|

市场调查报告书

商品编码

1686300

丙烯腈丁二烯苯乙烯 (ABS) 树脂:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Acrylonitrile Butadiene Styrene (ABS) Resin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

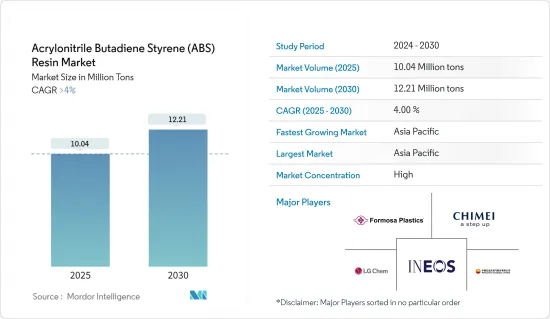

丙烯腈丁二烯苯乙烯 (ABS) 树脂市场规模预计在 2025 年为 1,004 万吨,预计在 2030 年达到 1,221 万吨,预测期间(2025-2030 年)的复合年增长率将超过 4%。

ABS 树脂市场受到 COVID-19 的严重影响。由于经济放缓,市场面临劳动力短缺、运输和原材料短缺等多重挑战。然而,随着大多数国家放鬆封锁措施后全球製造和进出口活动迅速增加,对 ABS 树脂的需求正在激增。

主要亮点

- 推动市场发展的首要因素是人们对汽车轻量化的日益关注以及在电子和消费品领域的应用不断扩大。

- 然而,预计 ABS 替代品的可用性是预测期内抑制该行业成长的主要因素。

- 然而,PC-ABS树脂在工业应用中的使用越来越广泛,可能为全球市场提供有利的成长机会。

- 亚太地区占全球市场主导地位,其中中国和印度等国家消费量最高。

丙烯腈丁二烯苯乙烯 (ABS) 树脂的市场趋势

电子及家电产业需求不断成长

- ABS 在电子领域的应用主要包括传输电力的塑胶零件。这包括盒子、外壳、线槽、塑胶机壳等。

- ABS树脂具有优异的抗衝击性、耐久性、重量轻和阻燃性。因此在电子设备中被广泛应用。此外,随着电子元件日益小型化以及整个产业的安全措施不断加强,电子应用对 ABS 树脂的需求预计将会增加。

- 全球电子产业正在经历巨大的成长。亚太地区占全球电子产品产量的70%以上,韩国、日本和中国等国家参与製造各种电气元件并供应全球各产业。此外,预计2025年印度将成为全球第五大家电和电子产业国。

- 预计2024年中国消费电子市场将反弹并实现正成长。中国家电零售总额预计将达到人民币2.2兆元(3,050亿美元),预计2024年成长率将进一步回升至5%。

- 由于终端消费者的需求旺盛,德国的电气和电子产业在欧洲占有最大的份额。此外,该行业还得到了跨国电子製造商的大力支持,满足了该国广泛的需求。电气工程业占德国工业总产值的11%。

- 在美国,电子产业的发展主要靠家用电子电器的销售。此外,由于美国工业活动的不断增加,工业电子在过去十年中发展势头强劲。预计电视、行动电话电脑和智慧型装置等家用电子电器的高需求将增加塑胶产品的使用量,对市场产生正面影响。

- 在预测期内,ABS 树脂市场可能会受到全球电子和家电行业持续扩张的推动。

亚太地区占市场主导地位

- 随着 ABS 树脂在蓬勃发展的汽车产业中取代传统塑料,亚太地区的 ABS 树脂市场正在快速成长。

- 在全球汽车总产量约6,900万辆中,中国产量约占34%。根据欧洲汽车工业协会(ACEA)的数据,日本和韩国占其中的14.7%,南亚约占10.8%。

- 而且,中国的汽车製造业是全世界最大的。根据国际汽车工业组织(OICA)的数据,该国的汽车产量将在2022年达到2,700万辆,比2021年的2,608万辆增加3%。

- 据估计,中国是世界上最大的电子製造基地之一。智慧型手机、电视、电线电缆、可携式电脑、游戏系统和其他个人电子设备等电子产品在电子产业中录得最高成长。预计这将促进该国的 ABS 消费。

- 据印度投资局称,印度电子产品市场价值 1,550 亿美元,其中 65% 来自国内市场。显示器市场正在成长,预计到 2025 年将成长到 150 亿美元。 23 财年,印度的电子产品进口额成长 8%,达到 878.5 亿美元。此外,印度国内生产年复合成长率率为 13%,从 2017 财年的490 亿美元增至 2023 财年的总合亿美元。

- 日本政府正在增加对电动车的补贴,并计划在2030年将电动车充电站的数量增加到15万个。因此,汽车产业的復苏可能会提振日本的ABS市场。

- 根据世界银行预测,2022年韩国家庭人均支出与前一年同期比较增加4.6%。这种支出增加的趋势可能会在未来几年促进许多使用丙烯腈丁二烯苯乙烯 (ABS) 的产品的销售,包括汽车、家用电器等。

- 因此,预计所有这些因素都将在预测期内影响亚太地区对丙烯腈丁二烯苯乙烯 (ABS) 树脂市场的需求。

丙烯腈丁二烯苯乙烯 (ABS) 树脂产业概况

丙烯腈丁二烯苯乙烯 (ABS) 树脂市场本质上是整合的。主要企业(不分先后顺序)包括 LG 化学、奇美、英力士、台塑和中国石油天然气有限公司。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 人们对轻型汽车的兴趣日益浓厚

- 在电子产品和消费品中的应用日益广泛

- 限制因素

- ABS 替代方案的可用性

- 其他阻碍因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 价格趋势

- 监理政策

第五章 市场区隔

- 行程类型

- 注射吹塑成型

- 挤出吹塑成型

- 注拉伸吹塑成型

- 最终用户产业

- 汽车和运输

- 建筑学

- 电子产品

- 消费品和家用电器

- 其他最终用户产业

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 泰国

- 越南

- 马来西亚

- 印尼

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 俄罗斯

- 土耳其

- 北欧的

- 西班牙

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 卡达

- 奈及利亚

- 阿拉伯聯合大公国

- 埃及

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- ABS树脂製造商

- CHIMEI

- Formosa Plastics Corporation

- LOTTE Chemical Corporation

- PetroChina Company Limited

- JSR Corporation

- Trinseo

- INEOS Styrolution Group GmbH

- LG Chem

- SABIC

- TORAY INDUSTRIES INC.

- Springboard(Stack Plastics)

- DONGGUAN SINCERE TECH CO. LTD

- Jaco Products

- ReblingPower Connectors

- AcoMold Co Limited

- Rutland Plastics

- HTI Plastics

- EX MOULD Co. Ltd

- ABS树脂製造商

第七章 市场机会与未来趋势

- 扩大 PC-ABS 树脂在工业应用的使用

The Acrylonitrile Butadiene Styrene Resin Market size is estimated at 10.04 million tons in 2025, and is expected to reach 12.21 million tons by 2030, at a CAGR of greater than 4% during the forecast period (2025-2030).

The ABS resin market has been significantly impacted due to COVID-19. The market has faced several challenges, such as labor shortages, transportation, and raw material shortages due to the economic slowdown. However, after the relaxation of the lockdown process in most countries, demand for ABS resins is surging as global manufacturing and export-import activities are rapidly increasing.

Key Highlights

- Major factors driving the market are the growing focus on lightweight automobiles and the increasing usage of electronics and consumer goods.

- However, the availability of substitutes for ABS is a key factor anticipated to restrain the growth of the target industry during the forecast period.

- However, the growing usage of PC-ABS resin in industrial applications will likely create lucrative growth opportunities in the global market.

- Asia-Pacific dominated the global market, with the largest consumption from countries like China and India.

Acrylonitrile Butadiene Styrene (ABS) Resin Market Trends

Increasing Demand in the Electronics and Appliances Industry

- The electronics applications for ABS resin mainly include plastic components for electricity transfer. These include boxes, casings, wiring channels, and plastic enclosures.

- ABS plastics are impact-resistant, durable, lightweight, and flame-retardant. Thus, they are widely used in electronics. Moreover, the growing miniaturization of electronic components and increased safety measures across industries are expected to increase the demand for ABS resin in electronics applications.

- The global electronics industry has witnessed massive growth. Asia-Pacific accounts for more than 70% of global electronics production, with countries like South Korea, Japan, and China involved in manufacturing various electrical components and supplying them to various industries globally. Additionally, India is expected to become the world's fifth-largest consumer electronics and appliances industry by 2025.

- China's consumer electronics market is set to bounce back with positive growth in 2024, driven by growing market demand and innovation while increasing retail spending. China's total retail sales of consumer electronics are expected to reach CNY 2.2 trillion (USD 305 billion), and the growth rate is expected to increase further to 5% in 2024.

- The German electrical and electronics industry in Europe accounts for the largest share due to high end-consumer demand. Moreover, the industry is supported by a strong presence of multinational electronics manufacturers catering to the wide demand in the country. The electrical industry accounted for 11% of the total industrial production in Germany.

- The sales of consumer electronics primarily drive the electronics industry in the United States. Moreover, industrial electronics have gained momentum in the past decade owing to the rise in industrial operations across the United States. The high demand for consumer electronics, including television, mobile phones, laptops, and smart gadgets, is expected to increase the utilization of plastic products, thereby positively impacting the market.

- During the forecast period, the market for ABS resin is likely to be driven by continued expansion in the global electronics and appliances industry.

Asia-Pacific to Dominate the Market

- The market for ABS witnessed rapid growth in Asia-Pacific, owing to the increased replacement of traditional plastics by ABS in the growing automotive industry.

- China manufactures about 34% of approximately 69 million cars worldwide each year. Japan and South Korea account for 14.7% of that volume, and South Asia accounts for around 10.8% of that volume, according to the European Automobile Manufacturers Association (ACEA).

- Moreover, the Chinese automotive manufacturing industry is the largest in the world. In 2022, the automotive production in the country reached 27 million, which increased by 3%, compared to 26.08 million vehicles produced in 2021, according to the International Organization of Motor Vehicle Manufacturers (OICA)

- China is estimated to be one of the world's largest electronics production bases. Electronic products, such as smartphones, TVs, wires, cables, portable computing devices, gaming systems, and other personal electronic devices, recorded the highest growth in the electronics segment. This is expected to drive the country's consumption of ABS.

- As per Invest India, the electronics market in India is worth USD 155 billion, with 65% of the total market being domestic. The display market is growing and is expected to grow to USD 15 billion by 2025. In FY23, electronic goods imported into India increased 8% to USD 87.85 billion. Moreover, India's domestic production registered a 13% compound annual growth rate from FY17's total of USD 49 billion to FY23's total of USD 101 billion.

- The Government of Japan has raised subsidies for EVs and aims to increase the number of EV charging stations to 150,000 by 2030. Thus, reviving the automotive industry is likely to boost the ABS market in the country.

- According to the World Bank, household expenditure per capita in South Korea grew 4.6% in 2022 over the previous year. Such growth trends in expenditure will increase the sales of numerous products, including automotive, consumer electronics, and others that utilize acrylonitrile butadiene styrene (ABS) in the coming years.

- Therefore, all these factors are expected to affect the demand in the Asia-Pacific acrylonitrile butadiene styrene resin market during the forecast period.

Acrylonitrile Butadiene Styrene (ABS) Resin Industry Overview

The acrylonitrile butadiene styrene (ABS) resin market is consolidated in nature. Some major key players (not in any particular order) include LG Chem, CHIMEI, INEOS, Formosa Plastics, and PetroChina Company Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Focus on Lightweight Automobiles

- 4.1.2 Increasing Usage in Electronics and Consumer Goods

- 4.2 Restraints

- 4.2.1 Availability of Substitutes for ABS

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Price Trends

- 4.6 Regulatory Policies

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Process Type

- 5.1.1 Injection Blow Molding

- 5.1.2 Extrusion Blow Molding

- 5.1.3 Injection Stretch Blow Molding

- 5.2 End-user Industry

- 5.2.1 Automotive and Transportation

- 5.2.2 Construction

- 5.2.3 Electronics

- 5.2.4 Consumer Goods and Appliances

- 5.2.5 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Thailand

- 5.3.1.6 Vietnam

- 5.3.1.7 Malaysia

- 5.3.1.8 Indonesia

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Turkey

- 5.3.3.7 NORDIC

- 5.3.3.8 Spain

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Qatar

- 5.3.5.4 Nigeria

- 5.3.5.5 United Arab Emirates

- 5.3.5.6 Egypt

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Manufacturers of ABS Resins

- 6.4.1.1 CHIMEI

- 6.4.1.2 Formosa Plastics Corporation

- 6.4.1.3 LOTTE Chemical Corporation

- 6.4.1.4 PetroChina Company Limited

- 6.4.1.5 JSR Corporation

- 6.4.1.6 Trinseo

- 6.4.1.7 INEOS Styrolution Group GmbH

- 6.4.1.8 LG Chem

- 6.4.1.9 SABIC

- 6.4.1.10 TORAY INDUSTRIES INC.

- 6.4.1.11 Springboard (Stack Plastics)

- 6.4.1.12 DONGGUAN SINCERE TECH CO. LTD

- 6.4.1.13 Jaco Products

- 6.4.1.14 ReblingPower Connectors

- 6.4.1.15 AcoMold Co Limited

- 6.4.1.16 Rutland Plastics

- 6.4.1.17 HTI Plastics

- 6.4.1.18 EX MOULD Co. Ltd

- 6.4.1 Manufacturers of ABS Resins

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing usage of PC-ABS Resin in Industrial Applications

丙烯腈丁二烯苯乙烯市场分析及预测(至2034年):类型、产品、应用、形式、材料类型、製程、最终用户、技术、功能

丙烯腈丁二烯苯乙烯市场分析及预测(至2034年):类型、产品、应用、形式、材料类型、製程、最终用户、技术、功能 全球丙烯腈丁二烯苯乙烯 (ABS) 市场研究报告 - 产业分析、规模、份额、成长、趋势及预测(2025 年至 2033 年)全球丙烯腈丁二烯苯乙烯市场规模(依最终用户、应用、技术、区域范围、预测)

全球丙烯腈丁二烯苯乙烯 (ABS) 市场研究报告 - 产业分析、规模、份额、成长、趋势及预测(2025 年至 2033 年)全球丙烯腈丁二烯苯乙烯市场规模(依最终用户、应用、技术、区域范围、预测) 全球再生 ABS 树脂市场:2031 年预测

全球再生 ABS 树脂市场:2031 年预测 全球丙烯腈丁二烯苯乙烯市场报告:趋势、预测和竞争分析(至 2031 年)丙烯腈丁二烯苯乙烯市场规模、份额、趋势分析报告:按类型、应用、地区、细分市场预测,2025-2030 年

全球丙烯腈丁二烯苯乙烯市场报告:趋势、预测和竞争分析(至 2031 年)丙烯腈丁二烯苯乙烯市场规模、份额、趋势分析报告:按类型、应用、地区、细分市场预测,2025-2030 年 丙烯睛-丁二烯-苯乙烯塑胶的全球市场:市场规模·占有率·趋势,产业分析 (各产品种类·各终端用户·各地区),未来预测 (2025年~2034年)

丙烯睛-丁二烯-苯乙烯塑胶的全球市场:市场规模·占有率·趋势,产业分析 (各产品种类·各终端用户·各地区),未来预测 (2025年~2034年) 丙烯腈丁二烯苯乙烯(ABS)全球市场(2025-2029)

丙烯腈丁二烯苯乙烯(ABS)全球市场(2025-2029) 丙烯腈丁二烯苯乙烯 (ABS) 市场规模、份额和成长分析(按应用、製程、最终用户产业和地区):产业预测 (2024-2031)

丙烯腈丁二烯苯乙烯 (ABS) 市场规模、份额和成长分析(按应用、製程、最终用户产业和地区):产业预测 (2024-2031) 丙烯腈丁二烯聚苯乙烯树脂市场:按成分、製造流程、类型、等级、最终用途产业 - 2025-2030 年全球预测

丙烯腈丁二烯聚苯乙烯树脂市场:按成分、製造流程、类型、等级、最终用途产业 - 2025-2030 年全球预测