|

市场调查报告书

商品编码

1686281

耐火材料:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Refractories - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

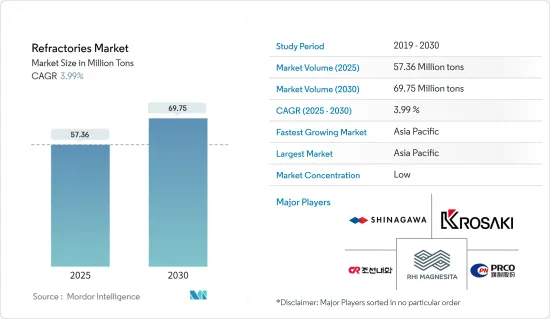

预计 2025 年耐火材料市场规模为 5,736 万吨,到 2030 年将达到 6,975 万吨,预测期内(2025-2030 年)的复合年增长率为 3.99%。

新冠肺炎疫情对全球经济产生了重大影响,许多国家进入封锁状态,经济和工业活动暂时停止。耐火材料市场也受到钢铁、水泥、能源、化学品和陶瓷等终端用户产业的生产和需求的影响。然而,在疫情后时期,由于经济开放后对产品的需求,终端用户产业正在成长。

主要亮点

- 钢铁业对耐火材料的需求大幅增长以及水泥和能源行业的需求增加正在推动耐火材料市场的成长。

- 环境和健康问题以及相关的准则和法规正在影响市场动态,并部分限制耐火材料市场的工业运作。

- 增加耐火材料回收的投资和研究为耐火材料市场的成长提供了重大机会。

- 预计亚太地区将引领市场,其中中国、印度和日本在预测期内占据大部分市场份额。

耐火材料市场趋势

钢铁业需求增加

- 耐火材料在钢铁业中至关重要,可以保护高温设备和製程。耐火材料可保护高炉零件(如炉床和炉腹)免受极端高温和腐蚀性炉渣的侵害。碱性氧气转炉 (BOF) 和电弧炉 (EAF) 依靠这些内衬来抵御炼钢的挑战。

- 根据美国地质调查局预测,2023年全球可用铁矿石产量将达25亿吨。澳洲铁矿石出口量为9.6亿吨,占全球铁矿石出口总额910亿美元的56.4%。

- 据印度品牌股权基金会称,到 2023 年,印度的铁矿石产量将增至创纪录的 2.82 亿吨,与前一年同期比较增长 14%。奥里萨邦的矿石产量占印度总矿石量的 56%,成长 18%,达到 1.59 亿吨。印度八大公司矿业产量总合超过2,000万吨。

- 根据世界钢铁协会的初步资料,2023年1-11月全球粗钢产量达17.1512亿吨,年增0.5%。 11月份,全国粮食产量达1.455亿吨,与前一年同期比较增加3.3%。

- 总之,钢铁业的产量和需求都呈现显着成长,凸显了耐火材料的重要作用以及铁矿石供应在支持此扩张的重要性。

亚太地区占市场主导地位

- 在亚太地区,中国是最大的经济体,在全球製造和生产中发挥主要企业。中国拥有丰富的原料供应,在耐火材料消费和生产方面均占主导地位。

- 中国是世界最大的钢铁生产国,占全球产量的一半以上,根据世界钢铁协会的报告,预计2023年中国钢铁产量将维持稳定在10.191亿吨左右,与2022年的数字持平。

- 此外,根据中国石油天然气集团公司研究院报告预测,2023年中国精製能力将增加至9.36亿吨/年,精製油消费量将年增与前一年同期比较%至3.99亿吨。

- 世界钢铁协会预计,印度2023年粗钢产量将从2022年的1.244亿吨增加11.80%至1.402亿吨。值得注意的是,光是2024年10月份的钢铁产量就达到1,250万吨,与前一年同期比较增1.7%。

- 2024 年 2 月,JSW 集团宣布计划在奥里萨邦 Jagatsinghpur 投资一座大型钢铁厂,年产量目标为 1,320 万吨。同时,AMNS印度公司正在投资74亿美元扩大产能并增加其上下游领域的价值,显示市场前景乐观。

- 第三大粗钢生产国日本预计 2023 年其钢铁产量将从 2022 年的 8,920 万吨下降 2.5% 至 8,700 万吨。 2024 年 10 月钢铁产量为 690 万吨,与前一年同期比较减 7.8%。

- 积极的一面是,JFE钢铁公司已获得资金,将在其位于仓敷的西日本工厂建造一座大型电弧炉(EAF),以取代现有的2号高炉,该高炉计划于2027/2028财年开始试运行,并于2027年4月1日开始运营。

- 总之,儘管面临日本的挑战,亚太地区,特别是中国和印度,钢铁和耐火材料市场仍经历动态成长,凸显了该地区在全球工业格局中的关键作用。

耐火材料产业概况

耐火材料市场高度分散。主要企业(不分先后顺序)包括RHI Magnesita NV、Krosaki Harima Corporation、濮阳耐火材料集团、朝鲜耐火材料、Shinagawa Refractories等。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 钢铁业更多使用耐火材料

- 水泥和能源产业对耐火材料的需求不断增加

- 限制因素

- 与耐火材料相关的环境和健康风险

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场区隔

- 产品类型

- 非黏土耐火材料

- 菱镁砖

- 锆砖

- 硅砖

- 铬砖

- 其他产品类型(碳化物、硅酸盐)

- 黏土耐火材料

- 高铝土

- 耐火粘土

- 隔热材料

- 非黏土耐火材料

- 最终用户产业

- 钢

- 能源与化工

- 非铁金属

- 水泥

- 陶瓷製品

- 玻璃

- 其他最终用户产业

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作、协议

- 市场占有率(%)分析

- 主要企业策略

- 公司简介

- Chosun Refractories

- HWI(Platinum Equity Advisors, LLC)

- Imerys

- Krosaki Harima Corporation

- Puyang Refractories Group Co., Ltd

- Refratechnik

- RHI Magnesita NV

- Saint-Gobain

- Shinagawa Refractories Co. Ltd

- Vesuvius

- List of Other Prominent Companies

第七章 市场机会与未来趋势

- 扩大耐火材料回收的投资与研究

The Refractories Market size is estimated at 57.36 million tons in 2025, and is expected to reach 69.75 million tons by 2030, at a CAGR of 3.99% during the forecast period (2025-2030).

Due to COVID-19, numerous countries were in lockdown, significantly affecting the global economy and economic and industrial activities were temporarily halted. The refractories market also witnessed repercussions in production and demand from the end-user industries, such as iron and steel, cement, energy and chemicals, ceramics, etc. However, in the post-pandemic period, the end-user industries are growing because of the demand for products after economies open up.

Key Highlights

- The significant demand for refractories in the iron and steel industry, along with increasing requirements from the cement and energy sectors, is driving the growth of the refractories market.

- Environmental and health concerns, along with the resulting guidelines and regulations, impact market dynamics and partially constrain industry operations in the refractories market.

- Increasing investments and research focused on the recycling of refractories present significant opportunities for growth in the refractories market.

- The Asia-Pacific region is projected to lead the market, with China, India, and Japan accounting for the majority of its share during the forecast period.

Refractories Market Trends

Increasing Demand from the Iron and Steel Industry

- Refractories are essential in the iron and steel industry, protecting high-temperature equipment and processes. They shield blast furnace components, such as the hearth and bosh, from extreme heat and corrosive slag. Basic Oxygen Furnaces (BOFs) and Electric Arc Furnaces (EAFs) rely on these linings to withstand the challenges of steelmaking.

- In 2023, global production of usable iron ore reached an estimated 2.5 billion metric tons, according to the United States Geological Survey. Australia led with 960 million metric tons, accounting for 56.4% of the world's iron ore exports, valued at USD 91 billion.

- According to the India Brand Equity Foundation, India set a record by increasing its iron ore production to 282 million tons in 2023, a nearly 14% rise from the previous year. Odisha, contributing 56% of India's ore, boosted its output by 18% to 159 million tons. The top eight mining firms in India collectively exceeded 20 million tons in production.

- According to provisional data from the World Steel Association, global crude steel production reached 1,715.12 million tons (mt) from January to November 2023, marking a year-on-year growth of 0.5%. Production hit 145.5 million tons in November alone, reflecting a 3.3% increase from the previous year.

- In conclusion, the iron and steel industry is witnessing significant growth in both production and demand, underscoring the vital role of refractories and the importance of iron ore supply in supporting this expansion.

Asia-Pacific region to Dominate the Market

- In the Asia-Pacific region, China stands out as the largest economy and a major player in global manufacturing and production. Its abundant supply of raw materials enables China to dominate the refractories market in both consumption and production.

- As the world's leading steel producer, China accounted for over half of global output, with the World Steel Association reporting steel production remained stable at approximately 1,019.1 million tons in 2023, consistent with 2022 figures.

- Additionally, a report from a research institute under the China National Petroleum Corporation revealed that China's annual oil refining capacity increased to 936 million tons in 2023, while refined oil consumption rose by 9.5% year-on-year to 399 million tons.

- In India, the World Steel Association noted a remarkable 11.80% increase in crude steel production for 2023, reaching 140.2 million tons, up from 124.4 million tons in 2022. Notably, October 2024 alone recorded steel production of 12.5 million tons, reflecting a 1.7% increase from the previous year.

- In February 2024, the JSW Group announced plans for a steel plant in Jagatsinghpur, Odisha, with a significant investment of USD 7.8 billion (Rs. 65,000 crore), targeting an annual production of 13.2 million tons. Concurrently, AMNS India is investing USD 7.4 billion in capacity expansion and value-added initiatives across upstream and downstream sectors, indicating a positive market outlook.

- Japan, the third-largest producer of crude steel, experienced a 2.5% decline in steel output in 2023, with production dropping to 87.0 million tons from 89.2 million tons in 2022. In October 2024, steel production was recorded at 6.9 million tons, marking a 7.8% decrease from the previous year.

- On a positive note, JFE Steel is securing funding to construct a significant electric arc furnace (EAF) at its West Japan Works in Kurashiki, set to replace the existing blast furnace No. 2, with commissioning anticipated in the fiscal year 2027/2028, starting April 1, 2027.

- In conclusion, the Asia-Pacific region, particularly China and India, is experiencing dynamic growth in the steel and refractories markets, despite challenges in Japan, highlighting the region's critical role in the global industrial landscape.

Refractories Industry Overview

The refractories market is highly fragmented in nature. The major players (not in any particular order) include RHI Magnesita N.V., Krosaki Harima Corporation, Puyang Refractories Group Co., Ltd, Chosun Refractories, and Shinagawa Refractories Co., Ltd, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Substantial Usage of Refractories in the Iron and Steel Industry

- 4.1.2 Growing Demand for Refractories from Cement and Energy Sectors

- 4.2 Restraints

- 4.2.1 Environmental and Health Risks Associated with Refractories

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Product Type

- 5.1.1 Non-clay Refractory

- 5.1.1.1 Magnesite Brick

- 5.1.1.2 Zirconia Brick

- 5.1.1.3 Silica Brick

- 5.1.1.4 Chromite Brick

- 5.1.1.5 Other Product Types (Carbides, Silicates)

- 5.1.2 Clay Refractory

- 5.1.2.1 High Alumina

- 5.1.2.2 Fireclay

- 5.1.2.3 Insulating

- 5.1.1 Non-clay Refractory

- 5.2 End-user Industry

- 5.2.1 Iron and Steel

- 5.2.2 Energy and Chemicals

- 5.2.3 Non-ferrous Metals

- 5.2.4 Cement

- 5.2.5 Ceramic

- 5.2.6 Glass

- 5.2.7 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-east and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Chosun Refractories

- 6.4.2 HWI (Platinum Equity Advisors, LLC)

- 6.4.3 Imerys

- 6.4.4 Krosaki Harima Corporation

- 6.4.5 Puyang Refractories Group Co., Ltd

- 6.4.6 Refratechnik

- 6.4.7 RHI Magnesita N.V.

- 6.4.8 Saint-Gobain

- 6.4.9 Shinagawa Refractories Co. Ltd

- 6.4.10 Vesuvius

- 6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Investments and Research on the Recycling of Refractories

耐火砖市场规模、份额、成长分析(按原料、按应用、按製造流程、按形状、按特性、按地区)-2025-2032 年产业预测

耐火砖市场规模、份额、成长分析(按原料、按应用、按製造流程、按形状、按特性、按地区)-2025-2032 年产业预测 耐火材料市场规模、份额、成长分析(按类型、产品、碱、最终用途产业和地区)-2025-2032 年产业预测

耐火材料市场规模、份额、成长分析(按类型、产品、碱、最终用途产业和地区)-2025-2032 年产业预测 2032 年耐火材料市场预测:按形式、材料、碱度、製造流程、最终用户和地区分類的全球分析

2032 年耐火材料市场预测:按形式、材料、碱度、製造流程、最终用户和地区分類的全球分析 高强度耐火耐火材料市场(按成分、类型、耐热性、形式、应用和最终用途)—2025-2030 年全球预测

高强度耐火耐火材料市场(按成分、类型、耐热性、形式、应用和最终用途)—2025-2030 年全球预测 2025年全球耐火材料市场报告

2025年全球耐火材料市场报告 耐火材料市场规模、份额和趋势分析报告:按最终用途、地区和细分市场预测,2025-2033 年

耐火材料市场规模、份额和趋势分析报告:按最终用途、地区和细分市场预测,2025-2033 年 耐火材料市场规模、份额、趋势及预测(按形式、碱度、製造工艺、成分、耐火矿物、应用和地区),2025 年至 2033 年日本耐火材料市场报告(按形式、碱度、製造工艺、成分、耐火矿物、应用和地区)2025-2033刚玉和莫来石耐火砖市场按原料类型、製造流程、热容量、应用和最终用户产业划分 - 2025-2030 年全球预测2030 年再生耐火材料市场预测:按类型、材料、製程、应用、最终用户和地区进行的全球分析

耐火材料市场规模、份额、趋势及预测(按形式、碱度、製造工艺、成分、耐火矿物、应用和地区),2025 年至 2033 年日本耐火材料市场报告(按形式、碱度、製造工艺、成分、耐火矿物、应用和地区)2025-2033刚玉和莫来石耐火砖市场按原料类型、製造流程、热容量、应用和最终用户产业划分 - 2025-2030 年全球预测2030 年再生耐火材料市场预测:按类型、材料、製程、应用、最终用户和地区进行的全球分析