|

市场调查报告书

商品编码

1687125

聚丙烯酰胺:市场占有率分析、产业趋势与成长预测(2025-2030)Polyacrylamide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

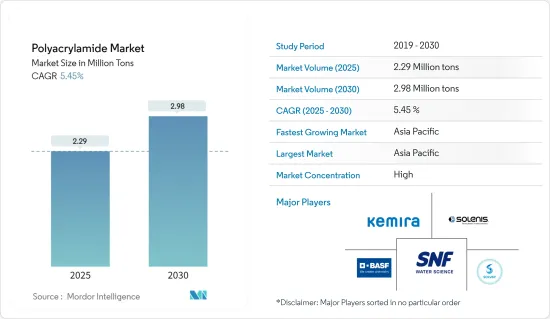

聚丙烯酰胺市场规模预计在 2025 年为 229 万吨,预计在 2030 年达到 298 万吨,预测期内(2025-2030 年)的复合年增长率为 5.45%。

2022年,全球新冠疫情迫使水处理、纸浆和造纸、石油和天然气以及采矿业停工,减少了对聚丙烯酰胺的需求。这场疫情几乎影响了这些产业的各个方面,从产品需求到劳动力发展,甚至加速或减缓了疫情爆发时已经出现的趋势。需求的减少对生产过程产生了重大影响,由于客户及其暂时停产,生产水准下降。不过,预计这种情况将会改善,市场预计将在预测期后半段恢復成长轨迹。

关键亮点

- 从中期来看,预计需求将受到石油和天然气行业对提高采收率的扩大使用以及水处理行业对聚丙烯酰胺作为凝聚剂的需求增加的推动。

- 预计接触丙烯酰胺单体引起的健康问题将阻碍市场成长。

- 聚丙烯酰胺在生物医药产业的新兴应用和生物基聚丙烯酰胺的开发有望为市场提供丰厚的机会。

- 亚太地区占据了最高的市场占有率,并可能在预测期内占据市场主导地位。

聚丙烯酰胺市场趋势

水处理产业占市场主导地位

- 聚丙烯酰胺是由丙烯酰胺聚合而成的一类水溶性高分子凝聚剂。该聚合物具有增加黏度和促进颗粒絮凝的能力,使其成为水和污水处理的理想选择。因此该聚合物可作为工业用水净化、废水净化、污水处理、污水处理中的凝聚剂。

- 它也可以用于饮用水产业,由于原水中含有胶体颗粒,钠元素不适合饮用,因此在使用前需要溶解和过滤。在这种情况下,聚丙烯酰胺可作为低分子量凝聚剂,去除水中多余的钠并使其适合饮用。

- 在用水和污水行业中使用聚丙烯酰胺可以最大限度地减少使用其他传统凝聚剂去除细菌、病毒、藻类和其他不必要的杂质,从而显着减少污泥量,使该过程更加经济且具有成本效益。

- 全球水消费量每20年增加100%。饮用水短缺的日益严重,加上人口的成长和用水需求的增加,推动了全球对膜污水处理市场的需求。目前,中国和美国是全球最大的两个水回收再利用市场。

- 2022年6月,专注于水环境治理的环保公司中国光大水务取得山东省淄博市张店东工业园区工业污水处理扩建改造计划。该计划将采用建设-运营-移交(BOT)模式运营,日处理工业污水能力约为5,000立方米。

- 美国环保署(EPA)宣布,将于2023年9月提供75亿美元的《水基础设施融资与创新法案》(WIFIA)资金。这项创新的低利率贷款计画旨在帮助社区投资饮用水、污水和雨水基础设施,同时节省数百万美元并创造高薪的当地就业机会。迄今为止,美国环保署的 WIFIA 计画已宣布拨款 190 亿美元,资助美国各地的 109 个计划。

- 德国的水处理技术市场是欧洲最大的市场,并且正在快速成长。活性化的水处理活动(主要在该国北部地区)正在推动对水处理化学品的需求。据联邦环境与自然保护部称,该国供水和污水处理行业每年的产值约为 220 亿欧元(233.3 亿美元)。

- 根据欧盟统计局和德国联邦统计局的数据,2022 年德国水、污水处理和废弃物管理产业的收益为 996.3 亿美元。

- 考虑到世界不同地区的成长趋势和各种水处理计划,水处理行业可能会主导市场,从而导致预测期内对聚丙烯酰胺的需求增加。

亚太地区占市场主导地位

- 2022 年,亚太地区在聚丙烯酰胺市场占据主导地位,占有相当大的份额,预计在预测期内仍将保持主导地位。

- 近年来,中国增加了处理水的使用量,以减少对淡水的依赖。随着中国五年计画(FYP)中水回用重要性的日益增强和法律规范的严格实施,中国正在迅速加强其水处理产业,以实现永续发展。

- 2023年9月,苏伊士集团订单一项水处理计划新订单,这将为中国2060年碳中和倡议做出贡献。该公司将与重庆水务集团(CWG)共同投资约1.68亿美元在中国重庆兴建和营运一座水处理厂。

- 在油气产业,中国最大油气生产商中国石油天然气集团公司控股的塔里木油田2022年油气产量创下3,310万吨的历史新高,预计2022年原油产量为736万吨,天然气产量为323亿立方公尺。

- 在印度,2023 年 7 月,IDE Treatment订单,为采矿业建造一座先进的污水处理厂 (WWTP)。该计划将于 2024 年由 IDE Technologies 向该公司供货,预计每天可处理 400 万公升盐水。

- 预计到 2025 年,印度的纸张需求量将达到每年 23.5 吨。一些造纸厂已经存在了几十年,需要升级和投资新机器。印度的人均纸张消费量仅13公斤多一点,远远落后于全球57公斤的平均值。预计到 2024 年,印度纸张和纸製品市场规模将达到 134 亿美元。

- 在采矿业,国营印度煤炭有限公司(CIL)已核准截至2022年1月的32个采矿计划,投资额达4,730亿印度卢比。

- 预计这些因素将在预测期内推动亚太地区聚丙烯酰胺市场的成长。

聚丙烯酰胺产业概况

聚丙烯酰胺市场高度整合,领先公司占据相当大的市场占有率。市场的主要企业(不分先后顺序)包括 SNF Group、 BASF SE、Kemira、Solenis 和 Solvay。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场驱动因素

- 扩大在石油和天然气产业中提高采收率的用途

- 水处理产业对聚丙烯酰胺作为凝聚剂的需求不断增加

- 市场限制

- 接触丙烯酰胺单体的健康问题

- 价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章市场区隔

- 依实体形态

- 粉末

- 液体

- 乳液/分散体

- 按应用

- 提高采收率

- 水处理凝聚剂

- 土壤改良剂

- 化妆品粘合剂和稳定剂

- 其他的

- 按最终用户产业

- 水处理

- 石油和天然气

- 纸浆和造纸

- 矿业

- 其他的

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 荷兰

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作与协议

- 市场排名分析

- 主要企业策略

- 公司简介

- AnHui JuCheng Fine Chemicals Co. Ltd

- Anhui Tianrun Chemical Industry Co. Ltd

- Ashland

- BASF SE

- Beijing Hengju Chemical Group Corporation

- Beijing Xitao Technology Development Co. Ltd

- CHINAFLOC

- Envitech Chemical Specialities Pvt.Ltd

- Kemira

- Liaocheng Yongxing Environmental Protection Science& Technology Co. Ltd

- Qingdao Oubo Chemical Co. Ltd

- Shandong Tongli Chemical Co. Ltd

- SNF Group

- Solenis

- Solvay

- Yixing Cleanwater Chemicals Co. Ltd

第七章 市场机会与未来趋势

- 聚丙烯酰胺的新应用领域,包括其作为生物材料的用途

- 生物基聚丙烯酰胺的开发

The Polyacrylamide Market size is estimated at 2.29 million tons in 2025, and is expected to reach 2.98 million tons by 2030, at a CAGR of 5.45% during the forecast period (2025-2030).

In 2022, the COVID-19 pandemic, on a global scale, forced water treatment, pulp and paper, oil and gas, and mining industries to shut down their operations, lowering the demand for polyacrylamide. The pandemic impacted almost every aspect of these industries, from product demand to workforce development to accelerating or decelerating trends already underway when it struck. Customers and their temporary production stops reduced production levels, and demand reductions significantly impacted production processes. However, the condition is expected to recover, restoring the growth trajectory of the market during the latter half of the forecast period.

Key Highlights

- In the medium term, the growing utilization in the oil and gas industry for enhanced oil recovery and the increasing need for polyacrylamide as a flocculant in the water treatment industry are expected to drive demand.

- Health concerns caused by exposure to acrylamide monomer is expected to hinder the market's growth.

- The emerging application of polyacrylamide in the biomedical industry and the development of bio-based polyacrylamide are expected to offer lucrative opportunities to the market.

- Asia-Pacific accounted for the highest market share, and the region will likely dominate the market during the forecast period.

Polyacrylamide Market Trends

Water Treatment Industry to Dominate the Market

- Polyacrylamide is a kind of polymer flocculant that is soluble in water and is produced using acrylamide polymerization. The polymer is deemed ideal for water and wastewater treatment because of its ability to increase viscosity and promote the flocculation of particles. Therefore, this polymer, as a flocculant, can be used for the purification of industrial water, drainage purification, sewage treatment, and wastewater treatment.

- It can also be utilized in the drinking water industry as well, where the presence of sodium in raw water due to colloidal particles makes it unfit for drinking, thereby needing to be dissolved and filtered before usage. Polyacrylamide, in this case, acts as a low molecular weight flocculant and removes the additional sodium from water, making it suitable for drinking purposes.

- The use of polyacrylamide in the water and wastewater industry minimizes the usage of other conventional flocculants for the removal of bacteria, viruses, algae, and other unwanted impurities, resulting in significantly less sludge and making the process more economical and cost-effective.

- The global water consumption rate is increasing by 100% every twenty years. The rising scarcity of potable water, coupled with the growing population and increasing water demand, is the major concern that is driving the demand for the membrane wastewater treatment market across the world. Currently, China and the United States represent the two largest water reclamation and reuse markets across the world.

- In June 2022, an environmental protection company that focuses on water environment management, named China Everbright Water, secured the expansion and upgrading project of the Zhangdian East Chemical Industry Park Industrial Wastewater Treatment in Zibo City, Shandong Province. This project will be operated on a BOT (Build-Operate-Transfer) model, with a designed daily industrial wastewater treatment capacity of around 5,000 m3.

- The United States Environmental Protection Agency (EPA) announced an investment of USD 7.5 billion in September 2023 in available Water Infrastructure Finance and Innovation Act (WIFIA) funding. This innovative low-interest loan program helps communities invest in drinking water, wastewater, and stormwater infrastructure while saving millions of dollars and creating good-paying local jobs. To date, EPA's WIFIA program has announced USD 19 billion to help finance 109 projects across the country.

- The German water treatment technology market is the largest in Europe and is growing considerably. The increasing water treatment activities, primarily in the country's Northern region, are boosting the demand for water treatment chemicals. The country's water supply and wastewater treatment sectors account for about EUR 22 billion (USD 23.33 billion) annually, as per the Federal Ministry for the Environment and Nature Conservation.

- According to the Eurostat and Statistisches Bundesamt, the revenue of Germany's water supply, sewerage, and waste management industry generated USD 99.63 billion in 2022.

- Considering the growth trends and various water treatment projects in different regions worldwide, the water treatment industry is likely to dominate the market, which, in turn, is expected to enhance the demand for polyacrylamide during the forecast period.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region dominated the polyacrylamide market in 2022 with a considerable volume share, and it is expected to maintain its dominance during the forecast period.

- In recent years, China has increased the use of treated water to reduce its dependency on fresh water. With a tough regulatory framework and the increasing importance of water reuse in China's five-year plans (FYPs), the country is rapidly moving toward enhancing its water treatment industry for a sustainable future.

- Suez Group bagged a new contract for a water treatment project in China in September 2023 to contribute to the country's 2060 carbon neutrality ambition. The company, in collaboration with Chongqing Water Group (CWG), is investing around USD 168 million for the construction and operation of a water treatment plant in Chongqing, China.

- In the oil and gas industry, The Tarim Oilfield, controlled by China National Petroleum Corporation (CNPC), China's largest oil and gas producer, saw its annual oil and gas production reach a record high of 33.1 million tons in 2022. The oilfield is estimated to have generated 7.36 million tons of crude oil and 32.3 billion cubic meters of natural gas in 2022.

- In India, in July 2023, IDE Technologies received a contract from CleanEdge Water Pte Ltd for the construction of a state-of-the-art wastewater treatment plant (WWTP) for mining industry applications. This project is expected to be supplied to the company by IDE Technologies in 2024 and is estimated to treat 4.0 million liters of challenging brine per day.

- The paper demand in India is expected to reach 23.5 metric tons per year by 2025. Some paper mills have existed for several decades, making upgrades and investments into newer machinery necessary. The per capita paper consumption in India, at a little over 13 kg, is way behind the global average of 57 kg. The market for paper and paper products in India is estimated to reach USD 13.4 billion by 2024.

- In the mining industry, state-run Coal India Ltd (CIL) has approved 32 mining projects till January 2022, with an investment of around INR 47,300 crore as the company seeks to replace imports and move toward its 1 billion tons of coal production target by 2023-2034.

- Factors like these are likely to fuel the growth of the polyacrylamide market in Asia-Pacific over the forecast period.

Polyacrylamide Industry Overview

The polyacrylamide market is highly consolidated, with the major players accounting for a major market share. Some of the major players in the market (not in any particular order) include SNF Group, BASF SE, Kemira, Solenis, and Solvay, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Growing Utilization in the Oil and Gas Industry for Enhanced Oil Recovery

- 4.1.2 Increasing Demand for Polyacrylamide as a Flocculant in Water Treatment Industry

- 4.2 Market Restraints

- 4.2.1 Health Concerns Caused by Exposure to Acrylamide Monomer

- 4.3 Industry Value Chain Analysis

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 By Physical Form

- 5.1.1 Powder

- 5.1.2 Liquid

- 5.1.3 Emulsion/Dispersions

- 5.2 By Application

- 5.2.1 Enhanced Oil Recovery

- 5.2.2 Flocculants for Water Treatment

- 5.2.3 Soil Conditioner

- 5.2.4 Binders and Stabilizers in Cosmetics

- 5.2.5 Other Applications

- 5.3 By End-user Industry

- 5.3.1 Water Treatment

- 5.3.2 Oil and Gas

- 5.3.3 Pulp and Paper

- 5.3.4 Mining

- 5.3.5 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Russia

- 5.4.3.5 Netherlands

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AnHui JuCheng Fine Chemicals Co. Ltd

- 6.4.2 Anhui Tianrun Chemical Industry Co. Ltd

- 6.4.3 Ashland

- 6.4.4 BASF SE

- 6.4.5 Beijing Hengju Chemical Group Corporation

- 6.4.6 Beijing Xitao Technology Development Co. Ltd

- 6.4.7 CHINAFLOC

- 6.4.8 Envitech Chemical Specialities Pvt.Ltd

- 6.4.9 Kemira

- 6.4.10 Liaocheng Yongxing Environmental Protection Science&Technology Co. Ltd

- 6.4.11 Qingdao Oubo Chemical Co. Ltd

- 6.4.12 Shandong Tongli Chemical Co. Ltd

- 6.4.13 SNF Group

- 6.4.14 Solenis

- 6.4.15 Solvay

- 6.4.16 Yixing Cleanwater Chemicals Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Applications of Polyacrylamide, such as its Use as a Biomaterial

- 7.2 Development of Bio-based Polyacrylamide

聚丙烯酰胺市场按应用、类型、分子量和形态划分-2025-2032年全球预测

聚丙烯酰胺市场按应用、类型、分子量和形态划分-2025-2032年全球预测 湿强树脂的全球市场:各类型树脂,各用途 - 产业动态,市场规模,机会分析,预测(2025年~2033年)

湿强树脂的全球市场:各类型树脂,各用途 - 产业动态,市场规模,机会分析,预测(2025年~2033年) 2025年全球聚丙烯酰胺市场报告

2025年全球聚丙烯酰胺市场报告 聚丙烯酰胺市场规模(按类型、应用、地区、范围和预测)

聚丙烯酰胺市场规模(按类型、应用、地区、范围和预测) 全球聚丙烯酰胺市场(2025年)

全球聚丙烯酰胺市场(2025年) 聚丙烯酰胺(PAM)全球市场需求、预测分析(2018-2034)

聚丙烯酰胺(PAM)全球市场需求、预测分析(2018-2034) 聚丙烯酰胺市场:全球2025-2029湿纸市场按产品类型、黏合剂类型、製造流程、应用类型、产品形式、分销管道和最终用户划分 - 2025-2030 年全球预测聚丙烯酰胺市场报告:2030 年趋势、预测与竞争分析

聚丙烯酰胺市场:全球2025-2029湿纸市场按产品类型、黏合剂类型、製造流程、应用类型、产品形式、分销管道和最终用户划分 - 2025-2030 年全球预测聚丙烯酰胺市场报告:2030 年趋势、预测与竞争分析 全球聚丙烯酰胺 (PAM) 市场:工厂产能、产量、利用率、供需、最终用户行业、销售渠道、区域需求、公司份额 (2015-2032)

全球聚丙烯酰胺 (PAM) 市场:工厂产能、产量、利用率、供需、最终用户行业、销售渠道、区域需求、公司份额 (2015-2032)