|

市场调查报告书

商品编码

1687175

三元乙丙橡胶(EPDM):市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Ethylene Propylene Diene Monomer (EPDM) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

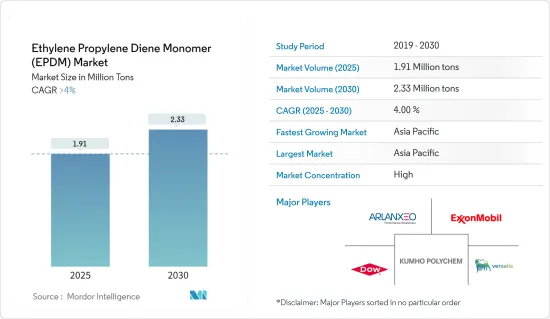

预计 2025 年三元乙丙橡胶(EPDM) 市场规模为 191 万吨,到 2030 年将达到 233 万吨,预测期内(2025-2030 年)的复合年增长率将超过 4%。

2020 年,新冠疫情对市场产生了负面影响。不过,目前估计市场已恢復到疫情前的水准。

主要亮点

- 从中期来看,建设产业的需求增加和电动车市场的成长是市场成长的主要驱动力。

- 由于 EPDM 使用石油衍生原料,油价波动可能会抑制市场成长。

- 生物基 EPDM 的出现可以为所研究的市场带来机会。

- 亚太地区占据市场主导地位,预计在预测期内将继续占据主导地位。

三元乙丙橡胶(EPDM) 市场趋势

汽车领域占据市场主导地位

- 三元乙丙橡胶橡胶(EPDM)是丙烯、乙烯和少量非共轭二烯单体的共聚物。它在汽车工业中有着广泛的应用,包括挡风雨条、玻璃和窗户密封系统、软管、管材、轮胎和皮带。

- 挡风雨条或密封条是一种密封任何开口的系统。它们是柔性的或半刚性的,可以吸收车辆运动引起的振动。

- 挡风雨条用于透过转移或返回水来部分或完全防止来自外部的水或雨的渗入。它还可以防止空气从车内流向车外。这有助于节省暖气、通风和空调 (HVAC) 的能源。

- 汽车上的每个车门至少需要 20 英尺的材料,每个窗户至少需要 10 英尺的材料。根据汽车的大小,汽车后车箱也需要大量的材料。这表明汽车对用于挡风雨条和密封应用的橡胶的需求。

- EPDM 的耐磨性、耐切割性、抗撕裂性和抗拉强度使其成为大多数应用的首选。 EPDM橡胶用于几乎所有机动车辆的密封条和密封应用,包括乘用车、轻型商用车、巴士、长途客车和重型卡车,其中轻型商用车占密封条和密封应用的大部分。

- 根据OICA的数据,2021年全球整体汽车销售(所有类型)为8,268万辆,总产量为8,014万辆。

- 2021年美国汽车产量为156万辆,商用车产量为760万辆,成长4%。

- 因此,鑑于上述情况,预计汽车产业将占据市场主导地位。

亚太地区占市场主导地位

- 亚太地区占据市场主导地位,并且很可能在预测期内继续占据主导地位。亚太地区是全球汽车和建筑业的中心,也是推动 EPDM 需求的主要地区。

- 中国是世界上最大的汽车製造业国家。 2021年商用车及汽车产量成长3%至2608万辆。

- 中国消费性电子产品收益预计将以每年2.04%的速度成长,到2025年市场规模将达到1,756.7亿美元。

- 建筑业是印度第二大产业,对GDP的贡献率约9%。预计预测期结束时印度建筑业价值将达到近 1 兆美元,成为全球第三大市场。

- 日本的电气电子产业是世界领先的产业之一。 2021年,受电子零件及设备出口强劲,以及生活方式改变带动通讯基础设施设备成长的推动,日本电子产业国内产值与前一年同期比较增11%,达到10.9322兆日圆(约997.5亿美元)。

- 预计所有上述因素都将在预测期内对市场产生重大影响。

三元乙丙橡胶(EPDM) 产业概览

三元乙丙橡胶(EPDM) 市场趋于整合,五大主要企业占相当大的份额。主要企业(不分先后顺序)包括陶氏化学、阿朗新科、埃克森美孚、Versalis SpA 和锦湖 POLYCHEMM。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 建设产业需求不断增长

- 电动车市场正在成长

- 限制因素

- 原油价格波动

- 其他限制因素

- 产业价值链分析

- 波特五力模型

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场区隔

- 製造过程

- 溶液聚合工艺

- 泥浆/悬浮液工艺

- 气相聚合工艺

- 应用

- 车

- 建筑和施工

- 製造业

- 电气和电子

- 其他用途

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作、协议

- 市场占有率(%)分析

- 主要企业策略

- 公司简介

- ARLANXEO

- Dow

- Elevate

- Exxon Mobil Corporation.

- ENEOS Materials Corporation

- Jilin Xingyun Chemical Co.,Ltd.

- Johns Manville

- KUMHO POLYCHEM

- Lion Elastomers

- Mitsui Chemicals, Inc.

- PetroChina Company Limited

- SK Global Co., Ltd.

- Versalis SpA

第七章 市场机会与未来趋势

- 生物基 EPDM 的出现

The Ethylene Propylene Diene Monomer Market size is estimated at 1.91 million tons in 2025, and is expected to reach 2.33 million tons by 2030, at a CAGR of greater than 4% during the forecast period (2025-2030).

The COVID-19 pandemic had a negative impact on the market in 2020. However, the market has now been estimated to have reached pre-pandemic levels.

Key Highlights

- Over the medium term, the major factor driving the growth of the market studied is the growing demand from the construction industry and the growth in the electric vehicles market.

- Since EPDM is derived from petroleum-based raw materials, the fluctuations in oil prices can restrain the market studied.

- The emergence of bio-based EPDM can be seen as an opportunity for the market studied.

- Asia-Pacific dominated the market and is expected to continue its dominance during the forecast period.

Ethylene Propylene Diene Monomer Market Trends

Automotive Segment to Dominate the Market

- Ethylene propylene diene monomer (EPDM) rubber is a copolymer of propylene, ethylene, and a small amount of non-conjugated diene monomers used in the automotive industry for various applications as weatherstripping, sealing systems for glass and windows, hose, and tubing, tires, and belts amongst others.

- Weatherstripping or weather seals is a system that seals any openings. They are flexible or semi-rigid and can take vibrations caused by vehicle movement.

- Weatherstripping is used to prevent the entry of water and rain partially or completely into the automobile from outside by either rerouting or returning the water. Also, it prevents the movement of air from the automotive interior to the outside and vice versa. This helps in saving energy on heating, ventilation, and air conditioning (HVAC).

- Each door in the automobile will need at least 20 feet of material, and every window requires a minimum of 10 feet of material. The trunk of the automobile may also require much larger amounts of material depending on the size of the automobile. It indicates the demand for rubber in the automobile for weather stripping and sealing applications.

- EPDM's resistance to abrasion, cutting, tearing, and tensile strength, EPDM is preferred in most applications. EPDM rubber is used for weather strip and sealing applications in almost all automobiles, such as passenger cars, lightweight commercial vehicles, busses, coaches, and heavy trucks, of which light commercial vehicles dominate the weather strip and sealing application.

- Globally, according to OICA, the sales of vehicles (all types) in the year 2021 were 82.68 million units, and the total production was 80.14 million units.

- The total production of cars in the United States in 2021 was 1.56 million units, and that of commercial vehicles was 7.60 million units registering an increase of 4%.

- Hence, owing to the above-mentioned aspects, the automotive segment is expected to dominate the market.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific dominated the market with a share and is likely to continue its dominance during the forecast period. Asia-Pacific is a hub for automotive and construction industries globally and is the major region driving the demand for EPDM.

- The Chinese automotive manufacturing industry is the largest in the world. The country observed a growth of 3% in the production of commercial vehicles and cars in the year 2021, with a total production of 26.08 million vehicles.

- China's revenue from consumer electronics is expected to show an annual growth rate of 2.04%, resulting in a projected market volume of USD 175,670 million by 2025.

- The construction industry is the second-largest industry in India, with a GDP contribution of about 9%. It is predicted that the Indian construction industry is expected to emerge as the third-largest market in the world, with a size of almost USD 1 trillion by the end of the forecast period.

- The Japanese electrical and electronics industry is one of the world's leading industries. In 2021, domestic production by the Japanese electronics industry surged by 11% year-on-year to JPY 10,932.2 billion (~ USD 99.75 billion) due to the strong export performance of electronic components and devices and the growth in telecommunications infrastructure equipment due to lifestyle changes.

- All the aforementioned factors, in turn, are projected to have a significant impact on the market during the forecast period.

Ethylene Propylene Diene Monomer Industry Overview

The ethylene propylene diene monomer (EPDM) market is consolidated, with the top five players accounting for a significant share. The key players (not in any particular order) include Dow, ARLANXEO., Exxon Mobil Corporation., Versalis S.p.A, and KUMHO POLYCHEM.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from the Construction Industry

- 4.1.2 Growth in the Electric Vehicles Market

- 4.2 Restraints

- 4.2.1 Fluctuations in the Oil Prices

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter Five Forces

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Manufacturing Process

- 5.1.1 Solution Polymerization Process

- 5.1.2 Slurry/Suspension Process

- 5.1.3 Gas-phase Polymerization Process

- 5.2 Application

- 5.2.1 Automotive

- 5.2.2 Building and Construction

- 5.2.3 Manufacturing

- 5.2.4 Electrical and Electronics

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ARLANXEO

- 6.4.2 Dow

- 6.4.3 Elevate

- 6.4.4 Exxon Mobil Corporation.

- 6.4.5 ENEOS Materials Corporation

- 6.4.6 Jilin Xingyun Chemical Co.,Ltd.

- 6.4.7 Johns Manville

- 6.4.8 KUMHO POLYCHEM

- 6.4.9 Lion Elastomers

- 6.4.10 Mitsui Chemicals, Inc.

- 6.4.11 PetroChina Company Limited

- 6.4.12 SK Global Co., Ltd.

- 6.4.13 Versalis S.p.A

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emergence of Bio-based EPDM

三元乙丙橡胶(EPDM)全球市场、产能、需求、平均价格及产业展望(至2034年)

三元乙丙橡胶(EPDM)全球市场、产能、需求、平均价格及产业展望(至2034年) 用于AR/MR的高屈光晶片:全球市场份额和排名、总收入和需求预测(2025-2031年)乙丙橡胶(EPDM):全球市场份额和排名、总收入和需求预测(2025-2031年)

用于AR/MR的高屈光晶片:全球市场份额和排名、总收入和需求预测(2025-2031年)乙丙橡胶(EPDM):全球市场份额和排名、总收入和需求预测(2025-2031年) 三元乙丙橡胶市场(按类型、製造流程、形式、最终用户、应用和销售管道)——全球预测 2025-2032

三元乙丙橡胶市场(按类型、製造流程、形式、最终用户、应用和销售管道)——全球预测 2025-2032 2025年三元乙丙橡胶全球市场报告

2025年三元乙丙橡胶全球市场报告 2025-2029年全球乙烯、丙烯及二烯单体市场

2025-2029年全球乙烯、丙烯及二烯单体市场 三元乙丙橡胶市场规模、份额、趋势分析报告:依产品、应用、地区、细分市场预测,2025-2030 年

三元乙丙橡胶市场规模、份额、趋势分析报告:依产品、应用、地区、细分市场预测,2025-2030 年 2025-2033年乙丙二烯单体市场报告(依製造流程、销售通路、应用及地区)

2025-2033年乙丙二烯单体市场报告(依製造流程、销售通路、应用及地区) 丙烯酸寡聚物市场报告:趋势、预测和竞争分析(至 2031 年)

丙烯酸寡聚物市场报告:趋势、预测和竞争分析(至 2031 年) 全球液态 EPDM 市场 -市场占有率与排名、总销售额、需求预测(2025-2031 年)

全球液态 EPDM 市场 -市场占有率与排名、总销售额、需求预测(2025-2031 年)