|

市场调查报告书

商品编码

1685870

氦气 -市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Helium - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

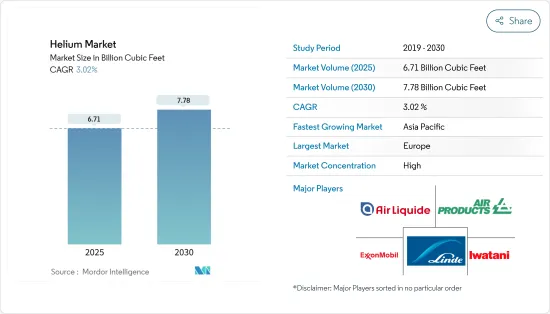

预计 2025 年氦气市场规模为 67.1 亿立方英尺,预计 2030 年将达到 77.8 亿立方英尺,预测期内(2025-2030 年)的复合年增长率为 3.02%。

由于新冠疫情,航太业受到严重影响,导致近期航太航太业萎缩,对氦气在航太应用的成长前景产生了负面影响。然而,受医疗保健等各种终端用途消费成长的推动,2021 年消费强劲反弹。

主要亮点

- 半导体产业对氦气的消耗量增加以及航空业对氦气的使用量增加是推动市场成长的主要因素。

- 另一方面,氦气提取製程的高成本和氦气供应的不稳定可能会阻碍市场成长。

- 然而,解决氦气短缺问题和增加氦气在肺部护理中的应用预计将在预测期内为市场提供大量机会。

- 预计欧洲将主导市场,而亚太地区预计将在预测期内实现最高成长率。

氦气市场趋势

医疗保健产业需求增加

- 氦气在医疗保健产业有广泛的用途。氦的温度可低至-269°C,因此液态氦是冷却核磁共振造影系统中磁铁的理想选择。氦气也用于监测呼吸。它是治疗肺气肿和气喘等影响呼吸的疾病的重要成分。

- 氦气通常用于治疗肺部疾病。氧气和氦气联合使用可治疗急性和慢性呼吸系统疾病。对于低温氦应用,没有什么可以取代氦。

- 根据经合组织的报告,美国的医疗卫生支出占国内生产总值(GDP)的比例最高,为16.6%,其次是德国(12.7%)、法国(11.9%)和日本(11.5%)。

- 由于对 MRI 扫描的需求不断增长,医疗保健领域对氦气的需求也在增加。 MRI 在癌症筛检和神经病学领域的应用也正在不断扩大。

- 从地理上看,氦气主要用于北美的医疗保健领域。美国和加拿大将其GDP的很大一部分用于医疗保健。

- 此外,亚太地区预计将成为医疗保健产业成长最快的地区。这一增长是由公共医疗体系改革和医疗旅游业的快速扩张所推动的。中国的健康医疗产业取得了显着成长,年增长率超过10%。

- 根据国际医学磁振造影学会的数据,截至 2024 年 1 月,已有超过 1.5 亿名患者接受过 MRI 扫描。每年约有 1000 万名患者接受 MRI 扫描。

- 此外,根据经济合作暨发展组织(OECD)的数据,日本的人均核磁共振造影系统拥有量遥遥领先,其次是美国的核磁共振造影系统数量,澳洲的 CT 扫描仪数量则位居第二。奥地利、德国、希腊、冰岛、义大利、韩国和瑞士的人均 MRI 和 CT 扫描仪数量也远高于经合组织的平均值。

- 此外,全球暖化对空气品质的不利影响以及新冠肺炎疫情的爆发加剧了急性和慢性呼吸系统疾病的发生率,因此需要更多专用于呼吸护理的医疗设备。

- 由于上述因素,预计预测期内医疗保健产业对氦气的需求将会成长。

欧洲主导市场

- 由于医疗保健、航太和电子等各领域的高需求,预计欧洲将主导市场。

- 德国在生产高品质医疗设备方面有着悠久的历史,重点是精密仪器、诊断成像和光学技术。日本医疗设备市场规模位居美国、日本之后,居世界第三位,在欧洲是法国的2倍,义大利、英国、西班牙的3倍。

- 德国还拥有强大的半导体产业,这是该国市场成长的主要驱动力之一。据估计,每年约有 155 亿欧元(144.7 亿美元)用于创新感测器和新时代技术的研发。主要的电子基础设施公司正在投资扩大其生产能力。例如,2023年2月,全球半导体领先企业英飞凌科技股份公司获得批准,开始在德勒斯登建造价值50亿欧元(53.5亿美元)的半导体工厂,以满足汽车电力电子、5G行动晶片以及工业晶片和感测器的需求。预计生产将于 2026 年开始。

- 航太工业是法国继汽车工业之后最大的工业部门。近年来,该产业发展迅速,现已成为世界上最大的航太产业之一。法国是世界上最重要的飞机零件和系统生产和出口地之一。此外,印度太空协会(ISpA)与法国航太工业协会(GIFAS)于 2023 年 10 月签署谅解备忘录(MoU),以加强两国之间的太空合作,这可能会对国内氦气市场产生积极影响。

- 此外,2022年7月,英国将与雪菲尔大学、剑桥大学和伦敦大学学院(UCL)合作建立一个名为「国家外延设施」的大型研究设施,以帮助英国成为半导体研发领域的世界领导者。该国还推出了一个名为东北先进材料和电子(NEAME)的新丛集,以突出和推广该国作为先进复合半导体技术设计和製造中心的地位。

- 由于这些因素,预计欧洲氦气市场在预测期内将稳定成长。

氦气产业概况

氦气市场本质上是高度整合的。市场的主要企业包括液化空气集团、林德集团、Matheson Try Gas、岩谷公司和梅塞尔集团(排名不分先后)。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 半导体产业氦气消耗量不断增加

- 扩大氦气在航空工业的使用

- 限制因素

- 昂贵的提取过程

- 稳定的氦气供应

- 产业价值链分析

- 波特五力模型

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔

- 阶段

- 液体

- 气体

- 应用

- 呼吸混合物

- 低温

- 洩漏检测

- 加压和吹扫

- 焊接

- 受控气氛

- 其他用途

- 最终用户产业

- 航太和飞机

- 电子和半导体

- 核能

- 卫生保健

- 焊接和金属製造

- 其他最终用户产业

- 地区

- 生产分析

- 美国

- 卡达

- 阿尔及利亚

- 澳洲

- 波兰

- 俄罗斯

- 其他国家

- 消费分析

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲和纽西兰

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 法国

- 义大利

- 英国

- 俄罗斯

- 其他欧洲国家

- 世界其他地区

- 南美洲

- 中东和非洲

- 生产分析

第六章竞争格局

- 併购、合资、合作与协议

- 市场占有率(%)分析

- 主要企业策略

- 公司简介

- Air Liquide

- Air Products Inc.

- Exxon Mobil Corporation

- Gazprom

- Gulf Cryo

- Iwatani Corporation

- Linde PLC

- Matheson Tri-Gas Inc.

- Messer Group GmbH

- NexAir LLC

- Pgnig Sa(Orlen)

- Qatarenergy Lng

- Renergen

- Weil Group

第七章 市场机会与未来趋势

- 发展4.0解决氦气短缺问题

- 氦气在肺部治疗的应用日益广泛

The Helium Market size is estimated at 6.71 Billion Cubic Feet in 2025, and is expected to reach 7.78 Billion Cubic Feet by 2030, at a CAGR of 3.02% during the forecast period (2025-2030).

Due to COVID-19, the aerospace industry was severely affected, resulting in the contraction of the aerospace industry in recent times, negatively affecting the growth prospects of helium in aerospace applications. However, it recovered significantly in 2021, owing to rising consumption from various end-use applications, including healthcare.

Key Highlights

- The increasing consumption of helium across the semiconductor industry and growing utilization of helium across the aviation industry are major factors driving the growth of the market studied.

- On the flip side, the high cost of the extraction process and the inconsistent supply of helium are likely to hinder the growth of the market studied.

- Nevertheless, developments toward ending helium shortage 4.0 and increasing adoption of helium in pulmonary treatment are anticipated to provide numerous opportunities for the market studied during the forecast period.

- Europe is expected to dominate the market, and Asia-Pacific is likely to witness the highest growth rate during the forecast period.

Helium Market Trends

Increasing Demand from the Healthcare Industry

- Helium has a wide range of uses in the healthcare industry. It can reach a temperature of -269 °C, making liquid helium the best option for cooling the magnets of MRI machines. Helium is also being used for breathing observation. It is an essential component in treating emphysema, asthma, and other conditions that affect breathing.

- Helium is usually used to treat lung diseases. Oxygen and helium are used together to treat acute and chronic respiratory ailments, as the combination reaches the lungs faster than all the others. There is no substitute for helium in cryogenic helium applications.

- As per the report of OECD, health expenditure as a percentage of gross domestic product (GDP) is highest in the United States (16.6%), followed by Germany (12.7%), France (11.9%), and Japan (11.5%).

- The demand for helium in the healthcare sector is increasing owing to the rising demand for MRI scans. MRI has also seen growing applications in cancer screening and neurology.

- Geographically, helium is predominantly used in the North American healthcare sector. The United States and Canada spend a major share of their GDP on healthcare.

- Also, Asia-Pacific is expected to be the fastest-growing region in the healthcare industry. This growth is fueled by public healthcare reforms and rapidly expanding medical tourism. The Chinese healthcare industry has been witnessing significant growth, registering a growth rate of more than 10% annually, followed by India.

- As of January 2024, according to the International Society for Magnetic Resonance in Medicine, over 150 million patients underwent MRI examinations. Every year, approximately 10 million patients undergo MRI procedures.

- Furthermore, as per the Organisation for Economic Cooperation and Development (OECD), Japan has by far the highest number of MRI units and CT scanners per capita, followed by the United States for MRI units and Australia for CT scanners. Austria, Germany, Greece, Iceland, Italy, Korea, and Switzerland also have significantly more MRI and CT scanners per capita than the OECD average.

- In addition, global warming's negative effects on air quality and the outbreak of COVID-19 exacerbated the rate of acute and chronic respiratory illnesses, prompting the need to increase the number of healthcare equipment specializing in respiratory care.

- Based on the factors mentioned above, the demand for helium from the healthcare industry is expected to grow over the forecast period.

Europe to Dominate the Market

- Europe is expected to dominate the market studied owing to the high demand from different sectors, such as healthcare, aerospace, electronics, and others.

- Germany has a long history of producing high-quality medical equipment, emphasizing precision instruments, diagnostic imaging, and optical technologies. The nation hosts the third-largest medical devices market in the world, after the United States and Japan, and the largest in Europe, comprising twice the size of the French market and three times as large as those of Italy, the United Kingdom, and Spain.

- Germany also focuses on the semiconductor industry, which is one of the main drivers of the market's growth in the country. It is estimated that around EUR 15.5 billion (USD 14.47 billion) has been invested annually in R&D for the development of innovative sensors and new-age technologies. Major electronic base companies are investing to expand their production capacity. For instance, in February 2023, Infineon Technologies AG, a global semiconductor leader, received the approval to begin work on a EUR 5 billion (USD 5.35 billion) semiconductor plant to meet the demand for power electronics in auto and mobile chips for 5G and industry chips and sensors, in Dresden. It is due to start production in 2026.

- The aerospace industry is the largest industrial sector in France, followed by the automotive industry. It has witnessed rapid growth in recent years and has become one of the largest aerospace industries in the world. France is one of the significant production and export hubs for aircraft components and systems in the global scenario. Furthermore, the signing of a Memorandum of Understanding (MoU) between the Indian Space Association (ISpA) and the French Aerospace Industries Association GIFAS in October 2023 to enhance space cooperation between the two countries was likely to impact the helium market within the country positively.

- Also, in July 2022, a major research facility named the National Epitaxy Facility collaborated with the Universities of Sheffield, Cambridge, and University College London (UCL) to support the United Kingdom in becoming a world leader in semiconductor R&D. The country also launched a new cluster, named the Northeast Advanced Material Electronics (NEAME), to highlight and promote the country as a center of excellence for advanced compound semiconductor technology design and production.

- Due to all such factors, the European helium market is expected to witness steady growth during the forecast period.

Helium Industry Overview

The helium market is highly consolidated in nature. The major players in the market include (not in any particular order) Air Liquide, Linde PLC, Matheson Tri-Gas Inc., Iwatani Corporation, and Messer Group.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Consumption of Helium Across the Semiconductor Industry

- 4.1.2 Growing Utilization of Helium Across Aviation Industry

- 4.2 Restraints

- 4.2.1 Expensive Extraction Process

- 4.2.2 Inconsistent Supply of Helium

- 4.3 Industry Value Chain Analysis

- 4.4 Porter Five Forces

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Phase

- 5.1.1 Liquid

- 5.1.2 Gas

- 5.2 Application

- 5.2.1 Breathing Mixes

- 5.2.2 Cryogenics

- 5.2.3 Leak Detection

- 5.2.4 Pressurizing and Purging

- 5.2.5 Welding

- 5.2.6 Controlled Atmosphere

- 5.2.7 Other Applications

- 5.3 End-user Industry

- 5.3.1 Aerospace and Aircraft

- 5.3.2 Electronics and Semiconductors

- 5.3.3 Nuclear Power

- 5.3.4 Healthcare

- 5.3.5 Welding and Metal Fabrication

- 5.3.6 Other End-user Industries

- 5.4 Geography

- 5.4.1 Production Analysis

- 5.4.1.1 United States

- 5.4.1.2 Qatar

- 5.4.1.3 Algeria

- 5.4.1.4 Australia

- 5.4.1.5 Poland

- 5.4.1.6 Russia

- 5.4.1.7 Other Countries

- 5.4.2 Consumption Analysis

- 5.4.2.1 Asia-Pacific

- 5.4.2.1.1 China

- 5.4.2.1.2 India

- 5.4.2.1.3 Japan

- 5.4.2.1.4 South Korea

- 5.4.2.1.5 Australia and New Zealand

- 5.4.2.1.6 Rest of Asia-Pacific

- 5.4.2.2 North America

- 5.4.2.2.1 United States

- 5.4.2.2.2 Canada

- 5.4.2.2.3 Mexico

- 5.4.2.3 Europe

- 5.4.2.3.1 Germany

- 5.4.2.3.2 France

- 5.4.2.3.3 Italy

- 5.4.2.3.4 United Kingdom

- 5.4.2.3.5 Russia

- 5.4.2.3.6 Rest of Europe

- 5.4.2.4 Rest of the World

- 5.4.2.4.1 South America

- 5.4.2.4.2 Middle East and Africa

- 5.4.1 Production Analysis

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Air Liquide

- 6.4.2 Air Products Inc.

- 6.4.3 Exxon Mobil Corporation

- 6.4.4 Gazprom

- 6.4.5 Gulf Cryo

- 6.4.6 Iwatani Corporation

- 6.4.7 Linde PLC

- 6.4.8 Matheson Tri-Gas Inc.

- 6.4.9 Messer Group GmbH

- 6.4.10 NexAir LLC

- 6.4.11 Pgnig Sa (Orlen)

- 6.4.12 Qatarenergy Lng

- 6.4.13 Renergen

- 6.4.14 Weil Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Developments Toward Ending Helium Shortage 4.0

- 7.2 Increasing Adoption of Helium In Pulmonary Treatment

氦气市场按产品形式、供应来源、等级类型、最终用途和分销管道划分-2025-2032年全球预测

氦气市场按产品形式、供应来源、等级类型、最终用途和分销管道划分-2025-2032年全球预测 氦气市场 - 全球产业规模、份额、趋势、机会和预测,按阶段、按应用、按最终用户、按地区和竞争进行细分,2020-2030 年

氦气市场 - 全球产业规模、份额、趋势、机会和预测,按阶段、按应用、按最终用户、按地区和竞争进行细分,2020-2030 年 2025年氦气全球市场报告

2025年氦气全球市场报告 氦气市场规模、份额、趋势分析报告:按阶段、应用、最终用途、地区、细分市场预测,2025-2030 年

氦气市场规模、份额、趋势分析报告:按阶段、应用、最终用途、地区、细分市场预测,2025-2030 年 全球氦气市场(2025-2035)

全球氦气市场(2025-2035) 氦气市场规模、份额、成长分析、按阶段、按应用、按最终用途、按地区 - 行业预测,2024-2031 年

氦气市场规模、份额、成长分析、按阶段、按应用、按最终用途、按地区 - 行业预测,2024-2031 年 氦气市场规模和预测、全球和地区份额、趋势和成长机会分析报告范围:按类型、应用、最终用途行业和地理位置

氦气市场规模和预测、全球和地区份额、趋势和成长机会分析报告范围:按类型、应用、最终用途行业和地理位置 到 2030 年氦气市场预测:按阶段、分销管道、应用、最终用户和地区进行的全球分析

到 2030 年氦气市场预测:按阶段、分销管道、应用、最终用户和地区进行的全球分析 全球氦市场规模、份额和趋势分析报告 - 按阶段、按最终用途、按应用、按地区、展望和预测,2023-2030 年

全球氦市场规模、份额和趋势分析报告 - 按阶段、按最终用途、按应用、按地区、展望和预测,2023-2030 年 2024-2028年全球氦气市场

2024-2028年全球氦气市场