|

市场调查报告书

商品编码

1687073

微灌溉系统:市场占有率分析、产业趋势与统计、成长预测(2025-2030)Micro-Irrigation Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

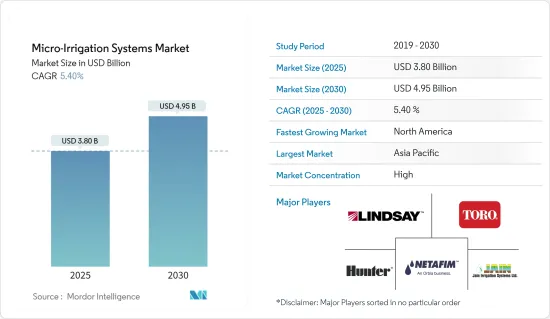

微型灌溉系统市场规模预计在 2025 年为 38 亿美元,预计到 2030 年将达到 49.5 亿美元,预测期内(2025-2030 年)的复合年增长率为 5.4%。

主要亮点

- 微灌溉系统市场正在经历令人瞩目的成长。推动这项扩张的关键因素包括全球水资源短缺、水肥一体化的广泛应用以及世界各国政府机构的大力支持。

- 值得注意的是,世界银行等知名组织正在透过微灌溉计画支持并积极推动乌干达的微灌溉,该计画是乌干达政府间财政转移结果计画(UgIFT)的一部分。对精密农业、永续农业和增加粮食产量的迫切需求进一步加强了微灌溉系统市场。

- 全球范围内微灌溉的普及正在加速,其中亚太地区处于领先地位。继中国之后,印度在该地区脱颖而出。印度多个邦政府正在推广使用微灌溉。例如,在安得拉邦微灌溉计划(APMIP)下,安得拉邦政府向拥有少于五英亩土地的农民提供灌溉设施(包括微灌溉)90%的补贴,并向拥有五英亩以上的农民提供70%的补贴。

- 由于精密农业,尤其是变数灌溉(VRI)技术的日益融合,微灌溉系统市场正在成长。这一趋势是由快速成长的食品需求所驱动,在开发中国家均有出现。透过利用监测土壤湿度和作物健康状况的感测器,基于 VRI 的微灌溉系统可以优化用水量、提高作物产量并降低投入成本。然而,高昂的初始成本和持续的维护成本对市场成长构成了障碍。

微灌溉系统市场趋势

户外种植引领细分市场

- 目前的食品生产方法高度依赖土地、水和清洁剂等资源,这引发了人们对其长期永续性的担忧。联合国预测,到2050年世界人口将接近96亿人。 2023年全球小麦产量将达7.885亿吨,米的生产量将达5.381亿吨。消费和生产趋势表明,粮食产量需要增加两倍才能充分养活世界人口。

- 农业消耗了全世界70%的水资源,而且大多数作物都是在露天田地种植的,需要耗水。这至关重要,因为农业用水直接影响饮用水和其他基本用水需求的供应。为了解决农业过度用水问题,各国政府和国际组织正大力推广微灌溉系统。

- 这些计划中常见的种植作物包括玉米、高粱、大豆、向日葵、各种谷物和豆类。此外,大量水果、蔬菜和种植作物都在露天田地中生产。灌溉系统主要有枢轴灌溉系统、喷水灌溉系统及滴灌系统。

- 有效的水资源管理对于提高埃及和其他东方国家等半干旱国家的作物水分生产率至关重要。 2023年,埃及国家水资源研究中心(NWRC)水资源管理实验室对茄子作物进行了研究。该研究重点比较了露天灌溉和地下滴灌系统对露天田土壤特性、水分生产率和产量指标的影响。研究结果强调了露地种植在节水、提高生产力和产量的有效性,尤其是在黏土条件下。

亚太地区是一个快速成长的市场

- 亚太地区引领微灌溉市场,主要原因是农业所有权分散、政府在人口密集的情况下大力推行节水措施以及提高农业产量。

- 中国是亚太地区的主要企业,也是微灌溉系统零件製造领域的全球领导者。这一有影响力的地位很大程度上归功于政府对农业实践现代化的重视。中国雄心勃勃的五年计画旨在大幅扩大其市场。至2030年,预计75%的灌溉区将采用节水微灌系统。

- 印度的农业高度依赖季风,因此与许多已开发国家相比,灌溉农业的比例较低。根据印度国家转型研究所(NITI)的报告,由于微灌溉技术和各种倡议措施的使用增加,2022-23年间,受益于可靠灌溉的耕地面积将增加 52%,达到 7,300 万公顷。

- 除中国和印度外,日本、越南、菲律宾、孟加拉和巴基斯坦等国家也对微灌溉市场产生了重大影响。微灌溉系统在这些国家的普及得益于各组织的支持和政府的大力支持。对该地区小农户来说,一个关键的奖励是该系统能够减少消费量,同时显着提高产量。

微灌溉系统产业概况

微灌溉系统市场由五大主要企业主导。随着各国政府越来越多地透过微灌溉系统提倡节约用水,市场有望实现强劲的两位数成长。塑造这一市场格局的主要企业是 Jain Irrigation Systems Limited、Netafim Limited、Lindsay Corporation、Hunter Industries 和 The Toro Company。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概况

- 市场驱动因素

- 推广缓解缺水问题的措施

- 施肥技术推广应用

- 增加政府支持

- 市场限制

- 较大的初始资本要求

- 复杂的设定带来部署挑战

- 波特五力分析– 产业吸引力

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章 市场区隔

- 机制

- 滴灌系统

- 喷水灌溉系统

- 其他微灌溉系统

- 成分

- 滴灌组件

- 滴头

- 管子

- 阀门和过滤器

- 压力调节器

- 其他滴灌组件

- 喷水灌溉组件

- 管子

- 喷嘴

- 压力调节器

- 其他喷水灌溉组件

- 滴灌组件

- 栽培技术

- 户外种植

- 保护地栽培

- 应用

- 农田作物

- 果园和葡萄园

- 蔬菜

- 种植作物

- 其他用途

- 地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 非洲

- 南非

- 埃及

- 非洲其他地区

- 北美洲

第六章 竞争格局

- 最受欢迎的策略

- 市场占有率分析

- 公司简介

- Jain Irrigation Systems Limited

- Netafim Limited

- Lindsay Corporation

- The Toro Company

- Deere & Company

- Harvel Agua

- Mahindra and Mahindra(EPC Irrigation Limited)

- Nelson Irrigation Corporation

- Rain Bird Corporation

- Elgo Irrigation Ltd

- Antelco Pty Ltd

- Kothari Agritech Private Limited

第七章 市场机会与未来趋势

The Micro-Irrigation Systems Market size is estimated at USD 3.80 billion in 2025, and is expected to reach USD 4.95 billion by 2030, at a CAGR of 5.4% during the forecast period (2025-2030).

Key Highlights

- The micro irrigation systems market is witnessing impressive growth. Key drivers fueling this expansion include global water scarcity, the rising adoption of fertigation practices, and robust backing from government entities worldwide.

- Notably, esteemed organizations like the World Bank are supporting and actively promoting micro-irrigation in Uganda through its Micro-scale Irrigation Program, which is part of the Uganda Intergovernmental Fiscal Transfers Program for Results (UgIFT). Precision farming, sustainable agriculture, and the urgent need for increased food production further bolster the micro irrigation systems market.

- Micro-irrigation adoption has accelerated globally, with Asia-Pacific leading the charge. Within this region, India stands out as the dominant player after China. Several Indian state governments are promoting the use of micro-irrigation. For instance, under the Andhra Pradesh Micro Irrigation Project (APMIP), the state government of Andhra Pradesh is offering a 90% subsidy on irrigation equipment (including micro irrigation) to farmers with less than five acres and 70% for those with larger holdings.

- The micro irrigation systems market is expanding, driven by the rising integration of precision agriculture, especially variable rate irrigation (VRI) technology. This trend is observable in developing and developed nations, fueled by surging food demand. VRI-based micro-irrigation systems optimize water usage, boost crop yields, and reduce input costs by leveraging sensors to monitor soil moisture and crop health. However, significant upfront costs and ongoing maintenance expenses challenge the market's growth.

Micro-Irrigation Systems Market Trends

Open Field Cultivation Leads the Market Segment

- Current food production methods heavily depend on resources like land, water, and detergents, sparking concerns about long-term sustainability. The United Nations (UN) forecasts the global population will near 9.6 billion by 2050. In 2023, global wheat and rice production reached 788.5 million metric tons and 538.1 million metric tons, respectively. Due to consumption and production trends, a threefold increase in food output is necessary to feed the world's population adequately.

- Agriculture consumes 70% of the world's water, with most crops grown in open fields where water use is prevalent. This is crucial, as water used in agriculture directly affects its availability for drinking and other essential needs. To address water overuse in agriculture, governments and international agencies are rigorously promoting the use of micro-irrigation systems.

- The crops commonly grown in these projects include maize, sorghum, soybean, sunflower, various grains, and legumes. Additionally, large quantities of fruits, vegetables, and plantation crops are being produced in open-field cultivation. The main irrigation systems used are pivot center systems, sprinkler irrigation systems, and drip irrigation.

- Effective water resource management is crucial for improving crop water productivity in semiarid countries like Egypt and other Eastern nations. In 2023, the Water Management Research Institute at the National Water Research Center (NWRC) in Egypt conducted a study on eggplant crops. The study focused on comparing the impact of surface and subsurface drip irrigation systems, soil characteristics, water productivity, and yield indices in open field settings. The research findings highlighted the effectiveness of open-field methods in conserving water and improving productivity and yield, particularly in clay soil conditions.

Asia-Pacific is the Fastest-growing Market

- Asia-Pacific leads the micro-irrigation market, driven by fragmented agricultural ownership, robust government initiatives aimed at water conservation for its dense population, and a heightened agricultural output.

- China, a major player in Asia-Pacific, is a global leader in manufacturing components for micro-irrigation systems. This influential position is primarily attributed to the government's dedication to modernizing agricultural practices. China's ambitious five-year plans aim for significant market expansion. By 2030, 75% of its irrigated areas will adopt water-saving micro-irrigation systems.

- Indian agriculture heavily relies on the monsoon, resulting in a lower percentage of irrigated farming than many developed nations. With the increasing use of micro-irrigation techniques and various irrigation initiatives, the amount of cultivated land benefiting from reliable irrigation has risen to 52%, which equals 73 million hectares in the 2022-23 period, according to a report by the National Institute for Transforming India (NITI) Aayog.

- Apart from China and India, countries such as Japan, Vietnam, the Philippines, Bangladesh, and Pakistan significantly impact the micro-irrigation market. The popularity of micro-irrigation systems in these nations can be attributed to endorsements from various organizations and strong government support. A key incentive for small-scale farmers across the region is the system's ability to reduce water consumption while simultaneously increasing production significantly.

Micro-Irrigation Systems Industry Overview

The micro irrigation systems market is dominated by five key players holding a significant share. As governments increasingly promote water conservation through micro-irrigation systems, the market is poised for robust double-digit growth. The leading companies shaping this market landscape are Jain Irrigation Systems Limited, Netafim Limited, Lindsay Corporation, Hunter Industries, and The Toro Company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Widespread Adoption Could Alleviate Water Scarcity Issues

- 4.2.2 Growing Adoption of Fertigation Techniques

- 4.2.3 Rising Government Support

- 4.3 Market Restraints

- 4.3.1 Significant Initial Capital Requirements

- 4.3.2 Challenges in Implementing Due to Their Intricate Setup

- 4.4 Porter's Five Forces Analysis-Industry Attractiveness -

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Mechanism

- 5.1.1 Drip Irrigation System

- 5.1.2 Sprinkler Irrigation System

- 5.1.3 Other Micro-irrigation Systems

- 5.2 Component

- 5.2.1 Drip Irrigation Components

- 5.2.1.1 Drippers

- 5.2.1.2 Tubing

- 5.2.1.3 Valves and Filters

- 5.2.1.4 Pressure Regulators

- 5.2.1.5 Other Drip Irrigation Components

- 5.2.2 Sprinkler Irrigation Components

- 5.2.2.1 Tubing

- 5.2.2.2 Nozzles

- 5.2.2.3 Pressure Regulators

- 5.2.2.4 Other Sprinkler Irrigation Components

- 5.2.1 Drip Irrigation Components

- 5.3 Cultivation Technology

- 5.3.1 Open Field

- 5.3.2 Protected Cultivation

- 5.4 Application

- 5.4.1 Field Crops

- 5.4.2 Orchards and Vineyards

- 5.4.3 Vegetables

- 5.4.4 Plantation Crops

- 5.4.5 Other Applications

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 Italy

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Jain Irrigation Systems Limited

- 6.3.2 Netafim Limited

- 6.3.3 Lindsay Corporation

- 6.3.4 The Toro Company

- 6.3.5 Deere & Company

- 6.3.6 Harvel Agua

- 6.3.7 Mahindra and Mahindra (EPC Irrigation Limited)

- 6.3.8 Nelson Irrigation Corporation

- 6.3.9 Rain Bird Corporation

- 6.3.10 Elgo Irrigation Ltd

- 6.3.11 Antelco Pty Ltd

- 6.3.12 Kothari Agritech Private Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025年全球微灌溉系统市场报告

2025年全球微灌溉系统市场报告 全球微灌溉系统市场:2032 年预测 - 按类型、组件、作物类型、分销管道、栽培技术、最终用户和地区进行分析

全球微灌溉系统市场:2032 年预测 - 按类型、组件、作物类型、分销管道、栽培技术、最终用户和地区进行分析 微灌系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

微灌系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 微灌系统市场报告,按类型(滴灌系统、喷灌系统)、作物类型(农田作物、果园作物、景观和草坪等)、最终用户(农业、工业)和地区划分,2025 年至 2033 年

微灌系统市场报告,按类型(滴灌系统、喷灌系统)、作物类型(农田作物、果园作物、景观和草坪等)、最终用户(农业、工业)和地区划分,2025 年至 2033 年 微灌溉系统市场规模、份额及成长分析(按类型、作物类型、最终用户和地区)-2025-2032 年产业预测

微灌溉系统市场规模、份额及成长分析(按类型、作物类型、最终用户和地区)-2025-2032 年产业预测 微灌溉系统市场 - 全球产业规模、份额、趋势、机会和预测,按类型、作物类型、地区和竞争细分,2019-2029F

微灌溉系统市场 - 全球产业规模、份额、趋势、机会和预测,按类型、作物类型、地区和竞争细分,2019-2029F 微型灌溉系统市场:按组件、类型、应用和最终用户划分 - 2025-2030 年全球预测

微型灌溉系统市场:按组件、类型、应用和最终用户划分 - 2025-2030 年全球预测 微灌溉系统市场:各类型,各作物类型,各终端用户,各地区,机会,预测,2017年~2031年微灌溉系统的全球市场:按机制、组件、最终用户、栽培技术、应用、区域前景、竞争策略和细分市场预测分類的市场规模(截至 2033 年)微型灌溉系统市场 - 全球产业分析、规模、份额、成长、趋势与预测,2023-2031 年

微灌溉系统市场:各类型,各作物类型,各终端用户,各地区,机会,预测,2017年~2031年微灌溉系统的全球市场:按机制、组件、最终用户、栽培技术、应用、区域前景、竞争策略和细分市场预测分類的市场规模(截至 2033 年)微型灌溉系统市场 - 全球产业分析、规模、份额、成长、趋势与预测,2023-2031 年