|

市场调查报告书

商品编码

1686551

铪:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Hafnium - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

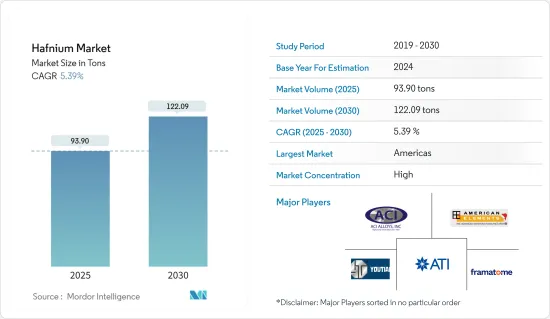

预计 2025 年铪市场规模为 93.90 吨,到 2030 年将达到 122.09 吨,预测期内(2025-2030 年)的复合年增长率为 5.39%。

主要亮点

- 新冠疫情对铪市场产生了负面影响。生产设施的关闭和短期停产对多种应用造成了严重损害,并限制了铪的消耗。儘管如此,市场仍将在 2020 年后继续保持这种发展势头,并在主要终端用户类别中持续努力,推动市场逐步发展。

- 推动市场发展的首要因素是航太工业对铪的需求不断增长以及其在半导体中的使用量不断增加。然而,材料价格上涨可能会阻碍市场成长。预计在预测期内,各种铪产品的应用不断增加将提供大量的成长机会。

- 在全球整体,中国预计将占据市场主导地位。然而,欧洲被认为是世界上成长最快的地区。

铪市场趋势

主导市场的高温合金应用

- 铪主要用作高温合金,此应用占其总用途的50%以上。铪具有高强度且在极高温度下稳定,因此被用作航太和工业涡轮机应用中的高温合金。

- 铪高温合金主要用于喷射发动机和火箭发动机。在火箭引擎喷嘴所使用的铌基合金中,铪的含量约为10%。铪是 MAR M 247 超级合金的组成部分,该合金用于喷射引擎的热部分(涡轮叶片和轮叶)。

- 铪高温合金可用于工业涡轮机,主要用于发电。因此,发电业和风力发电的趋势可能有利于铪高温合金的成长。

- 根据国际能源总署(IEA)的数据,预计2022年全球发电量将持续成长,与前一年同期比较增2.4%(约700TWh),与过去五年的复合年增长率大致相同。 2022年,全球燃煤发电量成长约2%(185TWh)。煤炭作为发电来源连续第二年增加,超过 10,000兆瓦时 (TWh),占总发电量的 36%。此外,国际能源总署预测,到 2025 年,全球燃煤发电装置容量将从 2022 年的 2,271 吉瓦增加到约 2,319 吉瓦。

- 中国已宣布计划部署1.7千兆瓦(GW)的电力,其排放比燃煤发电更少,以满足其最大群岛(1,390个岛屿)的电力需求。 GE Vernova 的燃气发电业务和哈尔滨电气今天宣布,中国国家开发投资公司 (SDIC) 的金能(郑)发电厂计划于 2023 年 10 月开始运营,该发电厂的排放气体燃煤电厂,可满足中国最大的群岛(由 1,390 个岛屿组成)的电力需求。 (国投)金能(舟山)燃气发电有限公司宣布,已为舟山群岛发电厂订购两台 GE 9HA.02燃气涡轮机。

- 2022 年 5 月,J-POWER 美国在位于美国埃尔伍德的 1,200 兆瓦 (MW)复合迴圈发电厂杰克逊发电工程上使用两台三菱动力 M501JAC燃气涡轮机实现了北美首次商业运营。

- 由于超级合金在各行业中的重要性日益增加,预计预测期内对铪的需求将会成长。

中国主宰亚太地区

- 在中国,铪以海绵、合金等形式应用于核子反应炉、飞机、工业涡轮机等工业。铪因具有较高的中子捕获截面和中子吸收能力,被用作核子反应炉控制棒的材料。

- 2022年,中国运作核能发电容量将达52,000兆瓦以上,同年,中国运作核能发电容量仅次于美国、法国,位居世界第三。

- 根据中国核能协会预测,到2035年核能发电将占中国发电量的10%左右,2060年将占18%。

- 2022年9月,中国核准了两座价值115亿美元的核能发电厂,完成了该国2022年10座核能发电厂的核准名单。该核电厂预计将协助缓解该国严重的电力短缺,并增加铪的消费量。

- 2023年8月,当局核准在三个工厂再建造六座核能发电厂,使去年核准的核能发电计划总合达到10个。预计新的核能计划将在预测期内推动核子反应炉控制棒对铪的需求。

- 氧化铪可用于光学涂层,也可作为 DRAM 电容器和先进金属氧化物半导体装置中的高介电常数材料。中国是半导体晶片的净进口国,生产的半导体不到全球所需半导体的20%。然而,为了从更广泛的需求情势中获益,中国已开始实施「中国製造2025」计画等战略倡议。根据该计划,中国政府宣布了2030年实现产出3,050亿美元、满足80%国内需求的目标。

- 中国企业正加紧进军半导体产业。中国政府透过各种政策诱因为半导体企业建设工厂提供补贴。已宣布建设计画半导体生产设施的城市包括重庆、上海、北京、成都、合肥、深圳、武汉、厦门/辽宁和陕西。

- 因此,由于新的半导体製造设施的建立,预计预测期内对氧化铪的需求将快速增长。

- 中国也是主要飞机製造国之一和最大的国内航空客运市场。此外,该国的航空零件和组装製造业正在迅速扩张,拥有超过200家小型飞机零件製造商。

- 根据波音《2022-2041年商用飞机展望》,到2041年将交付约8,485架新飞机,市场价值达5,450亿美元。由于这些新的国内交付,对铪的需求可能会上升。

- 预计上述所有因素都将增加国内铪消费量。

铪行业概况

全球铪市场高度集中,主要企业占铪金属产量和供应量的70%以上。市场的主要企业(不分先后顺序)包括法马通(EDF)、American Elements、南京有天金属科技、ATI 和 ACI Alloys。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查结果

- 调查前提

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 航太工业的需求不断成长

- 半导体中铪基材料的使用日益增多

- 限制因素

- 价格上涨,分离和提取困难

- 其他阻碍因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 定价分析

第五章 市场区隔

- 类型

- 氧化铪

- 碳化铪

- 其他类型(包括铪金属)

- 应用

- 高温合金

- 光学涂层

- 核能

- 电浆切割

- 其他用途

- 地区

- 生产分析

- 法国

- 美国

- 中国

- 世界其他地区

- 消费分析

- 美国

- 欧洲联盟

- 俄罗斯

- 中国

- 印度

- 日本

- 世界其他地区

- 生产分析

第六章 竞争格局

- 併购、合资、合作、协议

- 市场占有率分析

- 主要企业策略

- 公司简介

- ACI Alloys

- Alkane Resources Ltd

- American Elements

- Baoji ChuangXin Metal Materials Co. Ltd(CXMET)

- China Nulear JingHuan Zirconium Industry Co. Ltd.

- Framatome(EDF)

- Nanjing Youtian Metal Technology Co. Ltd

- Phelly Materials Inc.

- Starfire Systems Inc.

第七章 市场机会与未来趋势

- 可重复使用太空船的趋势日益增强

- 扩大氧化铪奈米粒子在放射治疗的研究

简介目录

Product Code: 52510

The Hafnium Market size is estimated at 93.90 tons in 2025, and is expected to reach 122.09 tons by 2030, at a CAGR of 5.39% during the forecast period (2025-2030).

Key Highlights

- The COVID-19 pandemic negatively impacted the hafnium market. Due to the lockdown and brief halts in production facilities, several applications suffered significant damage, limiting hafnium consumption. Nonetheless, beyond 2020, the market developed slowly due to ongoing efforts in the main end-user categories and is likely to continue on its path.

- Major factors driving the market are the rising demand for hafnium in the aerospace industry and its increasing usage in semiconductors. However, higher prices of the material will likely hinder the market growth. The increasing application base for various hafnium products is anticipated to provide numerous growth opportunities over the forecast period.

- China is expected to dominate the market across the world. However, Europe is considered to be the fastest-growing region in the world.

Hafnium Market Trends

Super Alloys Application to Dominate the Market

- Hafnium is majorly used as a superalloy, and this application accounts for more than 50% of the total usage of hafnium. Due to its high strength and stability when operating at very high temperatures, hafnium is used as a superalloy for applications in aerospace and industrial turbines.

- Hafnium superalloys are mostly found in jet and rocket engines. Hafnium makes up roughly 10% of the niobium-based alloy used in rocket engine nozzles. It is regarded as indispensable in the MAR M 247 superalloy and is used in the hot section of jet engines (turbine blades and vanes).

- Hafnium superalloys are potentially used in industrial turbines, which are majorly used to produce electricity. Hence, the growing trends in the power generation industry and wind energy generation will favor the growth of hafnium superalloys.

- According to the International Energy Agency (IEA) statistics, global electricity generation continued to grow in 2022, increasing by 2.4% (nearly 700 TWh) year-over-year, which is similar to the average annual growth observed over the previous 5 years. In 2022, Global coal-fired electricity generation rose by nearly 2% (185 TWh). Coal as a source for electricity generation increased for the second year in a row, generating more than 10,000 Terawatt-hour (TWh), accounting for 36% of total generation. Moreover, according to the IEA forecasts, the installed coal power generation capacity will reach around 2,319 GW by 2025 globally, an increase from 2,271 GW in 2022.

- China has announced plans to install 1.7 gigawatts (GW) of electricity to power demand for China's largest archipelago, comprised of 1390 islands, with lower emissions than coal-fired alternatives. In October 2023 - GE Vernova's Gas Power business and Harbin Electric today announced that Chinese State Development & Investment Corp., Ltd. (SDIC) Jineng (Zhoushan) Gas Power Generation Co., Ltd. ordered two GE 9HA.02 gas turbines this power plant located in the Zhoushan archipelago.

- In May 2022, J-Power USA Development Co. Ltd. (J-POWER USA) achieved commercial operation with the first two Mitsubishi Power M501JAC gas turbines manufactured in North America at its Jackson generation project, a 1,200 megawatt (MW) combined-cycle power plant in Elwood, Illinois, United States.

- Owing to the rising importance of superalloys in various industries, the demand for the hafnium market is expected to grow during the forecast period.

China to Dominate the Asia-Pacific Region

- In China, hafnium is used in nuclear reactors, aircraft, industrial turbines, and other industries in the form of sponges, alloys, and other forms. Hafnium is used in nuclear reactors to make control rods due to its strong neutron-capture cross-section and neutron-absorbing capabilities.

- China's operable nuclear power capacity reached over 52,000 megawatts of electrical in 2022. In the same year, China had the third-largest operable nuclear power capacity worldwide after the United States and France.

- Nuclear power is expected to contribute about 10% of power generation in the country by 2035 and 18% by 2060, as per China's Nuclear Energy Association.

- In September 2022, China approved two nuclear plants worth USD 11.5 billion, completing the list of 10 nuclear power units sanctioned by the country in 2022. The power plants are expected to sort out the country's crippling power shortage condition and trigger higher consumption of hafnium.

- In August 2023, authorities approved an additional six nuclear power units to be built at three plants, totaling ten nuclear power projects approved last year. New nuclear projects are expected to induce demand for hafnium for control rods used in the reactors in the forecast period.

- Hafnium oxide finds application in optical coatings and as a high dielectric in DRAM capacitors and advanced metal oxide semiconductor devices. China is the net importer of semiconductor chips, with China manufacturing less than 20% of semiconductors used. However, to benefit from the extensive demand scenario, China has embarked on strategic initiatives, like the Made in China 2025 plan, under which the Chinese government has announced its goal to reach an output of USD 305 billion by 2030 and, therefore, meet 80% of its domestic demand.

- The Chinese companies are stepping up efforts to push into the semiconductor industry. The Chinese government has subsidized semiconductor companies to build factories through various policy incentives. Some cities that have announced their plans for semiconductor production facilities include Chongqing, Shanghai, Beijing, Chengdu, Hefei, Shenzhen, Wuhan, Xiamen and Liaoning, and Shaanxi.

- Therefore, with the establishment of new semiconductor manufacturing facilities, the demand for hafnium oxide is expected to increase rapidly over the forecast period.

- China is also one of the leading aircraft manufacturers and one of the largest domestic air passenger markets. Furthermore, the country's aviation parts and assembly manufacturing sector has been quickly expanding, with over 200 minor aircraft parts manufacturers present.

- According to the Boeing Commercial Outlook 2022-2041, around 8,485 new deliveries will be made by 2041 with a market service value of USD 545 billion. The demand for hafnium will likely rise due to such new deliveries in the country.

- All the aforementioned factors, in turn, are expected to augment the consumption of hafnium in the country.

Hafnium Industry Overview

The global hafnium market is highly consolidated, with the top two players accounting for more than 70% of the production and supply of hafnium metal. Some of the market's major players (not in any particular order) include Framatome (EDF), American Elements, Nanjing Youtian Metal Technology Co. Ltd., ATI, and ACI Alloys, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Demand from the Aerospace Industry

- 4.1.2 Increasing Utilization of Hafnium-Based Materials in Semiconductors

- 4.2 Restraints

- 4.2.1 Higher Prices and Difficulties in Seperation and Extraction

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Price Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Hafnium Oxide

- 5.1.2 Hafnium Carbide

- 5.1.3 Other Types (including Hafnium Metal)

- 5.2 Application

- 5.2.1 Super Alloy

- 5.2.2 Optical Coating

- 5.2.3 Nuclear

- 5.2.4 Plasma Cutting

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 Production Analysis

- 5.3.1.1 France

- 5.3.1.2 United States

- 5.3.1.3 China

- 5.3.1.4 Rest of the World

- 5.3.2 Consumption Analysis

- 5.3.2.1 United States

- 5.3.2.2 European Union

- 5.3.2.3 Russia

- 5.3.2.4 China

- 5.3.2.5 India

- 5.3.2.6 Japan

- 5.3.2.7 Rest of the World

- 5.3.1 Production Analysis

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ACI Alloys

- 6.4.2 Alkane Resources Ltd

- 6.4.3 American Elements

- 6.4.4 Baoji ChuangXin Metal Materials Co. Ltd (CXMET)

- 6.4.5 China Nulear JingHuan Zirconium Industry Co. Ltd.

- 6.4.6 Framatome (EDF)

- 6.4.7 Nanjing Youtian Metal Technology Co. Ltd

- 6.4.8 Phelly Materials Inc.

- 6.4.9 Starfire Systems Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Inclination on Reusable Spacecrafts

- 7.2 Growing Research on Hafnium Oxide Nanoparticles for Radiotherapy