

- 5.2.3 Fertigation

- 5.2.4 Other Applications (Seed Treatment/Seed Coating, Hydroponics, etc.)

- 5.3 By Crop Type

- 5.3.1 Grains and Cereals

- 5.3.2 Pulses and Oilseeds

- 5.3.3 Commercial Crops

- 5.3.4 Fruits and Vegetables

- 5.3.5 Turfs and Ornamentals

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Spain

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Germany

- 5.4.2.5 Russia

- 5.4.2.6 Italy

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Nigeria

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Nouryon Chemicals Holding B.V.

- 6.4.2 BASF SE

- 6.4.3 Yara International ASA

- 6.4.4 Haifa Group

- 6.4.5 Syngenta Group (Valagro S.p.A)

- 6.4.6 Mitsubishi Chemical Corporation

- 6.4.7 BMS Micro-Nutrients NV

- 6.4.8 ICL Group Ltd.

- 6.4.9 Nufarm Limited

- 6.4.10 Protex International

- 6.4.11 Shandong IRO Chelating Chemical Co. Ltd.

- 6.4.12 Ava Chemicals Private Limited

- 6.4.13 Innospec Inc.

- 6.4.14 Brandt Consolidated, Inc.

- 6.4.15 Shiv Chem Industries

7 Market Opportunities and Future Outlook

农业螯合剂市场-2026-2031年预测

农业螯合剂市场-2026-2031年预测 农业螯合剂市场规模、份额和成长分析(按类型、作物类型、微量元素类型、应用方法、应用领域和地区划分)-2026-2033年产业预测

农业螯合剂市场规模、份额和成长分析(按类型、作物类型、微量元素类型、应用方法、应用领域和地区划分)-2026-2033年产业预测 按微量营养素类型、作物类型、应用方法、剂型和最终用户分類的农业螯合物市场—2025-2032年全球预测

按微量营养素类型、作物类型、应用方法、剂型和最终用户分類的农业螯合物市场—2025-2032年全球预测 全球农业螯合剂市场报告(2025年)

全球农业螯合剂市场报告(2025年) 2025-2033年农业螯合物市场报告(按类型、作物类型、应用和地区)

2025-2033年农业螯合物市场报告(按类型、作物类型、应用和地区) 农业用螫合物的全球市场:实际成果与预测(2019年~2030年)

农业用螫合物的全球市场:实际成果与预测(2019年~2030年) 2030 年农业螯合物市场预测:按类型、作物类型、微量营养素类型、应用、最终用户和地区进行的全球分析全球农业螯合物市场:到 2033 年的机会与策略

2030 年农业螯合物市场预测:按类型、作物类型、微量营养素类型、应用、最终用户和地区进行的全球分析全球农业螯合物市场:到 2033 年的机会与策略