|

市场调查报告书

商品编码

1686219

丙烯酸-市场占有率分析、产业趋势与统计、成长预测(2025-2030)Acrylic Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

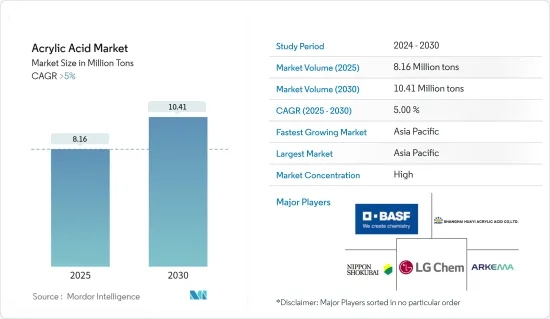

预计2025年丙烯酸市场规模为816万吨,2030年将达到1,041万吨,预测期内(2025-2030年)的复合年增长率将超过5%。

COVID-19疫情对市场产生了负面影响。然而,到 2021 年,人们对个人卫生和清洁环境的认识和意识不断增强,导致对衣物洗护产品的需求增加。丙烯酸用于生产液体清洁剂,刺激了丙烯酸市场的需求。

主要亮点

- 短期内,丙烯酸基高吸水聚合物的应用范围不断扩大以及化学合成使用的增加预计将推动市场成长。

- 与丙烯酸相关的健康危害可能会阻碍市场成长。

- 预计在预测期内,对生物基聚合物的需求不断增长将成为市场的成长机会。

- 亚太地区占据了最大的市场占有率,并可能在预测期内继续主导市场。

丙烯酸市场趋势

丙烯酸在油漆和被覆剂中的使用增加

- 丙烯酸用于生产丙烯酸酯,丙烯酸酯有多种用途,包括油漆和被覆剂。

- 丙烯酸用于建筑涂料、汽车(OEM)和目标商标产品製造商涂饰(包括修补漆)和特殊应用涂料。

- 丙烯酸粉末涂料用作汽车车体的透明涂层。丙烯酸粉末涂料是许多应用的理想解决方案,但它们需要在高温炉中固化。因此,它用途不广泛(例如用于涂漆木材或塑胶)。

- 建筑涂料用于粉刷建筑物和住宅,以保护和装饰表面。大多数都有特定用途,例如屋顶漆、墙面漆或甲板漆。无论用途如何,每种建筑涂料都必须提供一定程度的装饰性、耐用性和保护性。

- 大多数住宅都喜欢将自己喜欢的颜色用于客厅或卧室的墙壁。压克力型涂料是首选,因为它们在颜色和色调方面提供了多种选择。天花板大部分都漆成平面白色,可以反射房间的大部分环境光,让居住者感到房间宽敞、放鬆。水经常会渗入地下室的干墙。

- 2022 年 5 月,Grasim Industries(Aditya Birla Group)表示,计划在 2025 财年向其涂料业务投资 1,000 亿印度卢比(12.0947 亿美元)。 2021 年 1 月,该公司宣布计划在未来三年内投资 500 亿印度卢比(6.0473 亿美元)进军涂料业务。该公司计划于 2024 财年第四季运作一座年产能为 13.32 亿公升(MLPA)的涂料厂。

- 印度油漆和涂料行业是印度各个终端用户行业的重要晴雨表,对技术进步和宏观经济扩张做出了重大贡献。近年来,该行业经历了显着增长,反映了更广泛的行业趋势。

- 根据《欧洲涂料》报道,印度涂料产业预计到 2023 年将达到近 95 亿欧元(102.2 亿美元),未来几年将成长 14%。预计这将增加该国对特殊效果颜料的需求。

- 印度涂料产业预计将投资 3,500 亿印度卢比(41.9 亿美元)至 4,500 亿印度卢比(52.9 亿美元)。印度油漆和涂料行业的各种投资如下:

- 根据美国涂料协会预测,2023年美国建筑涂料将占整个市场的49%,其中OEM涂料占30%,特殊用途涂料占21%。 2023年,美国油漆和涂料产业产量估计约为13.1亿加仑,预计2024年收益将超过13.4亿加仑。

- 德国是欧洲主要的油漆和被覆剂生产国之一,拥有约300家油漆和印刷油墨製造商,其中许多是中小型企业。由于BASF、陶氏、贝克斯集团、Brillux、Altana Chemie、Meffert 和 Mankiewicz 等知名涂料製造商的总部均设在德国,预计该国的市场需求将会成长。

- 2023 年 6 月,奥地利油漆公司 Adler 开始在德国黑尔福德建造新的服务设施,耗资约 1,000 万欧元(1,086 万美元)。正式开幕和落成典礼计划于 2025 年初举行,预计施工将持续到 2024 年夏末。

- 总体而言,预计该地区对丙烯酸的需求将出现初步復苏,并呈现中高速成长。

亚太地区可望主导市场

- 由于中国、印度和日本等国家的需求旺盛,亚太地区占据市场主导地位。

- 中国是亚太地区最大的丙烯酸消费国,预计预测期内其需求将会成长。在中国,建筑和基础设施领域的投资不断增加也推动了对黏合剂、油漆和被覆剂的需求大幅成长。

- 中国是世界最大的个人卫生用品消费国之一。该国对个人卫生产品的需求受到大量婴儿人口和不断增长的可支配收入的推动,这推动了个人和卫生护理支出的增加。因此,预计丙烯酸市场在预测期内将会成长。

- 中国以其工业化和製造业而闻名,对油漆和被覆剂的需求十分广泛。该国使用油漆和被覆剂的主要领域包括汽车、工业和建筑。中国占全球涂料市场的四分之一以上。根据中国涂料工业协会统计,近年来该产业实现了7%的成长率,推动了涂料用丙烯酸市场的发展。

- 中国有近1万家涂料生产企业。全球大多数主要涂料製造商都在中国设有製造地,包括立邦涂料、阿克苏诺贝尔、中国船舶涂料、PPG工业、BASF和艾仕得涂料。涂料公司在中国的投资日益增加。这可能会促进用于生产汽车油漆和被覆剂的丙烯酸市场的发展。

- 中国政府已启动一项大规模建设计画,其中包括在未来十年内将2.5亿人迁移到新的特大城市。因此,丙烯酸可用于建筑施工过程中各种用途的油漆和被覆剂中,改善建筑物的性能。

- 预计到 2025 年,印度建筑业规模将达到 1.4 兆美元。到 2030 年,预计将有 6 亿人居住在城市中心,因此需要额外建造 2,500 万套中高端住宅。根据国家投资计画(NIP),印度已预算1.4兆美元用于基础设施投资,其中24%用于可再生能源、道路、高速公路和城市基础设施,12%用于铁路。

- 因此,预测期内亚太地区很可能主导丙烯酸市场。

丙烯酸产业概况

丙烯酸市场本质上呈现整合态势。市场的主要企业包括BASFSE、阿科玛、日本触媒、LG 化学和上海华谊丙烯酸。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 扩大高吸水性聚合物的应用

- 在化学合成上的应用日益广泛

- 限制因素

- 丙烯酸的健康危害

- 价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔

- 透过导数

- 丙烯酸甲酯

- 丙烯酸丁酯

- 丙烯酸乙酯

- 丙烯酸-2-乙基己酯

- 冰丙烯酸

- 高吸水性聚合物

- 按应用

- 油漆和被覆剂

- 黏合剂和密封剂

- 界面活性剂

- 卫生用品

- 纺织产品

- 其他用途

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 土耳其

- 俄罗斯

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 卡达

- 阿拉伯聯合大公国

- 奈及利亚

- 埃及

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章竞争格局

- 合併、收购、合资、合作和协议

- 市场占有率(%)分析

- 主要企业策略

- 公司简介

- Arkema

- BASF SE

- China Petroleum & Chemical Corporation(SINOPEC)

- Dow

- Formosa Plastics Corporation

- LG Chem

- Merck KGaA

- Mitsubishi Chemical Corporation

- NIPPON SHOKUBAI CO. LTD

- Sasol

- Shanghai Huayi Acrylic Acid Co. Ltd

- Satellite Chemical Co. Ltd

- Wanhua

第七章 市场机会与未来趋势

- 对生物基聚合物的需求不断增加

The Acrylic Acid Market size is estimated at 8.16 million tons in 2025, and is expected to reach 10.41 million tons by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the market. However, in 2021, the demand for laundry care products increased due to the increased awareness and consciousness regarding personal hygiene and clean surroundings. Acrylic acid is used to produce liquid laundry detergent, stimulating the demand for the acrylic acid market.

Key Highlights

- Over the short term, the rising applications of acrylic acid-based super absorbent polymers and the increasing use of chemical synthesis are expected to drive the growth of the market.

- Health hazards associated with acrylic acid may hinder the growth of the market.

- The rising demand for bio-based polymers is likely to act as a growth opportunity for the market during the forecast period.

- The Asia-Pacific accounted for the largest market share, and it is likely to dominate the market during the forecast period.

Acrylic Acid Market Trends

The Usage of Acrylic Acid in Paints and Coatings is Increasing

- Acrylic acid is used to make acrylate esters, which are used in various applications, including paints and coatings.

- Acrylics are used in architectural coatings, finishes for products for original equipment manufacturers, including automotive (OEM) and refinishes, and special-purpose coatings.

- Acrylic powder coatings have been introduced as clear coats on car bodies. Although it is an ideal solution for many applications, curing is achieved at a high temperature in an oven. It is, therefore, not universally applicable (e.g., painting of wood and plastics).

- Architectural coatings are meant to protect and decorate surface features and are used to coat buildings and homes. Most are designated for specific uses, such as roof coatings, wall paints, or deck finishes. Each architectural coating must provide certain decorative, durable, and protective functions despite their use.

- Most homeowners prefer the color of their choice for the living room and bedroom walls. Acrylic paints are the preferred choice as they offer a wide variety of choices in terms of color and shade. A vast majority of ceilings are painted flat white so that they may reflect the majority of the ambient light in the room to make the resident feel that the room is spacious and relaxed. Basement masonry walls can often weep water.

- In May 2022, Grasim Industries (Aditya Birla Group) planned to invest INR 10,000 crore (USD 1,209.47 million) in its paint business by FY 2025. In January 2021, the company announced plans to enter the paints business with INR 5,000 crore (USD 604.73 million) in the next three years. The company will likely commission a paint plant with a production capacity of 1,332 million liters per annum (MLPA) by Q4 FY 2024.

- The paints and coatings industry in India serves as a crucial barometer of the country's various end-user industries, significantly contributing to both technological advancements and macroeconomic expansion. In recent years, this sector has witnessed substantial growth, reflecting broader industry trends.

- According to European Coatings, the Indian paint industry amounted to nearly EUR 9.5 billion in 2023 (USD 10.22 billion), and it is expected to grow by 14% over the coming years. This is expected to increase the demand for special-effect pigments in the country.

- The Indian paint Industry is projected to invest INR 350,000 million (USD 4.19 billion) to INR 450,000 million (USD 5.29 billion) in capital expenditure. Various investments in the Indian paints and coating industry are as follows:

- According to the American Coatings Association, US architectural coatings accounted for 49% of the total market in 2023, while OEM and particular purpose coatings comprised 30% and 21%, respectively. In 2023, the production revenue of the paint and coatings industry in the United States was estimated at approximately 1.31 billion gallons, with forecasts predicting that production will exceed 1.34 billion gallons in 2024.

- Germany stands among the leading producers of paints and coatings in Europe, boasting approximately 300 manufacturers of paints and printing ink, many of which are small- and medium-sized enterprises. With prominent paint manufacturers such as BASF SE, Dow, Beckers Group, Brillux, Altana Chemie, Meffert, and Mankiewicz headquartered in Germany, the demand for the market is expected to escalate in the country.

- In June 2023, Adler, an Austrian paint company, commenced construction on its new service facility in Herford, Germany, with an investment of roughly EUR 10 million (USD 10.86 million). The official opening and inauguration are scheduled for early 2025, with construction set to continue until late summer 2024.

- Overall, the demand for acrylic acid is expected to witness moderate to high growth in the region after the initial recovery period.

The Asia-Pacific Region is Expected to Dominate the Market

- The Asia-Pacific dominated the market due to the high demand from countries like China, India, and Japan.

- China is the largest consumer of acrylic acid in the Asia-Pacific region, and its demand is expected to grow during the forecast period. The demand for adhesives, paints, and coatings in China is also increasing significantly due to the growing investments in the construction and infrastructure sectors.

- China is one of the major consumers of personal hygiene products globally. The country's demand for personal hygiene products is attributed to a large infant population and increasing disposable income, leading to increased spending on personal and hygiene care. Thus, the market for acrylic acid is expected to grow during the forecast period.

- China is known for its industrialization and manufacturing sector, where paints and coatings are widely required. Some of the major sectors where paints and coatings are used in the country are the automotive, industrial, and construction sectors, among others. China accounted for more than one-fourth of the global coatings market. According to the China National Coatings Industry Association, the industry has been registering a growth of 7% in recent years, driving the acrylic acid market in coatings application.

- Nearly 10,000 coatings manufacturers are located in China. Most leading global coating manufacturers, such as Nippon Paint, AkzoNobel, Chugoku Marine Paints, PPG Industries, BASF SE, and Axalta Coatings, have manufacturing bases in China. Paints and coatings companies have been increasingly growing investments in the country. This is likely to fuel the market for acrylic acid used to manufacture automotive paints and coatings.

- The Chinese government rolled out massive construction plans, including making provisions for the movement of 250 million people to its new megacities over the next ten years. Thus, this may create a major scope for acrylic acid in paints and coatings used in various applications during building construction, enhancing the building properties.

- India's construction Industry is projected to reach a value of USD 1.4 trillion by 2025. By 2030, an estimated 600 million people will live in urban centers, resulting in a need for 25 million additional mid and ultra-luxury units. Under the National Investment Plan (NIP), India has an infrastructure investment budget of USD 1.4 trillion, with 24% of the budget earmarked for renewable energy, roads and highways, urban infrastructure, and 12% for railways.

- Hence, due to these factors, the Asia-Pacific region is likely to dominate the acrylic acid market during the forecast period.

Acrylic Acid Industry Overview

The acrylic acid market is consolidated in nature. Some major players in the market include BASF SE, Arkema, NIPPON SHOKUBAI CO. LTD, LG Chem, and Shanghai Huayi Acrylic Acid Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Applications of Super Absorbent Polymers

- 4.1.2 Increasing Usage in Chemical Synthesis

- 4.2 Restraints

- 4.2.1 Health Hazards of Acrylic Acid

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 By Derivative

- 5.1.1 Methyl Acrylate

- 5.1.2 Butyl Acrylate

- 5.1.3 Ethyl Acrylate

- 5.1.4 2-Ethylhexyl Acrylate

- 5.1.5 Glacial Acrylic Acid

- 5.1.6 Superabsorbent Polymer

- 5.2 By Application

- 5.2.1 Paints and Coatings

- 5.2.2 Adhesives and Sealants

- 5.2.3 Surfactants

- 5.2.4 Sanitary Products

- 5.2.5 Textiles

- 5.2.6 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of the Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Arkema

- 6.4.2 BASF SE

- 6.4.3 China Petroleum & Chemical Corporation (SINOPEC)

- 6.4.4 Dow

- 6.4.5 Formosa Plastics Corporation

- 6.4.6 LG Chem

- 6.4.7 Merck KGaA

- 6.4.8 Mitsubishi Chemical Corporation

- 6.4.9 NIPPON SHOKUBAI CO. LTD

- 6.4.10 Sasol

- 6.4.11 Shanghai Huayi Acrylic Acid Co. Ltd

- 6.4.12 Satellite Chemical Co. Ltd

- 6.4.13 Wanhua

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand for Bio-based Polymers

纸币印刷市场(按产品供应、印刷类型、产品类型、面额、生产能力、安全功能和最终用户划分)—2025-2030 年全球预测

纸币印刷市场(按产品供应、印刷类型、产品类型、面额、生产能力、安全功能和最终用户划分)—2025-2030 年全球预测 丙烯酸市场分析:需求、应用(婴儿尿布和个人护理产品)及预测(2034年)

丙烯酸市场分析:需求、应用(婴儿尿布和个人护理产品)及预测(2034年) 丙烯酸衍生物市场规模、份额、成长分析、应用、产品类型、最终用途产业、分子量、地区 - 2025-2032 年产业预测生物丙烯酸市场(按类型、原料和应用)—2025-2030 年全球预测丙烯酸的全球市场:市场规模·占有率·趋势,产业分析 (衍生物·各用途·各地区),未来预测 (2025年~2034年)

丙烯酸衍生物市场规模、份额、成长分析、应用、产品类型、最终用途产业、分子量、地区 - 2025-2032 年产业预测生物丙烯酸市场(按类型、原料和应用)—2025-2030 年全球预测丙烯酸的全球市场:市场规模·占有率·趋势,产业分析 (衍生物·各用途·各地区),未来预测 (2025年~2034年) 丙烯酸市场规模、份额、成长分析、按类型、按技术、按最终用途、按地区 - 按行业预测,2024-2031 年丙烯酸市场:按衍生物、应用、最终用户分类 - 全球预测 2025-2030丙烯酸乙酯市场:按类型、应用分类 - 2025-2030 年全球预测丙烯酸市场:全球产业分析,规模,占有率,成长,趋势,2024-2032年预测全球丙烯酸乙酯市场(2016-2036)

丙烯酸市场规模、份额、成长分析、按类型、按技术、按最终用途、按地区 - 按行业预测,2024-2031 年丙烯酸市场:按衍生物、应用、最终用户分类 - 全球预测 2025-2030丙烯酸乙酯市场:按类型、应用分类 - 2025-2030 年全球预测丙烯酸市场:全球产业分析,规模,占有率,成长,趋势,2024-2032年预测全球丙烯酸乙酯市场(2016-2036)