|

市场调查报告书

商品编码

1687208

润滑油添加剂:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Lubricant Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

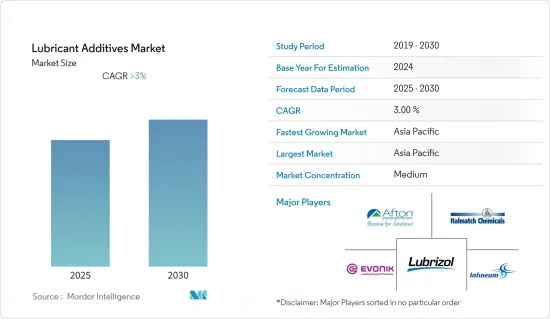

预测期内,润滑油添加剂市场预计将以超过 3% 的复合年增长率成长。

新冠疫情对市场产生了负面影响。与 COVID-19 相关的限制减少了多个行业的维护需求。主要影响体现在汽车和建筑业,但从 2021 年起,由于汽车和建设活动的增加,市场开始稳定成长。

主要亮点

- 短期内,中东和非洲有关排放气体和工业成长的严格环境法规是市场成长的主要驱动力。

- 然而,预测期内机器和汽车换油间隔的延长预计是抑制目标产业成长的主要因素。

- 然而,高性能润滑油在亚太地区日益普及,很可能在不久的将来为全球市场提供丰厚的成长机会。

- 预计在评估期内,亚太地区的润滑油添加剂市场将出现健康成长,这得益于润滑油因其优良的性能而被广泛应用于汽车和建筑等终端使用领域。

润滑油添加剂市场趋势

汽车和其他运输业的需求增加

- 汽车和飞机、船等其他运输媒介是润滑油的最大市场。

- 引擎设计不断改进,以提高性能、提高效率并满足环境排放气体法规。

- 引擎油、齿轮油、变速箱油、脂类及压缩机油是各类汽车中使用最广泛的润滑油。润滑油在售后市场和OEM中占有较高的市场份额。

- 中型和高性能润滑油广泛应用于承受高负荷和突然摩擦的汽车零件,例如齿轮、传动系统和引擎。

- 根据OICA的数据,2021年机动车(所有类型)总产量为80,145,988辆,而2020年为77,711,725辆,增长了3%。

- 在北美,美国也拥有世界上最大的汽车工业之一。根据 OICA 的数据,2021 年汽车产量为 9,167,214 辆,较 2020 年的 8,822,399 辆成长 4%。

- 航太工业,特别是商业航空运输中复合材料的强劲增长,将导致腐蚀抑制剂和去除液的变化。

- 此外,根据国际航空运输协会(IATA)的数据显示,2020年全球商业航空公司的收益价值为3,730亿美元,预计2021年将达到4,720亿美元,与前一年同期比较增26.7%。预计到 2022 年将达到 6,580 亿美元。

- 最近,飞机製造商一直在寻找加快生产的方法来填补订单积压。例如,波音公司的《2022-2041年商业展望》估计,到2041年,全球新飞机交付总量将达到41,170架。 2019年全球飞机持有约25,900架,2041年可能达到47,080架。

- 预计所有上述因素都将在未来几年推动润滑油添加剂市场的发展。

中国主宰亚太地区

- 在亚太地区,中国占据区域市场占有率的主导地位。食品和汽车行业正在成长。

- 根据OICA统计,2021年中国汽车产量为26082220辆,较去年同期成长3%。

- 食品加工行业正在成熟并经历缓慢增长。加工、包装、冷冻食品越来越受欢迎。饮料业正呈现向健康、天然、方便的即饮冰沙、果汁和优格发展的趋势。

- 中国是金属加工液的主要消费国。该地区建设活动的强劲增长以及造船和飞机订单的增加预计将推动金属製造的成长。

- 近年来,中国航空太空船工业取得了长足的发展。根据波音《2022-2041年商用飞机展望》,到2041年中国将交付约8,485架新飞机,市场价值达5,450亿美元。

- 鑑于上述情况,预计中国将在预测期内主导亚太地区。

润滑油添加剂产业概况

全球润滑油添加剂市场本质上是部分一体化的,主要企业包括赢创工业股份公司、意特麦琪化工有限公司 (The Elco Corporation)、润英联国际有限公司、路博润公司、雅富顿化学公司等(不分先后顺序)。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 有关排放的严格环境法规

- 中东和非洲的产业成长

- 限制因素

- 延长机器和汽车的换油间隔

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场区隔

- 产品类型

- 分散剂和乳化剂

- 黏度指数增进剂

- 清洗剂

- 腐蚀抑制剂

- 抗氧化剂

- 极压添加剂

- 摩擦改进剂

- 其他功能

- 润滑剂类型

- 机油

- 传动液和液压油

- 金属加工油

- 通用工业用油

- 齿轮油

- 润滑脂

- 加工油

- 其他润滑剂

- 最终用户产业

- 汽车和其他交通工具

- 发电

- 重型机械

- 冶金与金属加工

- 饮食

- 其他最终用户产业

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚国协

- 其他亚太地区

- 北美洲

- 美国

- 墨西哥

- 加拿大

- 欧洲

- 德国

- 英国

- 俄罗斯

- 义大利

- 法国

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 合併、收购、合资、合作和协议

- 市场排名分析

- 主要企业策略

- 公司简介

- Afton Chemical

- BASF SE

- BRB International

- Chevron Corporation

- Croda International PLC

- DOG Deutsche Oelfabrik Gesellschaft fur chemische Erzeugnisse mbH & Co. KG

- Dorfketal Chemicals(I)Pvt Ltd

- DOVER CHEMICAL CORPORATION

- Evonik Industries AG

- Infineum International Limited

- Jinzhou Kangtai Lubricant Additives Co. Ltd

- King Industries Inc.

- LANXESS

- Multisol

- RT Vanderbilt Holding Company Inc.

- Shepherd Chemical

- Italmatch Chemicals SpA(The Elco Corporation)

- The Lubrizol Corporation

- Wuxi South Petroleum Additives Co. Ltd

第七章 市场机会与未来趋势

- 高性能润滑油在亚太地区越来越受欢迎

The Lubricant Additives Market is expected to register a CAGR of greater than 3% during the forecast period.

The Covid pandemic had a negative impact on the market. COVID-19-related restrictions led to decreased maintenance requirements from several industries. The major impact was observed in the automotive and construction industry, However, the market started growing steadily, owing to increased automotive and construction activities, since 2021.

Key Highlights

- Over the short term, the stringent environmental regulations regarding emissions, and industrial growth in the Middle East and Africa are major factors driving the growth of the market studied.

- However, extended oil change intervals in machinery and automobiles are a key factor anticipated to restrain the growth of the target industry over the forecast period.

- Nevertheless, the growing popularity of high-performance lubricants in Asia-Pacific is likely to create lucrative growth opportunities for the global market soon.

- Asia-Pacific is estimated to witness healthy growth over the assessment period in the lubricant additives market due to the wide usage of lubricants in end-use application segments, such as automotive, and construction due to their desirable properties.

Lubricant Additives Market Trends

Increasing Demand from Automotive and Other Transportation Industry.

- Automotive and other transportation media, such as aircraft and marine, are the largest markets for lubricants.

- Engine designs have been continually improved to enhance performance, increase efficiency, and meet environmental emission regulations.

- Engine oils, gear oils, transmission oils, greases, and compressor oils are the most widely used lubricants in all kinds of automobiles. Lubricants have a good share in the aftermarket and among OEMs.

- Medium-duty and high-performance lubricants are used extensively in vehicle components, such as gears, transmission systems, and engines, which are subjected to high loads and rapid rubbing.

- The automotive industry has been growing rapidly increasing the usage of lubricants and additives, over the past few years, according to OICA, the total production of vehicles (all types) in the year 2021 was 80,145,988 units and registered a growth of 3% when compared to 77,711,725 units in 2020.

- In North America, the United States also has one of the largest automotive industries globally. According to OICA, the automotive production in 2021 accounted for 91,67,214 units, an increase of 4% in comparison to the production in 2020, which was reported to be 88,22,399 units.

- The strong growth of composites in the aerospace industry, particularly in commercial air transport, is poised to lead to changes in corrosion inhibitors and removal fluids.

- Furthermore, according to the International Air Transport Association (IATA), the global revenue for commercial airlines was valued at USD 373 billion in 2020 and was estimated at USD 472 billion in 2021, registering a growth rate of 26.7% Y-o-Y. Furthermore, the revenue is expected to reach USD 658 billion by 2022.

- Recently, aircraft manufacturers are looking for ways to accelerate production to fill order backlogs. For instance, according to the Boeing Commercial Outlook 2022-2041, the total global deliveries of new airplanes are estimated to be 41,170 by 2041. The global airplane fleet amounted to around 25,900 units as of the year 2019 and the fleet number is likely to reach 47,080 units by 2041.

- All the above factors are expected to drive the market for lubricant additives in the coming years.

China to Dominate the Asia-Pacific Region

- In the Asia-Pacific region, China dominated the regional market share. With growing food, and automotive industrial activities.

- China is the leading manufacturer of the automotive industry, According to, OICA, the country has also produced 26,082,220 units of vehicles in 2021, a 3% growth in comparison to the same period last year.

- The food processing industry is moving toward maturity in the country, witnessing moderate growth. Processed and packaged frozen foods are increasingly becoming popular. While in the beverage industry, the trend for the consumption of healthy, natural, and convenient ready-to-drink smoothies, juices, and yogurts has been emerging.

- China is the leading consumer of metalworking fluids. The growth for metalworking is expected to be driven by the robust growth in construction activities and increasing shipbuilding and aircraft orders in the region.

- The Chinese aircraft and spacecraft industry has depicted significant growth over the years. In China, according to the Boeing Commercial Outlook 2022-2041, around 8,485 new deliveries will be made by 2041 with a market service value of USD 545 billion.

- Based on the aforementioned aspects, China is expected to dominate the Asia-Pacific region in the forecast period.

Lubricant Additives Industry Overview

The global lubricant additives market is partially consolidated in nature, The major players include Evonik Industries AG, Italmatch Chemicals S.p.A (The Elco Corporation), Infineum International Limited, The Lubrizol Corporation, and Afton Chemical Corporation, among others (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Stringent Environmental Regulations Regarding Emissions

- 4.1.2 Industrial Growth in Middle-East and Africa

- 4.2 Restraints

- 4.2.1 Extended Oil Change Intervals in Machinery and Automobiles

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Dispersants and Emulsifiers

- 5.1.2 Viscosity Index Improvers

- 5.1.3 Detergents

- 5.1.4 Corrosion Inhibitors

- 5.1.5 Oxidation Inhibitors

- 5.1.6 Extreme-pressure Additives

- 5.1.7 Friction Modifiers

- 5.1.8 Other Functions

- 5.2 Lubricant Type

- 5.2.1 Engine Oil

- 5.2.2 Transmission and Hydraulic Fluid

- 5.2.3 Metalworking Fluid

- 5.2.4 General Industrial Oil

- 5.2.5 Gear Oil

- 5.2.6 Grease

- 5.2.7 Process Oil

- 5.2.8 Other Lubricant Types

- 5.3 End-user Industry

- 5.3.1 Automotive and Other Transportation

- 5.3.2 Power Generation

- 5.3.3 Heavy Equipment

- 5.3.4 Metallurgy and Metal Working

- 5.3.5 Food and Beverage

- 5.3.6 Other End-users Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Mexico

- 5.4.2.3 Canada

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Russia

- 5.4.3.4 Italy

- 5.4.3.5 France

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Afton Chemical

- 6.4.2 BASF SE

- 6.4.3 BRB International

- 6.4.4 Chevron Corporation

- 6.4.5 Croda International PLC

- 6.4.6 DOG Deutsche Oelfabrik Gesellschaft fur chemische Erzeugnisse mbH & Co. KG

- 6.4.7 Dorfketal Chemicals (I) Pvt Ltd

- 6.4.8 DOVER CHEMICAL CORPORATION

- 6.4.9 Evonik Industries AG

- 6.4.10 Infineum International Limited

- 6.4.11 Jinzhou Kangtai Lubricant Additives Co. Ltd

- 6.4.12 King Industries Inc.

- 6.4.13 LANXESS

- 6.4.14 Multisol

- 6.4.15 RT Vanderbilt Holding Company Inc.

- 6.4.16 Shepherd Chemical

- 6.4.17 Italmatch Chemicals SpA (The Elco Corporation)

- 6.4.18 The Lubrizol Corporation

- 6.4.19 Wuxi South Petroleum Additives Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Popularity of High-performance Lubricants in Asia-Pacific

润滑油添加剂市场-2025年至2030年预测

润滑油添加剂市场-2025年至2030年预测 润滑油添加剂:全球市场份额排名、总销售额和需求预测(2025-2031年)

润滑油添加剂:全球市场份额排名、总销售额和需求预测(2025-2031年) 全球工业润滑油添加剂市场

全球工业润滑油添加剂市场 2025年润滑油添加剂全球市场报告

2025年润滑油添加剂全球市场报告 润滑油添加剂市场,规模,占有率,趋势,产业分析报告:用途,类型,各地区,2025年~2034年的市场预测全球润滑油添加剂市场研究报告 - 产业分析、规模、份额、成长、趋势和预测 2025 年至 2033 年

润滑油添加剂市场,规模,占有率,趋势,产业分析报告:用途,类型,各地区,2025年~2034年的市场预测全球润滑油添加剂市场研究报告 - 产业分析、规模、份额、成长、趋势和预测 2025 年至 2033 年 2025 年至 2033 年润滑油添加剂市场报告(按类型、最终用途、配销通路和地区)

2025 年至 2033 年润滑油添加剂市场报告(按类型、最终用途、配销通路和地区) 润滑油添加剂市场规模、份额、成长分析、按产品、按应用、按地区 - 产业预测,2024-2031 年

润滑油添加剂市场规模、份额、成长分析、按产品、按应用、按地区 - 产业预测,2024-2031 年 润滑脂添加剂市场:按应用、类型、最终用户、配方、功能、添加剂化学、基础油类型 - 2025-2030 年全球预测

润滑脂添加剂市场:按应用、类型、最终用户、配方、功能、添加剂化学、基础油类型 - 2025-2030 年全球预测 全球工业润滑油添加剂市场,2024-2028

全球工业润滑油添加剂市场,2024-2028