|

市场调查报告书

商品编码

1686571

自我调整安全:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Adaptive Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

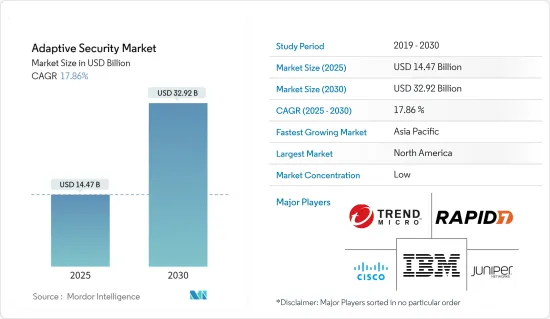

自我调整安全市场规模预计在 2025 年为 144.7 亿美元,预计到 2030 年将达到 329.2 亿美元,预测期内(2025-2030 年)的复合年增长率为 17.86%。

主要亮点

- 企业面临不断演变的威胁,包括进阶持续性威胁、零时差恶意软体和各种有针对性的攻击。这些现代网路攻击具有动态性和协调性,旨在利用组织传统防御中的弱点。

- 企业越来越多地采用预防策略来追踪这些无法侦测的威胁,以保护其组织的资料、网路和应用程式。对安全合规性和法规的日益增长的需求以及保护 IT 资源免受先进和复杂的网路攻击的需求是预计在预测期内推动自我调整安全市场发展的关键因素。

- 据律师事务所 DLA Piper 称,自 2018 年 5 月《一般资料保护规范》(GDPR)在欧洲生效以来,截至 2023 年 1 月,荷兰是报告个人资料外洩事件最多的国家,总数约为 117,434 起。德国位居第二,报告的个人资料外洩事件超过 76,000 起。此类资料外洩事件的激增正在推动市场需求。

- 此外,5G 的出现有望促进已迈向工业 4.0 的产业使用连网型设备。它正在透过物联网的兴起帮助实现各个行业的蜂窝连接。机器对机器的连接正在推动应用程式的安全性。

- 有效实施自我调整安全解决方案主要需要专业知识。由于缺乏熟练的网路安全专业人员,组织难以正确配置和部署这些解决方案,从而限制了它们减轻威胁和漏洞的有效性。

- 由于封锁和保持社交距离措施,COVID-19 疫情迫使大多数组织转向在家工作模式,从而对远端管理和监控应用程式产生了巨大的需求。随着组织对其应用服务的要求越来越高,对自我调整安全性的需求也随之增加。

自我调整安全市场趋势

云端部署模式显着成长

- 云端服务的日益普及要求出现自适应云端安全解决方案,该解决方案可以动态适应并响应不断演变的威胁以提供安全性。

- 云端基础的自我调整安全解决方案有助于与任何云端服务供应商的无缝集成,使企业能够利用其现有的云端基础设施,同时增强安全功能,加速所有垂直行业采用云端基础的自我调整安全解决方案。

- 随着企业为了实现可扩展性和成本效益而越来越多地将工作负载和资料迁移到云端,对旨在保护云端环境的安全解决方案的需求也日益增加。传统的内部部署解决方案不适合云端基础架构的动态和分散式特性,这推动了对云端基础的自我调整安全解决方案和服务的需求。

- 例如,Flexera Software 对来自世界各地组织的 627 名技术专业人士进行的一项调查发现,截至 2023 年,50% 的企业已经在公共云端中部署了工作负载,7% 的企业计划在未来一年内将更多工作负载迁移到云端。此外,48% 的受访者表示他们将资料储存在公共云端上。

- 基于最终用户垂直领域,BFSI 产业预计将推动对云端基础的自我调整安全解决方案和服务的需求。随着 BFSI 行业越来越多地采用云端平台,对自我调整安全解决方案的需求也日益增长,该解决方案可以透过存取与安全性和合规性要求相关的特定产业属性来提供安全性。因此,将复杂的业务和多方面的监管需求与行业中正确的云端平台业务相结合的需求正在推动对云端安全等应用中自我调整安全解决方案和服务的需求。

- 市场上的供应商正在推出云端基础的自我调整安全解决方案,以提供自动化、客製化的保护。例如,Egress 于 2023 年 7 月开始提供应用自我调整安全模式的云端电子邮件安全平台。随着该解决方案的推出,该公司提供针对高级入境和出站威胁的动态、自动化防护,从而改变组织透过电子邮件管理人员风险的方式。

- 云端基础的自我调整安全的需求是由云端运算的日益普及、混合和多重云端环境日益复杂以及与云端原生技术的整合所推动的。预计各行各业采用云端技术将在预测期内推动云端基础的自我调整安全的需求。

北美占据主要市场占有率

- 对网路、端点、应用程式和云端安全等一系列安全解决方案的需求日益增长,推动了北美采用自我调整安全。该地区致力于提高网路安全以应对不断变化的网路威胁,并需要先进的安全技术来保护关键资料和系统,这是推动自我调整安全解决方案市场发展的关键因素。此外,对数位技术的依赖性增加、网路攻击激增以及遵守法规的需要等因素都促使北美越来越多地采用自我调整安全。

- 美国在网路安全研发方面投入了大量资金。例如,2023年8月,美国能源局(DOE)向小型和农村电力公司开放了900万美元的竞争性联邦资金,以改善网路安全。这将允许电力行业的小型和地方公用事业公司和合作社申请一笔资金,在其基础设施中建立网路弹性,以防范网路攻击、勒索软体和其他数位威胁。

- 此外,加拿大的网路犯罪正在迅速增长,其影响也不断增加。 2023年8月,加拿大通讯安全局(CSE)发布报告,详细记录了加拿大发生的70,878起网路诈骗,导致超过3.9亿美元被盗。在加拿大,勒索软体攻击和资料外洩等网路威胁变得越来越频繁和复杂,刺激了对网路安全解决方案的投资,以防范新的威胁。

- 2024年1月,提供自适应和自主身分安全解决方案的公司Oleria在A轮资金筹措中筹集了3,300万美元。此次投资使该公司的总资金筹措超过 4,000 万美元,由 Evolution Equity Partners主导,Salesforce Ventures、Tapestry VC 和 Zscaler 参投。这笔资金筹措将使 Oleria 能够扩大招聘,以加强整体产品创新,包括其人工智慧能力和打入市场策略。

- 整体而言,社会对网路安全风险和网路威胁潜在后果的认知不断提高,更加重视实施有效的网路安全措施。这些因素共同凸显了网路安全在北美的重要性,推动了各行各业对先进解决方案和主动网路安全策略的需求,从而极大地推动了市场的成长机会。

自我调整安全产业概览

自我调整安全市场高度分散,既有全球参与者,也有中小型企业。市场的主要参与者包括思科系统公司、趋势科技公司、Rapid7 公司、IBM 公司和瞻博网路公司。市场参与者正在采用合作和收购等方式来加强其解决方案产品并获得永续的竞争优势。

2023 年 11 月,Trellix 宣布了其生成人工智慧 (GenAI) 功能,该功能基于 Amazon Bedrock 构建,主要由 Trellix 高级研究中心提供支援。透过扩大与 AWS 的伙伴关係,Trellix 继续投资 GenAI,以提供增强的威胁补救和改进的客户支援。

2023 年 11 月,趋势科技推出了 Trend Companion,这是一款新型生成式 AI 工具,主要旨在透过推动高效的工作流程和提高生产力来增强安全分析师的能力。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- 宏观经济因素如何影响市场

第五章市场动态

- 市场驱动因素

- 需要保护 IT 资源免受进阶网路攻击

- 安全合规和法规的必要性

- 市场限制

- 缺乏熟练的网路安全专业人员

第六章市场区隔

- 按应用

- 应用程式安全

- 网路安全

- 端点安全

- 云端安全

- 透过提供

- 服务

- 解决方案

- 按实施模型

- 本地

- 云

- 按最终用户

- BFSI

- 政府和国防

- 製造业

- 卫生保健

- 能源与公共产业

- 资讯科技/通讯

- 其他的

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

第七章竞争格局

- 公司简介

- Cisco Systems Inc.

- Trend Micro Incorporated.

- Rapid7 Inc.

- IBM Corporation

- Juniper Networks Inc.

- Trellix(STG Partners LLC)

- Panda Security Inc.(Watchguard Technologies Inc.)

- Illumio Inc.

- Lumen Technologies Inc.

- Aruba Networks Inc.(Hewlett Packard Enterprise Development LP)

第八章投资分析

第九章 市场机会与未来趋势

The Adaptive Security Market size is estimated at USD 14.47 billion in 2025, and is expected to reach USD 32.92 billion by 2030, at a CAGR of 17.86% during the forecast period (2025-2030).

Key Highlights

- A significant factor driving the demand growth is that firms are constantly being attacked by progressive threats such as advanced persistent threats, zero-day malware, and different targeted attacks. Dynamic and orchestrated, these modern cyberattacks seek to exploit weaknesses in an organization's traditional defenses.

- Enterprises have been adopting prevention strategies to increasingly keep track of such undetectable threats to protect the organizations' data, networks, and applications. The growing need for security compliances and regulations and the need to secure IT resources from sophisticated and complex cyberattacks are major factors expected to drive the adaptive security market over the forecast period.

- Law firm DLA Piper states that since the Europe-wide implementation of the General Data Protection Regulation (GDPR) in May 2018, the highest number of personal data breaches as of January 2023 were reported in the Netherlands, a total of around 117,434. Germany ranked second, with more than 76,000 private data breach notifications. Such a massive rise in data breaches is propelling the demand for the market.

- In addition, the advent of 5G is expected to expedite the use of connected devices in industries already pushing toward Industrial Revolution 4.0. This revolution has aided cellular connectivity throughout the industry through the rise of loT. Machine-to-machine connections are driving the traction of application security.

- Adaptive security solutions primarily need specialized expertise to be implemented effectively. Due to the lack of skilled cybersecurity professionals, organizations struggle to configure and deploy these solutions properly, limiting their effectiveness in mitigating threats and vulnerabilities.

- With the outbreak of COVID-19, most of the organization shifted to the work-from-home model due to the lockdown and social distancing measures that created a significant demand to manage and monitor applications remotely. As a result of the rising demand from organizations for adaptive security for their application services, the need for them increased.

Adaptive Security Market Trends

Cloud Deployment Model to Witness Major Growth

- The growing adoption of cloud services has necessitated the emergence of adaptive cloud security solutions, which dynamically adjust and respond to evolving threats and offer security.

- Cloud-based adaptive security solutions help seamlessly integrate with any cloud service providers, enabling organizations to leverage their existing cloud infrastructure while enhancing security capabilities and driving the adoption of cloud-based adaptive security solutions by organizations across industries.

- The increasing migration of workloads and data by businesses to the cloud for scalability and cost-effectiveness creates a growing need for security solutions designed to protect cloud environments. As traditional on-premises solutions are not suited to the dynamic and distributed nature of cloud infrastructure, the demand for cloud-based adaptive security solutions and services is increasing.

- For instance, according to a survey of 627 technical professionals across a cross-section of organizations globally by Flexera Software, as of 2023, 50% of enterprises already had workloads in the public cloud, with 7% planning to move additional workloads to the cloud in the next 12 months. In addition, 48% of the respondents reported having data stored on the public cloud.

- By end-user industry, the BFSI segment is expected to drive demand for cloud-based adaptive security solutions and services. As the BFSI industry is increasingly adopting cloud platforms, accessing industry-specific attributes related to security and compliance requirements is driving the need for adaptive security solutions to enable security. Thus, the need to match the complexities of operations and multi-faceted regulatory demands with the right cloud platform businesses in the industry is driving the need for adaptive security solutions and services in applications such as cloud security.

- The market vendors are introducing cloud-based adaptive security solutions and offering automated and tailored protection. For instance, in July 2023, Egress started offering a cloud email security platform to apply an adaptive security model. With the launch of this solution, the company would offer dynamic and automated protection against advanced inbound and outbound threats, transforming how organizations manage human risk via email.

- The demand for cloud-based adaptive security is growing due to the increasing adoption of cloud computing, the complexity of hybrid and multi-cloud environments, and the integration with cloud-native technologies. Implementing cloud technology across industries is anticipated to create demand for cloud-based adaptive security over the forecast period.

North America to Hold Significant Market Share

- The rising need for various security solutions, including network, endpoint, application, and cloud security, drives adaptive security adoption in North America. The region's focus on improving cybersecurity to address changing cyber threats and the requirement for advanced security technologies to safeguard critical data and systems are key factors driving the adaptive security solutions market. Furthermore, factors such as the growing reliance on digital technologies, the surge in cyberattacks, and the necessity for regulatory compliance all contribute to the rising implementation of adaptive security in North America.

- The United States has invested significantly in cybersecurity research and development. For instance, in August 2023, the United States Department of Energy (DOE) opened USD 9 million in competitive federal funding for small and rural electric utilities to improve cybersecurity. This will allow smaller and rural utilities and cooperatives in the electric sector to apply for chunks of funding to build more cyber resilience in their infrastructure that could defend against cyberattacks, ransomware, and other digital threats.

- Moreover, cybercrime is rapidly gaining traction in Canada, and its impact is increasing. In August 2023, the Communications Security Establishment (CSE) released a report detailing 70,878 cyber fraud cases in Canada, resulting in over USD 390 million being stolen. Organizations in Canada are investing in cybersecurity solutions to guard against emerging threats due to the mounting frequency and sophistication of cyber threats, such as ransomware attacks and data breaches.

- In January 2024, Oleria, a company providing adaptive and autonomous identity security solutions, raised USD 33 million in a Series A funding round. This latest investment, which brings the company's total funding to more than USD 40 million, is led by Evolution Equity Partners with participation from Salesforce Ventures, Tapestry VC, and Zscaler. This funding round allows Oleria to ramp up hiring to enhance its overall product innovation, involving AI capabilities and its go-to-market strategy.

- Overall, increased public awareness of cybersecurity risks and the potential consequences of cyber threats has contributed to a greater emphasis on implementing effective cybersecurity measures. The combination of these factors underscores the critical importance of cybersecurity in North America, leading to a growing demand for advanced solutions and proactive cybersecurity strategies across industries, driving the market's growth opportunities significantly.

Adaptive Security Industry Overview

The adaptive security market is highly fragmented due to the presence of both global players and small and medium-sized enterprises. Some of the major players in the market are Cisco Systems Inc., Trend Micro Incorporated., Rapid7 Inc., IBM Corporation, and Juniper Networks Inc. Players in the market are adopting approaches such as partnerships and acquisitions to enhance their solutions offerings and gain sustainable competitive advantage.

In November 2023, Trellix launched its generative Artificial Intelligence (GenAI) capabilities, built on Amazon Bedrock and mainly supported by Trellix Advanced Research Center. By expanding its partnership with AWS, Trellix continues investing in GenAI to deliver enhanced threat remediation and improved customer support.

In November 2023, Trend Micro launched its new generative AI tool, Trend Companion, mainly built to empower security analysts by driving efficient workflows and enhanced productivity.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Need to Secure IT Resources from Advanced Cyberattacks

- 5.1.2 Need for Security Compliances and Regulations

- 5.2 Market Restraints

- 5.2.1 Lack of Skilled Cyber Security Professionals

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Application Security

- 6.1.2 Network Security

- 6.1.3 End Point Security

- 6.1.4 Cloud Security

- 6.2 By Offering

- 6.2.1 Service

- 6.2.2 Solution

- 6.3 By Deployment Model

- 6.3.1 On-premise

- 6.3.2 Cloud

- 6.4 By End User

- 6.4.1 BFSI

- 6.4.2 Government and Defense

- 6.4.3 Manufacturing

- 6.4.4 Healthcare

- 6.4.5 Energy and Utilities

- 6.4.6 IT and Telecom

- 6.4.7 Other End Users

- 6.5 By Geography

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia

- 6.5.4 Australia and New Zealand

- 6.5.5 Latin America

- 6.5.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Cisco Systems Inc.

- 7.1.2 Trend Micro Incorporated.

- 7.1.3 Rapid7 Inc.

- 7.1.4 IBM Corporation

- 7.1.5 Juniper Networks Inc.

- 7.1.6 Trellix (STG Partners LLC)

- 7.1.7 Panda Security Inc. (Watchguard Technologies Inc.)

- 7.1.8 Illumio Inc.

- 7.1.9 Lumen Technologies Inc.

- 7.1.10 Aruba Networks Inc.(Hewlett Packard Enterprise Development LP)