|

市场调查报告书

商品编码

1685867

欧洲生物防治化学品:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Europe Biopesticides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

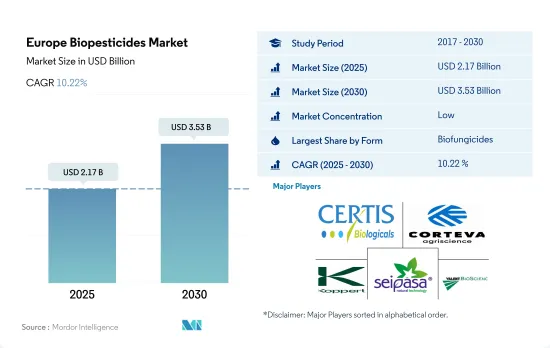

预计 2025 年欧洲生物农药市场规模为 21.7 亿美元,到 2030 年将达到 35.3 亿美元,预测期内(2025-2030 年)的复合年增长率为 10.22%。

- 生物农药是从动物、植物、昆虫或微生物(包括细菌和真菌)中提取的天然物质或药剂,用于控制农业害虫和感染疾病。 2022年,欧洲生物农药市场以金额为准约占全球作物保护市场的77.9%。

- 2017年至2022年间,欧洲生物农药市场价值成长了约31.2%。预计到预测期末,市场价值将成长约77.9%,达到32亿美元。儘管化学或合成农药在作物保护领域仍占主导地位,但人类和动物健康议题在推动生物农药成长方面发挥关键作用。

- 预计到2022年生物农药市场规模将达到约12.9亿美元,其中田间作物占市场份额的78.6%。田间作物的优势主要在于该地区的种植面积较大,到2022年将占有机作物种植总面积的约81.2%。

- 生物杀菌剂占据欧洲生物农药市场的主导地位。 2022 年,该细分市场的市场占有率为 59.3%,市场规模为 9.713 亿美元。

- 欧洲绿色新政提出了一项挑战,即到 2030 年将化学农药的使用和风险减少 50%。可能会采用病虫害综合治理 (IPM) 策略,该策略基于对农业生态系统的整体观点,旨在开发主要采用非化学病虫害管理措施的抗病虫害作物系统。我们也推广综合虫害管理 (IPM) 工具并帮助农民找到他们需要的解决方案。这些因素,加上农民越来越多地转向有机农业,预计将在 2023 年至 2029 年期间推动欧洲生物防治市场的发展。

- 由于向永续农业实践的转变和对有机产品的需求不断增加,欧洲生物农药市场在未来几年可能会成长。 2022 年,法国以 19.1% 的份额占据市场主导地位,因为法国农民使用生物农药来减少农业对化学投入的依赖,这符合该国的公共目标。

- 义大利是欧洲第二大生物农药市场。预计 2023 年至 2029 年期间成长率为 75.2%,复合年增长率为 9.8%。近日,欧盟委员会核准了四项法律草案,将简化包括微生物在内的生物植物保护产品的核准和授权程序。预计这将为农民提供化学植物保护产品的替代品,并支持「从农场到餐桌」策略的目标。

- 有机农业是欧盟农业的主要部门,2019年欧盟约有33万个有机农场实行有机农业,占成员国耕地面积的20%。 「从农场到餐桌」策略旨在2030年将欧盟有机农业的农业用地总面积增加到至少25%,为植物病虫害防治的永续替代方案提供机会。

- 预计未来几年,越来越多的产品推出和政府对生物农药使用的支持将对市场产生重大影响,并有可能推动永续农业解决方案的持续成长和创新。随着市场的发展,行业参与者需要投资研发,以跟上不断变化的消费者偏好、监管要求以及对永续农业解决方案日益增长的需求。

欧洲生物农药市场趋势

欧洲绿色新政极大地促进了全部区域有机农业的发展

- 欧洲国家正大力推广有机农业,过去十年来,被归类为有机农业的土地面积大幅增加。 2021年3月,欧盟委员会推出了“有机行动计画”,旨在实现《欧洲绿色新政》中到2030年25%的农业用地实现有机化的目标。奥地利、义大利、西班牙和德国是欧洲领先的有机农业国家。义大利有机耕种占其农业用地面积的 15.0%,高于欧盟 7.5% 的平均水准。

- 2021年,欧盟有机土地面积达1,470万公顷。农业生产区分为三大利用类型:作物(主要为谷物、根茎类作物和新鲜蔬菜)、永久性草地和永久性作物。 2021年,有机耕地面积为650万公顷,占欧盟有机农业总面积的46%。

- 2017年至2021年间,欧盟谷物、油籽、蛋白质作物和豆类的有机种植面积将增加32.6%,达到1,60万公顷以上。 2020 年,多年生作物种植面积达 130 万公顷,占有机土地面积的 15%。橄榄、葡萄、杏仁和柑橘类水果就是属于这一类作物的几个例子。西班牙、义大利和希腊是重要的有机橄榄种植国,近年来其种植面积分别为19.7万公顷、17.9万公顷和4.7万公顷。橄榄和葡萄对欧洲农业都至关重要,因为它们可以加工成国内外都需要的特色产品。该地区有机种植面积的增加可望增强欧洲有机农业产业。

该地区对有机产品的需求不断增加,人均支出不断增加

- 欧洲消费者越来越多地购买采用天然材料和工艺製成的产品。儘管有机食品在欧盟农业总产量中所占比例仍然很小,但它已不再是小众产业。欧盟是国际第二大有机产品单一市场,人均年支出为74.8美元。过去十年,欧洲人均有机食品支出翻了一番。 2020 年,瑞士和丹麦消费者在有机食品上的支出最高(人均分别为 494.09 美元和 453.90 美元)。

- 根据世界有机贸易组织的资料,德国是欧洲最大的有机食品市场,也是仅次于美国的全球第二大有机食品市场,2021年市场规模达63亿美元,人均消费量达75.6美元。该国占全球有机食品需求的 10.0%,预计 2021 年至 2026 年的复合年增长率为 2.7%。

- 法国有机食品市场成长强劲,2021年零售额成长12.6%。根据世界有机贸易组织的资料,2021年法国人均有机食品支出为88.8美元。 2018年,根据法国生物技术署/精神洞察晴雨表的记录,88%的法国人表示他们曾经食用过有机产品。保护健康、环境和动物福利是法国消费有机食品的主要原因。西班牙、荷兰和瑞典等其他几个国家的有机市场也开始成长,纷纷开设有机商店。在新冠疫情期间和之后,有机食品的销量增加。这是因为消费者越来越关注健康问题,并且了解传统种植食品的负面影响。

欧洲生物农药产业概况

欧洲生物农药市场分散,前五大公司占2.67%的市占率。市场的主要企业有:Certis USALLC、Corteva Agriscience、Koppert Biological Systems Inc.、Seipasa、SA 和 Valent Biosciences LLC。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章执行摘要和主要发现

第二章 报告要约

第三章 引言

- 研究假设和市场定义

- 研究范围

- 调查方法

第四章 产业主要趋势

- 有机种植区

- 有机产品人均支出

- 法律规范

- 法国

- 德国

- 义大利

- 荷兰

- 俄罗斯

- 西班牙

- 土耳其

- 英国

- 价值炼和通路分析

第五章市场区隔

- 形式

- 生物真菌剂

- 生物除草剂

- 生物杀虫剂

- 其他生物防治剂

- 作物类型

- 经济作物

- 园艺作物

- 耕地作物

- 原产地

- 法国

- 德国

- 义大利

- 荷兰

- 俄罗斯

- 西班牙

- 土耳其

- 英国

- 其他欧洲国家

第六章 竞争格局

- 关键策略趋势

- 市场占有率分析

- 商业状况

- 公司简介.

- Andermatt Group AG

- Atlantica Agricola

- Biolchim SPA

- Bionema

- Certis USALLC

- Corteva Agriscience

- Koppert Biological Systems Inc.

- Lallemand Inc.

- Seipasa, SA

- Valent Biosciences LLC

第七章:CEO面临的关键策略问题

第 8 章 附录

- 世界概况

- 概述

- 五力分析框架

- 全球价值链分析

- 市场动态(DRO)

- 资讯来源及延伸阅读

- 图片列表

- 关键见解

- 资料包

- 词彙表

简介目录

Product Code: 48764

The Europe Biopesticides Market size is estimated at 2.17 billion USD in 2025, and is expected to reach 3.53 billion USD by 2030, growing at a CAGR of 10.22% during the forecast period (2025-2030).

- Biopesticides are naturally occurring substances or agents derived from animals, plants, insects, and microorganisms, including bacteria and fungi, which are used to manage agricultural pests and infections. In 2022, the European biopesticides market accounted for about 77.9% of the global crop protection market by value.

- The European biopesticides market value increased by about 31.2%, between 2017 and 2022. The market value is anticipated to increase by about 77.9% and reach USD 3.20 billion by the end of the forecast period. While the prevalence of chemical or synthetic pesticides in crop protection is continuing, human and animal health concerns are playing key roles in driving the growth of biopesticides.

- The biopesticides market is dominated by field crops, which accounted for a 78.6% share, valued at about USD 1.29 billion in 2022. The dominance of field crops is mainly due to its large cultivation area in the region, which accounted for about 81.2% of the total organic crop cultivation area in 2022.

- Biofungicides dominate the European biopesticides market. The segment held a market share of 59.3% in 2022, valued at USD 971.3 million.

- The European Green Deal set the challenging goal of reducing the use and risk of chemical pesticides by 50% in 2030. IPM strategies are likely to be used, which are based on a holistic view of agroecosystems, with the goal of developing pest- and disease-resistant cropping systems that primarily employ non-chemical pest management measures. They also promote Integrated Pest Management (IPM) tools, which assist farmers in finding the required solutions. Such factors and the growing trend of farmers transitioning to organic agriculture are expected to drive the European biopesticides market between 2023 and 2029

- The European biopesticides market may grow in the coming years, owing to a shift toward sustainable agricultural practices and increasing demand for organic products. France dominated the market with a 19.1% share in 2022, as French farmers used biopesticides to reduce reliance on chemical inputs in agriculture, aligning with the country's public policy objectives.

- Italy is the second-largest market for biopesticides in Europe. It is projected to grow by 75.2%, with a CAGR of 9.8% between 2023 and 2029. Recently, the European Commission has endorsed four legal acts that simplify the approval and authorization process of biological plant protection products containing microorganisms, which are expected to provide farmers with tools to substitute chemical plant protection products and support the objectives of the Farm-to-Fork Strategy.

- Organic farming is a key sector of EU agriculture, with almost 330,000 organic farmers in the European Union in 2019 and a 20% share of the farming area in the Member States. The Farm-to-Fork Strategy aims to increase the total farmland under organic farming in the European Union to at least 25% by 2030, providing opportunities for sustainable alternatives to control plant pests.

- The rising product launches and government support for the use of biopesticides are expected to significantly impact the market in the coming years, with the potential for continued growth and innovation in sustainable agricultural solutions. As the market evolves, industry players must keep up with changing consumer preferences and regulatory requirements and invest in R&D to meet the growing demand for sustainable agricultural solutions.

Europe Biopesticides Market Trends

European green deal is majorly contributing for increasing organic cultivation across the region

- European countries are increasingly promoting organic farming, and the amount of land categorized as organic has significantly increased over the last 10 years. In March 2021, the European Commission launched an organic action plan to achieve the European Green Deal target of ensuring that 25% of agricultural land is under organic farming by 2030. Austria, Italy, Spain, and Germany are among the leading countries for organic cultivation in the European region. Italy has 15.0% of its agricultural area under organic farming, which is higher than the EU average of 7.5%.

- In 2021, organic land in the European Union was recorded at 14.7 million hectares. The agricultural production area is divided into three main types of use: arable land crops (mainly cereals, root crops, and fresh vegetables), permanent grassland, and permanent crops. The area of organic arable land was 6.5 million hectares in 2021, the equivalent of 46% of the European Union's total organic agricultural area.

- The organic cultivation area of cereals, oilseeds, protein crops, and pulses in the European Union increased by 32.6% between 2017 and 2021, amounting to more than 1.6 million hectares. With 1.3 million hectares in production, perennial crops accounted for 15% of the organic land in 2020. Olives, grapes, almonds, and citrus fruits are a few examples of crops in this group. Spain, Italy, and Greece are significant growers of organic olive trees, with 197,000, 179,000, and 47,000 hectares, respectively, in recent years. Both olives and grapes are crucial for the European agricultural industry because they can be turned into specialty products that are in demand locally and globally. The increasing organic acreage in the region is expected to strengthen the organic agricultural industry in Europe.

Growing demand and rising the per capita spending on organic products in the region

- European consumers are increasingly purchasing goods made using natural materials and methods. Even though organic food still only makes up a fraction of the European Union's overall agricultural production, it is no longer a niche industry. The European Union represents the second-largest single market for organic goods internationally, with an average per capita spending of USD 74.8 annually. The per capita spending on organic food in Europe has doubled in the last decade. In 2020, Swiss and Danish consumers spent the most on organic food (USD 494.09 and USD 453.90 per capita, respectively).

- Germany is the largest organic food market in Europe and the second largest market in the world after the United States, with a market size of USD 6.3 billion in 2021 and a per capita consumption of USD 75.6, as per Global Organic Trade data. The country accounted for 10.0% of the global organic food demand and is estimated to record a CAGR of 2.7% between 2021 and 2026.

- The organic food market in France witnessed strong growth, with a 12.6% rise in retail sales in 2021. The country's per capita spending on organic food was recorded at USD 88.8 in 2021, as per Global Organic Trade data. In 2018, as recorded by the Agence BIO/Spirit Insight Barometer, 88% of French people declared having consumed organic products. The preservation of health, environment, and animal welfare are the primary justifications for consuming organic foods in France. The organic market has begun to grow in several other nations, including Spain, the Netherlands, and Sweden, with the opening of organic stores. Organic food sales grew during and post the COVID-19 pandemic as consumers began paying more attention to health issues and learned the adverse effects of conventionally grown food.

Europe Biopesticides Industry Overview

The Europe Biopesticides Market is fragmented, with the top five companies occupying 2.67%. The major players in this market are Certis U.S.A. L.L.C., Corteva Agriscience, Koppert Biological Systems Inc., Seipasa, SA and Valent Biosciences LLC (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 France

- 4.3.2 Germany

- 4.3.3 Italy

- 4.3.4 Netherlands

- 4.3.5 Russia

- 4.3.6 Spain

- 4.3.7 Turkey

- 4.3.8 United Kingdom

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Form

- 5.1.1 Biofungicides

- 5.1.2 Bioherbicides

- 5.1.3 Bioinsecticides

- 5.1.4 Other Biopesticides

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Netherlands

- 5.3.5 Russia

- 5.3.6 Spain

- 5.3.7 Turkey

- 5.3.8 United Kingdom

- 5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Andermatt Group AG

- 6.4.2 Atlantica Agricola

- 6.4.3 Biolchim SPA

- 6.4.4 Bionema

- 6.4.5 Certis U.S.A. L.L.C.

- 6.4.6 Corteva Agriscience

- 6.4.7 Koppert Biological Systems Inc.

- 6.4.8 Lallemand Inc.

- 6.4.9 Seipasa, SA

- 6.4.10 Valent Biosciences LLC

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

生物杀线虫剂市场规模、份额和成长分析(按类型、剂型、应用方式、作物类型、虫害类型和地区划分)-产业预测,2025-2032年

生物杀线虫剂市场规模、份额和成长分析(按类型、剂型、应用方式、作物类型、虫害类型和地区划分)-产业预测,2025-2032年 全球生物肥料和生物农药市场:预测至2032年-按产品类型、形态、应用方法、作物类型和地区分類的分析

全球生物肥料和生物农药市场:预测至2032年-按产品类型、形态、应用方法、作物类型和地区分類的分析 生物农药市场(按类型、作物、剂型、应用和销售管道)——2025-2030 年全球预测

生物农药市场(按类型、作物、剂型、应用和销售管道)——2025-2030 年全球预测 2025-2033年生物农药市场报告(依产品、剂型、来源、应用方式、作物种类及地区)

2025-2033年生物农药市场报告(依产品、剂型、来源、应用方式、作物种类及地区) 2025年全球生物农药市场报告

2025年全球生物农药市场报告 生物农药市场:2025 年至 2030 年预测

生物农药市场:2025 年至 2030 年预测 细菌生物防治剂:市场占有率分析、产业趋势、统计数据、成长预测(2025-2030 年)2032年生物农药市场预测:按产品类型、作物类型、剂型、应用、最终用户和地区进行的全球分析日本生物农药市场报告(依产品类型(生物除草剂、生物杀虫剂、生物杀菌剂等)、应用领域(作物型、非作物型)及地区划分)2025-2033

细菌生物防治剂:市场占有率分析、产业趋势、统计数据、成长预测(2025-2030 年)2032年生物农药市场预测:按产品类型、作物类型、剂型、应用、最终用户和地区进行的全球分析日本生物农药市场报告(依产品类型(生物除草剂、生物杀虫剂、生物杀菌剂等)、应用领域(作物型、非作物型)及地区划分)2025-2033 生物农药市场规模、份额及成长分析(按类型、来源、剂型、应用类型、作物类型和地区)-2025-2032 年产业预测

生物农药市场规模、份额及成长分析(按类型、来源、剂型、应用类型、作物类型和地区)-2025-2032 年产业预测

▼