|

市场调查报告书

商品编码

1687190

拉丁美洲泡壳包装:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Latin America Blister Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

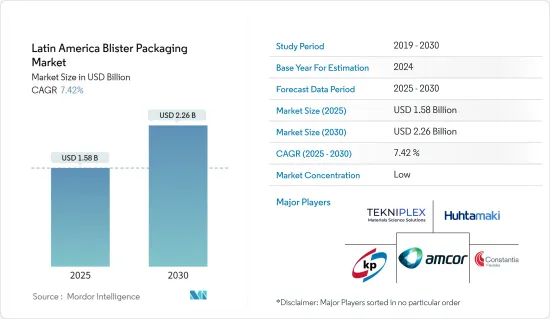

预计 2025 年拉丁美洲泡壳包装市场规模为 15.8 亿美元,到 2030 年将达到 22.6 亿美元,预测期内(2025-2030 年)的复合年增长率为 7.42%。

主要亮点

- 製药业是泡壳包装的最大终端用户,占有相当大的市场占有率。如此高的份额是因为泡壳包装在製药行业中具有许多优势,例如提高产品保护、易于分销、单位剂量包装和产品识别。

- 泡壳包装的创新,例如透过外包装密封部署的无线射频识别(RFID)标籤,因其有可能在整个供应链中提供个人化的安全性而变得越来越受欢迎。泡壳包装可保护小型医疗设备和药品免受氧气、异味和湿气的影响,并延长其保质期。服药依从性差是一个普遍存在的问题,会导致慢性疾病併发症和医疗成本增加。在预测期内,泡壳包装方法可能会得到更广泛的推荐,以解决药物依从性问题。

- 泡壳包装现在采用了更多的奈米技术。奈米技术提高了屏障保护能力并使包装更轻。拉丁美洲的製药公司是该技术的主要用户之一,因为它们需要更好地保护其产品免受潮湿、氧气和其他气体的影响。

- 泡壳包装是小单位包装轻量产品的理想选择。此外,由于它适合零售用途,因此不适合处理重物。这些限制阻碍了当前终端用户产业在重型应用中采用和应用泡壳包装,从而限制了成长机会。因此,这种包装类型的成长是渐进的、有机的。

拉丁美洲泡壳包装市场的趋势

製药业是成长最快的终端用户产业

- 製药业对泡壳包装解决方案提出了许多要求,包括环境隔离、成本效益、高水准保护、易于操作和维持药效。这些包装特别适合满足严格的法规,并且因其保护性能、成本效益、适应性以及製药和包装行业的要求而受到高度重视。

- 当药品采用泡壳包装时,消费者可以追踪他们的药物和剂量,从而提高用药依从性。泡壳包装的单位剂量特性降低了错误剂量的风险。药物锭剂、胶囊和锭剂通常以单位剂量的形式采用泡壳包装。与其他药品包装技术相比,单位剂量泡壳包装的主要优势在于,可以保证每剂产品/包装的完整性(包括保质期),并且能够通过在每个剂量上方打印星期几来製作依从性包装或日历包装。

- 药品通常采用泡壳包装,因为泡罩包装可以防止气体和湿气,并延长保质期。在高湿度和高温条件下实现产品稳定性是一项挑战。泡壳材料可以减轻运输过程中可能发生的温度波动。

- 药品泡壳包装主要有两种类型:第一种类型的盖子由透明塑胶或塑胶、纸和箔的复合材料製成,腔体由透明热成型塑胶製成。第二种型腔是由于冷拉而产生的,箔片是两种腹板的重要组成部分。 PVC、PCTFE、PVDC、用于较不敏感产品的热成型泡壳和用于敏感活性药物原料药(API) 的 Alu-Alu 冷成型泡壳是製药业泡壳包装中可用的部分解决方案。

- 由于创新包装技术的使用日益广泛且该地区对药品的需求日益增长,拉丁美洲已成为药品泡壳包装的成长市场。预计未来几年该地区将经历显着的增长。这是由不断上涨的医疗成本和对特殊药物的需求所推动的。

- 根据美国商务部的数据,2023 年墨西哥的药品销售额约为 108.3 亿美元,而 2018 年为 100.3 亿美元。随着製药业的发展,对泡壳包装等有效包装解决方案的需求也随之成长。泡壳包装通常用于锭剂和胶囊的单位剂量包装,提供对药品非常重要的保护和剂量准确性。

巴西可望占据主要市场占有率

- 同时,巴西政府努力改善商业环境,以相对廉价的生产能力维持巴西的稳定成长,吸引各行各业的大公司在巴西设立工厂。这使得这些公司能够同时服务国内市场和北美市场。因此,由于国内产量的增加,该地区对泡壳包装的需求预计将大幅快速发展。

- 有几种塑胶聚合物用于製造泡壳包装,包括 PVC、PVDC、PCTFE 和 COP。 PVC 是最常用的泡壳包装材料,有时也称为聚氯乙烯。它的最大优点就是成本低。在巴西,政府上週稍早宣布降低聚丙烯进口税的措施已取得成效。进口材料的提案、报价和交易增加。

- 根据巴西经济部消息,巴西政府自8月5日至2023年8月4日期间,暂时将悬浮法聚氯乙烯和聚丙烯共聚物(PPC)的进口关税从11.2%下调至4.4%。所有产品均不受进口配额限制。对于聚丙烯共聚物,考虑了 HS 代码为 3902.3000 的产品。 HS 编号 3904.1010 的产品视为悬浮 PVC。属于 HS 编码 3901.4000 且密度低于 0.94 的乙烯和 α-烯烃共聚物产品的进口关税也从 11.2% 降至 3.3%。

- 巴西对医疗产品的需求不断增长,推动了製药和医疗保健领域对泡壳包装的需求激增。对于药品生产企业来说,遵守药品包装标准至关重要,这增加了对泡壳包装等包装技术的需求。

- 根据美国商务部国际贸易管理局的数据,巴西是拉丁美洲最大的医药和医疗保健市场,其医疗保健支出占国内生产毛额的9.1%。该地区最大的赢家是当地的私人实验室,突显了随着固态剂型的增加,该地区对药品泡壳包装供应商的需求不断扩大。

- 根据 IQVIA 的数据,预计拉丁美洲在 2023 年至 2027 年期间的复合年增长率将达到 22%。与其他地区相比,拉丁美洲的医药市场成长率最高。随着医药市场的成长,符合法规要求的包装的需求也在成长。泡壳包装以防止篡改、安全和无污染的包装而闻名,使其成为满足严格的药品法规的首选。

拉丁美洲泡壳包装产业概况

拉丁美洲泡壳包装市场较为分散,主要参与者包括 Amcor Group GmbH、Tekni-Plex Inc.、Constantia Flexibles Group GmbH、Klockner Pentaplast Group 和 West Rock Company。市场参与者正在采用伙伴关係、创新和收购等策略来改善其产品供应并获得永续的竞争优势。

2024 年 1 月,TekniPlex Healthcare 与 Alpek Polyester 合作,宣布推出「世界上第一款」由消费后回收材料製成的药用级 PET泡壳膜。这款创新薄膜由 30% 的消费后回收单体製成,将在 Pharmapack 2024 上亮相。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

- 产业价值链分析

第五章 市场动态

- 市场驱动因素

- 老龄人口增加和疾病流行

- 小型化和相对低成本等产品创新

- 市场挑战

- 法规的动态性质和缺乏处理重负荷的能力

第六章 市场细分

- 按工艺

- 热成型

- 冷成型

- 按材质

- 塑胶薄膜

- 纸和纸板

- 铝

- 按最终用户产业

- 消费品

- 药品

- 按国家

- 巴西

- 墨西哥

第七章 竞争格局

- 公司简介

- Amcor Group GmbH

- Tekni-Plex Inc.

- Constantia Flexibles Group GmbH

- Klockner Pentaplast Group

- West Rock Company

- Huhtamaki Oyj

- Honeywell International Inc.

- Sonoco Products Company

第八章投资分析

第九章 市场机会与展望

The Latin America Blister Packaging Market size is estimated at USD 1.58 billion in 2025, and is expected to reach USD 2.26 billion by 2030, at a CAGR of 7.42% during the forecast period (2025-2030).

Key Highlights

- The pharmaceutical industry is the largest end-user of blister packaging and has a significant market share. This high share is due to the many advantages of blister packaging in the pharmaceutical industry, including improved product protection, ease of distribution, unit dosage packaging, and product identification.

- Innovative technology in blister packs, such as radio frequency identification (RFID) tags deployed using seals on the outside packaging, is increasingly used due to the potential to provide individualized security throughout the supply chain. Blister packs protect compact medical devices and pharmaceuticals from oxygen, odors, and moisture, extending shelf life. Inadequate medication adherence is a pervasive problem that leads to chronic disease complications and increased healthcare costs. Packaging methods using blister packs may be widely recommended to address drug adherence issues during the forecast period.

- Blister packaging is now using more nanotechnology. Nanotechnology improves barrier protection and makes the packaging lighter. Pharmaceutical businesses in Latin America, which need better protection for their products against moisture, oxygen, and other gases, are among the primary users of this technology.

- Blister packaging is best suited for lightweight products packaged in small units. It is also suited for retail handling, making it not a preferred choice in heavy goods handling. Such limitations have hindered the adoption and application of blister packaging for heavy goods, even in the current end-user industry applications, limiting growth opportunities. Therefore, the growth of this type of packaging has been gradual and organic.

Latin America Blister Packaging Market Trends

The Pharmaceutical Segment to be the Fastest-growing End-user Industry

- The pharmaceutical sector poses different demands for blister packaging solutions concerning insulation from external surroundings, cost-effectiveness, high levels of protection, and ease of handling and retaining the effectiveness of the medicine. These packs are uniquely suited to meet stringent regulations and are highly valued for their protective properties, cost-effectiveness, adaptability, and pharmaceutical and packaging industry requirements.

- Adherence is improved when medicines are blister packaged because consumers can track their medications and dosage. The unit dosage feature of blisters reduces the risk of incorrect dosing. Pharmaceutical pills, capsules, or tablets are frequently packaged in blister packs as unit doses. The main benefits of unit-dose blister packs over other packaging techniques for pharmaceutical products are the assurance of product/packaging integrity (including shelf life) of each dose and the capacity to produce a compliance pack or calendar pack by printing the days of the week above each dose.

- Drugs are typically packaged in blister packs because they are more protected from gas and moisture, giving them a longer shelf life. Product stability is challenging to achieve in situations of high humidity and temperature. Blistering materials can mitigate temperature swings that can happen during shipping.

- For pharma packaging, there are primarily two types of blister packing. The lid of the first type is made of clear plastic or a composite material made of plastic, paper, and foil, while the cavity is made of clear thermoformed plastic. The second type's cavity is caused by cold stretching, and foil is a crucial component of both webs. PVC, PCTFE, PVDC, and thermoform blisters for less sensitive products or Alu-Alu cold-form blisters for more sensitive active pharmaceutical ingredients (APIs) are a few solutions available in blister packaging for the pharmaceutical industry.

- Latin America is a growing market for pharmaceutical blister packaging due to the increased use of creative packaging techniques and a rising need for medications in the region. The region is predicted to have significant growth in the following years. This results from rising medical expenses and the demand for specialty medications.

- According to the US Department of Commerce, in 2023, Mexico sold around USD 10.83 billion worth of pharmaceutical products, compared with USD 10.03 billion in 2018. As the pharmaceutical industry grows, the need for effective packaging solutions like blister packaging also increases. Blister packaging is commonly used for unit-dose packaging of tablets and capsules, providing protection and dosage accuracy, which are crucial for pharmaceutical products.

Brazil is Expected to Hold Major Market Share

- Many large companies across all industries have established facilities in Brazil due to the government's simultaneous efforts to improve the business environment and maintain Brazil's steady growth in relatively cheap productive capacity. This has enabled these companies to serve both domestic markets and North America. As a result, the demand for blister packaging is anticipated to develop significantly fast in the region due to rising domestic production.

- Several plastic polymers, including PVC, PVDC, PCTFE, and COP, create blister packaging. PVC is the most used blister packing material, sometimes known as polyvinyl chloride. Its key benefit is its cost-effectiveness. Brazil saw results from the government's reduction in PP import taxes, which was announced at the start of the previous week. More proposals, offers, and deals were made for imported material.

- According to the Ministry of Economy, the Brazilian government temporarily lowered import duties on suspension-produced polyvinyl chloride and polypropylene copolymers (PPC) from 11.2% to 4.4% starting on August 5 and lasting until August 4, 2023. The import of either product is not subject to a set quota. Products listed under the HS code 3902.3000 were considered for polypropylene copolymer. The products with the HS number 3904.1010 were considered for suspension-made PVC. Import duties on ethylene and alpha-olefin copolymer products with densities less than 0.94 that fall under the HS code 3901.4000 were also lowered from 11.2% to 3.3%.

- The pharmaceutical and healthcare sectors are witnessing a surge in demand for blister packaging due to Brazil's rising demand for medical products. Following packaging standards for pharmaceutical products is crucial for pharmaceutical producers, which drives the need for packaging techniques like blister packing.

- According to the International Trade Administration, US Department of Commerce, with a 9.1% GDP expenditure on healthcare, Brazil has the largest pharmaceutical and healthcare market in Latin America. The most considerable profits in the region are made by the local private laboratories, which highlights the expanding need for pharmaceutical blister packaging suppliers in the area as the number of solid dosages develops.

- According to IQVIA, Latin America is expected to register a CAGR of 22% from 2023 to 2027. Latin America has the highest pharmaceutical market growth percentage compared with other regions. As the pharmaceutical market grows, so does the need for packaging that complies with regulatory standards. Blister packaging is known for its ability to provide tamper-evident, secure, and contamination-free packaging, making it a preferred choice to meet stringent pharmaceutical regulations.

Latin America Blister Packaging Industry Overview

The Latin American blister packaging market is fragmented, with major players like Amcor Group GmbH, Tekni-Plex Inc., Constantia Flexibles Group GmbH, Klockner Pentaplast Group, and West Rock Company. Market players employ strategies like partnerships, innovations, and acquisitions to improve their product offerings and achieve a sustainable competitive edge.

In January 2024, TekniPlex Healthcare, in collaboration with Alpek Polyester, introduced the 'world's inaugural' pharmaceutical-grade PET blister film featuring post-consumer recycled material. This innovation, highlighting 30% post-consumer recycled monomers, will debut at Pharmapack 2024.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Geriatric Population and Prevalence of Diseases

- 5.1.2 Product Innovations such as Downsizing, Coupled with Relatively Low Costs

- 5.2 Market Challenges

- 5.2.1 Dynamic Nature of Regulations and Inability to Support Heavy Goods

6 MARKET SEGMENTATION

- 6.1 By Process

- 6.1.1 Thermoforming

- 6.1.2 Cold Forming

- 6.2 By Material

- 6.2.1 Plastic Films

- 6.2.2 Paper and Paperboard

- 6.2.3 Aluminum

- 6.3 By End-user Industry

- 6.3.1 Consumer Goods

- 6.3.2 Pharmaceutical

- 6.4 By Country

- 6.4.1 Brazil

- 6.4.2 Mexico

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor Group GmbH

- 7.1.2 Tekni-Plex Inc.

- 7.1.3 Constantia Flexibles Group GmbH

- 7.1.4 Klockner Pentaplast Group

- 7.1.5 West Rock Company

- 7.1.6 Huhtamaki Oyj

- 7.1.7 Honeywell International Inc.

- 7.1.8 Sonoco Products Company

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND OUTLOOK

泡壳包装设备市场:依设备类型、成型材料、自动化程度、速度及最终用途产业划分-2026-2032年全球预测泡壳包装市场:2026-2032年全球市场预测(依材料、技术、剂型、应用及通路划分)

泡壳包装设备市场:依设备类型、成型材料、自动化程度、速度及最终用途产业划分-2026-2032年全球预测泡壳包装市场:2026-2032年全球市场预测(依材料、技术、剂型、应用及通路划分) 2026-2034年全球泡壳包装器材市场规模、份额、趋势及成长分析报告泡壳包装生产线市场按组件、包装类型、材料、自动化程度、成型技术、应用和最终用途行业划分,全球预测,2026-2032年泡壳包装市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测

2026-2034年全球泡壳包装器材市场规模、份额、趋势及成长分析报告泡壳包装生产线市场按组件、包装类型、材料、自动化程度、成型技术、应用和最终用途行业划分,全球预测,2026-2032年泡壳包装市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测 2026年全球泡壳包装市场报告2026年全球泡壳包装机械消费市场报告

2026年全球泡壳包装市场报告2026年全球泡壳包装机械消费市场报告 安瓿及泡壳包装市场-全球产业规模、份额、趋势、机会、预测:依包装类型、材料、最终用户、地区及竞争格局划分,2021-2031年泡壳包装市场 - 全球产业规模、份额、趋势、机会及预测(按类型、材料、最终用途产业、技术、区域和竞争格局划分,2021-2031年)PVC Aclar泡壳市场按形状、封装类型、最终用户和应用划分,全球预测,2026-2032 年

安瓿及泡壳包装市场-全球产业规模、份额、趋势、机会、预测:依包装类型、材料、最终用户、地区及竞争格局划分,2021-2031年泡壳包装市场 - 全球产业规模、份额、趋势、机会及预测(按类型、材料、最终用途产业、技术、区域和竞争格局划分,2021-2031年)PVC Aclar泡壳市场按形状、封装类型、最终用户和应用划分,全球预测,2026-2032 年