|

市场调查报告书

商品编码

1939117

兆赫技术:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Terahertz Technologies - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

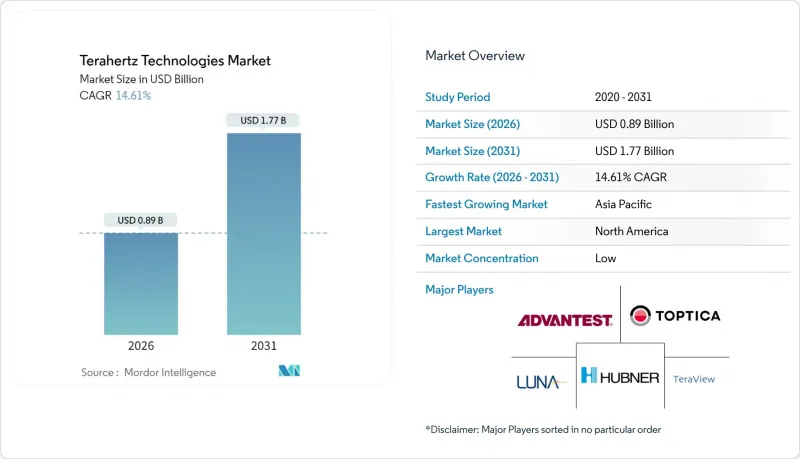

预计兆赫技术市场将从 2025 年的 7.8 亿美元成长到 2026 年的 8.9 亿美元,到 2031 年将达到 17.7 亿美元,2026 年至 2031 年的复合年增长率为 14.61%。

紧凑型光子整合光源的创新、6G示范回程传输链路的扩展以及製药公司向即时在线连续品管的转变,正在加速商业化进程。中频系统(1-5 THz)因其在大气渗透性和影像解析度方面的平衡而维持需求,而高于5 THz的高频率系统则在精密计量和高资料速率研究领域日益受到关注。儘管医疗保健产业是最大的终端用户,但随着6G频谱策略的逐步成型,通讯产业正经历最快的成长。儘管供应商仍按行业垂直领域进行专业化分工,市场碎片化现象仍然存在,但价值正从分立组件转向具有人工智慧驱动分析功能的承包平台。

全球兆赫技术市场趋势与洞察

紧凑型光子整合兆赫光源的研究进展

硅光电技术实现了兆赫引擎的小型化,无需笨重的低温冷却设备,与分立结构相比,面积减少了75%。 TOPTICA公司已成功整合单片量子级联雷射,在室温下可提供高达3THz、输出功率超过10mW/cm²的输出,为在预期时间内实现单位成本大幅降低的大规模生产铺平了道路。

6G回程传输现场试验数量迅速增加

NTT Docomo 和富士通在 2024 年的都市区试验中,成功地在 300GHz 频段以 1 公里的距离传输了 100Gbps 的数据,证明了兆赫技术在高密度小型基地台配置中的可行性。三星也实现了类似的数据传输速率,同时与毫米波技术相比,功耗降低了 40%。

有限的大气传输视窗限制了室外链路

水蒸气吸收会导致每公里 100 dB 的损耗,但在 220 GHz、340 GHz 和 650 GHz 附近的窄频内除外,这需要精确的频率控制,并将室外链路限制在短距离或受控环境中运行。

细分市场分析

到2025年,兆赫成像技术将占据兆赫技术市场41.32%的份额,这主要得益于其在製药、安防和无损检测领域的成熟应用。通讯平台目前贡献的收入较为有限,但随着6G架构的日益完善,它将成为成长最快的细分市场,年复合成长率将达到15.46%。罗氏在涂层检测领域高达99.8%的缺陷检测准确率是支撑成像技术高附加提案的基础,而通讯领域的发展则仰赖标准化进程的推进。

需求趋势包括:早期采用者利用成像技术已建立的投资收益;网路营运商试点多Gigabit链路,以在密集的都市区网路中分担光纤压力;硬体供应商捆绑向人工智慧分析功能,并促进其与製药 MES(製造执行系统)和电信编配堆迭的集成,从而推动向利用人工智慧性能数据的软体订阅收入模式转变。

由于其卓越的传输解析度比,工作在 1-5 THz 频段的平台将在 2025 年占据兆赫技术市场 38.20% 的份额。更高频宽(5 THz 以上)的系统尚处于起步阶段,但随着 6 THz 以上频率放大器链的成熟,预计其复合年增长率将达到 15.81%。 Virginia 维吉尼亚的固体放大器可提供稳定的输出功率,从而实现奈米级精度的测量,并扩展其应用范围。

由于供应链日趋成熟,元件价格不断下降,中频宽将保持其现有优势;而高频宽的采用将在半导体线宽计量、增材製造光栅检测和量子材料研究等需要极高分辨率才能创造新价值的领域增加,从而抵消光学对准日益增长的复杂性。

区域分析

北美在2025年占据了34.45%的市场份额,这主要得益于1.5亿美元的联邦研究津贴、国防部采购远程扫描仪以及成熟製药公司为寻求符合过程分析技术(PAT)而采取的措施。产学研联盟正透过共用无尘室设施和智慧财产权池加速商业化进程,缩短Start-Ups从概念到试点阶段的週期。加拿大的采矿业和纸浆造纸业正在整合加固型兆赫成像器,用于远端矿石和纤维等级分类。

亚太地区正以17.55%的复合年增长率引领成长。中国营运商在兆赫6G研发领域累计超过20亿美元,日本精密仪器供应商正将中波段探头整合到其计量台上。韩国正将太赫兹分析技术应用于其极紫外光微影(EUV)半导体工厂,以进行晶粒键合均匀性检测。印度学名药生产商正在部署在线连续光谱仪,以符合出口药典标准。强而有力的政府补贴和不断扩大的国内供应链正在推动成本降低。

在欧洲,太赫兹技术的应用正稳定成长,这得益于汽车轻量化、製药连续生产以及「地平线欧洲」研发计画(价值2亿欧元,约2.14亿美元)的推动。德国机械製造商正在将兆赫收发器整合到工业4.0机器人中;北欧航太公司正在使用高频宽成像器检测复合材料材料分层;中东能源公司正在试用油井检测工具进行水合物测绘;巴西相关企业正在测试手持式扫描仪,以检测出口玉米中的黄曲毒素。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 紧凑型光子整合兆赫光源的研究进展

- 6G回程传输示范安装快速成长

- 在药品品质保证和品管(QA/QC)中扩大在线连续检测的应用

- 国防领域对毫米级分辨率被动式远距离扫描仪的需求

- 加速引入兆赫兹重复频率超快雷射泵浦兆赫系统

- 政府资助的天文有效载荷需要低温兆赫检测器

- 市场限制

- 户外链路受限于有限的大气传输窗口。

- 高功率雷射(QCL)源的低温冷却需求

- 缺乏可製造的低损耗兆赫封装

- 275 GHz 以上频段缺乏统一的全球电磁相容性/健康暴露限值

- 产业供应链分析

- 宏观经济因素的影响

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 定价分析

- 兆赫技术无损检测应用分析

- 兆赫技术的法律和监管框架

第五章 市场规模与成长预测

- 按应用程式类别

- 兆赫成像系统

- 主动系统

- 被动系统

- 兆赫光谱系统

- 时域

- 频域

- 通讯系统

- 兆赫成像系统

- 按频率范围

- 低频兆赫频宽(0.1至1太赫兹)

- 中频兆赫频宽(1至5太赫兹)

- 高频太兆赫频宽(5 THz 以上)

- 最终用户

- 卫生保健

- 国防与安全

- 电讯

- 产业

- 食品和农业

- 研究所

- 其他最终用户

- 依组件类型

- 兆赫光源

- 兆赫检测器

- 光学和被动元件

- 系统和软体

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- ADVANTEST Corporation

- Luna Innovations Incorporated

- TeraView Limited

- TOPTICA Photonics AG

- HUBNER GmbH and Co. KG

- BATOP GmbH

- Microtech Instruments Inc.

- Menlo Systems GmbH

- Gentec-EO Inc.

- Bakman Technologies LLC

- QMC Instruments Ltd

- Bruker Corporation

- Lytid SAS

- Attocube Systems AG

- Helmut Fischer GmbH

- Baugh and Weedon Ltd

- Das-nano SL

- Teravil Ltd

- Terasense Group Inc.

- Virginia Diodes Inc.

第七章 市场机会与未来展望

The terahertz technologies market is expected to grow from USD 0.78 billion in 2025 to USD 0.89 billion in 2026 and is forecast to reach USD 1.77 billion by 2031 at 14.61% CAGR over 2026-2031.

Breakthroughs in compact photonic-integrated sources, the expansion of 6G proof-of-concept backhaul links, and pharmaceutical companies' shift toward real-time inline quality control are accelerating commercialization. Mid-frequency systems (1-5 THz) sustain demand by balancing atmospheric transmission with imaging resolution, while high-frequency systems above 5 THz attract precision metrology and high-data-rate research. Healthcare remains the largest end user, yet telecommunications records the steepest growth as 6G spectrum strategies crystallize. Fragmentation persists because vendors specialize by vertical; value is migrating from discrete components to turnkey platforms with AI-driven analytics.

Global Terahertz Technologies Market Trends and Insights

Advances in compact photonic-integrated THz sources

Silicon photonics has shrunk terahertz engines, eliminating bulky cryocoolers and cutting the footprint by 75% relative to discrete architectures. TOPTICA demonstrated monolithic quantum-cascade-laser integration delivering >10 mW/cm2 at room temperature up to 3 THz, opening mass-manufacturing pathways that can slash per-unit costs by an order of magnitude within the outlook period.

Surge in 6G backhaul proof-of-concept installations

NTT DOCOMO and Fujitsu achieved 100 Gbps over 1 km at 300 GHz in urban trials in 2024, validating the feasibility of terahertz technology for dense small-cell topologies. Samsung logged similar data rates while lowering power consumption by 40% compared to millimeter-wave alternatives.

Limited atmospheric transmission windows constrain outdoor links

Water-vapor absorption imposes 100 dB/km losses outside narrow bands near 220 GHz, 340 GHz, and 650 GHz, forcing precise frequency control and restricting outdoor spans to short ranges or controlled climates.

Other drivers and restraints analyzed in the detailed report include:

- Rising adoption in inline pharmaceutical QA/QC

- Defense demand for millimeter-resolution passive standoff scanners

- Cryogenic cooling requirements for high-power QCL sources

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Terahertz imaging retained 41.32% of the terahertz technology market in 2025 as pharmaceutical, security, and non-destructive testing installations matured. Communication platforms contribute modest revenue today, yet are set to expand fastest at 15.46% CAGR as 6G architectures formalize. Robust defect-detection accuracy-99.8% in Roche's coating inspections-underpins imaging's premium value proposition, whereas communications hinge on standard-setting milestones.

Demand patterns show early adopters capitalizing on established ROI for imaging, while network operators trial multi-gigabit links to offload fiber in dense urban grids. Hardware vendors bundle AI-enabled analytics, easing integration into pharmaceutical MES or telecom orchestration stacks, thereby shifting revenue toward software subscriptions that monetize performance data.

Platforms operating 1-5 THz commanded 38.20% of the terahertz technologies market share in 2025 thanks to favorable transmission-to-resolution ratios. High-band (>5 THz) systems, though nascent, should log 15.81% CAGR as frequency-multiplier chains mature beyond 6 THz. Solid-state multipliers from Virginia Diodes now deliver stable output enabling nanometer-precision metrology, broadening addressable use cases.

Mid-band incumbency benefits from supply-chain maturity and lower component prices. High-band adoption will rise where extreme resolution unlocks new value, such as in semiconductor linewidth metrology, additive-manufactured lattice inspection, and quantum materials research, offsetting the higher optical-alignment complexity.

The Terahertz Technologies Market Report is Segmented by Application Category (Terahertz Imaging Systems, and More), Frequency Range (Low-Frequency Terahertz, and More), End User (Healthcare, Defense and Security, and More), Component Type (Terahertz Sources, Terahertz Detectors, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America secured 34.45% market share in 2025, propelled by USD 150 million federal research grants, defense procurement of standoff scanners, and pharmaceutical incumbents seeking PAT compliance. Academic-industry consortia accelerate commercialization through shared clean-room facilities and IP pools, shortening concept-to-pilot cycles for start-ups. Canadian mining and pulp-and-paper sectors integrate ruggedized THz imagers for remote ore and fiber-grade classification.

Asia-Pacific leads growth at 17.55% CAGR as Chinese operators earmark over USD 2 billion for terahertz 6G R&D and Japanese precision-tool vendors integrate mid-band probes into metrology benches. South Korea embeds THz analytics in EUV semiconductor fabs for die-bond uniformity checks, and Indian generics producers deploy inline spectrometers to meet export pharmacopeia standards. Robust government subsidies and domestic supply-chain scaling compress cost curves.

Europe charts steady uptake anchored in automotive lightweighting, pharmaceutical continuous manufacturing, and Horizon Europe R&D funding worth EUR 200 million (USD 214 million). German machine builders bundle terahertz transceivers into Industry 4.0 robotics, while Nordic aerospace firms use high-band imagers for composite delamination audits. Middle East energy companies pilot well-logging tools for hydrate mapping, and Brazilian agribusinesses trial handheld scanners for aflatoxin detection in corn exports.

- ADVANTEST Corporation

- Luna Innovations Incorporated

- TeraView Limited

- TOPTICA Photonics AG

- HUBNER GmbH and Co. KG

- BATOP GmbH

- Microtech Instruments Inc.

- Menlo Systems GmbH

- Gentec-EO Inc.

- Bakman Technologies LLC

- QMC Instruments Ltd

- Bruker Corporation

- Lytid SAS

- Attocube Systems AG

- Helmut Fischer GmbH

- Baugh and Weedon Ltd

- Das-nano S.L.

- Teravil Ltd

- Terasense Group Inc.

- Virginia Diodes Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advances in compact photonic-integrated THz sources

- 4.2.2 Surge in 6G-backhaul proof-of-concept installations

- 4.2.3 Rising adoption in inline pharmaceutical QA/QC

- 4.2.4 Defense demand for mm-resolution passive standoff scanners

- 4.2.5 Accelerating deployment of MHz-repetition ultrafast laser-pumped THz systems

- 4.2.6 Government-funded astronomy payloads requiring cryogenic THz detectors

- 4.3 Market Restraints

- 4.3.1 Limited atmospheric transmission windows constrain outdoor links

- 4.3.2 Cryogenic cooling requirements for high-power QCL sources

- 4.3.3 Scarcity of volume-manufacturable low-loss THz packaging

- 4.3.4 Absence of harmonised global EMC/health exposure limits above 275 GHz

- 4.4 Industry Supply-Chain Analysis

- 4.5 Impact of Macroeconomic Factors

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Degree of Competition

- 4.9 Pricing Analysis

- 4.10 Analysis of Non-destructive Testing Applications of Terahertz Technology

- 4.11 Legal and Regulatory Space for Terahertz Technologies

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application Category

- 5.1.1 Terahertz Imaging Systems

- 5.1.1.1 Active Systems

- 5.1.1.2 Passive Systems

- 5.1.2 Terahertz Spectroscopy Systems

- 5.1.2.1 Time-Domain

- 5.1.2.2 Frequency-Domain

- 5.1.3 Communication Systems

- 5.1.1 Terahertz Imaging Systems

- 5.2 By Frequency Range

- 5.2.1 Low-Frequency Terahertz (0.1 - 1 THz)

- 5.2.2 Mid-Frequency Terahertz (1 - 5 THz)

- 5.2.3 High-Frequency Terahertz (Above 5 THz)

- 5.3 By End User

- 5.3.1 Healthcare

- 5.3.2 Defense and Security

- 5.3.3 Telecommunications

- 5.3.4 Industrial

- 5.3.5 Food and Agriculture

- 5.3.6 Laboratories

- 5.3.7 Other End Users

- 5.4 By Component Type

- 5.4.1 Terahertz Sources

- 5.4.2 Terahertz Detectors

- 5.4.3 Optics and Passive Components

- 5.4.4 Systems and Software

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ADVANTEST Corporation

- 6.4.2 Luna Innovations Incorporated

- 6.4.3 TeraView Limited

- 6.4.4 TOPTICA Photonics AG

- 6.4.5 HUBNER GmbH and Co. KG

- 6.4.6 BATOP GmbH

- 6.4.7 Microtech Instruments Inc.

- 6.4.8 Menlo Systems GmbH

- 6.4.9 Gentec-EO Inc.

- 6.4.10 Bakman Technologies LLC

- 6.4.11 QMC Instruments Ltd

- 6.4.12 Bruker Corporation

- 6.4.13 Lytid SAS

- 6.4.14 Attocube Systems AG

- 6.4.15 Helmut Fischer GmbH

- 6.4.16 Baugh and Weedon Ltd

- 6.4.17 Das-nano S.L.

- 6.4.18 Teravil Ltd

- 6.4.19 Terasense Group Inc.

- 6.4.20 Virginia Diodes Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

兆赫(THz):全球市场份额和排名、总收入和需求预测(2026-2032年)

兆赫(THz):全球市场份额和排名、总收入和需求预测(2026-2032年) 太赫兹医疗诊断、治疗、硬体和材料:市场与技术(2026-2046)

太赫兹医疗诊断、治疗、硬体和材料:市场与技术(2026-2046) 2026年兆赫技术全球市场报告

2026年兆赫技术全球市场报告 日本兆赫技术市场报告:按类型、组件、终端应用产业和地区划分(2026-2034年)

日本兆赫技术市场报告:按类型、组件、终端应用产业和地区划分(2026-2034年) 兆赫光谱:全球市场份额和排名、总收入和需求预测(2025-2031 年)兆赫光谱仪:全球市占率及排名、总收入及需求预测(2025-2031年)兆赫成像检测:全球市场份额和排名、总销售额和需求预测(2025-2031 年)太赫兹技术市场规模、份额、趋势及预测(按类型、组件、最终用途行业和地区),2025 年至 2033 年

兆赫光谱:全球市场份额和排名、总收入和需求预测(2025-2031 年)兆赫光谱仪:全球市占率及排名、总收入及需求预测(2025-2031年)兆赫成像检测:全球市场份额和排名、总销售额和需求预测(2025-2031 年)太赫兹技术市场规模、份额、趋势及预测(按类型、组件、最终用途行业和地区),2025 年至 2033 年 兆赫技术市场:按应用、组件类型、产业、技术和产品划分 - 全球预测(2025-2032年)

兆赫技术市场:按应用、组件类型、产业、技术和产品划分 - 全球预测(2025-2032年) 兆赫技术市场:2030 年全球预测(按类型、应用、发生器和检测器以及地区)

兆赫技术市场:2030 年全球预测(按类型、应用、发生器和检测器以及地区)