|

市场调查报告书

商品编码

1686276

食品加工机械:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Food Processing Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

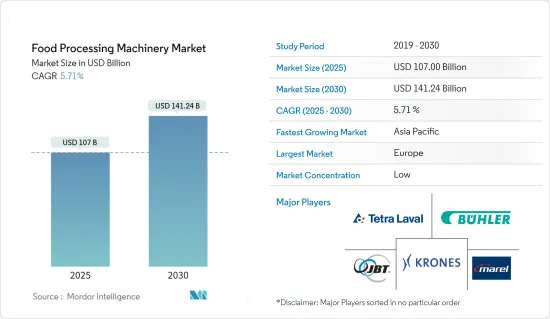

食品加工机械市场规模预计在 2025 年为 1,070 亿美元,预计到 2030 年将达到 1,412.4 亿美元,预测期内(2025-2030 年)的复合年增长率为 5.71%。

消费者偏好转向方便、即食食品,推动了对先进加工设备的需求。消费者生活方式的演变特征是越来越依赖节省时间的解决方案和即食食品。这种模式转移要求食品加工设备不断发展,以满足对方便食品生产效率、种类和品质日益增长的要求。製造商正在投资能够高效加工各种方便食品的设备。全球新兴经济体对加工食品的需求不断增长,以及设备回扣等政府激励措施也推动了新兴市场的需求。

例如,根据印度农业和加工食品出口发展局 (APEDA) 的数据,2021 年印度加工食品出口额为:加工蔬菜 3,909.9 亿美元,加工水果、果汁和坚果 7,801.9 亿美元。

加工食品的需求和消费正在稳步增长,这是该行业发展的主要推动力。儘管这是一种全球现象,但这种愿望在欠发达国家尤其普遍。印度和中国等国的食品加工行业由于近年来经济的成功和市场向国际商品的日益开放而发生了根本性的变化。肉食摄取量的增加是最重要的后果之一。肉类加工设备产业是成长最快的领域之一,尤其是在开发中国家。

西欧、美国和加拿大等新兴市场对烘焙和饮料行业的加工和包装设备的需求强劲。机能饮料的日益流行,也增加了对用于生产非酒精和乳製品的设备的需求。

此外,食品设备製造商正在透过投资高级资料和分析、机器人和自动化等新功能来开发新的工作方式,以吸引更多的加工商。物联网(IoT)技术和智慧感测器在食品加工设备中的整合是一个值得关注的趋势。这实现了即时监控、预测性维护和资料主导的决策,从而提高了整体业务效率。主要市场参与者专注于提供高效机械以满足食品加工商的需求。

食品加工机械市场趋势

食品饮料加工自动化程度提高

食品加工设备技术的进步正在提高效率、生产力和产品品质。自动化、机器人、物联网整合、人工智慧、资料分析等越来越多地被采用,以简化营运、降低人事费用并提高食品安全和可追溯性。随着需求和成本不断上升,自动化有助于增加生产量并缩短生产时间。食品加工商越来越意识到资料主导洞察力在充分利用原材料、确保可追溯性、支持持续改进和提高食品品质和安全方面的价值。机器人屠宰机是最常见的自动化设备之一,有助于加速屠宰过程。自动化设备还可以减少操作潜在有害工具和设备的人员数量,从而提高设施的安全性。

例如,2023 年 11 月,伯明翰大学企业宣布了 EvoPhase。它使用进化 AI 演算法结合工业搅拌机等系统内的颗粒模拟来优化混合叶片和混合容器的形状或尺寸。 EvoPhase 提供广泛的製程设备,包括研磨机、干燥机、焙烧机、涂布机、流体化床和搅拌槽,预计将为产业节省大量成本和能源。

肉类、烘焙和乳製品市场是加工和包装自动化的主要采用者,从而提高了市场的生产效率。随着大量参与者进入市场,自动化技术进步预计将在未来几年推动市场发展。

欧洲占有最大市场占有率

欧洲是主要的区域市场之一,由于对高品质系统的需求不断增加,预计未来几年将经历显着增长。法国、德国、荷兰、英国、西班牙和丹麦是主要的欧洲市场。这家欧洲公司也是食品和饮料产品的主要出口商。法国是食品的主要出口国,包括乳製品、肉类、葡萄酒和加工食品。为了满足国际市场对法国食品日益增长的需求,食品加工商需要有效率、可靠的设施,能够扩大生产规模以满足出口需求,同时保持产品品质和一致性。例如,根据欧盟统计局的数据,到 2022 年,法国起司产量将达到 665,400 吨,而 2020 年为 657,060 吨。同样,根据联合国商品贸易统计资料库的数据,法国新鲜、冷藏和冷冻形式的羊肉或山羊肉出口额将增加,到 2022 年将达到 3.4061 亿欧元,高于 2021 年的 2.9729 亿欧元。

永续性和环境责任在食品业变得越来越重要。为了实现永续性目标并减少对环境的影响,食品加工商正在投资能够减少能源消耗、减少废弃物和优化资源利用的设备。需要具有节能技术、水循环系统和废弃物减少措施等特点的设施来支持永续的食品生产实践。这促使公司开始生产配备节能技术的食品加工机器。例如,OctoFrost Processing Solutions 提供节能的食品加工机械,特别是在冷冻和热处理领域。该公司提供创新的解决方案,旨在优化能源使用,同时保持食品品质和完整性。

食品加工机械产业概况

全球食品加工机械市场由各国的区域性和国家性参与者主导,其中国内参与者比跨国参与者更受青睐,拥有更高的市场占有率。全球食品加工机械市场的主要参与者包括 JBT Corporation、Buhler AG、Krones AG、Marel 和 Tetra Laval。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场驱动因素

- 加工食品需求不断增加

- 技术进步支持市场成长

- 市场限制

- 能源和人事费用上升导致生产成本上升

- 波特五力分析

- 新进入者的威胁

- 购买者和消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场区隔

- 类型

- 加工机械设备

- 包装器材及设备

- 实用工具

- 应用

- 乳製品和乳製品替代品

- 肉类、鱼贝类以及肉类和鱼贝类替代品

- 麵包和糖果零食

- 饮料

- 水果、蔬菜和坚果

- 其他用途

- 地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 北美其他地区

- 欧洲

- 英国

- 德国

- 法国

- 俄罗斯

- 义大利

- 西班牙

- 其他欧洲国家

- 亚太地区

- 印度

- 中国

- 日本

- 澳洲

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 其他中东和非洲地区

- 北美洲

第六章 竞争格局

- 最受欢迎的策略

- 市场占有率分析

- 公司简介

- Anko Food Machine

- Buhler AG

- GEA

- Krones AG

- Tetra Laval

- Atlas Pacific Engineering Co. Inc.

- Bean(John)Technologies Corp.

- Hosokawa Micron Corp.

- Nichimo Co. Ltd

- Satake Corp.

- Spx Corp.

- Tomra Systems ASA

第七章 市场机会与未来趋势

The Food Processing Machinery Market size is estimated at USD 107.00 billion in 2025, and is expected to reach USD 141.24 billion by 2030, at a CAGR of 5.71% during the forecast period (2025-2030).

The shift in consumer preferences toward convenient and ready-to-eat food products is driving the need for sophisticated processing equipment. Evolving consumer lifestyles are characterized by an increasing reliance on time-saving solutions and ready-to-consume food products. This paradigm shift necessitates an evolution in food processing equipment to meet the growing expectations for efficiency, variety, and quality in the production of convenience foods. Manufacturers are investing in equipment that allows for the efficient processing of a wide variety of convenience food products. The growing demand for processed foods from developing nations worldwide and government incentives, such as reimbursement on equipment, are also among the factors driving demand from the growing markets.

For instance, according to the Agricultural & Processed Food Products Export Development Authority (APEDA), the export value of processed food and products from India in 2021 amounted to USD 390.99 billion for processed vegetables and USD 780.19 for processed fruits, juices, and nuts.

Processed food demand and consumption have been steadily increasing, which is a major driver for the industry. Despite being a global phenomenon, this desire is particularly prevalent in underdeveloped countries. The food processing industry in nations like India and China has fundamentally evolved as a result of recent economic success and increased market openness to international commodities. An increase in meat eating is one of the most significant consequences of this. One of the fastest-expanding segments, especially in developing nations, is the meat processing equipment segment.

The developed markets of Western Europe, the United States, and Canada are witnessing a strong demand for processing and packaging equipment from the bakery and beverage industries. The increasing popularity of functional beverages has escalated the demand for equipment that is utilized in the production of non-alcoholic drinks and dairy-based beverage products.

Moreover,food equipment manufacturers are developing new ways of working by investing in new capabilities, like advanced data and analytics, robotics, and automation, to attract more processors. The integration of Internet of Things (IoT) technologies and smart sensors in food processing equipment is a notable trend. This enables real-time monitoring, predictive maintenance, and data-driven decision-making, enhancing overall operational efficiency. The key market players are focused on providing machinery with high efficiency to cater to the demand from food processors.

Food Processing Machinery Market Trends

Increasing Automation in Food and Beverage Processing

Advances in food processing equipment technology have led to improved efficiency, productivity, and product quality. Automation, robotics, IoT integration, artificial intelligence, and data analytics are being increasingly adopted to streamline operations, reduce labor costs, and enhance food safety and traceability. Automation is helping reduce production time while increasing output as demand and costs continue to rise. Food processors are increasingly aware of the value of data-driven insights in maximizing the utilization of raw materials, ensuring traceability and support for constant improvement, and improving food quality and safety. The robotic butchery machine, which helps speed up the process, is among the most common types of automation gear. This automated equipment also makes facilities safer since it reduces the amount of personnel handling potentially harmful tools and apparatus.

For instance, in November 2023, the University of Birmingham Enterprise launched EvoPhase. It uses evolutionary AI algorithms, coupled with simulations of particulates in systems such as industrial mixers, to evolve an optimized design for the mixing blade and the shape or size of the blending vessel. EvoPhase offers a diverse range of process equipment, including mills, dryers, roasters, coaters, fluidized beds, and stirred tanks, and is expected to result in huge cost and energy savings for the industry.

The meat, baking, and dairy segments of the market are among the major segments adopting automation in terms of processing and packaging, resulting in increased production efficiency in the market. With a significant number of players operating in the market, technical advancements in terms of automation are expected to drive the market in a positive direction over the coming years.

Europe Holds the Largest Market Share

Europe, one of the prominent regional markets, is likely to witness significant growth over the coming years owing to the growing demand for high-quality systems. France, Germany, the Netherlands, the United Kingdom, Spain, and Denmark are the important markets in Europe. Firms belonging to Europe are also major exporters of food and beverage products. France is a major exporter of food products, including dairy, meats, wines, and processed foods. To meet the growing demand for French food products in international markets, food processors require efficient and reliable equipment that can scale production to meet export requirements while maintaining product quality and consistency. For example, according to Eurostat, the volume of cheese from France reached 665.4 thousand tons in 2022, while it was 657.06 thousand tons in 2020. Similarly, according to UN Comtrade, the export of meat from sheep or goats, in fresh, chilled, and frozen forms, in France increased and reached EUR 340.61 million in 2022, registering an increase from EUR 297.29 million in 2021.

There is a growing emphasis on sustainability and environmental responsibility in the food industry. Food processors are investing in equipment that reduces energy consumption, minimizes waste, and optimizes the use of resources to achieve sustainability goals and reduce their environmental footprint. Equipment with features such as energy-efficient technologies, water recycling systems, and waste reduction measures are in demand to support sustainable food production practices. Thus, companies have started to manufacture food processing machinery with energy-efficient technology. For example, OctoFrost Processing Solutions provides energy-efficient food processing machinery, particularly in the fields of freezing and thermal processing. The company offers innovative solutions designed to optimize energy usage while maintaining the quality and integrity of food products.

Food Processing Machinery Industry Overview

The global food processing machinery market includes the presence of large regional and domestic players across different countries, with domestic companies having gained preference over multinationals with a higher market share. Some of the major players in the global food processing machinery market include JBT Corporation, Buhler AG, Krones AG, Marel, and Tetra Laval.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasing Demand for Processed Food Products

- 4.1.2 Technological Advancements Supporting Market Growth

- 4.2 Market Restraints

- 4.2.1 Increasing Cost of Production Due to Rise in Energy and Labor Cost

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Processing Machinery and Equipment

- 5.1.2 Packaging Machinery and Equipment

- 5.1.3 Utilities

- 5.2 Application

- 5.2.1 Dairy and Dairy Alternatives

- 5.2.2 Meat/Seafood and Meat/Seafood Alternatives

- 5.2.3 Bakery and Confectionery

- 5.2.4 Beverages

- 5.2.5 Fruits, Vegetables, and Nuts

- 5.2.6 Other Applications

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Italy

- 5.3.2.6 Spain

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Anko Food Machine

- 6.3.2 Buhler AG

- 6.3.3 GEA

- 6.3.4 Krones AG

- 6.3.5 Tetra Laval

- 6.3.6 Atlas Pacific Engineering Co. Inc.

- 6.3.7 Bean (John) Technologies Corp.

- 6.3.8 Hosokawa Micron Corp.

- 6.3.9 Nichimo Co. Ltd

- 6.3.10 Satake Corp.

- 6.3.11 Spx Corp.

- 6.3.12 Tomra Systems ASA

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

食品加工机械市场规模、份额、成长分析(按类型、营运、应用和地区)- 2025-2032 年产业预测

食品加工机械市场规模、份额、成长分析(按类型、营运、应用和地区)- 2025-2032 年产业预测 乳酪加工设备市场按产品类型、技术、产能、乳酪类型、最终用户和分销管道划分 - 全球预测 2025-2032商用奶昔机市场按类型、最终用户、销售管道、容量、技术和电源划分-2025年至2032年全球预测商用烤肉设备市场(按设备类型、最终用户、动力来源、应用和容量划分)-全球预测(2025-2032年)工业蒸汽去皮机市场:依终端用户产业、设备类型、操作模式、技术及销售管道划分-2025-2032年全球预测工业食品铣床切割机市场:按机器类型、材料、应用、最终用户、技术类型和自动化程度划分 - 全球预测(2025-2032 年)水果加工市场按产品类型、通路、水果品种和最终用途划分-2025年至2032年全球预测腌製和滚揉设备市场按类型、应用、最终用户、技术和产能划分 - 全球预测(2025-2032 年)食品加工和包装设备市场:按设备类型、应用、最终用户产业、包装材料、加工技术和自动化程度划分 - 全球预测(2025-2032年)食品加工和处理设备市场:按设备类型、操作模式、技术、最终用户、产能和设备材料划分-2025-2032年全球预测

乳酪加工设备市场按产品类型、技术、产能、乳酪类型、最终用户和分销管道划分 - 全球预测 2025-2032商用奶昔机市场按类型、最终用户、销售管道、容量、技术和电源划分-2025年至2032年全球预测商用烤肉设备市场(按设备类型、最终用户、动力来源、应用和容量划分)-全球预测(2025-2032年)工业蒸汽去皮机市场:依终端用户产业、设备类型、操作模式、技术及销售管道划分-2025-2032年全球预测工业食品铣床切割机市场:按机器类型、材料、应用、最终用户、技术类型和自动化程度划分 - 全球预测(2025-2032 年)水果加工市场按产品类型、通路、水果品种和最终用途划分-2025年至2032年全球预测腌製和滚揉设备市场按类型、应用、最终用户、技术和产能划分 - 全球预测(2025-2032 年)食品加工和包装设备市场:按设备类型、应用、最终用户产业、包装材料、加工技术和自动化程度划分 - 全球预测(2025-2032年)食品加工和处理设备市场:按设备类型、操作模式、技术、最终用户、产能和设备材料划分-2025-2032年全球预测