|

市场调查报告书

商品编码

1685812

铍:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Beryllium - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

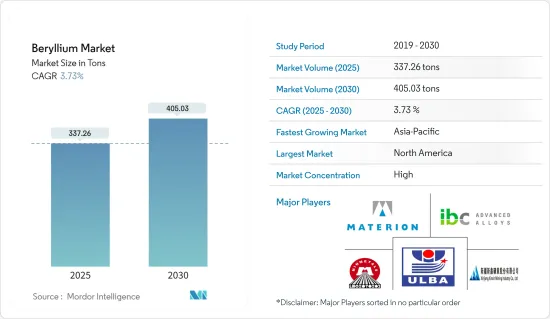

预计 2025 年铍市场规模为 337.26 吨,到 2030 年将达到 405.03 吨,预测期间(2025-2030 年)的复合年增长率为 3.73%。

受新冠疫情影响,铍市场遭遇挫折。全球停工和严格的政府监管已导致大面积生产关闭。不过,预计市场将在 2021 年復苏,并在未来几年内实现显着成长。

主要亮点

- 短期内,电子和通讯基础设施需求的不断增长以及铍合金在航太和军事应用中的广泛使用将推动市场需求。

- 然而,预计潜在替代品的竞争将阻碍市场成长。

- 然而,未来核能发电对氧化铍的需求和铍镜的新兴应用预计将为研究市场创造新的机会。

- 预计北美将主导全球市场,大部分需求来自美国和加拿大。

铍市场趋势

电子和通讯领域占据市场主导地位

- 消费性电子和通讯是铍的主要终端用户产业。铍主要与铜形成合金,形成铜铍合金。这些合金用于各种产品,包括电缆、高清晰度电视(HDTV)、电触点、行动电话和电脑中的连接器、电脑晶片的散热器、水下光缆、插座、恆温器和波纹管。

- 铍的优异导热性可增加散热能力,降低过热风险并增强电子元件的可靠性。

- 随着感测器、天线、电容器和电阻器等电子元件变得越来越小、功能越来越强大,铍在这一不断发展的领域中的重要性变得更加突出。

- 电子产业是世界上规模最大、成长最快的产业之一。在当今数位时代,电子设备对人们的生活产生着巨大的影响。预计电子产品的需求将持续成长,并继续成为全球重要的经济驱动力。

- 根据电子情报技术产业协会(JEITA)的资料,2023年全球电子及IT产业规模预计为3.3826兆美元,与前一年同期比较下降3%。不过,预计市场将出现復苏,到 2024 年将成长 9%,达到 36,868 亿美元。

- 印度是继中国之后的第二大智慧型手机製造国。据印度投资局称,印度的目标是到 2025-26 年生产价值 1,260 亿美元的行动电话。全球范围内,智慧型手机的需求正在大幅成长。据 Telefonaktiebolaget LM Ericsson 称,到 2027 年,智慧型手机用户数量预计将达到 76.9 亿部,从电子应用角度研究的市场利用率将不断提高。

- 在美国,快速的技术进步和强劲的研发活动正在推动对尖端电子产品的需求。该行业正在经历持续而显着的发展。根据美国消费科技协会的报告,2023年美国消费性电子产品销售的零售收入将达到4,850亿美元,预计2024年将达到5,120亿美元。

- 德国拥有欧洲最大的电子产业。根据德国电气电子工业协会(ZVEI)的资料,该产业的总销售收入预计将在2023年达到2,381亿欧元(约2,580.6亿美元)。全球消费性电器产品市场的主要驱动力包括技术进步、快速的都市化、蓬勃发展的住宅行业、人均收入的增加、生活水准的提高、对居家舒适度的日益重视、消费者生活方式的演变以及小型家庭数量的增加。

- 这些趋势预计将增加对电子设备和通讯的需求,进而推动对铍的需求。

北美占据市场主导地位

- 预计北美将引领铍市场,并将成为预测期内成长最快的地区。这种快速成长主要归因于汽车、医疗保健、航太和国防、石油和天然气、电子和通讯等领域的需求不断增长,尤其是在美国和加拿大。

- 根据美国地质调查局的数据,美国是世界上最大的铍矿产生产国,到 2023 年产量将达到 190 吨,高于 2022 年的 175 吨。

- 约 60% 的铍矿资源位于美国,主要分布在犹他州斯帕尔山地区,该地区含有包括大型铍石源在内的錶壳层矿床。犹他州已探明和可能的铍石蕴藏量估计含有约蕴藏量吨铍。

- 铍被用于汽车工业,因为其优异的导热性、强度和耐腐蚀性使其成为各种应用的理想材料,包括煞车盘、点火器开关、安全气囊感知器、动力传动系统总成部件和电气部件。随着该地区汽车产量的增加,对铍的需求也预计将增加。

- 美国拥有仅次于中国的世界第二大汽车产业,在区域和全球市场中发挥着至关重要的作用。根据国际汽车製造商组织(OICA)的资料,预计2023年美国汽车产量将达到10,611,555辆,较2022年增长5.56%,这将推动对铍的需求。

- 根据加拿大汽车工业协会的报告,汽车产业为加拿大的GDP贡献了190多亿美元。根据预测,到 2024 年,这项贡献将增加到 401 亿美元,为铍市场创造成长机会。根据OICA资料,2023年加拿大汽车产量将为1,553,026辆,与前一年同期比较增长25.92%。

- 铍的高热导率和出色的强度重量比使其在航太和国防领域极为重要。它用于高速飞机、飞弹和火箭发动机的喷嘴。该地区不断扩大的航太和国防部门预计将增加对铍的需求。

- 美国拥有北美最大的航空市场,并拥有世界上最大的飞机持有之一。航太零件向法国、中国和德国等国家的强劲出口,正在促进该行业的製造活动,从而对铍市场产生积极影响。

- 根据美国联邦航空管理局(FAA)的数据,受航空旅行和货运需求大幅復苏的推动,民航机队在2022-23年增长了0.2%。此外,预计未来 20 年美国航空客运量每年将成长 2.4%,从 2023 年的 9,220 亿美元达到 2044 年的 1.32 兆美元,而美国干线喷射机持有将从 2023 年的 4,832 架成长到 20494 年的 6,84 架。

- 在电子领域,铍的高热导率和非磁性使其成为电接触、半导体和通讯的必需材料。随着该地区电子产业的发展,预计未来几年对铍的需求将会成长。

- 美国电子产业正处于温和的成长轨迹,这得益于对先进技术产品的需求激增以及强劲的研发活动所推动的快速技术创新。

- 2024 年 4 月,根据拜登总统的两党基础设施立法,能源部 (DOE) 宣布计划投资高达 3.31 亿美元建设新的输电线路,优先考虑工会劳动力。此外,我的政府正在主导倡议,与公共和私营部门领导人合作,加强国家电网,目标是在未来五年内升级10万英里的输电线路。

- 铍具有高强度和电导性,广泛应用于石油和天然气领域,从井下油管到压缩机和发电机。随着该地区石油和天然气行业的扩张,未来几年对铍的需求预计会增加。

- 加拿大统计局称,2023年加拿大原油产量将连续第三年增加,与前一年同期比较增加1.4%,达2.864亿立方公尺。此外,加拿大能源承包商协会预测,2024 年将钻探 6,229 口油井,比 2023 年增加 481 口,这表明油砂生产商正处于扩张阶段。

- 鑑于这些发展,预测期内北美对铍的需求将会激增。

铍行业细分

铍市场高度整合。主要企业有Materion公司、乌尔巴冶金厂(哈萨克原工业股份公司)、湖南水口山有色金属集团、IBC先进合金、新疆新鑫矿业等。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 电子和通讯基础设施需求不断增长

- 由于性能优异,在医疗设备中的应用日益广泛

- 其他驱动因素

- 限制因素

- 与替代品的竞争

- 其他限制因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场区隔

- 产品类型

- 合金

- 金属

- 陶瓷

- 其他产品类型

- 最终用户产业

- 工业部件

- 车

- 卫生保健

- 航太和国防

- 石油和天然气

- 电子和通讯

- 其他最终用户产业

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 土耳其

- 俄罗斯

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 卡达

- 阿拉伯聯合大公国

- 奈及利亚

- 埃及

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作、协议

- 市场占有率**/排名分析

- 主要企业策略

- 公司简介

- American Beryllia Inc.

- American Elements

- Belmont Metals

- Hunan Shuikoushan Nonferrous Metals Group Co. Ltd

- IBC Advanced Alloys

- Materion Corporation

- NGK Metals

- Texas Mineral Resources Corp.

- Tropag Oscar H. Ritter Nachf GmbH

- Ulba Metallurgical Plant(kazatomprom)

- Xiamen Beryllium Copper Technologies Co. Ltd

- Xinjiang Xinxin Mining Industry Co. Ltd

第七章 市场机会与未来趋势

- 未来核能发电。

- 铍镜的新应用

- 其他机会

The Beryllium Market size is estimated at 337.26 tons in 2025, and is expected to reach 405.03 tons by 2030, at a CAGR of 3.73% during the forecast period (2025-2030).

The beryllium market faced setbacks due to COVID-19. Global lockdowns and stringent government regulations led to widespread shutdowns of production hubs. However, the market rebounded in 2021, and it is estimated to witness significant growth in the upcoming years.

Key Highlights

- Over the short term, the growing demand from electronics and telecommunication infrastructure and extensive usage of beryllium alloys in aerospace and military applications drive the market's demand.

- However, competition from potential alternatives is expected to hinder the market's growth.

- Nevertheless, future demand for beryllium oxide in nuclear power generation and emerging applications of beryllium mirrors are expected to create new opportunities for the market studied.

- North America is expected to dominate the global market, with the majority of demand coming from the United States and Canada.

Beryllium Market Trends

Electronics and Telecommunications Segment to Dominate the Market

- Consumer electronics and telecommunications stand out as key end-user industries for beryllium. Beryllium is predominantly alloyed with copper in these applications, forming copper-beryllium alloys. These alloys find their way into various products, including cables, high-definition televisions, electrical contacts, cell phone and computer connectors, computer chip heat sinks, underwater fiber optic cables, sockets, thermostats, and bellows.

- Beryllium's excellent thermal conductivity enhances heat dissipation, mitigating overheating risks and bolstering the reliability of electronic components.

- As electronic components like sensors, antennas, capacitors, and resistors shrink and gain capabilities, beryllium's significance in this evolving landscape becomes even more pronounced.

- The electronics industry is one of the world's largest and fastest growing. In the current digital era, electronic items significantly impact people's lives. The demand for electronic gadgets is projected to rise continuously and remain a significant economic driver globally.

- As per data from the Japan Electronics and Information Technology Industries Association (JEITA), the global electronics and IT industry saw a 3% year-over-year decline in 2023, totaling USD 3,382.6 billion. However, a rebound is anticipated, with projections of a 9% growth in 2024, reaching USD 3,686.8 billion.

- India is the second largest smartphone producer after China. As per Invest India, the country aims to manufacture cell phones worth USD 126 billion by 2025-26. Globally, the demand for smartphones is increasing at a significant rate. According to the Telefonaktiebolaget LM Ericsson, the subscription is likely to reach 7,690 million by 2027, enhancing the usage of the market studied from electronics applications.

- In the United States, swift technological advancements and robust R&D activities fuel a demand for cutting-edge electronic products. The industry is witnessing continuous and significant progress. The Consumer Technology Association reports that retail revenue from US consumer electronics sales reached an impressive USD 485 billion in 2023, with projections for 2024 set at USD 512 billion.

- Germany boasts the largest electronics industry in Europe. Data from the Germany Electrical and Electronics Association (ZVEI) indicates that the sector achieved an aggregated turnover of EUR 238.1 billion (approximately USD 258.06 billion) in 2023. Key drivers for the global household appliances market include technological advancements, rapid urbanization, a booming housing sector, rising per capita income, enhanced living standards, a growing emphasis on comfort in household chores, evolving consumer lifestyles, and an increasing number of smaller households.

- Given these dynamics, the demand for electronics and telecommunications is set to rise, subsequently fueling the demand for beryllium.

North America to Dominate the Market

- North America is poised to lead the beryllium market, emerging as the region with the fastest growth during the forecast period. This surge is primarily fueled by increasing demands across various sectors, including automotive, healthcare, aerospace and defense, oil and gas, and electronics and telecommunications, particularly in the United States and Canada.

- As per the US Geological Survey, the United States was the world's largest beryllium mine producer, with production amounting to 190 metric tons in 2023, growing from 175 tons in 2022.

- About 60% of beryllium resources are in the United States, mainly in the Spor Mountain area in Utah, where the epithermal deposit contains a large bertrandite source. Proven and probable bertrandite reserves in Utah are estimated at about 20,000 tons of contained beryllium.

- Beryllium is used in the automotive industry due to its high thermal conductivity, strength, and resistance to corrosion, making it an ideal material for various applications, including brake discs, ignition switches, airbag sensors, powertrain components, and electrical components. As vehicle production rises in the region, the demand for beryllium is expected to bolster.

- The United States boasts the world's second-largest automotive industry, trailing only China, and plays a pivotal role in regional and global markets. Data from the Organisation Internationale des Constructeurs Automobiles (OICA) indicates that the US automotive production reached 10,611,555 units in 2023, marking a 5.56% increase from 2022, bolstering the demand for beryllium.

- As reported by the Automotive Industries Association of Canada, the automotive sector contributes over USD 19 billion to Canada's GDP. Projections suggest this contribution will rise to USD 40.1 billion in 2024, presenting growth opportunities for the beryllium market. OICA data shows Canada produced 1,553,026 vehicles in 2023, a 25.92% increase from the prior year.

- Beryllium's high thermal conductivity and exceptional strength-to-weight ratio render it crucial in aerospace and defense. It is employed in high-speed aircraft, missiles, and rocket engine nozzles. With the aerospace and defense sector expanding in the region, the demand for beryllium is set to rise.

- The United States has the largest aviation market in North America and boasts one of the world's most extensive fleet sizes. Strong exports of aerospace components to nations like France, China, and Germany are propelling the industry's manufacturing activities, positively influencing the beryllium market.

- According to the Federal Aviation Administration (FAA), boosted by the sharp recovery in demand for air travel and cargo, the number of aircraft in the commercial fleet grew by 0.2% in 2022-23. Additionally, US airline enplanements are estimated to grow 2.4% per year over the next 20 years to USD 1.32 trillion in 2044 compared to USD 922 billion in 2023, and projects the US mainline jet fleet to grow from 4,832 in 2023 to 6,894 in 2044.

- In electronics, beryllium's high thermal conductivity and non-magnetic properties are essential for electrical contacts, semiconductors, and telecommunications. As the electronics sector grows in the region, the demand for beryllium is expected to grow in the coming years.

- The US electronics sector is on a moderate growth trajectory, driven by a surge in demand for advanced technological products and rapid innovation spurred by robust R&D activities.

- The Department of Energy (DOE), in April 2024, announced plans to invest up to USD 331 million in a new transmission line, prioritizing union labor, under President Biden's Bipartisan Infrastructure Law. Additionally, the administration is leading an initiative by collaborating with public and private sector leaders to enhance the nation's transmission network, aiming to upgrade 100,000 miles of transmission lines in the next five years.

- With its high strength and conductivity, beryllium finds applications in the oil and gas sector, from down-hole tubing to compressors and generators. With the expanding oil and gas sector in the region, the demand for beryllium is set to rise in the coming years.

- Statistique Canada reports that Canada's crude oil production rose for the third consecutive year in 2023, hitting 286.4 million cubic meters, a 1.4% increase from the previous year. Moreover, with projections from the Canadian Association of Energy Contractors anticipating 6,229 wells to be drilled in 2024, up 481 from 2023, it is evident that oil sand producers are in an expansion phase.

- Given these dynamics, North America is poised for a surge in beryllium demand during the forecast period.

Beryllium Industry Segmentation

The beryllium market is highly consolidated. The major players include Materion Corporation, Ulba Metallurgical Plant (Kazatomprom), Hunan Shuikoushan Nonferrous Metals Group Co. Ltd, IBC Advanced Alloys, and Xinjiang Xinxin Mining Industry Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from Electronics and Telecommunication Infrastructure

- 4.1.2 Increasing Usage in Medical Equipment Owing to its Superior Properties

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Competition from Potential Alternatives

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Product Type

- 5.1.1 Alloys

- 5.1.2 Metals

- 5.1.3 Ceramics

- 5.1.4 Other Product Types

- 5.2 End-user Industry

- 5.2.1 Industrial Components

- 5.2.2 Automotive

- 5.2.3 Healthcare

- 5.2.4 Aerospace and Defense

- 5.2.5 Oil and Gas

- 5.2.6 Electronics and Telecommunication

- 5.2.7 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share **/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 American Beryllia Inc.

- 6.4.2 American Elements

- 6.4.3 Belmont Metals

- 6.4.4 Hunan Shuikoushan Nonferrous Metals Group Co. Ltd

- 6.4.5 IBC Advanced Alloys

- 6.4.6 Materion Corporation

- 6.4.7 NGK Metals

- 6.4.8 Texas Mineral Resources Corp.

- 6.4.9 Tropag Oscar H. Ritter Nachf GmbH

- 6.4.10 Ulba Metallurgical Plant (kazatomprom)

- 6.4.11 Xiamen Beryllium Copper Technologies Co. Ltd

- 6.4.12 Xinjiang Xinxin Mining Industry Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Future Demand for Beryllium Oxide in Nuclear Power Generation

- 7.2 Emerging Applications of Beryllium Mirrors

- 7.3 Other Opportunities

氢氧化铍市场规模、份额及成长分析(依等级、应用、最终用户及地区划分)-2026-2033年产业预测

氢氧化铍市场规模、份额及成长分析(依等级、应用、最终用户及地区划分)-2026-2033年产业预测 全球铍市场-2025-2030年预测

全球铍市场-2025-2030年预测 全球铍矿开采市场:市场规模、份额、趋势分析(按应用、最终用途和地区划分)、细分市场预测(2025-2033年)

全球铍矿开采市场:市场规模、份额、趋势分析(按应用、最终用途和地区划分)、细分市场预测(2025-2033年) 铍市场按产品类型、最终用途产业、形态、纯度和应用划分-2025-2032年全球预测

铍市场按产品类型、最终用途产业、形态、纯度和应用划分-2025-2032年全球预测 铍市场规模、份额、成长分析(按等级、按应用、按形式、按纯度等级、按地区)-2025-2032 年产业预测

铍市场规模、份额、成长分析(按等级、按应用、按形式、按纯度等级、按地区)-2025-2032 年产业预测 2032 年铍市场预测:按产品、形态、应用和地区分類的全球分析

2032 年铍市场预测:按产品、形态、应用和地区分類的全球分析 2025-2033年铍市场报告(依产品类型、最终用途产业和地区)

2025-2033年铍市场报告(依产品类型、最终用途产业和地区) 铍全球市场2024-2028

铍全球市场2024-2028