|

市场调查报告书

商品编码

1687127

建筑复合材料:市场占有率分析、产业趋势与成长预测(2025-2030)Construction Composite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

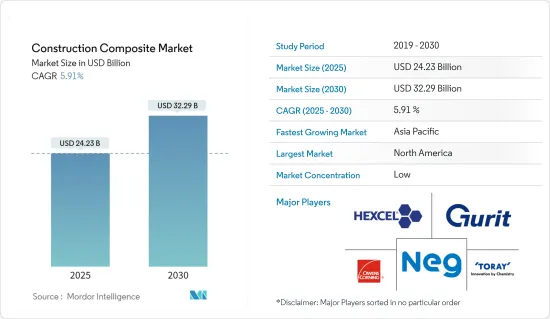

预计 2025 年建筑复合材料市场规模为 242.3 亿美元,到 2030 年将达到 322.9 亿美元,预测期内(2025-2030 年)的复合年增长率为 5.91%。

2020 年,COVID-19 对市场产生了负面影响,因为这场疫情严重影响了国际贸易,并扰乱了製造业、建筑业和施工业等多个行业。然而,2021年这些产业的市场需求强劲復苏。

关键亮点

- 从中期来看,复合材料在建筑应用中的使用不断增加以及破旧水泥建筑物的修復正在推动市场成长。

- 然而,复合材料的初始生产和安装成本高,加上技术纯熟劳工的短缺,阻碍了市场的成长。

- 建筑领域复合材料大规模生产能力的提高可能在未来几年为市场创造机会。

- 就收益而言,北美预计将占据市场主导地位,而亚太地区预计将在预测期内以最高的复合年增长率成长。

建筑复合材料的市场趋势

土木工程和建筑领域占据市场主导地位

- 土木工程包括桥樑、水坝、道路、机场、运河、铁路基础设施和相关结构的建设。

- 2021年底,中国多个省份宣布了大型基础设施计划。中国南方的广西壮族自治区宣布了一系列重大建设计划,总投资达 1,859 亿元人民币(291.5 亿美元)。这些计划涉及交通运输、新能源、物流、基础设施等多个领域。

- 作为促进都市化和地方经济发展的长期计划的一部分,中国还计划在未来15年内将其世界第二大铁路网络扩大三分之一。根据中国中铁股份有限公司发布的规划,中国计划在2035年底铺设铁路约20万公里,其中包括约7万公里高铁。

- 德国交通运输和数位基础设施部计画投资3.4872亿美元用于电动车出行、电动车充电基础设施的自动化和连网运作等未来技术。连接施瓦尔姆施塔特 (Schwalmstadt) 与黑森州中部 Ohmtal 立交桥的 A49 高速公路计划也已开工。预计这将导致复合材料消费量的增加。

- 施瓦尔姆施塔特-奥姆塔尔计划采用官民合作关係模式,投资金额为8.1368亿美元。该工程包括 93 公里的道路,计划于 2024 年第三季完工。这些大型铁路和公路建设计划可能会在预测期内推动对建筑复合材料的需求。

- 根据美国人口普查局的数据,2021年美国公路和道路建设的年价值为1.0068亿美元,而2020年为1.0232亿美元。

- 在加拿大,作为「投资加拿大」计画的一部分,政府宣布计画在2028年在该国主要基础建设上投资约1,400亿美元。

北美占据市场主导地位

- 在北美,由于美国、加拿大和墨西哥等国家建筑业的成长,复合材料在建筑中的使用正在增加。

- 北美是建筑复合材料最大的消费市场之一。美国是世界上最大的建筑业国家之一。 2021年全年建筑支出达15,903.7亿美元,较2020年的1,4692亿美元成长8.2%。

- 根据美国人口普查局的数据,2022年2月美国建筑支出经季节性已调整的成年率估计为1704亿美元,比1月修订后的1.6955万亿美元高出0.5%。此外,2022 年 2 月的估计值比 2021 年 2 月的 15,333 亿美元估计值高出 11.2%。 2022年1-2月建筑支出为2,378亿美元,较2021年同期的2,154亿美元成长10.4%。

- 加拿大的住宅和商业领域近期经历了稳定成长。加拿大(特别是多伦多)最近正经历高层建筑建设的热潮。预计到 2025 年,多伦多将有 30 多栋高层建筑竣工,另有 50 座高层建筑处于提案或规划阶段。

- 此外,作为「投资加拿大」计画的一部分,加拿大政府宣布计画在2028年全国投资近1,400亿美元用于基础建设。

建筑复合材料产业概况

全球建筑复合材料市场是细分的。市场的主要企业(不分先后顺序)包括 Hexcel Corporation、Owens Corning、Nippon Electric Glass、Toray Industries Inc. 和 Gurit。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 复合材料在建筑应用上的使用日益增多

- 破旧水泥建筑物修復

- 限制因素

- 复合材料的初始製造和安装成本高

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔

- 树脂类型

- 聚酯树脂

- 乙烯基酯

- 聚乙烯

- 聚丙烯

- 环氧树脂

- 其他的

- 光纤类型

- 碳纤维

- 玻璃纤维

- 天然纤维

- 其他纤维类型

- 最终用途部分

- 工业的

- 商业

- 住宅

- 私人的

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚国协

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 西班牙

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作与协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介(概况、财务状况、产品与服务、最新发展)

- Aegion Corporation

- Exel Composites

- Gurit

- Hexcel Corporation

- Kordsa Teknik Tekstil AS

- Toray Industries Inc.

- Mitsubishi Chemical Corporation

- Nippon Electric Glass Co. Ltd

- Owens Corning

- SGL Carbon

- Teijin Limited

第七章 市场机会与未来趋势

- 提升建筑领域复合材料的量产能力

The Construction Composite Market size is estimated at USD 24.23 billion in 2025, and is expected to reach USD 32.29 billion by 2030, at a CAGR of 5.91% during the forecast period (2025-2030).

COVID-19 negatively impacted the market in 2020 as the pandemic severely affected international trade and hampered several industries, including manufacturing, building, and construction. However, in 2021, the market demand from these sectors recovered significantly.

Key Highlights

- Over the medium term, the factors driving the growth of the market studied are the increasing usage of composites in construction applications and the rehabilitation of old concrete structures.

- On the other hand, the high initial production and installation costs of composites, coupled with the inadequacy of skilled labor, are hindering the market's growth.

- Increasing the ability to mass-produce composites in the construction sector will likely create opportunities for the market in the coming years.

- North America is expected to dominate the market in terms of revenue while the Asia-Pacific region is likely to witness the highest CAGR during the forecast period.

Construction Composites Market Trends

Civil Construction Sector to Dominate the Market

- Civil construction comprises the construction of bridges, dams, roads, airports, canals, railway infrastructure, and related structures.

- Toward the end of 2021, several Chinese provinces announced major infrastructure projects. South China's Guangxi Zhuang Autonomous Region unveiled a batch of major construction projects, with a total investment of CNY 185.9 billion (USD 29.15 billion). Those projects cover many sectors, including transportation, new energy, logistics, and basic infrastructure.

- Furthermore, China plans to expand its railway network, which is the second-largest in the world, by one-third in the next 15 years, as part of a long-term plan to propel urbanization and stimulate local economies. According to a plan issued by the state-owned China State Railway Group, China aims to have about 200,000 km (124,274 miles) of railway tracks by the end of 2035, including about 70,000 km of high-speed railways.

- In Germany, the Ministry of Transport and Digital Infrastructure plans to invest USD 348.72 million in future technologies, such as electric mobility or automated and networked driving for electric vehicle charging infrastructure. Also, the country has started working on the A49 highway project connecting Schwalmstadt and the Ohmtal interchange in Central Hesse. This, in turn, is expected to increase the consumption of composite materials.

- The Schwalmstadt-Ohmtal project is based on a public-private partnership model with an investment of USD 813.68 million. The construction, which comprises 93 km of road, is expected to be completed in the third quarter of 2024. These massive railway and road construction projects may drive the demand for construction composites during the forecast period.

- According to US Census Bureau, annual value of highway and street construction put in place of United states, in 2021 accounted for USD 100.68 million, compared to USD 102.32 million in 2020.

- In Canada, as part of the "Investing in Canada" plan, the government announced plans to invest nearly USD 140 billion in major infrastructure developments in the country by 2028.

North America Region to Dominate the Market

- In North America, the utilization of construction composites is increasing due to the growing construction sector in countries such as the United States, Canada, and Mexico.

- The North American region is one of the largest consumption markets for construction composites. The United States has one of the world's largest construction industries. In the full year 2021, construction spending amounted to USD 1,590.37 billion, 8.2% above USD 1,469.2 billion in 2020, thereby increasing the consumption of construction composites from various construction applications.

- According to the US Census Bureau, during February 2022, the construction spending in the country was estimated at a seasonally adjusted annual rate of USD 1704.4 billion, 0.5% more than the revised January estimate of USD 1,695.5 billion. Moreover, the February 2022 estimation is 11.2% more than the February 2021 estimate of USD 1,533.3 billion. During the first two months of 2022, construction spending amounted to USD 237.8 billion, 10.4% percent above USD 215.4 billion for the same period in 2021.

- In Canada, the residential and commercial sectors have been witnessing steady growth in the recent past. There has been a boom in the construction of skyscrapers in Canada (more specifically in Toronto) in recent times. Over 30 high-rise buildings are expected to be completed by 2025, and another 50 such buildings are in the proposal and planning phases in Toronto.

- Moreover, as part of the ''Investing in Canada Plan'', the government has announced plans to invest nearly USD 140 billion in infrastructure developments in the country by 2028.

Construction Composites Industry Overview

The global construction composite market is fragmented. Some major players in the market (in no particular order) include Hexcel Corporation, Owens Corning and Nippon Electric Glass Co. Ltd., Toray Industries Inc., and Gurit.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Use of Composites in Construction Applications

- 4.1.2 Rehabilitation of Old Concrete Structures

- 4.2 Restraints

- 4.2.1 High Initial Production and Installation Costs of Composites

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Revenue)

- 5.1 Resin Type

- 5.1.1 Polyester Resin

- 5.1.2 Vinyl Ester

- 5.1.3 Polyethylene

- 5.1.4 Polypropylene

- 5.1.5 Epoxy Resin

- 5.1.6 Other Resin Types

- 5.2 Fiber Type

- 5.2.1 Carbon Fibers

- 5.2.2 Glass Fibers

- 5.2.3 Natural Fibers

- 5.2.4 Other Fiber Types

- 5.3 End-use Sector

- 5.3.1 Industrial

- 5.3.2 Commercial

- 5.3.3 Housing

- 5.3.4 Civil

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) ** / Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles (Overview, Financials, Products and Services, and Recent Developments)

- 6.4.1 Aegion Corporation

- 6.4.2 Exel Composites

- 6.4.3 Gurit

- 6.4.4 Hexcel Corporation

- 6.4.5 Kordsa Teknik Tekstil AS

- 6.4.6 Toray Industries Inc.

- 6.4.7 Mitsubishi Chemical Corporation

- 6.4.8 Nippon Electric Glass Co. Ltd

- 6.4.9 Owens Corning

- 6.4.10 SGL Carbon

- 6.4.11 Teijin Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Ability to Mass Produce Composites in the Construction Sector

建筑复合材料市场:依材料、製造流程、树脂、形状和应用划分-2026年至2032年全球预测

建筑复合材料市场:依材料、製造流程、树脂、形状和应用划分-2026年至2032年全球预测 全球建筑用复合材料市场:规模、份额、趋势和成长分析报告(2026-2034)

全球建筑用复合材料市场:规模、份额、趋势和成长分析报告(2026-2034) 建筑复合材料市场-全球产业规模、份额、趋势、机会与预测:按树脂类型、纤维类型、应用、地区和竞争格局划分,2021-2031年树脂黏合骨材市场(按骨材类型、树脂类型、铺放类型、骨材尺寸、应用和分销管道)—2025-2030 年全球预测

建筑复合材料市场-全球产业规模、份额、趋势、机会与预测:按树脂类型、纤维类型、应用、地区和竞争格局划分,2021-2031年树脂黏合骨材市场(按骨材类型、树脂类型、铺放类型、骨材尺寸、应用和分销管道)—2025-2030 年全球预测 建筑复合材料市场按纤维类型(碳纤维、玻璃纤维等)、树脂类型(热塑性、热固性)、最终用途(工业、商业、住宅)和地区划分,2025 年至 2033 年

建筑复合材料市场按纤维类型(碳纤维、玻璃纤维等)、树脂类型(热塑性、热固性)、最终用途(工业、商业、住宅)和地区划分,2025 年至 2033 年 建筑复合材料市场:依树脂种类、纤维类型、最终使用领域及地区划分

建筑复合材料市场:依树脂种类、纤维类型、最终使用领域及地区划分![北美建筑用复合材料市场:趋势、机会与竞争分析 [2024-2030]](/sample/img/cover/42/default_cover_5.png) 北美建筑用复合材料市场:趋势、机会与竞争分析 [2024-2030]欧洲建筑市场的复合材料:市场规模、趋势与成长分析[2024-2030]全球建筑市场复合材料:趋势、机会与竞争分析[2024-2030]

北美建筑用复合材料市场:趋势、机会与竞争分析 [2024-2030]欧洲建筑市场的复合材料:市场规模、趋势与成长分析[2024-2030]全球建筑市场复合材料:趋势、机会与竞争分析[2024-2030]