|

市场调查报告书

商品编码

1686665

工业马达:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)Industrial Motors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

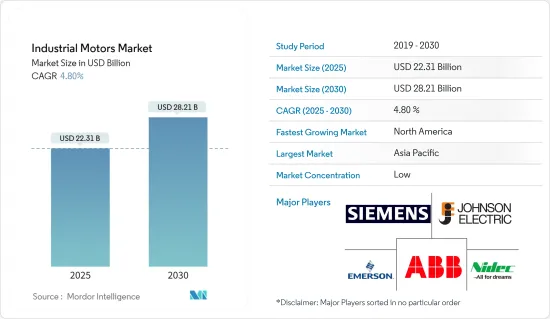

预计 2025 年工业马达市场规模为 223.1 亿美元,到 2030 年将达到 282.1 亿美元,预测期内(2025-2030 年)的复合年增长率为 4.8%。

工业马达是电子机械。工业马达旨在为製造、石油和天然气、建筑、运输等领域使用的各种设备和机械提供动力和动力。这些马达通常比住宅和商业应用中使用的马达更坚固、更强大,因为它们必须承受高负载并在恶劣的环境中运行。

主要亮点

- 马达是工业生产的驱动力。监控、调整、测试和连接马达的创新方法可以节省时间和金钱并提高安全性。同时,节能马达和智慧驱动器可提高效率和性能并简化故障排除。

- 随着世界朝着能源效率和永续性的方向发展,製造商越来越多地选择节能马达。这些选择旨在降低能源消耗和营业成本,其中 IE4 高效能马达因比旧型号节省大量能源而脱颖而出。

- 全球工业化正在推动对节能马达的需求。随着行业的建立和扩张,对降低能耗和营业成本的马达的需求变得至关重要。这些节能马达提高了效率并最大限度地减少了能量损失,从长远来看可以显着节省成本。这种不断增长的需求涉及製造业、农业、建设业和运输业等多个领域。

- 自动化系统对于製造、工程、建筑和发电至关重要,可提高效率和生产力。在人工智慧 (AI)、云端处理、巨量资料和物联网 (IoT) 的推动下,工业自动化正在快速发展。

- 儘管有这些优点,但仍存在一些挑战阻碍节能马达的广泛应用。基本限制包括能源、维护和初始购买等相关成本。此外,生产节能马达需要优质的材料、先进的製造技术以及严格的测试和认证。这些要求可能会增加製造商的生产成本,并导致消费者支付更高的价格。

工业马达市场趋势

石油和天然气产业预计将成长

- 由于需要工业马达为钻井、采矿、精製和运输等各种过程提供动力,石油和天然气产业目前在市场中处于领先地位。随着人们对气候变迁和减少二氧化碳排放的需求的认识不断提高,石油和天然气产业逐渐意识到节能马达的重要性。

- 据估计,交流感应马达将在石油和天然气行业中普及,因为它们广泛应用于泵浦、压缩机、涡轮机以及石油和天然气的开采、加工和从精製场到炼油厂再销售给消费者的运输中。此外,低压感应马达也用于炼油厂驱动泵浦、压缩机和搅拌器,将原油转化为汽油、柴油和喷射机燃料等多种产品。

- 开发中国家快速都市化伴随着能源需求的大幅增加。这将导致液体燃料和天然气的消费量增加。例如,根据英国石油公司预测,2023年天然气产量将达到4.8兆立方公尺。全球对电力和燃料的需求日益增长,推动了对石油和天然气的需求。

- 随着对石油和天然气的需求增加,勘探与生产机械、设备及零件的市场也在成长。因此,石油和天然气产业的下游和上游部分对各种容量的AC马达的需求也在增加。

- 据贝克休斯称,北美拥有世界上最多的石油和天然气钻机。截至 2024 年 8 月,该区共有陆上钻井钻机781 个,海上钻机23 个。至2023年,全球石油钻机数量平均将超过1,800座。

预计北美将占据较大的市场占有率

- 工业马达市场主要受到美国越来越多专注于工业 4.0 的工业的推动。预计工业自动化将在预测期内实现强劲成长,因为它可以帮助製造商生产更有效率的产品。这种模式引发了开发新型工业马达的愿望。预计工业自动化在各行业的渗透率将会更加均衡。因此,预计美国工业马达市场将得到发展,以满足工业自动化的成长。

- 随着产业和消费者寻求减少能源消耗并尽量减少碳排放,对节能解决方案的需求日益增加。众所周知,工业马达比传统马达效率更高、能量损失更少。

- 石油和天然气是一个涉及钻井作业以使用钻井机从储存中提取原油和天然气的行业。马达是钻井设备常见的动力来源。贝克休斯称,北美在石油和天然气钻井平台持有居世界之冠。截至 2024 年 8 月,该地区共有 781 个陆上钻机,另有 23 个海上钻机。 2023年底,美国将有500台石油天然气旋转钻机和120台天然气旋转钻机运作,总合622运作旋转钻机。

- 加拿大已经实施了能源效率法规,将低效马达从市场淘汰。加拿大公司可以透过该性能标准获得 NEMA MG-1 提供的马达效率指南。这些法规涵盖功率从 1 到 500 马力的三相感应马达。这些性能标准涵盖了製造和工业应用中使用的大多数马达。企业主必须遵守这些能源标准。

- 加拿大政府采取了多项倡议来促进加拿大製造业的发展,包括对新投资实施税收减免、与各国签订贸易协定、投资新技术以及开展多项技能培训计划。加拿大政府也进行了投资,以确保当地企业和企业家拥有成功所需的工具。

- 例如,2024 年 7 月,日立能源加拿大公司从加拿大政府获得 3,000 万加元(2,154 万美元)的资金。这笔资金将有助于在蒙特娄建立一个新的高压直流模拟中心,并对瓦雷纳的电力变压器工厂进行现代化改造。这些努力旨在满足北美对永续能源日益增长的需求。

工业马达市场概况

竞争程度取决于影响市场的各种因素,例如品牌识别、强大的竞争策略和透明度。

工业马达市场由各种知名公司代表,例如 ABB、艾默生电气公司、日本电产工业解决方案、德昌电机控股有限公司和西门子股份公司。在这个市场中,每家公司的品牌形像都具有很大的影响力。由于强大的品牌是良好业务表现的代名词,因此老字型大小企业有望占据优势。

在一个很可能透过创新获得永续竞争永续的市场中,随着采矿、石油天然气和能源等终端用户产业新客户需求的预期激增,竞争只会加剧。由于大型现有企业的存在,市场渗透率也很高。

由于市场渗透率和提供先进产品的能力,预计未来竞争对手之间的竞争仍将保持在高水准。市场上有各种各样的公司,但只有少数公司凭藉高标准和卓越品质脱颖而出。

随着综合技术的进步和地缘政治格局的扩大,所研究的市场正经历波动。除此之外,主要产业参与者也考虑其收入产生的投资能力,并依赖其附属公司作为原料供应商。

创新水准、上市时间和绩效是公司在研究市场中脱颖而出的关键标准。

总体而言,研究市场参与者之间的竞争正在加剧,由于行业的成长,预计在预测期内竞争仍将保持高水准。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 和其他宏观经济因素对市场的影响

第五章市场动态

- 市场驱动因素

- 政府法规推动能源效率需求

- 向智慧马达的转变日益明显

- 市场挑战

- 便携性问题

- 购买新设备和升级现有设备的前期投资较高

第六章市场区隔

- 依马达类型

- 交流马达

- 直流马达

- 其他马达(伺服马达和电子换向马达(EC马达))

- 按电压

- 高压

- 中压

- 低电压

- 按最终用户

- 石油和天然气

- 发电

- 矿业与金属

- 用水和污水管理

- 化工和石化

- 离散製造

- 其他最终用户

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

第七章竞争格局

- 公司简介

- ABB Ltd.

- Emerson Electric Co.

- Siemens AG

- Nidec Industrial Solutions

- Johnson Electric Holdings Limited

- Arc Systems Inc.

- Ametek Inc.

- Toshiba Electronic Devices and Storage Corporation

- Wolong Industrial Motors

- Allen-Bradly Co. LLC(Rockwell Automation Inc.)

- Maxon Motor AG

- Franklin Electric Co. Inc.

- Fuji Electric Co. Ltd

- ATB Austria Antriebstechnik AG

- Menzel Elektromotoren GmbH

第八章投资分析

第九章:市场的未来

The Industrial Motors Market size is estimated at USD 22.31 billion in 2025, and is expected to reach USD 28.21 billion by 2030, at a CAGR of 4.8% during the forecast period (2025-2030).

An industrial motor is an electrical machine that converts electrical energy into mechanical energy to perform various tasks in industrial settings. Industrial motors are designed to provide power and motion to different equipment and machinery used in manufacturing, oil and gas, construction, transportation, etc. These motors are typically more robust and powerful than motors used in residential or commercial applications, as they need to withstand heavy loads and operate in demanding environments.

Key Highlights

- Motors drive industrial production. Innovative methods in motor monitoring, alignment, testing, and connections save time and costs and enhance safety. Concurrently, energy-saving motors and intelligent drives elevate efficiency and performance and simplify troubleshooting.

- With a global push towards energy efficiency and sustainability, manufacturers are increasingly opting for energy-efficient motors. These choices aim to reduce energy consumption and operating costs, with IE4 efficiency motors standing out for their significant energy savings over older models.

- Global industrialization has heightened the demand for energy-efficient motors. As industries establish and expand, the need for motors that curtail energy consumption and operating costs becomes paramount. These energy-efficient motors enhance efficiency and minimize energy loss, leading to notable cost savings over time. This growing demand spans multiple sectors, including manufacturing, agriculture, construction, and transportation.

- Automation systems are pivotal for manufacturing, engineering, construction, and power generation, driving enhanced efficiency and productivity. Industrial automation is witnessing rapid advancements fueled by artificial intelligence (AI), cloud computing, Big Data, and the Internet of Things (IoT).

- Despite the advantages, several challenges hinder the widespread adoption of energy-efficient motors. Fundamental limitations include the associated costs: energy, maintenance, and initial purchase. Furthermore, producing energy-efficient motors demands superior materials, advanced manufacturing techniques, and rigorous testing and certification. These requirements can inflate production costs for manufacturers, leading to higher consumer prices.

Industrial Motors Market Trends

The Oil and Gas Segment is Expected to Witness Growth

- The oil and gas sector is currently leading the market due to its need for industrial motors to power a range of processes, including drilling, extraction, refining, and transportation. Due to increasing awareness of climate change and the necessity of decreasing CO2 emissions, the oil and gas industry is progressively acknowledging the significance of energy-efficient motors.

- Due to the significant use of AC induction motors in pumps, compressors, and turbines, as well as their application for extraction, processing, and transport of oil and gas from drilling sites into refineries, which are sold to consumers, it is estimated that these motors will be trendy within the oil and gas industry. In addition, low-voltage induction motors are used in refineries for drive pumps, compressors, and agitators to convert crude oil into multiple products such as gasoline, diesel, and jet fuel.

- Rapid urbanization in developing nations accompanies a considerable increase in energy demand. Consequently, the consumption of liquid fuels and natural gas rises. For instance, according to BP, natural gas production amounted to 4.08 trillion cubic meters in 2023. The escalating global need for electricity and fuel has increased the demand for oil and natural gas.

- With rising oil and gas demand, the market for E&P machines, equipment, and components is growing. As a result, the need for AC motors used in different capacities within the downstream and upstream segments of the oil and gas industry is also increasing.

- According to Baker Hughes, North America hosts oil and gas rigs globally. As of August 2024, the region boasted 781 land rigs and 23 offshore rigs. In 2023, the global count of oil rigs surpassed 1,800 units on average.

North America is Expected to Hold Significant Market Share

- Industrial motor markets are mainly driven by the increasing focus of industries on Industry 4.0 within the United States. Industrial automation encourages manufacturers to produce more effective products, with solid growth expected throughout the projection period. This pattern would result in a desire to develop new industrial motor machines. The spread of industrial automation across all sectors is expected to be evenly distributed. Consequently, to cope with industrial automation's growth, the market for industrial motors is predicted to develop in the United States.

- As industries and consumers seek to reduce energy consumption and minimize their carbon footprint, there is a growing demand for energy-efficient solutions. Industrial electric motors are known for their higher efficiency and lower energy losses than traditional motors.

- Oil and gas is an industry in which drilling operations are carried out to extract crude oil and natural gas from reservoirs using drilling rigs. Electric motors are a common source of power for drilling equipment. According to Baker Hughes, North America leads the world in hosting oil and gas rigs. As of August 2024, the region boasted 781 land rigs and an additional 23 offshore. By the end of 2023, the United States had 500 active rotary oil rigs and 120 gas rigs, contributing to a total rotary rig count of 622.

- Canada has implemented energy efficiency regulations to remove inefficient motors from the market. The guidelines for motor efficiency, provided by NEMA MG-1, are available to Canada's businesses through these performance standards. These regulations cover three-phase induction motors with power between 1 and 500 horsepower. These performance standards cover most motors used in manufacturing and industrial applications. Compliance with these energy standards is mandatory for business owners.

- The Government has taken several initiatives to foster Canada's manufacturing sector, including tax reductions on new investments, various trade agreements with different countries, investment in new technologies, and many skill training programs. The Canadian Government has also invested in local companies and entrepreneurs to ensure they have the tools necessary for success.

- For instance, in July 2024, Hitachi Energy Canada secured CAD 30 million (USD 21.54 million) in funding from the Government of Canada. This funding will help set up a new HVDC simulation center in Montreal and modernize the power transformer factory in Varennes. These initiatives aim to meet North America's surging demand for sustainable energy.

Industrial Motors Market Overview

The degree of competition depends on various factors affecting the market, such as brand identity, powerful competitive strategy, and degree of transparency.

The industrial motors market comprises various prominent players such as ABB Ltd., Emerson Electric Co., Nidec Industrial Solutions, Johnson Electric Holdings Limited, and Siemens AG, among others. The brand identity associated with the companies has a major influence in this market. As strong brands are synonymous with good performance, long-standing players are expected to have the upper hand.

In a market where the sustainable competitive advantage through innovation is considerably high, the competition is only going to increase, considering the anticipated surge in demand from new customers from the end-user industries like mining, oil and gas, energy. With the presence of large market incumbents, market penetration levels are also high

Owing to their market penetration and the ability to offer advanced products, the competitive rivalry is expected to continue to be high. Although the market comprises various players, only a handful are prominent in the market for their high standards and excellent quality.

With the growing consolidation technological advancement, and geopolitical scenarios, the studied market has been witnessing fluctuation. In addition to this, the major industry player depends on their affiliates for raw materials vendors, considering their ability to invest, which result from their revenues.

The level of innovation, time-to-market, and performance are the key terms by which the players differentiate themselves in the market studied.

Overall, the intensity of the competitive rivalry in the studied market is growing and expected to be high during the forecast period owing to the growth of the industry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Demand for Energy Efficiency Owing to Government Regulations

- 5.1.2 Growing Shift towards Smart Motors

- 5.2 Market Challenges

- 5.2.1 Portability Issues

- 5.2.2 High Initial Investment for Procuring New Equipment and Upgrading Existing Equipment

6 MARKET SEGMENTATION

- 6.1 By Type of Motor

- 6.1.1 Alternating Current (AC) Motors

- 6.1.2 Direct Current (DC) Motor

- 6.1.3 Other Types of Motors (Servo and Electronically Commutated Motors (EC))

- 6.2 By Voltage

- 6.2.1 High Voltage

- 6.2.2 Medium Voltage

- 6.2.3 Low Voltage

- 6.3 By End User

- 6.3.1 Oil & Gas

- 6.3.2 Power Generation

- 6.3.3 Mining & Metals

- 6.3.4 Water & Wastewater Management

- 6.3.5 Chemicals & Petrochemicals

- 6.3.6 Discrete Manufacturing

- 6.3.7 Other End Users

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ABB Ltd.

- 7.1.2 Emerson Electric Co.

- 7.1.3 Siemens AG

- 7.1.4 Nidec Industrial Solutions

- 7.1.5 Johnson Electric Holdings Limited

- 7.1.6 Arc Systems Inc.

- 7.1.7 Ametek Inc.

- 7.1.8 Toshiba Electronic Devices and Storage Corporation

- 7.1.9 Wolong Industrial Motors

- 7.1.10 Allen - Bradly Co. LLC (Rockwell Automation Inc.)

- 7.1.11 Maxon Motor AG

- 7.1.12 Franklin Electric Co. Inc.

- 7.1.13 Fuji Electric Co. Ltd

- 7.1.14 ATB Austria Antriebstechnik AG

- 7.1.15 Menzel Elektromotoren GmbH