|

市场调查报告书

商品编码

1939581

机器学习即服务 (MLaaS):市场占有率分析、产业趋势与统计、成长预测 (2026-2031)Machine Learning As A Service (MLaaS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

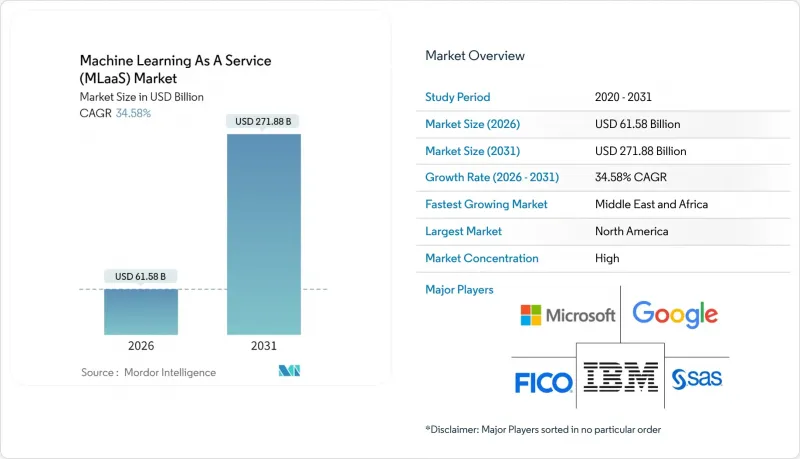

2025 年机器学习即服务 (MLaaS) 市场价值为 457.6 亿美元,预计到 2031 年将达到 2,718.8 亿美元,高于 2026 年的 615.8 亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 34.58%。

计量收费GPU实例的快速普及、生成式AI工具包的民主化以及将敏感资料保留在本国的主权云端计划,都在加速推动市场需求。企业也正在转向机器学习即服务(MLaaS),以避免在本地基础设施上投入巨额资金,同时满足即将出台的关于可解释性和资料居住的监管要求。来自中东主权财富基金的资金流入,以及新加坡、欧盟和中国的国家人工智慧战略,正在推动符合监管要求的云端区域的区域扩张。同时,基于人工智慧的威胁侦测的保费折扣以及超大规模企业的竞争性定价,进一步降低了中小企业(SME)的进入门槛。

全球机器学习即服务 (MLaaS) 市场趋势与洞察

生成式人工智慧工具包作为一种服务而大量涌现

主流云端基础架构模型目录现已包含承包、编配和向量资料库连接器。亚马逊的 Nova 套件可直接与 Bedrock 集成,使企业能够在数小时内而非数季内测试多模态原型。微软与 xAI 合作,在 Azure 上託管 Grok 3,增加了模型选择的多样性,并在 API 层整合了偏差减少遥测功能。这些创新使机器学习背景有限的开发人员也能将文字、图像和影片推理功能整合到他们的工作流程中。较低的技能要求缩短了概念验证(PoC) 週期,降低了实施成本,并扩大了机器学习即服务 (MLaaS) 市场的潜在基本客群。基于现有的付费使用制模式,财务部门将高阶人工智慧视为营运支出。

加速新兴亚洲中小企业的云端迁移

在东协地区,99%的企业都是中小企业,政府政策正在推动后勤部门营运和客户体验功能的数位化。宽频补贴、金融科技赋能的小额贷款以及区域资料中心的扩张,共同推动了2024年云端运算采用率成长37%。新加坡的国家云端计画提供一系列预先已通过核准的机器学习即服务(MLaaS)额度,使营运商无需资本投入即可部署需求预测模型。越南和印尼的出口型製造商正在试验预测性维护仪表板,将感测器资料直接连接到云端託管的自动化机器学习(AutoML)引擎。随着中小企业越来越依赖云端服务供应商来实现可扩展性,MLaaS市场正在吸引数百万倾向于订阅模式的新兴高成长用户。

人工智慧模型知识产权纠纷

使用自身资料对基础模型进行微调的机构正面临着关于衍生重所有权的激烈争论。 OpenAI因训练资料权利问题被处以1500万欧元的GDPR罚款,这一事件已成为热门话题,促使风险管理部门要求籤订严格的授权合约。由于缺乏既定的法律先例,越来越多的专案部署被推迟或冻结,直到法务部门在合约条款中明确所有权、赔偿和特许权使用费等条款。Start-Ups担心,如果智慧财产权索赔威胁到后续收入,可能会失去创业融资。这种不确定性正在扭曲董事会层面的风险评估,并阻碍机器学习即服务(MLaaS)市场的成长。

细分市场分析

到2025年,模型训练和调优将占总收入的30.62%,这主要得益于企业加速将基础模型应用于专业资料集的趋势。这一趋势导致生产工作负载激增,使得可观测性至关重要。因此,机器学习运作和监控预计将以35.30%的最高复合年增长率成长,并在2031年之前巩固其在机器学习服务市场规模中的基础地位。整合工具链现已整合资料沿袭撷取、公平性指标和回滚触发器,以满足监管机构对持续检验的要求。

Start-Ups仍依赖低程式码开发工作室进行快速原型製作,但随着使用量的激增,它们正转向託管式机器学习维运服务 (MLOps)。随着边缘优化运行时支援低延迟的关键零售和行动应用,推理和配置收入稳步增长。受影片分析计划对多模态标註需求的推动,资料准备服务也维持成长动能。总体而言,服务组合表明,决定机器学习服务市场长期价值创造的关键在于管治和运作保证,而不是原始模型建构。

到2025年,诈欺侦测将占收入的26.95%,银行将从交易流程中提取异常模式。电脑视觉是下一个发展浪潮,其复合年增长率将达到36.85%,因为配备摄影机的预测性维护平台可以将非计划性停机时间减少高达70%。製造商正在对传统生产线进行改造,加装人工智慧摄影机,以便在毫秒内检测缺陷,从而实现每个工厂六位数的成本节约。零售商正在部署货架扫描机器人来减少缺货情况,医院正在采用跌倒侦测舱来提高病患安全。

行销部门正在将视觉API与生成模型结合,以实现广告创意的自动化生成,并利用视觉线索进行受众创新。通讯业者正在塔架上安装视觉感测器,用于结构健康检查,并将影像串流传输到云端推理丛集。视觉技术、物联网和机器学习即服务(MLaaS)的整合,正在为电脑视觉即服务(CVAaS)创造多元化的市场机会。

机器学习即服务 (MLaaS) 市场报告按服务类型(模型开发、资料准备、训练、推理、MLOps)、应用领域(行销、预测性维护、诈欺侦测、网路管理、电脑视觉)、组织规模(中小企业、大型企业)、最终用户(IT、银行、金融服务和保险 (BFSI)、医疗保健、汽车私人、零售、政府及其他)、部署混合云端和企业类型预测数据以美元计价。

区域分析

欧洲机器学习即服务 (MLaaS) 市场正取得显着进展,在政府和私营部门对人工智慧和机器学习技术的大规模投资推动下,2019 年至 2024 年的年均成长率约为 35%。德国、法国和英国等主要经济体强大的数位基础设施以及工业 4.0倡议的日益普及,都为这一增长提供了有力支撑。欧洲企业尤其关注在工业自动化、预测性维护和提升客户体验方面利用 MLaaS。该地区严格的资料保护条例,特别是《一般资料保护规则》(GDPR),正在推动安全合规的 MLaaS 解决方案的开发,并为资料隐私和安全设定了高标准。欧盟委员会的数位转型和人工智慧发展计画为 MLaaS 的应用创造了有利环境,各国多样化的人工智慧策略也进一步加速了市场成长。该地区对永续和合乎伦理的人工智慧发展的重视,也影响着 MLaaS 解决方案的演进,确保这些技术在各个领域得到负责任的应用。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 「即服务」型生成式人工智慧工具包的激增

- 加速新兴亚洲中小企业的云端迁移

- 基于人工智慧的威胁侦测可享网路保险折扣

- 超大规模资料中心业者提供的计量收费GPU定价

- 产业特定机器学习模型市场

- 国家人工智慧云端计画(例如欧盟的 Gaia-X)

- 市场限制

- 关于人工智慧模式智慧财产权所有权的争议

- 主权云端授权的兴起

- 揭露隐性碳成本

- 运行时数据偏差责任

- 产业价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按服务类型

- 模型开发平台

- 资料准备和标註

- 模型训练和调优

- 推理与配置

- MLOps 和监控

- 透过使用

- 行销与广告

- 预测性维护

- 诈欺侦测与风险分析

- 自动化网路管理

- 电脑视觉

- 按组织规模

- 中小企业

- 大公司

- 按最终用户行业划分

- 资讯科技和电信

- BFSI

- 医疗保健和生命科学

- 汽车与出行

- 零售与电子商务

- 政府和国防部

- 其他终端用户产业(能源、教育等)

- 透过部署模式

- 公共云端

- 私有云端

- 混合/多重云端

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 其他亚洲地区

- 中东

- 以色列

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Amazon Web Services, Inc.

- Microsoft Corporation

- Alphabet Inc.(Google Cloud)

- IBM Corporation

- Salesforce, Inc.

- Oracle Corporation

- SAP SE

- Hewlett Packard Enterprise Company

- Alibaba Cloud Computing Co., Ltd.

- Baidu, Inc.

- SAS Institute Inc.

- H2O.ai, Inc.

- DataRobot, Inc.

- BigML, Inc.

- FICO(Fair Isaac Corporation)

- Yottamine Analytics, LLC

- MonkeyLearn, Inc.

- C3.ai, Inc.

- Sift Science, Inc.

- Iflowsoft Solutions, Inc.

第七章 市场机会与未来展望

The Machine Learning As A Service Market was valued at USD 45.76 billion in 2025 and estimated to grow from USD 61.58 billion in 2026 to reach USD 271.88 billion by 2031, at a CAGR of 34.58% during the forecast period (2026-2031).

Rapid adoption of pay-per-use GPU instances, the democratization of generative AI toolkits, and sovereign-cloud programs that keep sensitive data inside national borders jointly accelerate demand. Enterprises also gravitate toward MLaaS to meet looming regulatory requirements on explainability and data residency while avoiding large capital outlays on on-premises infrastructure. Capital inflows from sovereign wealth funds in the Middle East and national AI strategies in Singapore, the EU, and China reinforce regional buildouts of compliant cloud zones. At the same time, insurers' premium rebates for AI-based threat detection and hyperscale's' competitive pricing further lower barriers for small and medium enterprises (SMEs).

Global Machine Learning As A Service (MLaaS) Market Trends and Insights

Surge in Gen-AI Toolkits Offered "As-a-Service

Foundation-model catalogues from leading clouds now ship with turnkey fine-tuning, orchestration, and vector-database connectors. Amazon's Nova suite integrates directly with Bedrock so enterprises can test multimodal prototypes in hours rather than quarters. Microsoft's partnership with xAI to host Grok 3 on Azure adds diversity to model choices and embeds bias-mitigation telemetry at the API layer. These innovations allow developers with limited ML backgrounds to embed text, image, and video reasoning into workflows. Lower skill requirements shorten proof-of-concept cycles, slash implementation costs, and boost the Machine Learning as a Service market's addressable base. Because the offerings ride on existing consumption-based billing, finance teams treat advanced AI as an operating expense.

Rapid SME Cloud Migration in Emerging Asia

Across ASEAN, 99% of firms qualify as SMEs, and government policy pushes them to digitize back-office and customer-experience functions. Subsidized broadband, fintech-enabled micro-lending, and regional data-centre expansions combine to lift cloud adoption by 37% in 2024. Singapore's national cloud program bundles pre-approved MLaaS credits, letting merchants deploy demand-forecasting models without capex. Export-oriented manufacturers in Vietnam and Indonesia are piloting predictive-maintenance dashboards that feed sensor data straight to cloud-hosted AutoML engines. As SMEs lean on cloud providers for scalability, the Machine Learning as a Service market gains millions of new, high-growth tenants that prefer subscription models.

AI-Model IP-Ownership Disputes

Organizations fine-tuning foundation models on proprietary data increasingly debate who owns derivative weights. The issue hit center stage when OpenAI drew a EUR 15 million GDPR penalty over training-data rights, spurring risk teams to demand watertight licenses. Without clear case law, legal teams slow or freeze deployments until contract clauses spell out ownership, indemnity, and royalty terms. Start-ups fear venture funding gaps if IP claims threaten downstream revenue. The uncertainty skews board-level risk assessments and subtracts points from the Machine Learning as a Service market growth trajectory.

Other drivers and restraints analyzed in the detailed report include:

- Cyber-Insurance Rebates for AI-Enabled Threat Detection

- Pay-Per-Use GPU Pricing by Hyperscale's

- Rising Sovereign-Cloud Mandates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Model Training and Tuning retained 30.62% of 2025 revenue as firms rushed to adapt foundation models to specialty datasets. That activity produced an explosion of production workloads, making observability indispensable. Consequently, MLOps and Monitoring are expected to log the highest 35.30% CAGR, reinforcing its role as the connective tissue of the Machine Learning as a Service market size through 2031. Integrated toolchains now bundle lineage capture, fairness metrics, and rollback triggers, answering regulators' calls for continuous validation.

Start-ups still lean on low-code development studios to prototype quickly, yet they pivot to managed MLOps once usage spikes. Inference and Deployment revenues grow steadily as edge-optimized runtimes enable latency-critical retail and mobility applications. Data Preparation services keep pace thanks to multimodal labelling demands from video-analytic projects. Overall, the service mix shows that governance and uptime assurance, not raw model building, now determine long-term value creation in the Machine Learning as a Service market.

Fraud Detection supplied 26.95% of 2025 sales as banks mined transaction streams for anomalous patterns. The next wave belongs to Computer Vision, which is tracking a 36.85% CAGR thanks to camera-fed predictive-maintenance platforms that cut unplanned downtime by up to 70%. Manufacturers retrofit legacy lines with AI cameras that flag defects in milliseconds, unlocking six-figure savings per plant. Retailers deploy shelf-scanning robots to curb stock-outs, while hospitals adopt fall-detection pods to boost patient safety.

Marketing teams increasingly pair vision APIs with generative models to auto-produce ad creatives and segment audiences by visual cues. Network operators attach vision sensors to towers for structural-integrity checks, streaming imagery into cloud inference clusters. This convergence of vision, IoT, and MLaaS propels a diversified addressable market for Computer-Vision-as-a-Service.

The MLaaS Market Report is Segmented by Service Type (Model Development, Data Preparation, Training, Inference, Mlops), Application (Marketing, Predictive Maintenance, Fraud Detection, Network Management, Computer Vision), Organization Size (SMEs, Large Enterprises), End-User (IT, BFSI, Healthcare, Automotive, Retail, Government, Others), Deployment (Public, Private, Hybrid Cloud), and Geography. Forecasts in Value (USD).

Geography Analysis

Europe has demonstrated remarkable progress in the machine learning as a service market, experiencing approximately 35% growth annually from 2019 to 2024, driven by significant governmental and private sector investments in AI and ML technologies. The region's growth is underpinned by strong digital infrastructure development and the increasing adoption of Industry 4.0 initiatives across major economies like Germany, France, and the United Kingdom. European organizations are particularly focused on leveraging MLaaS for industrial automation, predictive maintenance, and enhanced customer experiences. The region's stringent data protection regulations, particularly GDPR, have shaped the development of secure and compliant MLaaS solutions, setting high standards for data privacy and security. The European Commission's commitment to digital transformation and AI development has created a favorable environment for MLaaS adoption, while various national AI strategies have further accelerated market growth. The region's focus on sustainable and ethical AI development has also influenced the evolution of MLaaS solutions, ensuring responsible implementation of these technologies across various sectors.

- Amazon Web Services, Inc.

- Microsoft Corporation

- Alphabet Inc. (Google Cloud)

- IBM Corporation

- Salesforce, Inc.

- Oracle Corporation

- SAP SE

- Hewlett Packard Enterprise Company

- Alibaba Cloud Computing Co., Ltd.

- Baidu, Inc.

- SAS Institute Inc.

- H2O.ai, Inc.

- DataRobot, Inc.

- BigML, Inc.

- FICO (Fair Isaac Corporation)

- Yottamine Analytics, LLC

- MonkeyLearn, Inc.

- C3.ai, Inc.

- Sift Science, Inc.

- Iflowsoft Solutions, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Gen-AI toolkits offered "as-a-service"

- 4.2.2 Rapid SME cloud-migration in emerging Asia

- 4.2.3 Cyber-insurance rebates for AI-enabled threat-detection

- 4.2.4 Pay-per-use GPU pricing by hyperscalers

- 4.2.5 Vertical-specific ML model marketplaces

- 4.2.6 National AI-cloud programs (e.g., EU's Gaia-X)

- 4.3 Market Restraints

- 4.3.1 AI-model IP-ownership disputes

- 4.3.2 Rising sovereign-cloud mandates

- 4.3.3 Hidden carbon-cost disclosures

- 4.3.4 Run-time data-bias liabilities

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Model Development Platforms

- 5.1.2 Data Preparation and Annotation

- 5.1.3 Model Training and Tuning

- 5.1.4 Inference and Deployment

- 5.1.5 MLOps and Monitoring

- 5.2 By Application

- 5.2.1 Marketing and Advertising

- 5.2.2 Predictive Maintenance

- 5.2.3 Fraud Detection and Risk Analytics

- 5.2.4 Automated Network Management

- 5.2.5 Computer Vision

- 5.3 By Organization Size

- 5.3.1 Small and Medium-sized Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By End-User Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare and Life-Sciences

- 5.4.4 Automotive and Mobility

- 5.4.5 Retail and E-commerce

- 5.4.6 Government and Defense

- 5.4.7 Others End-User Industry (Energy, Education, etc.)

- 5.5 By Deployment Mode

- 5.5.1 Public Cloud

- 5.5.2 Private Cloud

- 5.5.3 Hybrid / Multi-Cloud

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia

- 5.6.4 Middle East

- 5.6.4.1 Israel

- 5.6.4.2 Saudi Arabia

- 5.6.4.3 United Arab Emirates

- 5.6.4.4 Turkey

- 5.6.4.5 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Egypt

- 5.6.5.3 Rest of Africa

- 5.6.6 South America

- 5.6.6.1 Brazil

- 5.6.6.2 Argentina

- 5.6.6.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amazon Web Services, Inc.

- 6.4.2 Microsoft Corporation

- 6.4.3 Alphabet Inc. (Google Cloud)

- 6.4.4 IBM Corporation

- 6.4.5 Salesforce, Inc.

- 6.4.6 Oracle Corporation

- 6.4.7 SAP SE

- 6.4.8 Hewlett Packard Enterprise Company

- 6.4.9 Alibaba Cloud Computing Co., Ltd.

- 6.4.10 Baidu, Inc.

- 6.4.11 SAS Institute Inc.

- 6.4.12 H2O.ai, Inc.

- 6.4.13 DataRobot, Inc.

- 6.4.14 BigML, Inc.

- 6.4.15 FICO (Fair Isaac Corporation)

- 6.4.16 Yottamine Analytics, LLC

- 6.4.17 MonkeyLearn, Inc.

- 6.4.18 C3.ai, Inc.

- 6.4.19 Sift Science, Inc.

- 6.4.20 Iflowsoft Solutions, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

全球机器学习服务市场规模、份额、趋势和成长分析报告(2026-2034)

全球机器学习服务市场规模、份额、趋势和成长分析报告(2026-2034) 全球云端人工智慧(AI)市场,2025-2029年

全球云端人工智慧(AI)市场,2025-2029年 全球云端通讯人工智慧市场,2025-2029年

全球云端通讯人工智慧市场,2025-2029年 机器学习即服务 (MaaS) 市场规模、份额和成长分析(按组件、组织规模、应用、最终用户和地区划分)—2026-2033 年行业预测

机器学习即服务 (MaaS) 市场规模、份额和成长分析(按组件、组织规模、应用、最终用户和地区划分)—2026-2033 年行业预测 机器学习即服务市场-全球产业规模、份额、趋势、机会和预测(按应用、组织规模、最终用户、地区和竞争格局划分,2020-2030 年预测)

机器学习即服务市场-全球产业规模、份额、趋势、机会和预测(按应用、组织规模、最终用户、地区和竞争格局划分,2020-2030 年预测) 2025年全球云端人工智慧(AI)解决方案市场报告2025年全球机器学习即服务(MLaaS)市场报告

2025年全球云端人工智慧(AI)解决方案市场报告2025年全球机器学习即服务(MLaaS)市场报告 2025-2029年全球云端客服中心解决方案人工智慧市场

2025-2029年全球云端客服中心解决方案人工智慧市场 2025-2029年全球人工智慧云端解决方案市场

2025-2029年全球人工智慧云端解决方案市场 云端电信 AI 市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

云端电信 AI 市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测