|

市场调查报告书

商品编码

1685877

下一代先进电池-市场占有率分析、产业趋势与统计、成长预测(2025-2030)Next Generation Advanced Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

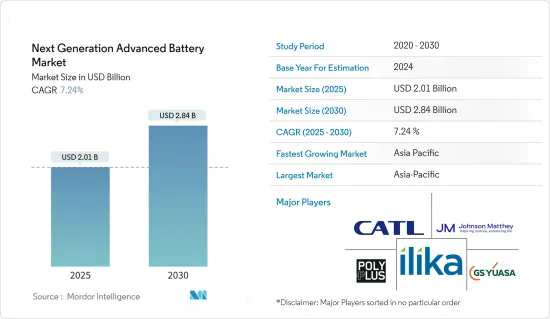

下一代先进电池市场规模预计在 2025 年为 20.1 亿美元,预计到 2030 年将达到 28.4 亿美元,预测期内(2025-2030 年)的复合年增长率为 7.24%。

2020 年,市场受到了新冠疫情的负面影响。目前市场已恢復至疫情前的水准。

主要亮点

- 从长远来看,电动车需求的成长和普及预计将推动市场成长。

- 然而,预计高昂的製造和研发成本将在预测期内阻碍下一代先进电池的成长。

- 然而,预计下一代先进电池製造设施的发展将在预测期内为下一代先进电池市场提供有利的成长机会。

- 亚太地区占据市场主导地位,并可能在预测期内实现最高的复合年增长率。这一增长归因于印度、中国和日本等地区国家投资的增加以及家用电器和电动汽车的普及。

下一代先进电池市场的趋势

预计运输领域将主导市场

- 交通运输系统的电气化越来越受欢迎,各种政府指令加速了电动车的普及,这直接推动了交通运输领域下一代先进电池的成长。

- 2021年,各大汽车製造商表示,通用汽车将在2035年前停止销售汽油和柴油汽车,而奥迪股份公司则计划在2033年前停止生产这类汽车。汽车製造商正在争取将其电动车电气化,并正在投资先进的电池,以使电动车更有效率、更盈利。

- 本田于2022年4月宣布,将在未来十年投资398.4亿美元用于电气化和软体技术,以加速其全球业务的发展。该公司还将在北美建造一条固态电池示范生产线,投资约3.4265亿美元。该投资公司计划与通用汽车合作,到 2024 年推出两款中大型电动车 (EV)。

- 根据国际能源总署(IEA)预测,全球电动车保有量将从2015年的125万辆增加到2020年的1,020万辆左右。 2020年,纯电动车将占电动车的大多数,约685万辆,而插电式混合动力车将占电动车的大多数,约335万辆。

- 此外,与传统的锂离子电池相比,铝空气电池的优点在于,它以铝为燃料,空气透过电解与金属反应,产生电能。续航里程与汽油车相当,能量密度高于锂离子电池。然而,政府的政策支持和汽车製造商的兴趣不足以将其广泛用于电动车的蓄电池。

- 2021年12月,德国汽车製造商梅赛德斯-宾士宣布将投资1亿美元用于一系列电动车。该公司还打算在未来五年内将固态电池技术整合到有限数量的汽车中。宾士计划向开发固态电池的电池公司 Factoral Energy 投资数千万美元。

- 2022 年 4 月,日产汽车公司开始建造层压固态电池原型生产设施,并计划在 2028 年前将其推向市场。这是日产「2030 雄心」策略的一部分,该策略将使该公司投资 170 亿美元用于四款新型电动车概念。

- 总体而言,汽车製造商正在大力投资固态电池和金属空气电池的开发,使汽车成为下一代先进电池市场的关键领域之一。

亚太地区占市场主导地位

- 截至2021年,中国、印度和日本是亚太地区下一代先进电池技术的潜在市场。

- 截至2022年3月,中国电池能源储存装置容量达到3GW,较2019年的1.7GW成长76.5%。此外,中国政府预计到2030年将电池储存容量提高到100GW。这一情况为该地区各类下一代先进电池开发商创造了巨大的机会。

- 根据中国储能产业技术联盟(CNESA)介绍,受电网配套服务(能源储存的主要用途)相关政策的完善以及青海、广东、江苏、内蒙古、新疆等地区的政策发展推动,中国正迎来一波能源储存建设发展热潮。在预测期内,此类政府政策可能会刺激对先进电池技术的需求。

- 目前,中国正在进行下一代先进电池技术的各项开发计划与投资。 2021年7月,宁德时代推出首款新一代钠离子电池及其AB电池组解决方案。宁德时代将电动车市场转向钠离子电池的倡议也得到了中央政府的推动,工业和资讯化部宣布将制定此类电池的标准。

- 除了中国方案外,2022年1月,日本国家材料科学研究所(NIMS)和Softbank Corporation公司开发了一种锂空气电池,其能量密度超过500Wh/kg,大大高于目前的锂离子电池。研究团队证实,该电池可以在室温下充电和放电。研究团队研发的电池展现出最高的能量密度和循环寿命性能。这项成果标誌着锂空气电池向实用化迈出了重要一步。

- 锂空气电池具有成为终极二次电池的潜力,其重量轻、容量大,理论能量密度是现有锂离子电池的数倍。这些潜在优势可用于各种技术,包括无人机、电动车和家庭储能係统。

- 此外,「印度製造」是印度的一项高度优先的倡议,并且已经为生产电动车提供了奖励。汽车电池和电网储存是印度製造业的重点。两轮车、三轮车、汽车和小型巴士的电动车市场对价格的敏感度高于对性能的敏感度。即使下一代先进电池比性能参数略高的类似锂离子电池具有价格优势,但它们在印度的市场机会可能比在其他地方更好。规模经济生产的先进电池在印度具有巨大的市场潜力。

- 2022 年 3 月,印度核准了四家公司根据 PLI 计划製造先进化学电池 (ACC) 蓄电池的激励措施的竞标。这四家公司——Reliance New Energy Solar Limited、Ola Electric Mobility Private Limited、现代环球汽车有限公司和 Rajesh Exports Limited——获得了 1,810 亿印度卢比计划的奖励,以促进印度国内电池的生产。根据该计划,选定的ACC电池製造商预计将在两年内建立生产设施。预计这种政府支持的优惠待遇将有助于创造有利于下一代先进电池市场未来发展的环境。

- 因此,预计上述因素将在预测期内推动亚太地区下一代先进电池市场的发展。

下一代先进电池产业概况

从本质上来说,下一代先进电池市场处于适度整合状态。市场的主要企业(不分先后顺序)包括 Sion Power Corporation、Contemporary Amperex Technology、PolyPlus Battery Co. Ltd.、GS Yuasa Corporation 和 Saft Groupe SA。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究范围

- 市场定义

- 调查前提

第二章执行摘要

第三章调查方法

第四章 市场概述

- 介绍

- 2027 年市场规模与需求预测

- 近期趋势和发展

- 政府法规和政策

- 市场动态

- 驱动程式

- 限制因素

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章市场区隔

- 技术领域

- 固体电解质电池

- 镁离子电池

- 新一代液流电池

- 金属空气电池

- 锂硫电池

- 其他技术

- 最终用户

- 家电

- 运输

- 工业的

- 能源储存

- 其他最终用户

- 地区

- 北美洲

- 亚太地区

- 欧洲

- 南美洲

- 中东和非洲

第六章竞争格局

- 併购、合资、合作与协议

- 主要企业策略

- 公司简介

- Pathion Holding Inc.

- GS Yuasa Corporation

- Johnson Matthey PLC

- PolyPlus Battery Co. Inc.

- Ilika PLC

- Sion Power Corporation

- LG Chem Ltd

- Saft Groupe SA

- Contemporary Amperex Technology Co. Ltd

第七章 市场机会与未来趋势

The Next Generation Advanced Battery Market size is estimated at USD 2.01 billion in 2025, and is expected to reach USD 2.84 billion by 2030, at a CAGR of 7.24% during the forecast period (2025-2030).

The market was negatively impacted by COVID-19 in 2020. Presently the market has now reached pre-pandemic levels.

Key Highlights

- Over the long term, the growing demand and increasing adoption of electric vehicles are expected to drive the growth of the market studied.

- On the other hand, high manufacturing and R&D costs are expected to hamper the growth of Next-Generation advanced batteries during the forecast period.

- Nevertheless, the development of manufacturing facilities for next-generation advanced batteries is likely to create lucrative growth opportunities for the Next-Generation advanced battery market in the forecast period.

- Asia-Pacific region dominates the market and is also likely to witness the highest CAGR during the forecast period. This growth is attributed to the increasing investments, coupled with adoption of consumer electronics and electric vechiles in the countries of this region including India, China and Japan.

Next Generation Advanced Battery Market Trends

Transportation Segment Expected to Dominate the Market

- The electrification of the transportation system is gaining popularity, and various government mandates have accelerated the adoption of electric vehicles, which directly aids the growth of next-generation advanced batteries in the transportation sector.

- In 2021, automobile giants announced that General Motors will stop selling petrol and diesel models by 2035, and Audi AG plans to stop producing such vehicles by 2033. The carmakers are rushing to electrify their electric cars, which has led the company to invest in advanced batteries for more efficient and profitable electric vehicles.

- In April 2022, Honda Motors announced that it would invest USD 39.84 billion in electrification and software technologies to accelerate its business globally for the next ten years. It will also build a demonstration production line for all-solid-state batteries in North America, allocating approximately USD 342.65 million. The investment company plans to launch two mid-to-large-scale electric vehicles (EV) models by 2024 with a partnership with General Motors.

- According to the International Energy Agency (IEA), the global electric vehicle stock increased from 1.25 million in 2015 to about 10.2 million in 2020. In 2020, battery-electric vehicles accounted for most of the electric vehicles at about 6.85 million, and plug-in hybrid electric vehicles were about 3.35 million.

- Furthermore, aluminium-air batteries have an advantage over the conventional lithium-ion battery as the aluminium acts as a fuel where air reacts with the metal via an electrolyte to produce power. It has a travel range similar to gasoline-powered cars and a higher energy density than the lithium-ion battery. However, it lacks government policy support and attention from automakers to make it a popular battery energy storage system for electric vehicles.

- In December 2021, Mercedes Benz, a German car manufacturer, announced to invest of USD 100 million in a wide range of electric cars. The company also intends to integrate solid-state battery technology into a limited number of vehicles within the next five years. Mercedes Benz plans to invest tens of millions into Factorial Energy, a battery company to develop solid-state batteries.

- In April 2022, Nissan Motor Company planned to bring laminated solid-state batteries to the market by 2028, with the beginning of a prototype production facility. It is a part of Nissan's Ambition 2030 strategy, plus an investment of USD 17 billion for the four new electric vehicle concepts.

- Overall, automobile manufacturers are investing heavily in developing solid-state batteries and metal-air batteries, making automobiles one of the major sectors of the next-generation advanced battery market.

Asia-Pacific to Dominate the Market

- As of 2021, China, India, and Japan were the potential markets for the next generation advanced battery technology in the Asia-Pacific region.

- As of March 2022, China's battery energy storage capacity reached 3 GW, representing an increase of 76.5% compared to 1.7 GW in 2019. Furthermore, the Chinese Government is expected to increase its battery storage capacity to 100 GW by 2030. Such scenarios are creating vast opportunities for various next-generation advanced battery developers in the region.

- According to the China Energy Storage Alliance (CNESA), the refinement of policy related to grid ancillary services - energy storage's primary application - as well as policy developments in regions including Qinghai, Guangdong, Jiangsu, inner Mongolia, and Xinjiang, have created a wave of energy storage construction and development in China. Such government policies will likely boost the demand for advanced battery technologies during the forecast period.

- At present, various development projects and investments in the next generation advanced battery technologies are happening in China. In July 2021, CATL unveiled the first next-generation sodium-ion battery and its AB battery pack solutions. Also, CATL's quest to shift the electric vehicle market toward a sodium-ion cell received a boost from the central government after the Ministry of Industry and Information Technology announced the creation of standards for such battery types.

- In addition to the scenario in China, in January 2022, Japan's National Institute for Material Science (NIMS) and the Softbank Corp. developed a lithium-air battery with an energy density of over 500Wh/kg-significantly higher than currently lithium-ion batteries. The research team confirmed that this battery could be charged and discharged at room temperature. The battery developed by the team shows the highest energy densities and best cycle life performances. These results signify a major step toward the practical use of lithium-air batteries.

- The lithium-air batteries are expected to have the potential to be the ultimate rechargeable batteries: they are lightweight and high capacity, with theoretical energy densities several times that of currently available lithium-ion batteries. Because of these potential advantages, they may use various technologies, such as drones, electric vehicles, and household electricity storage systems.

- Further, "Make in India" is a high-priority movement for India and has already provided incentives to produce electric cars. Batteries for cars and grid storage are high on the agenda for manufacturing in India. The EV market for two-wheelers, three-wheelers, cars, and minibusses is more price-sensitive than performance sensitive. If the next generation advanced batteries have a price advantage over a comparable lithium-ion battery whose performance parameters are marginally higher, it would still find a better market opportunity in India than elsewhere. The advanced batteries made with economies of scale have huge market potential in India.

- In March 2022, India approved bids for four companies to avail incentives under the PLI Scheme for the Advanced Chemistry Cell (ACC) Battery Storage Manufacturing. Reliance New Energy Solar Limited, Ola Electric Mobility Private Limited, Hyundai Global Motors Company Limited, and Rajesh Exports Limited received incentives under India's INR 181 billion program to boost local battery cell production. Under the scheme, selected ACC battery storage manufacturers were expected to set up a production facility within two years. Such government-supportive incentives are expected to create an environment for the future development of the next generation advanced battery market.

- Therefore, the above-mentioned factors are expected to drive the next-generation advanced battery market in the Asia-Pacific region during the forecast period.

Next Generation Advanced Battery Industry Overview

The next-generation advanced battery market is moderately consolidated in nature. Some of the major players in the market (in no particular order) include Sion Power Corporation, Contemporary Amperex Technology Co. Ltd, PolyPlus Battery Co. Inc., GS Yuasa Corporation, and Saft Groupe SA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2027

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Solid Electrolyte Battery

- 5.1.2 Magnesium Ion Battery

- 5.1.3 Next-generation Flow Battery

- 5.1.4 Metal-Air Battery

- 5.1.5 Lithium-Sulfur Battery

- 5.1.6 Other Technologies

- 5.2 End User

- 5.2.1 Consumer Electronics

- 5.2.2 Transportation

- 5.2.3 Industrial

- 5.2.4 Energy Storage

- 5.2.5 Other End Users

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 Asia-Pacific

- 5.3.3 Europe

- 5.3.4 South America

- 5.3.5 Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Pathion Holding Inc.

- 6.3.2 GS Yuasa Corporation

- 6.3.3 Johnson Matthey PLC

- 6.3.4 PolyPlus Battery Co. Inc.

- 6.3.5 Ilika PLC

- 6.3.6 Sion Power Corporation

- 6.3.7 LG Chem Ltd

- 6.3.8 Saft Groupe SA

- 6.3.9 Contemporary Amperex Technology Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

2026年下一代先进电池全球市场报告

2026年下一代先进电池全球市场报告 下一代先进电池市场:2026-2032年全球市场预测(按电池化学成分、形状、生命週期阶段、应用和销售管道)2026年新一代电池全球市场报告

下一代先进电池市场:2026-2032年全球市场预测(按电池化学成分、形状、生命週期阶段、应用和销售管道)2026年新一代电池全球市场报告 新一代先进电池市场-全球产业规模、份额、趋势、机会及预测(依技术、最终用户、地区及竞争格局划分,2021-2031年预测)

新一代先进电池市场-全球产业规模、份额、趋势、机会及预测(依技术、最终用户、地区及竞争格局划分,2021-2031年预测) 全球锂离子电池及新一代电池市场(2026-2036)

全球锂离子电池及新一代电池市场(2026-2036) 下一代高性能电池的全球市场

下一代高性能电池的全球市场 下一代生物分解性电池市场分析及预测(至 2034 年):类型、产品、技术、组件、应用、材料类型、最终用户、部署、功能

下一代生物分解性电池市场分析及预测(至 2034 年):类型、产品、技术、组件、应用、材料类型、最终用户、部署、功能 下一代电池的全球市场(2024-2028)

下一代电池的全球市场(2024-2028) 下一代电池市场规模、份额、趋势分析报告:按技术、按应用、按地区、细分市场预测,2024-2030

下一代电池市场规模、份额、趋势分析报告:按技术、按应用、按地区、细分市场预测,2024-2030 下一代锂电池的全球市场(2024-2028)

下一代锂电池的全球市场(2024-2028)