|

市场调查报告书

商品编码

1687204

声学感测器-市场占有率分析、产业趋势与统计、成长预测(2025-2030)Sound Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

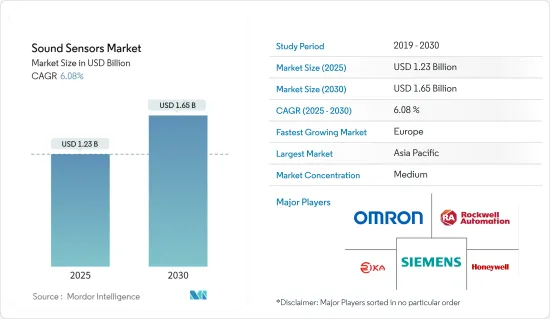

声学感测器市场规模预计在 2025 年为 12.3 亿美元,预计到 2030 年将达到 16.5 亿美元,预测期内(2025-2030 年)的复合年增长率为 6.08%。

关键亮点

- 对可靠、高性能感测器的需求不断增长是推动声学感测器市场高速成长的关键因素。此外,市场上的多项技术进步和声学感测器製造成本的下降也促进了这些感测器的普及。

- 例如,数位讯号处理在将类比音讯转换为数位形式以供数位环境使用的过程中起着关键作用。数位讯号处理是一个持续改进的过程,它影响着专业安装的音响系统的设计、安装和使用。

- 现在,感测器技术可以让自动化设备无需非常强大的智慧处理就能解释声音和其他资料。这使得紧凑、低功耗系统的开发成为可能,这些系统可以提高机器对机器互动的自主性,并在人机互动中提供自然感知的使用者介面。

- 声学感测器技术的进步正在提高无线耳机和头戴式耳机的音质和电池寿命。预计这些改进将推动市场成长。

- 然而,以其他技术(如麦克风、超音波感测器等)取代声音感测器的可能性可能会抑制所研究市场的成长。

- 自新冠疫情爆发以来,对变革和创意解决方案的需求不断增加。在新技术方面,研究人员正在开发一种响应特定声波而振动的新型感测器。被动声学感测器用于建筑、地震和某些医疗设备监测,可以节省数百万个电池。研究人员也对用于监测废弃油井的无电池感测器感兴趣。当气体从井孔洩漏时,会产生独特的嘶嘶声。这种机械感测器可以检测到这种嘶嘶声并启动警报,而无需持续消耗电力。

声学感测器市场趋势

工业领域是成长最快的终端用户产业

- 声学感测器广泛应用于各种工业应用,例如监测机器振动和噪声,以及分析高速运行过程中机器元件疲劳故障引起的声波发射。这些设备为工业自动化系统提供资料输入,使机器和机器人能够根据透过所述感测部件获得的相应参数按照特定规则执行任务,从而能够更有效地控制不同环境条件下的操作,同时显着改善安全通讯协定。

- 工业 4.0 的兴起趋势以及机器人在製造、库存和其他部门的各种用途的应用预计将推动市场成长。德国正在发展成为专注于人工智慧及其应用(包括机器学习、深度学习、电脑视觉和预测分析)的新兴企业的首选中心。根据欧盟Start-Ups的数据,柏林是继伦敦之后欧洲第二大新Start-Ups中心。超过 65% 的德国公司最近采用了工业 4.0,其余 25% 的公司正在尝试遵循当前的工业 4.0 计划。

- 根据 IFR 预测,全球工业机器人的采用率将大幅增加,到 2024 年,全球工厂将有 518,000 台工业机器人运作。工业机器人市场的显着成长轨迹预计将推动所研究市场的需求。消息人士称,预计未来几年工业机器人出货量将大幅成长,超过2022年的峰值,当时全球工业机器人出货量约为45.3万台。到2024年,亚洲/澳洲的工业机器人安装量预计将达到37万台。

- 为了加强本国製造业,许多国家正在大力投资并与其他国家合作创造製造业机会。中国正在将第四次工业革命(工业 4.0)的概念作为其十年计划「中国製造 2025」的一部分,以赶上德国等製造业强国,并以更低的人事费用击败其他新兴经济体的竞争对手。这是中国全面实现工业现代化的努力。该计划重点关注10个领域,包括高端电脑机械和机器人技术。此类工业 4.0 倡议可望在市场中创造机会。

- 强大的生态系统也为该市场提供了助力,支援各地区快速采用新技术。例如,物联网和工厂自动化的采用正在帮助市场,因为已开发国家已经建立了最大限度发挥声学感测器效用所需的基础设施。预计「美国製造」等政府倡议将推动工业领域采用先进技术,从而在预测期内为市场创造机会。

欧洲正在经历快速成长

- 声学感测器广泛应用于各种工业用途,例如监测机器振动和噪声,以及分析高速运行过程中机器元件疲劳故障引起的声波发射。根据Make UK的数据,截至2023年,英国年产值将达到1,830亿英镑(2,325亿美元),是世界第九大製造业国家。近年来,人工智慧(AI)及相关数位和机器人技术的兴起为英国製造业带来了新的机会。它有望提高效率、生产力和盈利。

- 此外,国防系统的发展和创新也有望推动市场发展。例如,2023 年 6 月,以色列航太公司的子公司 Elta Systems 与德国声纳製造商 Atlas Elektronik 合作开发反潜战系统。该公司还宣布与德国蒂森克虏伯海洋系统公司的子公司阿特拉斯建立新的合作伙伴关係,推出一款联合产品,即名为「蓝鲸」的反潜战(ASW)型号。该系统基于 Elta Systems 自主水下航行器 (AUV),并整合了 Atlas 拖曳式被动声纳三重阵列。

- 声学感测器广泛应用于各种工业用途,例如监测机器的振动和噪声,以及分析设备高速运作时机器元件疲劳失效引起的声波发射。根据Make UK的数据,英国仍是全球第九大製造业国家,年产值达1,830亿英镑(2,319.8亿美元)。近年来,人工智慧(AI)及相关数位和机器人技术的兴起为该国的製造业带来了新的机会。它有望提高效率、生产力和盈利。

- 该国製造业先进技术的引进也得到了政府大量资金的支持。例如,2022 年 10 月,英国研究与开发部门 (UKRI) 向 12 个智慧工厂计划拨款 1,370 万英镑(1,737 万美元),用于开发可提高製造业能源效率、生产力和成长的技术。这是英国政府耗资 1.47 亿英镑(1.8634 亿美元)的「製造更智慧创新挑战」计画的一部分,旨在提高英国製造业的技术应用。

- 2022 年 5 月,英国政府公布了透过新的智慧製造资料中心 (SMDH) 提高中小型製造企业生产力和竞争力的计画。新的中心和试验平台将由阿尔斯特大学主导,并获得 5,000 万英镑(6,338 万美元)的政府资助和企业共同投资。此外,在第二次疫情期间,法国为了维护国家主权和军事独立,开始研究第三代核弹弹道导弹潜舰的设计,并已建造了第一段。

声学感测器市场概况

- 声学感测器市场是一个分散的市场,有几家主要企业,包括霍尼韦尔国际公司、通用电气测量与控制解决方案、Maxbotix 公司、罗克韦尔自动化公司、西门子公司、意法半导体公司、罗伯特博世有限公司、松下公司、Bruel & Kjaer GmbH 和 Teledyne Technologies Incorporated。市场已经看到主要市场参与企业之间的多项创新、伙伴关係和协作,以增强技术力并更好地满足消费者不断变化的需求。

- 2023 年 6 月,霍尼韦尔推出了一项旨在提高低压燃烧空气和燃气监测和管理的有效性和可靠性的解决方案:DG 智慧感测器。对于OEM) 、最终用户和系统整合商而言,该解决方案代表着机会,即透过采用符合工业 4.0 的数位化趋势来改善燃烧系统的性能并改变其运作动态。它还列出了精确的监控功能。

- 2023年2月,Polysense宣布推出面向智慧城市和工业环境的室内外声学和噪音感测器集群,实现健康监测和城市管理。升级后的声学/噪音感测器由 iEdge 4.0 OS 上的模组化和可配置的 WxS 产品平台提供支持,与带有附加 PolySense PSS 感测器的 BYOD 结合使用时,可为用户提供更强大的监测和采取行动应对噪音污染的能力。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章市场动态

- 市场驱动因素

- 由于市场技术进步而采用率提高

- 製造成本低

- 市场限制

- 替代技术的出现

第六章 技术简介

- 透过水中听音器

- 定向

- 定向

- 透过麦克风

- 驻极体麦克风

- 压电麦克风

- 电容麦克风

- 动圈/磁性麦克风

- 其他麦克风

第七章市场区隔

- 按最终用户产业

- 消费性电子产品

- 通讯

- 产业

- 防御

- 医疗保健

- 其他的

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

第八章竞争格局

- 公司简介

- Honeywell International Inc.

- Omron Corporation

- Hunan Rika Electronic Tech Co. Ltd

- Rockwell Automation Inc.

- Siemens AG

- Stmicroelectronics NV

- Robert Bosch Gmbh

- Panasonic Corporation

- Bruel And Kjaer

- Teledyne Technologies Incorporated

第九章投资分析

第十章 市场机会与未来趋势

简介目录

Product Code: 56504

The Sound Sensors Market size is estimated at USD 1.23 billion in 2025, and is expected to reach USD 1.65 billion by 2030, at a CAGR of 6.08% during the forecast period (2025-2030).

Key Highlights

- The rising demand for reliable and high-performance sensors is a primary driver responsible for the high growth rate of the sound sensors market. Several technology advancements in the market and decreasing manufacturing costs of sound sensors have also led to the increasing adoption of these sensors.

- For instance, digital signal processes play a crucial role in converting analog audio to digital format for use in a digital environment. They have undergone continual improvement, influencing the design, installation, and use of professionally installed sound systems.

- Sensor technology has enabled automated devices to interpret sounds and other data without extremely powerful intelligent processing. This has led to the development of compact, low-power systems that enable increased autonomy in machine-to-machine interactions and offer natural perceptual user interfaces for human-machine interactions.

- Advancements in sound sensor technology have led to improvements in sound quality and battery life for wireless earphones and headphones. These improvements are expected to lead to the market's growth.

- However, the possibility of substituting sound sensors with other technologies (like microphones, ultrasonic sensors, etc.) is likely to restrain the growth of the market studied.

- In the post-COVID-19, there is an increased demand for transformation and creative solutions. In terms of newer technology, researchers are developing a new type of sensor that reacts to certain sound waves, causing it to vibrate. This Passive sound-sensitive sensors could be used to monitor buildings, earthquakes or certain medical devices and save millions of batteries. There is also interest by researchers in battery-free sensors for monitoring decommissioned oil wells. Gas can escape from leaks in boreholes, producing a characteristic hissing sound. Such a mechanical sensor could detect this hissing and trigger an alarm without constantly consuming electricity - making it far cheaper and requiring much less maintenance.

Sound Sensors Market Trends

Industrial Sector to be the Fastest Growing End-user Industry

- Sound sensors are widely employed for various industrial purposes like monitoring machinery vibrations and noises and analyzing acoustic emissions generated due to fatigue failure on machine elements when equipment runs at high speeds. These devices provide data input into industrial automation systems, which allow machines or robots to execute tasks according to specific rules depending on corresponding parameters acquired through said detection components, leading toward more effective control over operations under different environmental conditions while increasing safety protocols significantly.

- The growing trend of Industry 4.0 and the use of robotics for various purposes in manufacturing, stock, and other units is expected to drive the market's growth. Germany is growing as a preferred hub for start-ups focusing on AI and its applications, such as machine learning, deep learning, computer vision, and predictive analytics. According to EU start-ups, Berlin is Europe's second-biggest start-up hub after London. Over 65% of German companies recently implemented Industry 4.0 practices, with the other 25% pitching to follow the ongoing suit.

- According to the IFR forecasts, the global adoption of industrial robots is expected to increase significantly to 518,000 industrial robots operational across factories worldwide by 2024. The significant growth trajectory of the industrial robot market is expected to drive the demand for the market studied. According to the same source, industrial robot shipments are expected to rise significantly in the coming years, surpassing the peak in 2022, when around 453,000 industrial robots were shipped worldwide. It is projected that by 2024, industrial robot installations in Asia/Australia are projected to reach 370,000 units.

- Many countries invest heavily and collaborate with other countries to create opportunities for manufacturers to strengthen their manufacturing industry. China is embracing the concept of the fourth industrial revolution (Industry 4.0) as part of its 10-year Made in China 2025 plan to catch up with manufacturing powerhouses like Germany and stand tall in competition with other developing countries with lower labor costs. It is an effort to modernize Chinese industry comprehensively. The plan focuses on ten areas: high-end computerized machinery, robotics, etc. Such initiatives in Industry 4.0 are anticipated to create opportunities in the market.

- The market has also been helped by a robust ecosystem sustaining the fast adoption of new technology in various regions. For instance, IIOT adoption and factory automation have aided the market, as the infrastructure required to maximize the utility of acoustic sensors is already in use in developed countries. Government initiatives such as "Made in America" are expected to drive the adoption of advanced technologies in the industrial domain, creating opportunities in the market during the forecast period.

Europe to Witness Significant Growth

- Sound sensors are widely employed for various industrial purposes like monitoring machinery vibrations and noises and analyzing acoustic emissions generated due to fatigue failure on machine elements when equipment runs at high speeds. As per 2023, with an annual output of GBP 183 (USD 232.5 Billion) billion, the United Kingdom remains the ninth-largest manufacturing nation in the world, according to Make UK. Moreover, in recent times, the rise of artificial intelligence (AI) and associated digital and robotic technologies has presented new opportunities for the country's manufacturers. It promises even greater levels of efficiency, productivity, and profitability.

- Moreover, developments and innovations in the defense system are also expected to boost the market. For instance, in June 2023, Elta Systems, a subsidiary of Israel Aerospace Industries, teamed up with German sonar manufacturer Atlas Elektronik to develop an anti-submarine warfare system. The firm announced its new partnership with Atlas, a subsidiary of Germany's Thyssenkrupp Marine Systems, aimed at launching a joint product, the BlueWhale anti-submarine warfare (ASW) variant. The system is based on Elta's autonomous underwater vehicle (AUV), integrated with Atlas's towed passive sonar triple array.

- Sound sensors are widely employed for various industrial purposes like monitoring machinery vibrations and noises and analyzing acoustic emissions generated due to fatigue failure on machine elements when equipment runs at high speeds. According to Make UK, with an annual output of GBP 183 billion (USD 231.98 billion), the United Kingdom remains the ninth-largest manufacturing nation in the world. Moreover, in recent times, the rise of artificial intelligence (AI) and associated digital and robotic technologies has presented new opportunities for the country's manufacturers. It promises even greater levels of efficiency, productivity, and profitability.

- The adoption of advanced technologies in the country's manufacturing industry is also aided by much government funding. For instance, in October 2022, UK Research and Innovation (UKRI) awarded 12 smart factory projects a share of GBP 13.7 million (USD 17.37 million) in funding to develop technologies that improve energy efficiency, productivity, and growth in manufacturing. It is a part of the government's wider GBP 147 million (USD 186.34 million) Made Smarter Innovation Challenge that seeks to increase the use of technology within UK manufacturing.

- In May 2022, the UK government revealed plans to boost manufacturing SMEs' productivity and competitiveness through a new Smart Manufacturing Data Hub (SMDH). The new hub and testbed were expected to be led by Ulster University and backed by GBP 50 million (USD 63.38 million) in government funds and business co-investment. Moreover, during the second pandemic, France launched design studies and built the first sections of a third-generation nuclear ballistic missile submarine to maintain national sovereignty and military independence.

Sound Sensors Market Overview

- The sound sensors market is a fragmented market with the presence of several significant players like Honeywell International Inc., GE Measurement & Control Solutions, Maxbotix Inc., Rockwell Automation Inc., Siemens Inc., ST Microelectronics Inc., Robert Bosch GmbH, Panasonic Corporation, Bruel & Kjaer GmbH, Teledyne Technologies Incorporated, etc. The market studied is witnessing several innovations, partnerships, and collaborations among significant market players to enhance their technical capabilities and better serve consumers' evolving requirements.

- In June 2023, Honeywell unveiled a solution to improve the effectiveness and dependability of monitoring and managing low-pressure combustion air and fuel gases as the DG Smart Sensor. For OEMs, end users, and system integrators, this solution presents an opportunity to enhance combustion system performance and change the operating dynamics by embracing digitalization trends in line with Industry 4.0. It also offers accurate monitoring capabilities.

- In February 2023, Polysense announced the launch of indoor and outdoor sound/noise sensor clusters for Smart City and Industrial environments, enabling health monitoring and city management. Empowered by the iEdge 4.0 OS modular and configurable WxS product platform, the upgraded sound/noise sensor is claimed to be BYODed with additional Polysense PSS sensors to equip users with more powerful capabilities to monitor and take action on noise pollution.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute

- 4.2.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Technology Advancement in the Market, Leading to Increasing Adoption

- 5.1.2 Low Manufacturing Cost

- 5.2 Market Restraints

- 5.2.1 Emergence of Alternative Technologies

6 TECHNOLOGY SNAPSHOT

- 6.1 By Hydrophone

- 6.1.1 Omni-directional

- 6.1.2 Directional

- 6.2 By Microphone

- 6.2.1 Electret Microphones

- 6.2.2 Piezoelectric Microphones

- 6.2.3 Condenser Microphones

- 6.2.4 Dynamic/Magnetic Microphones

- 6.2.5 Other Microphones

7 MARKET SEGMENTATION

- 7.1 By End-user Industry

- 7.1.1 Consumer Electronics

- 7.1.2 Telecommunications

- 7.1.3 Industrial

- 7.1.4 Defense

- 7.1.5 Healthcare

- 7.1.6 Other End-user Industries

- 7.2 By Geography

- 7.2.1 North America

- 7.2.2 Europe

- 7.2.3 Asia

- 7.2.4 Australia and New Zealand

- 7.2.5 Latin America

- 7.2.6 Middle East and Africa

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Honeywell International Inc.

- 8.1.2 Omron Corporation

- 8.1.3 Hunan Rika Electronic Tech Co. Ltd

- 8.1.4 Rockwell Automation Inc.

- 8.1.5 Siemens AG

- 8.1.6 Stmicroelectronics NV

- 8.1.7 Robert Bosch Gmbh

- 8.1.8 Panasonic Corporation

- 8.1.9 Bruel And Kjaer

- 8.1.10 Teledyne Technologies Incorporated

9 INVESTMENT ANALYSIS

10 MARKET OPPORTUNITIES AND FUTURE TRENDS

02-2729-4219

+886-2-2729-4219

2025年全球智慧建筑声波感测器市场报告

2025年全球智慧建筑声波感测器市场报告 全球声学感测器市场(按类型、技术、最终用途和应用)预测 2025-2032全球声波感测器市场(按类型、应用和材料)预测 2025-2032

全球声学感测器市场(按类型、技术、最终用途和应用)预测 2025-2032全球声波感测器市场(按类型、应用和材料)预测 2025-2032 全球声音感测器市场

全球声音感测器市场 声波感测器市场规模、份额及成长分析(按感测器类型、技术、最终用途产业和地区)-2025 年至 2032 年产业预测2025年声波感测器全球市场报告高保真声波感测器市场分析与预测(至2034年):类型、产品、服务、技术、组件、应用、材料类型、部署、最终用户、功能

声波感测器市场规模、份额及成长分析(按感测器类型、技术、最终用途产业和地区)-2025 年至 2032 年产业预测2025年声波感测器全球市场报告高保真声波感测器市场分析与预测(至2034年):类型、产品、服务、技术、组件、应用、材料类型、部署、最终用户、功能 船用声学感测器-市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)表面声波感测器:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)2025年海洋声波感测器全球市场报告

船用声学感测器-市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)表面声波感测器:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)2025年海洋声波感测器全球市场报告

▼