|

市场调查报告书

商品编码

1686561

高性能隔热材料:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)High-Performance Insulation Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

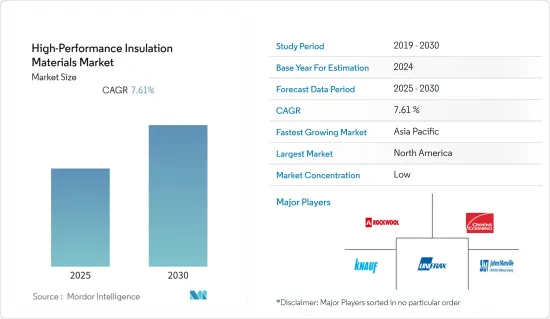

预计高性能隔热材料市场在预测期内的复合年增长率将达到 7.61%。

主要亮点

- 石油和天然气行业的使用量不断增加以及人们对温室气体排放和节能意识的不断增强预计将推动高性能隔热材料市场的成长。

- 然而,高安装和维护成本、相对较短的使用寿命以及含 CFC 的隔热材料和泡沫产品的高可燃性预计将阻碍市场成长。

- 预计亚太地区基础设施活动投资的增加将为所研究的市场带来新的机会。

高性能隔热材料的市场趋势

石油和天然气产业的需求不断成长

- 热的油气混合物在井口上升,透过XMT、歧管、各种关键设备、短管和出油管线输送,然后由立管将油输送到地面。

- 高性能隔热材料在石油和天然气领域的需求庞大,这主要是由于海底管线应用需求的不断增加。

- 此外,这些材料还具有石油和天然气行业所需的特性,例如防火防水、优异的耐热性、增强的隔音性、重量轻和外形薄。

- 根据经济产业省统计,2021年日本原油产量约49万千公升,较上年的约51.2千万公升有所下降。

- 加拿大统计局称,2021 年 10 月美国原油及等效产品产量增加 10.8%,达到 2,440 万立方米,为 2019 年 12 月以来的最高原油产量。

- 预计上述因素将在预测期内推动高性能隔热材料的使用。

亚太地区占市场主导地位

- 预计预测期内亚太地区将主导高性能隔热材料市场。

- 该地区石油天然气和建筑业的成长极大地推动了对这些隔热板的需求。

- 由于对能源和石化产品的需求不断增加,亚太地区的石油和天然气产业正在成长。印度、马来西亚、印尼、中国、韩国和日本等国家正在增加海上钻井活动。

- 2022年1-2月中国原油产量为3,347万吨,年增约4.6%。根据中国国家统计局统计,原油日产量接近57.6万吨。

- 根据OICA统计,2021年汽车产量为7,846,955辆,较2020年的8,067,557辆下降3%。不过,预计预测期内日本对电动车的需求将会成长。

- 在航太领域,根据印度品牌股权基金会 (IBEF) 的数据,预计未来四年印度航空业将吸引 3,500 亿印度卢比(49.9 亿美元)的投资。

- 上述因素可能会在预测期内增加对高性能隔热材料的需求。

高性能隔热材料产业概况

全球高性能隔热材料市场高度分散,前十大公司在研究市场中占有相当大的份额。市场的主要企业包括欧文斯科宁、可耐福 Gips KG、Rockwool、Johns Manville、Unifrax 等(排名不分先后)。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 在石油和天然气产业的应用日益广泛

- 提高温室气体排放与节能意识

- 限制因素

- 安装维护成本高,使用寿命相对较短

- 含氯氟烃的隔热材料及泡沫产品易燃性高

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔

- 依材料类型

- 气凝胶

- 真空绝热板(VIP)

- 玻璃纤维

- 陶瓷纤维

- 高性能泡沫

- 其他的

- 按最终用户产业

- 石油和天然气

- 产业

- 建筑与施工

- 运输

- 发电

- 其他的

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 北美其他地区

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章竞争格局

- 併购、合资、合作与协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- 3M

- Aerogel Technologies LLC

- Armacell

- Aspen Aerogels Inc.

- BASF SE

- Cabot Corporation

- IBIDEN

- Isolite Insulating Products Co. Ltd

- Johns Manville

- Knauf Gips KG

- Luyang Energy-Saving Materials Co. Ltd

- Morgan Advanced Materials

- Owens Corning

- Panasonic Corporation

- PAR Group

- Rath Group

- ROCKWOOL Group

- Saint-Gobain

- Unifrax

第七章 市场机会与未来趋势

- 增加亚太地区基础建设投资

简介目录

Product Code: 52653

The High-Performance Insulation Materials Market is expected to register a CAGR of 7.61% during the forecast period.

Key Highlights

- The growing usage in the oil and gas industry and rising awareness regarding greenhouse emissions and energy savings are likely to drive the growth of the high-performance insulation materials market.

- On the flip side, high set-up and maintenance costs, relatively low service life, and high flammability with insulated materials and foam products that contain CFC are expected to hinder the market's growth.

- Increasing investments in infrastructural activities in Asia-Pacific are expected to unveil new opportunities for the market studied.

High Performance Insulation Materials Market Trends

Increasing Demand from the Oil and Gas Industry

- The hot oil and gas composition flows up at the wellhead and is transported through XMTs, manifolds, various critical instruments, spools, and flow lines before the riser brings the oil to the surface.

- High-performance insulation materials are witnessing a huge demand from the oil and gas sector, primarily owing to the increasing demand for subsea pipeline applications.

- Additionally, these materials offer properties, such as fire and water resistance, excellent thermal resistance, enhanced acoustic insulation, lightweight, and reduced thickness, that are required in the oil and gas sector.

- According to the Ministry of Economy, Trade, and Industry (METI), in 2021, approximately 490 thousand kiloliters of crude oil were produced in Japan, down from about 512 thousand kiloliters in the previous year.

- According to StatCan, the production of crude oil and equivalent products in the United States rose 10.8% in October 2021 to 24.4 million cubic meters, the highest crude production level since December 2019.

- The aforementioned factors are likely to result in an increase in the usage of high-performance insulation materials during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific is expected to dominate the market for high-performance insulation materials during the forecast period.

- The growth in the oil and gas and the construction sector in the region has significantly boosted the demand for such insulation panels.

- The oil and gas industry in the Asia-Pacific region is growing due to the increasing demand for energy and petrochemicals. Countries such as India, Malaysia, Indonesia, China, South Korea, and Japan are experiencing increased offshore drilling activities.

- The crude oil output of China has registered at 33.47 million tons in the first two months of 2022, which is about 4.6% up from the same period of the previous year. According to the National Bureau of Statistics China, the daily output of crude oil is nearly 576,000 tons.

- According to OICA, the production of vehicles in 2021 accounted for 78,46,955 units, a fall of 3% compared to 80,67,557 units produced in 2020. However, the demand for electric vehicles in Japan is projected to grow over the forecast period.

- In the aerospace sector, according to the India Brand Equity Foundation (IBEF), the country's aviation industry is expected to witness INR 35,000 crore (USD 4.99 billion) investment in the next four years.

- The aforementioned factors will likely increase the demand for high-performance insulation materials during the forecast period.

High Performance Insulation Materials Industry Overview

The global High-Performance Insulation Materials Market is highly fragmented, with the top 10 players capturing a noticeable share in the market studied. Some of the major players in the market include (not in any particular order) Owens Corning, Knauf Gips KG, Rockwool, Johns Manville, and Unifrax, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Usage in the Oil and Gas Industry

- 4.1.2 Rising Awareness Regarding Greenhouse Emissions and Energy Savings

- 4.2 Restraints

- 4.2.1 High Set-up and Maintenance Costs and Relatively Low Service Life

- 4.2.2 High Flammability with Insulated Materials and Foam Products that Contain CFC

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Material Type

- 5.1.1 Aerogel

- 5.1.2 Vacuum Insulation Panel (VIP)

- 5.1.3 Fiberglass

- 5.1.4 Ceramic Fiber

- 5.1.5 High-performance Foam

- 5.1.6 Other Material Types

- 5.2 End-user Industry

- 5.2.1 Oil and Gas

- 5.2.2 Industrial

- 5.2.3 Building and Construction

- 5.2.4 Transportation

- 5.2.5 Power Generation

- 5.2.6 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.2.4 Rest of North America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Aerogel Technologies LLC

- 6.4.3 Armacell

- 6.4.4 Aspen Aerogels Inc.

- 6.4.5 BASF SE

- 6.4.6 Cabot Corporation

- 6.4.7 IBIDEN

- 6.4.8 Isolite Insulating Products Co. Ltd

- 6.4.9 Johns Manville

- 6.4.10 Knauf Gips KG

- 6.4.11 Luyang Energy-Saving Materials Co. Ltd

- 6.4.12 Morgan Advanced Materials

- 6.4.13 Owens Corning

- 6.4.14 Panasonic Corporation

- 6.4.15 PAR Group

- 6.4.16 Rath Group

- 6.4.17 ROCKWOOL Group

- 6.4.18 Saint-Gobain

- 6.4.19 Unifrax

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Investments in Infrastructural Activities in Asia-Pacific