|

市场调查报告书

商品编码

1685817

毫米波技术-市场占有率分析、产业趋势与统计、成长预测(2025-2031)Millimeter Wave Technology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

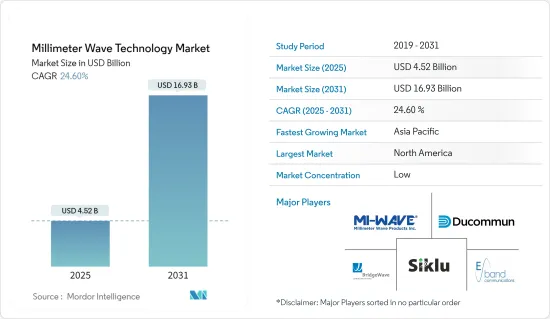

毫米波技术市场规模预计在 2025 年为 45.2 亿美元,预计到 2031 年将达到 169.3 亿美元,预测期内(2025-2031 年)的复合年增长率为 24.6%。

主要亮点

- 该技术将满足连网家庭、AR/VR 设备、云端游戏系统和其他云端连接设备的资料需求的大幅增长。此外,50 GHz 以上的毫米波频宽可以以大而重的区块形式提供额外的 20 GHz 或更多频宽,从而实现更高的资料速率。一些传统无线电频宽,尤其是 26 GHz 和 28 GHz,对于回程传输来说前景不明朗,因为它们目前的目标是 5G 无线存取。 ETSI mWT ISG 已经表示担心,在为 5G 分配毫米波频谱时,需要考虑营运商继续运行其 3G 和 4G 网路回程传输的能力。

- 由于频率再生性和宽通道频宽等优势,毫米波频段的使用正在增加,这使得毫米波和亚毫米波频段非常适合 5G 增强行动宽频所需的高容量。因此,在接取网路中使用毫米波频段来提高用户设备吞吐量和基地台回程传输正在推动对毫米波技术的需求。

- 预计预测期内市场将以温和的速度成长。政府部署 5G 的倡议以及物联网和智慧城市等新技术的进步正在鼓励市场参与者开发新服务/解决方案以占领市场占有率。

- 从 4G 到 5G 的过渡推动了对毫米波频宽的需求,毫米波频段具有更宽的频宽和更快的资料速率,从而推高了生产成本。这些大批量零件的零件和劳动成本不断上涨,迫使製造商重新评估自动化零件测试的经济性。

- 对相容毫米波组件的需求迫使製造商投入大量资金。 mmWave 5G 设备的製造和销售成本要高得多。部署足够多的毫米波小型基地台以覆盖整个城市的挑战预计将减缓近年来的市场采用速度。

毫米波技术的市场趋势

天线和收发器部分占据了很大的市场占有率

- 高性能毫米波设备需要高效率、低剖面的天线来确保可靠、无干扰的通讯。由于波长较小,毫米波技术基础设施需要将大型天线阵列封装在较小的实体尺寸内,这推动了针对毫米波 (mm) 技术设计的天线和收发器的需求,并推动了市场成长。

- 毫米波技术的高资料传输支援各种应用,包括即时游戏、高清视讯串流和其他频宽应用,这些应用需要天线和收发器来中继和转换讯号,从而对毫米波技术的微带、片上整合喇叭、透镜、反射器和其他天线产生了需求。

- 根据 GSMA 最近发布的报告,预计到 2030 年,5G 应用程式将达到约 10 亿个连线。该技术将支撑未来的行动创新并推动持续部署,并可能在 2030 年为全球经济增加约 1 兆美元。根据该报告,到 2023 年,非洲和亚洲将有 30 个新市场推出 5G 服务。随着 5G 部署的不断扩大,网路营运商正在加紧努力扩展 5G 固定无线存取 (FWA) 服务。固定宽频普及率较低且收入不断增长的市场也将迎来高于平均的 5G 成长。

- 市场供应商正在采取策略性倡议,扩大产品系列,以占领相当大的市场占有率。例如,2023 年 10 月,马来西亚 5G 网路营运商 DNB(Digital Nasional Berhad)与马来西亚电信™ 和中国供应商中兴通讯股份有限公司合作,进行 5G 即时试验,达到高达 28Gbps 的速度。中兴通讯表示,此次伙伴关係预计将利用马电讯现有的网路基础设施、数位专业知识和中兴通讯的毫米波有源天线单元,为马来西亚下一代传输网路提供首个独立的 5G 核心。

- 2023年8月,射频和微波产品供应商Marki Microwave收购了亚太地区赫兹波导技术供应商Precision Millimeter Wave LLC的波导业务。 Marki Microwave 将提供 100 多种标准商用波导产品,包括天线、连接器、开关和隔离器,以及从毫米波到亚太赫兹的多种自订波导产品。

- 各种终端用户应用对高速通讯的需求、对相控天线和毫米波通讯高性能收发器的需求正在刺激市场的成长,而毫米波技术市场相关人员的收购、投资和合作则为市场的成长提供了支持。

预计北美将占据较大的市场占有率

- 美国在利用毫米波频谱进行各种应用方面取得了长足的进展。联邦通讯委员会 (FCC) 等监管机构负责分配和竞标毫米波频宽以供授权和未授权使用。具体来说,FCC已经向5G和其他无线通讯技术开放了28GHz、37GHz、39GHz和47GHz频段的频率。

- 美国5G 网路的推出正在推动毫米波技术的采用。此外,总部位于亚利桑那州的网路测试和测量公司 Viavi Solutions 表示,美国是全球采用网路存取的城市最多的国家之一。

- 例如,截至2023年4月,美国约有503个城市已采用5G网路存取。排名第二的是中国,5G涵盖356个城市。因此,毫米波频率正在成为 5G 部署的关键组成部分,尤其是对于都市区的高速、低延迟 5G 网路而言。通讯公司正在积极推出包括毫米波频率在内的 5G 基础设施,以实现超快的互联网速度并支援扩增实境(AR)、虚拟实境 (VR) 和物联网等新兴用例。

- 根据CTIA(2023年7月)的报导,美国是全球5G部署领先的国家,并且比其他任何国家都拥有更多的5G接入。 5G 响应速度更快的网路和速度将推动企业和消费者的强劲采用。无线产业正在提前推出 5G,利用创纪录的资本和全球最高额度的资本,以比以往任何一代无线技术更快的速度推出 5G。

- 预计5G最终将为国内经济增加1.5兆美元,并创造新的就业(至少450万个)。美国5G网路目前已覆盖超过3.25亿人,是全球覆盖率最高的5G网路。 Ookla 认为美国是全球无障碍领域的领导者,超过 54% 的 5G 装置连接已连接到 5G 网路。

- 加拿大在利用毫米波频谱实现多种用途方面取得了长足进步。加拿大创新、科学和经济发展部 (ISED) 等监管机构为许可和未许可用途分配毫米波频率并管理其使用。 26GHz、28GHz、38GHz 和其他频宽的频率对于毫米波应用来说是重要的资产。

- 此外,该国对 5G 网路的需求日益增长,5G 网路利用毫米波频率来提供超快的网路速度和低延迟。例如,爱立信的一份报告发现,截至 2022 年 11 月,400 万加拿大智慧型手机用户表示打算在未来 12 到 15 个月内升级到 5G 服务。此外,只有三分之一的加拿大 5G 用户认为他们超过 50% 的时间都连接到网络,45% 的用户仍然表示他们担心覆盖范围。这些重大问题预计将导致人们关注在毫米波频谱中部署更高频率的无线电波,以满足日益增长的需求。

毫米波技术市场概况

mmWave 技术市场分散,主要参与者包括 Siklu Communication Ltd(Ceragon Networks Ltd)、Bridgewave Communications Inc(Remec Broadband Wireless International)、E-band Communications LLC(Axxcss Wireless Solutions Inc)、Millimeter Wave Products Inc. 和 Ducommun Incorporated。市场上的公司正在采取联盟和收购等策略来加强其产品供应并获得永续的竞争优势。

- 2023 年 12 月 - Eravant(SAGE Millimeter Inc.)获得了一项新型电连接器系列专利,该系列可用于快速增长的毫米波电子领域。该专利设备与现有的同轴介面相容。 Uni-Guide 波导连接器可协助组件製造商以更少的封装设计提供各种波导尺寸和方向。

- 2023 年 8 月 - Sikul 是一家为数位城市和Gigabit无线接入 (GWA) 提供毫米波 (mmWave) 解决方案的全球供应商,推出了其新的 MultiHaul TG T261 终端单元。 T261 是 Sicuru MultiHaul TG 系列的第四个新成员,该系列主要为点对多点 60GHz 产品,并通过了 Terragraph (TG) 认证。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

- COVID-19 产业影响评估

- GaN 在毫米波应用的重要性

- 毫米波基板概况(包括 LCP、PI 和 PTFE 等毫米波基板及其对基地台、电话和周边设备等 5G 基础设施的影响)

第五章市场动态

- 市场驱动因素

- 基地台无线回程传输的普及

- 5G演进可望推动市场

- 市场挑战/限制

- 製造可互换零件的需求和零件成本的上升

- 降低讯号强度的技术漏洞

第六章市场区隔

- 依组件类型

- 天线和收发器

- 通讯和网路

- 介面

- 频率及相关零件

- 影像学

- 其他组件

- 按许可模式

- 全部/部分许可

- 未经许可

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 亚洲

- 中国

- 日本

- 印度

- 韩国

- 中东和非洲

- 拉丁美洲

- 北美洲

第七章竞争格局

- 公司简介

- Siklu Communication Ltd(Ceragon Networks Ltd)

- Bridgewave Communications Inc.(REMEC Broadband Wireless Networks LLC)

- E-band Communications LLC(Axxcss Wireless Solutions Inc.)

- Millimeter Wave Products Inc.

- Ducommun Incorporated

- Eravant(SAGE Millimeter Inc.)

- Keysight Technologies Inc.

- Farran Technology Ltd

- Smiths Interconnect Group Limited

- NEC Corporation

- L3Harris Technologies Inc.

第八章投资分析

第九章 市场机会与未来趋势

The Millimeter Wave Technology Market size is estimated at USD 4.52 billion in 2025, and is expected to reach USD 16.93 billion by 2031, at a CAGR of 24.6% during the forecast period (2025-2031).

Key Highlights

- The technology accommodates the massive increase in data demands from connected homes, AR/VR devices, cloud gaming systems, and other cloud-connected devices. Furthermore, mmWave bands above 50 GHz can provide over 20 GHz additional bandwidth in large, heavy chunks, allowing higher data rates. Some traditional wireless bands, notably 26 GHz and 28 GHz, have an uncertain future for backhaul since they are now targeted for 5G radio access. ETSI's mWT ISG already expressed concern regarding the need, while allocating mmWave bands for 5G, to consider operators' ability to continue operating the backhaul for their 3G and 4G networks.

- The rising use of millimeter-wave bands, owing to the advantages such as frequency re-usability and large channel bandwidths, make millimeter-wave and sub-millimeter, suitable for the high capacities required by 5G enhanced Mobile Broadband. Thus, the use of millimeter-wave bands for the access networks to increase the throughput of the User Equipment and backhaul of the base stations is adding demand for Millimeter Wave Technology.

- The market is expected to grow moderately during the forecasted period. The government initiatives toward the deployment of 5G and advancement in new technologies like IoT and smart cities are pushing the market players to develop new services/solutions to capture the market share.

- Migration from 4G to 5G has increased the demand for mmWave bands with wider bandwidths and high-speed data rates, increasing manufacturing costs. These higher costs for components and operations in high-volume manufacturing parts have forced manufacturers to rethink the economics of automated component testing.

- Demands for compatible millimeter wave components are adding substantial expense to manufacturers. mmWave 5G devices are substantially expensive to produce and sell. The challenge of deploying enough of the mmWave small cells to cover entire cities is anticipated to slow down market adoption in recent years.

Millimeter Wave Technology Market Trends

Antennas and Transceivers Segment Holds Significant Market Share

- High-performing millimeter-wave devices require efficient low-profile antennas to ensure reliable and interference-free communications, and due to small wavelength, mmWave technology infrastructure requires large antenna arrays to be packed in miniature physical dimensions, which fueling the requirement of antennas and transceivers designed for the millimeter (mm) wave technology, fueling the market growth.

- The higher data transfer rate of the mmWave technology has various uses in real-time gaming, high-quality video streaming, and other bandwidth-intensive applications, which require antennas and transceivers for relaying and transforming the signals, creating a demand for microstrip, on-chip integrated horn, lens, and reflector, and other antennas for mmWave technology.

- According to a recent GSMA report, 5G adoption is anticipated to reach around a billion connections by 2030. The technology will likely underpin future mobile innovation and boost ongoing deployments, adding almost USD 1 trillion to the global economy in 2030. The report states that throughout 2023, 30 new markets across Africa and Asia will launch 5G services. As 5G adoption continues to scale, network operators are increasing their efforts to expand their 5G fixed wireless access (FWA) offerings. Markets with low fixed broadband penetration and rising incomes will also see faster-than-average 5G growth.

- Market vendors are undergoing strategic initiatives to expand antennas and transceivers' product portfolio for mmWave technology applications and hold a major market share. For instance, in October 2023, Malaysia's 5G network operator, Digital Nasional Berhad (DNB), partnered with Telekom Malaysia (TM) and Chinese vendor ZTE Corporation to conduct a 5G live trial which would deliver speeds up to 28 Gbps. ZTE stated that this partnership was expected to help leverage TM's established network infrastructure, digital expertise, and ZTE's mmWave active antenna unit to deliver the first standalone 5G core of Malaysia for the next-generation transport network.

- In August 2023, Marki Microwave, a provider of radio frequency and microwave products, acquired the waveguide business of Precision Millimeter Wave LLC, a supplier of sub-THz waveguide technology. Marki Microwave plans to offer over 100 standard commercial waveguide products and multiple custom waveguide products like mmWave to sub-THz, including antennas, connectors, switches, and isolators.

- The need for high-speed communications in various end-user applications and the need for phase antennas and highly capable transceivers for mmWave communication add growth to the market, which is supported by acquisitions, investments, and collaborations among the millimeter wave technology market stakeholders.

North America is Expected to Hold Significant Market Share

- The United States has made significant strides in utilizing the millimeter wave spectrum for various applications. Regulatory bodies like the Federal Communications Commission (FCC) have allocated and auctioned millimeter wave frequency bands for licensed and unlicensed use. Notably, the FCC opened spectrum in the 28 GHz, 37 GHz, 39 GHz, and 47 GHz bands for 5G and other wireless communication technologies.

- The rollout of 5G networks in the United States has driven the adoption of millimeter wave technology. Moreover, Viavi Solutions, an Arizona-based network test and measurement company, stated that the United States was one of the significant global countries with the most cities adopting network access.

- For instance, as of April 2023, around 503 cities adopted 5G network access in the country. China followed in second, with 5G availability in 356 cities. As a result, millimeter wave frequencies are a key component of 5G, particularly in deploying high-speed, low-latency 5G networks in urban areas. Telecom companies have been actively deploying 5G infrastructure that includes millimeter wave spectrum to deliver ultra-fast internet speeds and support emerging use cases like augmented reality (AR), virtual reality (VR), and IoT.

- According to CTIA (July 2023), the United States was the leading country in the world to deploy 5G, with more 5G accessibility than any other nation. 5G's more responsive networks and faster speeds drive strong enterprise and consumer adoption. The wireless sector is distributing 5G ahead of schedule, capitalizing records and world-leading capital amounts to deploy 5G faster than any preceding generation of wireless.

- It is expected that 5G will eventually add USD 1.5 trillion to the nation's economy and create new jobs (at least 4.5 million). 5G networks across the country already cover over 325 million individuals, giving the world's most accessible 5G networks. Ookla places the United States as the world leader in accessibility, with more than 54% of connections from 5G-capable handsets linking to a 5G network most of the time.

- Canada has made substantial strides in leveraging the millimeter wave spectrum for various applications. Regulatory authorities, such as Innovation, Science, and Economic Development Canada (ISED), allocate and control the use of millimeter wave frequencies for licensed and unlicensed purposes. Frequencies in the 26 GHz, 28 GHz, 38 GHz, and other bands are significant assets for millimeter wave applications.

- Moreover, the country's rising need for 5G networks that leverage millimeter wave frequencies to deliver ultra-fast internet speeds and low latency is increasing. For instance, according to Ericsson reports, as of November 2022, in the upcoming 12 to 15 months, four million Canadian smartphone users intend to upgrade to 5G service. Additionally, only a third of Canadian 5G users believe they are connected to the network more than 50% of the time, while 45% of users still stated they have coverage concerns. Such significant concerns are anticipated to focus on deploying high-frequency radio waves in the millimeter wave spectrum to capture the growing demand.

Millimeter Wave Technology Market Overview

The millimeter wave technology market is fragmented with the presence of major players like Siklu Communication Ltd (Ceragon Networks Ltd), Bridgewave Communications Inc. (Remec Broadband Wireless International), E-band Communications LLC (Axxcss Wireless Solutions Inc.), Millimeter Wave Products Inc., and Ducommun Incorporated. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- December 2023 - Eravant (SAGE Millimeter Inc.) received a patent related to a novel series of electrical connectors used in the rapidly growing field of millimeter-wave electronics. The patented devices are compatible with the existing coaxial interfaces. Uni-Guide waveguide connectors help component manufacturers offer a wide range of waveguide sizes and orientations using a reduced number of package designs.

- August 2023 - Siklu, a global provider of millimeter wave (mmWave) solutions for Digital City and Gigabit Wireless Access (GWA), launched its new MultiHaul TG T261 terminal unit. The T261 mainly represents Siklu's fourth addition to the MultiHaul TG family of point-to-multipoint 60 GHz products and is Terragraph (TG) certified.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

- 4.3 Assessment of Impact of COVID-19 on the Industry

- 4.4 Significance of GaN Across mmWave Applications

- 4.5 mmWave Substrate Landscape (to Include Coverage on mmWave Substrates Such as LCP, PI, and PTFE, along With Their Impact on 5G Infrastructure, Including Base Stations, Phones, and Peripherals)

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Proliferation of Wireless Backhaul of Base Stations

- 5.1.2 Evolution of 5G is Expected to Drive the Market

- 5.2 Market Challenges/Restraints

- 5.2.1 Need for Manufacturing of Compatible Components and Rising Cost of Components

- 5.2.2 Technological Vulnerabilities Leading to Reduced Wave Strength

6 MARKET SEGMENTATION

- 6.1 By Type of Component

- 6.1.1 Antennas and Transceiver

- 6.1.2 Communications and Networking

- 6.1.3 Interface

- 6.1.4 Frequency and Related Components

- 6.1.5 Imaging

- 6.1.6 Other Components

- 6.2 By Licensing Model

- 6.2.1 Fully/Partly Licensed

- 6.2.2 Unlicensed

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.3 Asia

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 South Korea

- 6.3.4 Middle East and Africa

- 6.3.5 Latin America

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Siklu Communication Ltd (Ceragon Networks Ltd)

- 7.1.2 Bridgewave Communications Inc. (REMEC Broadband Wireless Networks LLC)

- 7.1.3 E-band Communications LLC (Axxcss Wireless Solutions Inc.)

- 7.1.4 Millimeter Wave Products Inc.

- 7.1.5 Ducommun Incorporated

- 7.1.6 Eravant (SAGE Millimeter Inc.)

- 7.1.7 Keysight Technologies Inc.

- 7.1.8 Farran Technology Ltd

- 7.1.9 Smiths Interconnect Group Limited

- 7.1.10 NEC Corporation

- 7.1.11 L3Harris Technologies Inc.

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

毫米波技术市场报告(按组件、产品、频段、许可类型、应用和地区)2025 年至 2033 年

毫米波技术市场报告(按组件、产品、频段、许可类型、应用和地区)2025 年至 2033 年 毫米波 5G 市场 - 全球产业规模、份额、趋势、机会和预测(按组件、按用例、按应用、按地区、按竞争)2020-2030F

毫米波 5G 市场 - 全球产业规模、份额、趋势、机会和预测(按组件、按用例、按应用、按地区、按竞争)2020-2030F 全球毫米波 5G 市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测全球毫米波技术市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测

全球毫米波 5G 市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测全球毫米波技术市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测 毫米波技术市场规模、份额及成长分析(按组件、产品类型、授权类型、应用和地区)-2025-2032 年产业预测

毫米波技术市场规模、份额及成长分析(按组件、产品类型、授权类型、应用和地区)-2025-2032 年产业预测 毫米波技术市场分析与预测(2034 年):类型、产品、服务、技术、组件、应用、设备、部署、最终用户和功能

毫米波技术市场分析与预测(2034 年):类型、产品、服务、技术、组件、应用、设备、部署、最终用户和功能 2025年mmWave 5G全球市场报告2025 年毫米波技术全球市场报告全球毫米波 5G 市场电信毫米波技术市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测

2025年mmWave 5G全球市场报告2025 年毫米波技术全球市场报告全球毫米波 5G 市场电信毫米波技术市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测