|

市场调查报告书

商品编码

1687109

电缆管理:市场占有率分析、产业趋势、统计数据、成长预测(2025-2030 年)Cable Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

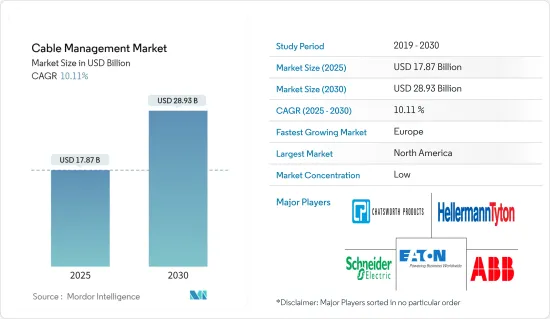

电缆管理市场规模预计在 2025 年为 178.7 亿美元,预计到 2030 年将达到 289.3 亿美元,预测期内(2025-2030 年)的复合年增长率为 10.11%。

关键亮点

- 推动电缆管理产品需求的主要趋势之一是 IT 领域的快速成长以及机构和企业对高效能资料通讯电缆的日益依赖。

- 据许多主要製造商称,对管道和其他系统的大部分需求是用于资料通讯。因此,製造商正在设计更新的产品和系统修改,这些产品和修改远远超出了这些系统的原始功能。

- 此外,电网、地下电网、可再生能源电网、太阳能发电厂和风力发电机对能够承受持续阳光、火焰和极端温度的缆线连接器和热缩材料的需求不断增长,预计将在整个预测期内支持市场成长。

- 此外,随着全球各行业向工业4.0迈进,通讯已成为支撑各领域发展的关键因素之一。与通讯、地下电缆管理、电缆密封和声学领域的其他常见产品一样,架空电缆管理系统由于其成本效益、供电和配电范围广,已成为最受欢迎的解决方案之一。

- 此外,原材料价格波动以及随着消费者和企业对更高性能电缆的需求增加,室内无线网路布线的安装和维护可能变得具有挑战性,这可能会阻碍成长。除此之外,许多现代办公室面临的一个常见问题是电缆管理不善和设计过时。海量资料和电力需求意味着需要大量的电缆和电线,使用电缆配线架和梯子等过时的方法来管理它们通常是不可能的。除了容量问题之外,平衡营运效率和空间美观度的问题也日益严重。

- 相反,电缆管理在创造视觉上令人愉悦和整洁的工作环境、维持基本功能以及保护设备免受因杂乱无章的电缆而造成的气流阻塞方面的重要性日益增加,为市场的增长创造了巨大的机会。

电缆管理市场趋势

IT和通讯领域可望推动市场成长

- 众所周知,电讯设备非常敏感,尤其是保持连接正常运作所需的网路和电缆。因此,用于管理和组织电缆的设备必须能够控制它们而不会造成损害。

- 电缆传输着我们所需的资料,照亮城市、实现云端运算并为数十亿台设备供电。因此,电缆管理对于有效控制满足商业和住宅客户需求以及 5G 等新兴技术所需的光纤部署至关重要。

- 此外,据Viavi Solutions称,到2022年5月,全球72个国家的约1947个城市将推出5G网路。中国最多,有356个城市,其次是美国,有296个,菲律宾有98个。

- 此外,根据印度电讯监管局 (TRAI) 的数据,截至 2022 年 9 月,Reliance Jio 是印度最大的参与企业,在印度拥有超过 4.19 亿通讯用户,使印度成为全球第二大通讯市场。根据 GSMA Intelligence 预测,到 2023 年初,印度的蜂巢行动连线将达到 11 亿。此外,到 2023 年 1 月,印度的行动连线将占其总人口的 77.0%。此外,据 Ericcsion 称,到 2029 年,该地区的行动电话用户总数预计将增长到 12.7 亿。

预计欧洲将实现强劲成长

- 随着电缆在各行业的应用越来越广泛,对电缆管理解决方案的需求也日益增加。该地区对有线网路和设施的需求正在大幅增长。此外,大容量网路的部署增加了各行业布线安装的复杂性。因此,对电缆管理的需求变得突出,从而推动了该地区的电缆管理市场的发展。

- 德国、法国等多个地区已开发国家正大力投资基础建设。随着各领域投资的激增,该公司也专注于维修和加强现有基础设施,以提供更好的营运支持,从而推动电缆管理市场的成长。

- 此外,随着能源需求的激增和电力基础设施的老化,该地区各国政府正在采取重大倡议,透过采用智慧电网解决方案来实现电网现代化。这种转变与新的电力分配和交通基础设施投资日益增长的趋势相吻合。

- 此外,IT和电讯市场是该地区成长最快的市场之一。由于该行业对高速连接的需求不断增加,大大小小的公司都主要致力于提供可靠的服务。对于电缆管理解决方案的需求也源自于为支援新服务而安装的新电缆。作为电缆管理的早期用户之一,该行业有望影响市场需求。

电缆管理行业概览

电缆管理市场竞争激烈且分散。市场参与企业包括 ABB 集团公司 Thomas & Betts、施耐德电机 SE、Cooper Industries (Eaton)、Chatsworth Products Inc. 和 HellermannTyton。认识到潜在的需求,这些领先的製造商正在向开发中国家扩张。

2023 年 12 月,Fischer Connectors 用于超高清 (UHD) 的新型高速连接器和电缆组件将在苛刻的环境中提供 18 Gb/s 的音讯/视讯资料传输,与 HDMI 2.0 的效能速度相符。这些新的 UHD 解决方案适用于旗舰 Fischer MiniMax 和 Fischer Core 产品线,具有 10,000 次配接次数、360° EMI 保护、从 IP68 到气密性和可灭菌性的密封性能以及三种锁定机制。

2023 年 1 月,Houdson Group 宣布与 Wibe Group 建立新的伙伴关係,为腐蚀性和危险环境提供电缆管理解决方案。此次合作将使 Wibe 电缆梯和 Mita 玻璃增强聚合物 (GRP) 密封产品透过Hudson Group 的新部门 Milton 在英国分销。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 市场影响

第五章市场动态

- 市场驱动因素

- 可再生能源商业化的需求

- 数位化和互联解决方案的采用日益增多

- 市场限制

- 原物料价格不稳定

第六章市场区隔

- 按产品

- 电缆配线架

- 电缆电气管槽

- 电缆管道

- 缆线连接器和密封接头

- 电缆托架

- 电缆接头

- 接线盒/分配盒

- 其他产品(扎线带、盖子、紧固件、夹子)

- 按最终用户产业

- 资讯科技/通讯

- 建造

- 能源公共产业

- 製造业

- 商业

- 其他的

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 世界其他地区(拉丁美洲、中东和非洲)

第七章竞争格局

- 公司简介

- ABB Ltd.

- Schneider Electric SE

- Cooper Industries(Eaton)

- Chatsworth Products Inc

- HellermannTyton

- Panduit Corporation

- Prsymian SP

- Legrand SA

- Leviton Manufacturing Co. Inc.

- Atkore International Holdings

- Enduro Composites SP(Creative Composites Group)

第八章投资分析

第九章:市场的未来

The Cable Management Market size is estimated at USD 17.87 billion in 2025, and is expected to reach USD 28.93 billion by 2030, at a CAGR of 10.11% during the forecast period (2025-2030).

Key Highlights

- One of the major trends driving the need for cable management products is the IT sector's rapid growth and the growing reliance of institutions and businesses on high-performance data & communication cabling.

- Many leading manufacturers report that most of their demands for raceways and other systems are for data & communication applications. As a result, manufacturers are designing newer products and system modifications, taking these systems well above their origins.

- Additionally, the growing need for cable connectors and heat shrinks in power networks, underground power networks, renewable energy networks, solar plants, and wind turbines are expected to support the market's growth throughout the forecast period, owing to their resistance to continuous sunlight, flames, and severe temperatures.

- Moreover, as industries around the globe are moving toward Industry 4.0, telecommunication has been turning out to be one of the key factors supporting every sector's development. Like other commonplace products in telecommunications, underground cable management, and cable sealing and acoustics, overhead cable management systems have been some of the most popular solutions for their cost-effectiveness, power supply, and distribution range.

- Moreover, the surge in high volatile raw material prices and cable installations for in-building wireless networks can be unmanageable to install and challenging to maintain as rising consumer and business demand for higher-performance cables might hamper the growth. In addition to this, common problems many modern offices have been facing are cable mismanagement and outdated design as oftentimes, with a significantly large number of cables and wires serving massive data and power needs, management has become untenable with antiquated methods such as cable trays or ladders. In addition to this capacity problem, there's also a rising issue of balancing operational efficiency with the aesthetics of a space.

- On the contrary, its rising importance in creating a visually pleasing and clean work environment, as well as the maintenance of basic functionality and protection of the devices from clogged airflow due to messy and disorganized cables, is creating significant opportunities for the studied market to grow.

Cable Management Market Trends

IT & Telecommunication segment is expected to promote market growth

- Telecom equipment is notoriously sensitive, especially the cables needed to maintain networks and connections properly. Owing to that reason, any equipment utilized to manage or organize those cables is required to be able to offer control without the risk of harm.

- Cables carry the data required to light cities, make cloud computing possible, and allow billions of devices to function. Hence, cable management is crucial to effectively control fiber rollouts, which are required to help the needs of business and residential customers, and the rollout of advanced technologies, such as 5G.

- In addition, according to Viavi Solutions, by May 2022, around 1947 cities across 72 countries had 5G networks available worldwide. China had the most cities with 356, followed by the USA with 296, and followed Philipinnes with 98 cities respectively.

- Furthermore, according to TRAI (Telecom Regulatory Authority of India), Reliance Jio was the top player in the country, with a wireless telecom subscriber base of over 419 million around India as of September 2022. and India was the second-largest telecom market worldwide. According to GSMA Intelligence, there were 1.10 billion cellular mobile connections in India at the start of 2023. It also indicates that mobile connections in India were equivalent to 77.0 percent of the total population in January 2023. Further, according to, Ericcsion, Total mobile subscriptions in the region are estimated to grow to 1.27 billion in 2029.

Europe is Expected to Witness Major Growth

- With the raised deployment of cables across multiple industries, the need for cable management solutions is also growing. The expanded demand for networks and facilities with the vast volume of cables has increased drastically in the region. Additionally, deploying high-capacity networks has led to complicated cable installations across different verticals. Thus, the requirement for the management of cables has gained prominence, promoting the region's cable management market.

- Multiple regional developed nations, such as Germany and France, are spending significantly on developing their infrastructure. With these surged investments in various sectors, enterprises also focus on renovating and enhancing their existing infrastructure to build better support for operations, which has been leading to growth in the cable management market.

- Moreover, with the surging energy demand and aging electricity infrastructure, governments across the region are largely moving toward modernizing energy grids by adopting smart grid solutions. Such transformations align with the rising propensity toward adopting new distribution and transportation infrastructure investments.

- Furthermore, one of the fastest-growing markets in the region is IT and telecom. Owing to the industry's rising demand for high-speed connectivity, various small and large businesses mainly concentrate on providing dependable services. The requirement for cable management solutions is also an outcome of the installation of new cables for supporting new services. One of the initial users of cable management, the industry is expected to influence market demand.

Cable Management Industry Overview

The cable management market is competitive and fragmented. ABB group company Thomas & Betts, Schneider Electric SE, Cooper Industries (Eaton), Chatsworth Products Inc., HellermannTyton, and others are some of the prominent participants in the market. After identifying potential needs, these top manufacturers have expanded into developing countries.

December 2023: Fischer Connectors' new high-speed connectors and cable assemblies for Ultra High Definition (UHD) provide audio/video data transfer at 18 Gb/s in demanding environments, matching the performance speed of HDMI 2.0. These new UHD solutions are available in the flagship Fischer MiniMax and Fischer Core product lines with 10,000 mating cycles, 360° EMI protection, different sealing performances from IP68 to hermeticity and sterilization capacities, and three locking mechanisms.

January 2023: The Houdson Group announced the form of a new partnership with Wibe Group to provide specialist cable management solutions for corrosive and hazardous environments. This collaboration is expected to see Wibe cable ladders and Mita Glass Reinforced Polymer (GRP) containment products distributed to the UK through 'Milton,' a new division of the Hudson Group.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Demand in Renewable Energy Commercialization

- 5.1.2 Growing Trend of Digitization and Adoption of Connected Solution

- 5.2 Market Restraints

- 5.2.1 Volatile Raw Material Prices

6 MARKET SEGMENTATION

- 6.1 By Product

- 6.1.1 Cable Trays

- 6.1.2 Cable Raceways

- 6.1.3 Cable Conduits

- 6.1.4 Cable Connectors and Glands

- 6.1.5 Cable Carriers

- 6.1.6 Cable Lugs

- 6.1.7 Junction/Distribution Boxes

- 6.1.8 Other Products (Ties, Covers, Fasteners, Clips)

- 6.2 By End-user Industry

- 6.2.1 IT and Telecommunication

- 6.2.2 Construction

- 6.2.3 Energy and Utility

- 6.2.4 Manufacturing

- 6.2.5 Commercial

- 6.2.6 Other End User Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Rest of the World (Latin America and Middle East and Africa)

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ABB Ltd.

- 7.1.2 Schneider Electric SE

- 7.1.3 Cooper Industries (Eaton)

- 7.1.4 Chatsworth Products Inc

- 7.1.5 HellermannTyton

- 7.1.6 Panduit Corporation

- 7.1.7 Prsymian SP

- 7.1.8 Legrand SA

- 7.1.9 Leviton Manufacturing Co. Inc.

- 7.1.10 Atkore International Holdings

- 7.1.11 Enduro Composites SP (Creative Composites Group)

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

垂直生命线电缆系统市场:依产品类型、材料、安装方式和最终用户产业划分,全球预测,2026-2032年电缆弯曲加固件市场按类型、材料、安装方式、应用和最终用户划分,全球预测(2026-2032)

垂直生命线电缆系统市场:依产品类型、材料、安装方式和最终用户产业划分,全球预测,2026-2032年电缆弯曲加固件市场按类型、材料、安装方式、应用和最终用户划分,全球预测(2026-2032) 全球电缆管理系统市场规模、份额、趋势和成长分析报告(2026-2034年)

全球电缆管理系统市场规模、份额、趋势和成长分析报告(2026-2034年) 日本电缆管理市场规模、份额、趋势和预测:按产品、材质、最终用户和地区划分,2026-2034年

日本电缆管理市场规模、份额、趋势和预测:按产品、材质、最终用户和地区划分,2026-2034年 2026年全球玻璃纤维增强塑胶(GRP)或纤维增强塑胶(FRP)电缆保护管市场报告梯形电缆桥架市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2026-2034)

2026年全球玻璃纤维增强塑胶(GRP)或纤维增强塑胶(FRP)电缆保护管市场报告梯形电缆桥架市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2026-2034) 线缆管理市场-全球产业规模、份额、趋势、机会及预测(依产品、线缆类型、材料、最终用户、地区及竞争格局划分,2021-2031年)无纸化系统市场:依部署模式、组件、应用、组织规模、技术类型、通路和最终用户产业划分,全球预测,2026-2032年资料中心线管理市场按产品类型、最终用户、安装类型和资料速率划分 - 全球预测 2026-2032 年

线缆管理市场-全球产业规模、份额、趋势、机会及预测(依产品、线缆类型、材料、最终用户、地区及竞争格局划分,2021-2031年)无纸化系统市场:依部署模式、组件、应用、组织规模、技术类型、通路和最终用户产业划分,全球预测,2026-2032年资料中心线管理市场按产品类型、最终用户、安装类型和资料速率划分 - 全球预测 2026-2032 年 电缆管理系统市场规模、份额和成长分析(按产品、材质、应用和地区划分)-2026-2033年产业预测

电缆管理系统市场规模、份额和成长分析(按产品、材质、应用和地区划分)-2026-2033年产业预测