|

市场调查报告书

商品编码

1686546

超快雷射:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Ultrafast Lasers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

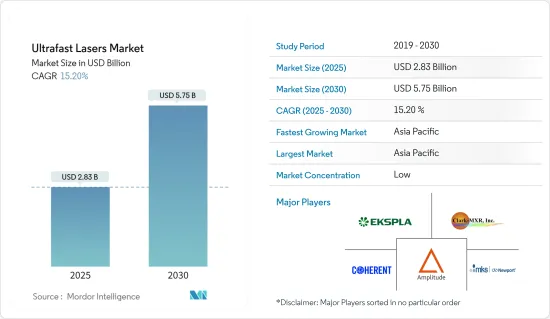

超快雷射器市场规模预计在 2025 年为 28.3 亿美元,预计到 2030 年将达到 57.5 亿美元,预测期内(2025-2030 年)的复合年增长率为 15.2%。

超快雷射是一种发射一系列脉衝的激光,每个脉衝持续时间不到 1 奈秒。它们以超短脉衝持续时间和高峰值强度而闻名,可以实现精确且可控的材料处理。它用于切割、钻孔、烧蚀和构造各种各样的材料。

超快雷射在材料加工中具有高精度,可实现极其精确和复杂的材料加工和改质。这些雷射器能够处理几乎任何类型的材料,使其成为适用于广泛应用的多功能工具。

超快雷射的市场成长主要受到材料加工和半导体行业不断增长的需求的推动,并且在汽车、家用电器、通讯技术和医疗保健等终端用户领域得到广泛应用。超快雷射和微加工实现的高尺寸精度是推动超快雷射需求的关键因素。这些雷射用于半导体工业的光掩模修復。它也可用于切片和切块。

对更小、更复杂的组件的需求要求更高水平的尺寸精度,而超快雷射器以其超短脉衝持续时间和最小的热效应锥来满足这一需求。此功能可提高产品品质并减少製造时间和成本。随着技术的进步,超快雷射市场预计将进一步扩大,以满足对卓越尺寸精度日益增长的需求。

由于製造超快雷射需要先进的技术和极高的精度,因此其生产过程十分复杂。为了了解製造的复杂性,我们需要深入研究製造这些高性能设备的复杂过程。

新冠肺炎疫情对全球经济造成了扰乱。此外,电子和半导体市场的生产设施也停止了生产。製造能力下降、劳动力和原材料短缺、旅行禁令和工厂关闭导致市场成长放缓。随着自动化的广泛应用和精密製造需求的不断增长,疫情过后,雷射的应用和需求正在更高。

超快雷射市场趋势

消费性电子产品成长强劲

- 大多数家用电子电器应用需要高度可重复的脉衝和聚焦雷射光束,以实现最高的生产力和精度。光纤雷射器出色的光束品质、灵活性和稳定性使其成为微加工应用的理想选择。近年来,IPG 已大幅扩展产品系列,从传统的红外线扩展到绿光和紫外线,并开发了皮秒和高飞秒脉衝功能。

- 此外,家用电子电器产业对 IPG 光纤雷射和整合自动化系统青睐有加,因为它们将可靠性、灵活性、效率、高功率、光束品质、紧凑性和成本效益完美地融为一体。

- 研究领域的主要推动因素是家用电子电器领域不断增长的需求以及快速的技术发展,这迫使OEM持续向市场推出独特的产品。消费性电子产品供应商主要依赖电子产品製造商为市场带来好处,例如降低成本、缩短时间、提高品质、缩短时间和灵活性。

- 据消费科技协会称,美国消费科技零售收益预计将在 2022 年至 2024美国间小幅成长,到 2024 年底将达到 5,000 亿美元以上。大部分收益将来自硬件,到 2024 年将达到约 3,450 亿美元。

- 如今,市场上大多数的电子设备都在小型化,对设备尺寸公差的要求越来越严格,以适应越来越小的尺寸,从而推动了超快雷射的成熟。电子製造製程需要提高对较小元件特征的侦测精度。

- 超快雷射器对于某些智慧型手机零件(例如微处理器和半导体)的生产至关重要。智慧型手机的日益普及将极大地促进研究市场的成长。

亚太地区可望占据主要市场占有率

- 亚太地区是世界最大製造业经济体的所在地,包括中国、日本、韩国和台湾。汽车、电子、航太和医疗设备等领域製造业的持续扩张,对工业雷射的需求庞大,以支援各种加工、切割、焊接和标记应用。

- 亚太地区在这个市场上有一些关键参与者,例如大族雷射科技产业集团。该地区以其在汽车和医疗行业的能力而闻名,预计将推动市场成长。此外,预计亚太地区将呈现最高的市场成长率,各类参与者将进行投资以推动成长和发展。

- 此外,该地区的汽车工业正朝着电气化和小型化的方向发展,同时要求高刚性、设计灵活性和可製造性。蓝色雷射具有较高的光吸收效率,在汽车引擎和电池的铜加工方面需求强劲。生产性加工需要高功率和高光束品质的雷射光束源。

- 由于台湾半导体製造公司等公司的存在,该地区是最大的半导体和电子产品製造商。台湾生产了全球60%以上的半导体,以及90%以上的先进半导体。半导体大部分都是由台积电生产的。

超快雷射市场概览

超快雷射市场较为分散,且有多家参与者,竞争十分激烈。市场似乎相当集中。市场供应商纷纷参与新产品的发布,并投入大量研发资金和伙伴关係,这大大促进了市场的成长。此外,各公司正在将收购作为一种成长策略。市场由 Amplitude Laser Group Coherent Inc.、Ekspla(EKSMA 集团)、MKS Instruments Inc.(Newport Corporation)和 Clark-MXR Inc. 等雷射/光子巨头组成。

2024 年 1 月 - IPG Photonics Corporation 在旧金山的光电 West 上展示了全新创新的光纤雷射解决方案。 2,000 平方英尺的展位展示了各种雷射源、整合系统和特定产业解决方案以及大量应用样品。

2023 年 6 月-相干公司推出其新一代超低成本奈秒脉衝紫外线雷射器,用于工业电子、消费品、设备、包装等领域的高对比度标记应用。新型阵列雷射的输出功率为 5 W 和 10 W,脉衝重复率为 50 kHz 至 300 kHz。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 新冠肺炎疫情及其他宏观经济因素对市场的影响

第五章 市场动态

- 市场驱动因素

- 需要提高尺寸精度

- 政府要求推动超快雷射的采用

- 市场限制

- 製造业的复杂性挑战市场成长

第六章 市场细分

- 依雷射类型

- 固体雷射

- 光纤雷射

- 脉衝时间

- 皮秒

- 飞秒

- 按应用

- 材料加工与微加工

- 医学和生物成像

- 研究

- 按最终用户

- 消费性电子产品

- 医疗

- 车

- 航太和国防

- 研究

- 其他最终用户

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第七章 竞争格局

- Vendor Positioning Analysis

- 公司简介

- Amplitude Laser Group

- Coherent Inc.

- Ekspla(EKSMA group)

- MKS Instruments Inc.(Newport Corporation)

- Clark-MXR Inc.

- TRUMPF Group

- Novanta(Laser Quantum Ltd)

- Lumentum Holdings

- Aisin Seiki(IMRA America Inc.)

- IPG Photonics

- NKT Photonics

- Light Conversion Ltd

第八章投资分析

第九章:市场的未来

The Ultrafast Lasers Market size is estimated at USD 2.83 billion in 2025, and is expected to reach USD 5.75 billion by 2030, at a CAGR of 15.2% during the forecast period (2025-2030).

Ultrafast lasers are a variety of lasers that emits a series or train of pulses, each lasting less than a nanosecond. They are known for their ultra-short pulse duration and high peak intensity, allowing precise and controlled material processing. They are used for cutting, drilling, ablating, and structuring various materials.

Ultrafast lasers offer high precision in material processing, allowing for extremely accurate and intricate fabrication and modification of materials. These lasers can process almost every type of material, making them versatile tools for various applications.

The market growth for ultrafast lasers is primarily driven by the increasing demand in the materials processing and semiconductor industries, finding applications in several end users like automotive, consumer electronics, communications technology, and healthcare. The high dimensional accuracy enabled by ultrafast lasers and micromachining are significant factors boosting the demand for ultrafast lasers. These lasers are used for photomask repairs in the semiconductor industry. They are also employed for slicing and dicing activities

The demand for smaller, more complex components necessitates a higher level of dimensional accuracy, which ultrafast lasers deliver with their ultrashort pulse durations and minimal heat-affected cones. This capability improves product quality and reduces production time and costs. As technology advances, the market for ultrafast lasers is expected to expand further to meet the growing need for superior dimensional accuracy.

Manufacturing ultrafast lasers involves many complexities stemming from the advanced technology and precision required to produce these devices. Understanding the manufacturing complexities requires delving into the intricate process of creating these high-performance devices.

The COVID-19 pandemic caused disruptions in the global economy. It also halted the production facilities of the electronics and semiconductors markets. The slowdown in manufacturing capacity, unavailability of workers and raw materials, travel bans, and facility closures led to a slowdown in the market's growth. With the proliferation of automation and a growth in the demand for precision manufacturing, lasers are witnessing higher application and demand after the pandemic effect.

Ultrafast Lasers Market Trends

Consumer Electronics to Witness Significant Growth

- Most consumer electronics applications require a focused laser beam delivered in highly repeatable pulses at a rapid repetition rate for maximum productivity and precision. Fiber lasers' outstanding beam quality, flexibility, and stability are ideal for micromachining applications. Recently, IPG significantly expanded its product portfolio from the traditional infrared into the green and ultraviolet wavelengths and developed picosecond and high femtosecond pulse capabilities, which greatly broaden the scope of consumer electronics applications able to benefit from fiber laser technology.

- In addition, the consumer electronics industry covets IPG fiber lasers and integrated automated systems for their unique combination of reliability, flexibility, efficiency, high power, beam quality, compactness, and cost-effectiveness.

- The studied sector is driven primarily by the increasese in demand from the consumer electronics sector and fast-paced technological developments, which force OEMs to introduce unique products continuously in the market. Consumer electronics providers primarily rely on electronic manufacturers who offer benefits like cost savings, reduced time-to-volume, quality, decreased time-to-market, and flexibility to provide their products in the market.

- According to the Consumer Technology Association, in the United States, consumer technology retail revenue is forecast to increase slightly between 2022 and 2024, reaching over USD 500 billion at the end of the period. Hardware accounts for most of the revenue, bringing in around USD 345 billion in 2024.

- Most of the electronic appliances in the market nowadays are downsized and demand tighter dimensional tolerances so that the elements can fit inside ever-smaller form factors, driving the maturation of the ultrafast laser. The electronic manufacturing process needs to inspect the tinier component features and improve accuracy.

- Ultrafast lasers are crucial in manufacturing specific smartphone components, such as microprocessors and semiconductors. The increasing adoption of smartphones is going to to aid the studied market's growth significantly.

Asia-Pacific is Expected to Hold Major Market Share

- The Asia-Pacific is home to some of the world's largest manufacturing economies, including China, Japan, South Korea, and Taiwan. The ongoing expansion of manufacturing industries in sectors such as automotive, electronics, aerospace, and medical devices creates a significant demand for industrial lasers to support various machining, cutting, welding, and marking applications.

- The Asia-Pacific houses some important players in the market, such as Han's Laser Technology Industry Group, among others. The region is known for its capabilities in the automotive and medical industries, which are expected to drive its market growth. Also, various players have invested in driving their growth and development, as the Asia-Pacific is expected to witness the highest growth rate in the market.

- Moreover, the automotive industry in the region is moving toward electrification and miniaturization while requiring high rigidity, design flexibility, and productivity. Blue lasers with high optical absorption efficiency are in high demand in copper fabrication for automotive motors and batteries. The highly productive processing requires a laser beam source with high output power and beam quality.

- The region is the biggest manufacturer of semiconductor and electronics products owing to the presence of companies like Taiwan Semiconductor Manufacturing Company. Taiwan produces more than 60% of the global semiconductors and over 90% of the advanced ones. Most of the semiconductors are manufactured by TSMC.

Ultrafast Lasers Market Overview

The Ultrafast laser market is fragmented and highly competitive due to multiple players. The market appears to be moderately concentrated. Vendors in the market are taking part in new product rollouts with crucial R&D investments and partnerships that significantly boost market growth. Additionally, companies have acquisitions as their growth strategy. The market consists of laser/photonic giants, like Amplitude Laser Group Coherent Inc., Ekspla (EKSMA group), MKS Instruments Inc. (Newport Corporation), and Clark-MXR Inc.

January 2024 -The IPG Photonics Corporation highlighted new and innovative fiber laser solutions at Photonics West January 30 - February 01, 2024, in San Francisco. The 2,000-square-foot booth displays include a wide range of laser sources, integrated systems, and industry-specific solutions, along with numerous showcases of application samples.

June 2023 - Coherent Corporation introduced an ultra-low-cost, next-generation nanosecond pulsed UV laser for high-contrast marking applications in industrial electronics, consumer goods, equipment, and packaging. The new array lasers are available with 5W and 10W output power and operate at pulse repetition rates between 50kHz and 300kHz.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Need for Enhanced Dimensional Accuracy

- 5.1.2 Government Mandates Promoting Adoption of Ultrafast Lasers

- 5.2 Market Restraints

- 5.2.1 Manufacturing Complexities Challenge the Market Growth

6 MARKET SEGMENTATION

- 6.1 By Laser Type

- 6.1.1 Solid State Laser

- 6.1.2 Fiber Laser

- 6.2 By Pulse Duration

- 6.2.1 Picosecond

- 6.2.2 Femtosecond

- 6.3 By Application

- 6.3.1 Material Processing And Micromachining

- 6.3.2 Medical And Bioimaging

- 6.3.3 Research

- 6.4 By End User

- 6.4.1 Consumer Electronics

- 6.4.2 Medical

- 6.4.3 Automotive

- 6.4.4 Aerospace and Defense

- 6.4.5 Research

- 6.4.6 Other End Users

- 6.5 By Geography

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia-Pacific

- 6.5.4 Latin America

- 6.5.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Vendor Positioning Analysis

- 7.2 Company Profiles

- 7.2.1 Amplitude Laser Group

- 7.2.2 Coherent Inc.

- 7.2.3 Ekspla (EKSMA group)

- 7.2.4 MKS Instruments Inc. (Newport Corporation)

- 7.2.5 Clark-MXR Inc.

- 7.2.6 TRUMPF Group

- 7.2.7 Novanta (Laser Quantum Ltd)

- 7.2.8 Lumentum Holdings

- 7.2.9 Aisin Seiki (IMRA America Inc.)

- 7.2.10 IPG Photonics

- 7.2.11 NKT Photonics

- 7.2.12 Light Conversion Ltd

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

超快雷射市场规模、份额和趋势分析报告:按雷射类型、脉衝宽度、应用、地区和细分市场预测(2026-2033 年)

超快雷射市场规模、份额和趋势分析报告:按雷射类型、脉衝宽度、应用、地区和细分市场预测(2026-2033 年) 全球超快雷射市场规模、份额、趋势和成长分析报告(2026-2034)

全球超快雷射市场规模、份额、趋势和成长分析报告(2026-2034) 超快雷射市场-全球产业规模、份额、趋势、机会、预测:按类型、脉衝持续时间、应用、地区和竞争格局划分,2021-2031年

超快雷射市场-全球产业规模、份额、趋势、机会、预测:按类型、脉衝持续时间、应用、地区和竞争格局划分,2021-2031年 光纤雷射(2025):技术、应用与市场趋势

光纤雷射(2025):技术、应用与市场趋势 超快雷射市场按类型、组件、应用和最终用户行业划分 - 全球预测 2025-2032

超快雷射市场按类型、组件、应用和最终用户行业划分 - 全球预测 2025-2032 2025-2033 年超快雷射市场报告(按类型、脉衝持续时间、最终用户和地区)

2025-2033 年超快雷射市场报告(按类型、脉衝持续时间、最终用户和地区) 超快雷射器市场(2025)-技术、应用及市场趋势:超快雷射器助力从科学研究到工业生产等各领域的创新。超快雷射市场:全球按雷射类型、脉衝持续时间、最终用户和地区划分,2026 年至 2032 年

超快雷射器市场(2025)-技术、应用及市场趋势:超快雷射器助力从科学研究到工业生产等各领域的创新。超快雷射市场:全球按雷射类型、脉衝持续时间、最终用户和地区划分,2026 年至 2032 年