|

市场调查报告书

商品编码

1687233

穿戴式惯性感测器:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Wearable Inertial Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

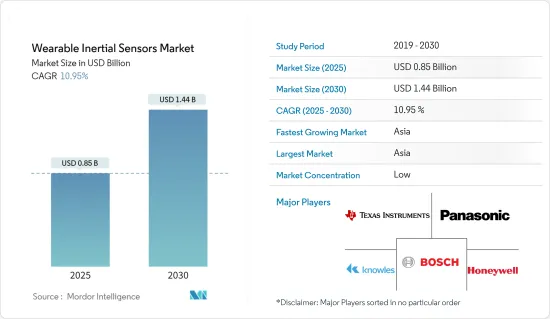

穿戴式惯性感测器市场规模预计在 2025 年为 8.5 亿美元,预计到 2030 年将达到 14.4 亿美元,预测期内(2025-2030 年)的复合年增长率为 10.95%。

穿戴式惯性感测器,也称为惯性测量单元 (IMU),是一种使用一个或多个加速计、陀螺仪和磁力计测量运动相关参数的电子设备。这些感测器体积小、重量轻,个人可以轻鬆佩戴以追踪日常活动中的动作。

主要亮点

- 穿戴式惯性感测器,包括陀螺仪、加速计和地磁感测器,在过去十年中取得了重大发展。由于其性能、小型化和成本下降,可穿戴惯性感测器正在整合到许多日常生活产品中,例如智慧型手机和智慧型手錶。

- 可穿戴惯性感测器具有广泛的应用范围。例如,活动监测和健身追踪在消费市场被广泛采用。基于穿戴式惯性感测器讯号资料的各种医疗应用也正在开发中,包括跌倒风险评估、跌倒检测和帕金森氏症的早期检测。根据帕金森基金会统计,2016 年,全球约有 100 万人患有帕金森氏症。预计到 2030 年这一数字将增加到约 180 万。这些发展正在推动所研究市场的需求。

- 全球都市化的加速显着增加了对先进且美观的消费性电子产品的需求,这些产品可以更好地满足消费者的需求,例如便携性、一机多种功能、紧凑性和时间安排。此外,近年来,由于可支配收入的增加和数位解决方案的普及率不断提高,全球相当一部分千禧世代已成为各种穿戴式装置的早期采用者,包括智慧型手錶。

- 随着苹果、三星和 Fitbit 等大多数穿戴式装置供应商都整合了可提供即时健康更新的先进健康监测功能,穿戴式装置在老年人群中的采用率进一步激增。考虑到对医疗穿戴式装置的需求不断增长,新参与企业不断透过推出创新解决方案在研究产业中展现自己的存在,这也对研究市场的成长产生了积极影响。

- 然而,穿戴式产品的高成本和全部区域严格的监管合规性对研究市场构成了挑战。此外,由于缺乏全球通用标准而导致的互通性问题也有望成为限制调查市场成长的主要因素之一。

可穿戴惯性感测器市场趋势

消费性电子产品将大幅成长

- 惯性穿戴式感测器技术是一种新兴趋势,它将消费性电子产品融入日常活动中,并且可以佩戴在身体的任何部位,适应不断变化的生活方式。消费性电子产业穿戴惯性感测器的趋势受到网路连线等因素的驱动。根据国际电信联盟预测,2023年全球网路用户数将达54亿。

- 感测器(尤其是压力感测器和激活器)的不断进步和小型化也正在扩大消费性电子产业穿戴式惯性感测器市场的范围。随着感测器的生物相容性不断增强,其在医疗保健和健身活动中的应用也显着增长。因此,近年来可穿戴设备的销售量大幅成长。根据思科预测,连网穿戴装置的数量将从 2020 年的 8.35 亿台成长到 2022 年的 11.05 亿台,在医疗保健应用方面前景看好。许多公司正在投资开发先进的微电子机械系统(MEMS)和数位感测器,其尺寸将不断缩小以涵盖广泛的市场应用。

- 电子机械感测器 (MEMS) 和加速计用于电子稳定控制和安全气囊展开。随着技术的进步,惯性测量单元或 IMU(MEMS加速计和 MEMS 陀螺仪的组合)已被开发用于穿戴式设备,并受到日常家用电子电器的影响,例如全球定位系统 (GPS) 和惯性测量单元(由加速计、陀螺仪和地磁仪组成)感测器。因此,健身追踪穿戴式装置完全围绕着这些感测器运转。

- 例如,Nintendo Switch Nintendo Labo Joy-con 具有加速计和陀螺仪的预设感应器。透过将Joy-con与纸板结合,我们创造了一个具有游戏功能的人工智慧可穿戴机器人。这是任天堂透过简化、自订的穿戴式科技创造身临其境型的体验,打破与未来几代人(通常更精通科技)障碍的方式。

- 加速计是穿戴式装置中使用的动作感测器。重力、线性等加速度品牌显示了其感应能力。同时,它的测量能力允许对测量资料进行编程以用于各种目的。例如,跑步者可以获得最大速度输出和加速度。此外,加速计可以像智慧型手錶和腕带一样追踪睡眠模式,从而推动消费性电子领域对穿戴式动作感测器的需求。

亚太地区占市场主导地位

- 由于穿戴式装置和数位技术的普及度不断提高以及消费者群体庞大,预计亚太地区在预测期内将显着成长。考虑到这种前景, OEM也对 IMU(惯性测量单元)和 MEMS 技术的扩展提供了大力支持,以增强新开发产品的采用。此外,由于中国大陆、台湾等地区的崛起,电子产业的发展也促进了市场的成长。

- 穿戴式惯性感测器市场已成为中国最大、成长最快的市场之一。智慧型手錶、健身追踪器、虚拟实境 (VR) 耳机和动态捕捉服都使用穿戴式惯性感测器,即可侦测移动和方向的感测器。中国穿戴式惯性感测器市场的快速成长主要得益于中国对穿戴式科技的接受度不断提高,以及人口健康意识的不断增强。

- 穿戴式科技的日益普及以及对健康和健身测量的需求不断增长,都推动了近年来印度穿戴式惯性感测器市场的大幅成长。加速计、陀螺仪和磁力计等穿戴式惯性感测器对于为穿戴式装置提供运动和方向资讯至关重要,受到国内消费者、运动员和医疗专业人士的欢迎。

- 技术熟练的环境和重视便利和创新的社会正在推动日本可穿戴惯性感测器市场的持续成长。穿戴式惯性感测器应用于医疗保健、体育、娱乐和游戏产业等多个领域。由于人口老化和对健康和福祉的高度关注,日本正在加速使用带有惯性感测器的可穿戴设备进行一般健康监测和增强。

- 由于韩国民众精通科技且对穿戴式科技的高度兴趣,韩国可穿戴惯性感测器市场近年来迅速扩张。智慧型手錶、健身带、虚拟实境耳机和其他穿戴式医疗设备都在一定程度上配备了可穿戴惯性感测器。人们对娱乐、健康和健身的关注度不断提高以及先进技术的采用导致韩国市场对这些产品的需求增加。

- 亚太地区其他地区(包括新加坡、澳洲、马来西亚和其他对亚太地区可穿戴感测器需求敏感的国家)的惯性感测器市场在过去几年中一直稳步增长,这得益于人们对健身和健康的兴趣日益浓厚、人口老龄化日益严重以及技术和医疗保健领域的进步。

穿戴式惯性感测器产业概况

预计对研发、伙伴关係和联盟的投资将成为该市场供应商的策略重点的一部分。此外,对技术创新和透过策略联盟进行市场扩张的投资预计也将成为该市场供应商的关注重点。对于在市场上营运的规模较大的供应商来说,他们获得分销管道和客户群的机会更高。除此之外,供应商越来越注重透过合作和收购来扩大其在市场上的能力。总体而言,竞争对手之间的敌意预计会很高。市场的主要供应商包括德州仪器公司、松下公司、博世感测器公司、楼氏电子和霍尼韦尔国际公司。

2023 年 1 月,Quadric 与 Osram 建立合作伙伴关係,开发整合感测模组,将尖端的 Mira 系列可见光和红外线光 CMOS 感测器与 Quadric 尖端的 Chimera GPNPU 处理器结合。整合的超低功耗模组使穿戴式科技中新型智慧感应成为可能。

2022年12月,Analog Devices, Inc.与奥勒冈健康与科学大学(OHSU)合作开发了智慧型手錶,以应对青少年日益严重的心理健康危机。作为这项全球首创、独一无二的计划合作的一部分,俄勒冈健康与科学大学 (OHSU) 将利用 ADI 的创新技术和产品来应对日益严重的全球精神健康危机,拯救、改善和丰富人们的生活。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- 新冠疫情和宏观经济趋势对该产业的影响

- 技术简介

第五章 市场动态

- 市场驱动因素

- 增强健康意识

- 穿戴健身监测器的需求不断增加

- 科技快速进步

- 市场限制

- 安全问题

- 设备高成本

第六章 市场细分

- 依产品类型

- 智慧型手錶

- 健身带/活动追踪器

- 智慧穿戴

- 运动装备

- 其他的

- 按最终用户

- 卫生保健

- 运动与健身

- 家电

- 娱乐与媒体

- 政府及公共工程

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 亚洲

- 中国

- 印度

- 日本

- 韩国

- 澳洲和纽西兰

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 以色列

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 北美洲

第七章 竞争格局

- 公司简介

- Texas Instruments Incorporated

- Panasonic Corporation

- Bosch Sensortec GmbH

- Knowles Electronics

- Honeywell International Inc.

- TE Connectivity Ltd

- Analog Devices Inc

- General Electric Co.

- AMS osram AG

- STMicroelectronics NV

- Infineon Technologies AG

- NXP Semiconductors NV

- InvenSense, Inc.(TDK Corporation)

第八章投资分析

第九章 市场机会与未来趋势

The Wearable Inertial Sensors Market size is estimated at USD 0.85 billion in 2025, and is expected to reach USD 1.44 billion by 2030, at a CAGR of 10.95% during the forecast period (2025-2030).

Wearable inertial sensors, also known as inertial measurement units (IMUs), are electronic devices designed to measure motion-related parameters using one or more accelerometers, gyroscopes, and magnetometers. These sensors are small, lightweight, and can be effortlessly worn by individuals to track their movements during daily activities.

Key Highlights

- Wearable inertial sensors, including gyroscopes, accelerometers, and magnetometers, have developed considerably during the last decade. Through performance, miniaturization, and cost drop, wearable inertial sensors have been integrated into several daily life products, such as smartphones and smartwatches.

- The fields of application of wearable inertial sensors are numerous. For instance, activity monitoring and fitness tracking are widely employed in the consumer market. Various medical applications based on signal data from wearable inertial sensors have been developed, including fall risk assessment, fall detection, and early identification of Parkinson's disease. According to the Parkinson's Foundation, in 2016, the estimated number of Parkinson's disease patients was around 1 million. This number is predicted to increase to approximately 1.8 million by 2030. Such developments raise the demand for the market studied.

- The rising urbanization across the globe has significantly driven the demand for advanced, aesthetically appealing consumer electronic products that can better serve the consumers' requirements, such as portability, multiple features in one device, and compact and time schedules. Moreover, in recent years, a sizable number of millennials globally has been quick to adopt wearables of different types, including smartwatches, owing to the increased disposable income and the growing penetration of digital solutions.

- Wearables are further witnessing a surge in adoption among the older age population, as most wearable device providers, including Apple, Samsung, and Fitbit, are integrating advanced health-monitoring features that keep them updated about their health status in real time. Considering the growing demand for healthcare wearables, new players are continuously marking their presence in the studied industry by launching innovative solutions, which are also positively impacting the growth of the market studied.

- However, the high cost of wearable products and stringent regulatory compliances across developed regions are challenging the studied market. Furthermore, interoperability concerns owing to the lack of common global standards are also anticipated to remain among the major factors restraining the growth of the studied market.

Wearable Inertial Sensors Market Trends

Consumer Electronics to Witness Significant Growth

- Inertial wearable sensors technology, an emerging trend, integrates consumer electronics into daily activities and addresses the changing lifestyles with the ability to be worn on any part of the body. The trend of wearable inertial sensors in the consumer electronics industry is driven by the factors such as internet connectivity As per ITU, the approximate global internet user count reached 5.4 billion in 2023. and enhanced data exchange capabilities, enabling seamless communication between devices and networks.

- The growing advancement and reduction in the size of sensors, especially pressure sensors and activators, also exp anded the scope of the wearables inertial sensor market in the consumer electronics industry. As sensors become increasingly bio-compatible, their use for healthcare and fitness activities has also significantly increased. This has led to a significant increase in wearable devices sold over the past few years. According to Cisco, the growth in connected wearable devices, from 835 million devices in 2020 to 1.105 billion in 2022, holds great promise, specifically for healthcare applications. Many compa nies are investing in developing advanced Microelectromechanical systems (MEMS) and digital sensors, further decreasing their sizes and covering a wide range of market applications.

- The micro-electro-mechanical sensors (MEMS) and accelerometers are used for electronic stability control and airbag deployment. Inertial Measurement Units or IMU (they are a combination of MEMS Accelerometer and MEMS Gyroscope) have been developed for wearables as technology has advanced and are influenced by the impact of consumer electronic devices being used daily, such as global positioning system (GPS) or inertial measuring unit (composed of accelerometer, gyroscope, and magnetometer) sensors. This has helped fitness-tracking wearables revolve around these sensors exclusively.

- For instance, Nintendo Switch Labo edition Joy-cons possess default sensors in the accelerometer and gyroscope, usually in electronics consumer wearables. Joy-cons and cardboard combine to build artificial wearables, such as robots, to apply to a gaming function. It is usually Nintendo's way of breaking barriers for future generations (who are more involved with technology at younger ages) in immersive experiences with simplified custom wearable tech.

- Accelerometers are motion sensors, used in wearables. Their brand of acceleration, such as gravity and linear, demonstrates their sensing capabilities. Meanwhile, their measuring ability enables the programming of measured data for different purposes. For instance, a user who runs can access their top speed output and acceleration. Further, accelerometers can track sleep patterns like smartwatches and wristbands, thus driving the demand for wearable motion sensors in the consumer electronics segment.

Asia Pacific to Dominate the Market

- The Asia Pacific region is expected to witness notable growth during the forecast period owing to a large consumer base with a growing penetration of wearable devices and digital technologies. Considering the prospects, OEMs are also creating considerable support toward the enlargement of IMUs (inertial measurement units) and MEMS technology further to enhance the penetration of the newly developed products. Furthermore, the evolution of the electronics industry, owing to the emergence of countries such as China, Taiwan, etc., also contributes to the growth of the studied market.

- The market for wearable inertial sensors has become one of the largest and fastest-growing in China. Smartwatches, fitness trackers, virtual reality (VR) headsets, and motion-capture suits all use wearable inertial sensors, which are sensors that can detect motion and direction. The rapid growth of the wearable inertial sensor market in China has been primarily fueled by the country's rising acceptance of wearable technology and its expanding population of health-conscious individuals.

- The growing popularity of wearable technology and rising demand for measuring one's health and fitness have both contributed to the enormous rise of the wearable inertial sensors market in India in recent years. Wearable inertial sensors, such as accelerometers, gyroscopes, and magnetometers, are essential for giving wearable devices information about motion and orientation, which makes them popular for customers, athletes, and healthcare professionals in the nation.

- Japan's technologically proficient environment and a society that values convenience and innovation has propelled consistent growth in the wearable inertial sensor market there. Wearable inertial sensors have several uses in the healthcare, sports, entertainment, and gaming industries, among other fields. The use of wearables with inertial sensors for monitoring and enhancing general well-being has been accelerated by Japan's aging population and a strong focus on health and wellbeing.

- Due to the nation's tech-savvy population and keen interest in wearable technology, the South Korean Wearable Inertial Sensors Market has rapidly expanded in recent years. Smartwatches, fitness bands, virtual reality headsets, and other wearable medical equipment all feature wearable inertial sensors to some extent. Due to the rising emphasis on entertainment, health, and fitness and the adoption of advanced technologies, the demand for these gadgets has increased in the South Korean market.

- The Rest of Asia Pacific's inertial sensor market, which includes nations like Singapore, Australia, Malaysia, and others perceiving demand for wearable sensors in the Rest of Asia Pacific, has been steadily increasing over the past few years, driven by a growing interest in fitness and wellness, a rising aging population, as well as advancements in technology and healthcare.

Wearable Inertial Sensors Industry Overview

Investments in research and development, along with partnerships and alliances, are expected to be some of the strategic focus of vendors operating in the market. In addition to this, investment into technological innovations and market expansions via strategic alliances are expected to be focal points for the vendors in the market. Access to distribution channels and the deep clientele is significantly higher for large vendors operating in the market. In addition to this, vendors tend to focus on expanding their capabilities in the market via partnerships and acquisitions. Overall, the competitive rivalry is expected to be high among the vendors. Some of the major vendors in the market are Texas Instruments Incorporated, Panasonic Corporation, Bosch Sensortec GmbH, Knowles Electronics, Honeywell International Inc., etc.

In January 2023, Quadric and OSRAM established a collaborative partnership to create integrated sensing modules that combine the cutting-edge Mira Family of CMOS sensors for visible and infrared light with Quadric's cutting-edge Chimera GPNPU processors. The integrated ultra-low power modules will make it possible for wearable technology to use new types of smart sensing.

In December 2022 , Analog Devices Inc. collaborated with Oregon Health & Science University (OHSU) to develop a smartwatch that detects vital mental health indicators to help address the rising mental health crisis in teens. As per the collaboration on the first and one-of-a-kind project, OHSU would leverage ADI's innovative technology and products for the burgeoning worldwide mental health crisis to save, improve, and enrich human lives.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter Five Force Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 and Macro Economic Trends on the Industry

- 4.4 Technology Snapshot

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing health awareness

- 5.1.2 Growing Demand for Wearable Fitness Monitors

- 5.1.3 Rapid Technology Advancements

- 5.2 Market Restraints

- 5.2.1 Security concerns

- 5.2.2 High cost of the devices

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Smart Watches

- 6.1.2 Fitness Bands/Activity Tracker

- 6.1.3 Smart Clothing

- 6.1.4 Sports Gear

- 6.1.5 Others

- 6.2 By End-user Type

- 6.2.1 Healthcare

- 6.2.2 Sports and Fitness

- 6.2.3 Consumer electronics

- 6.2.4 Entertainment and Media

- 6.2.5 Government and Public Utilities

- 6.2.6 Others

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 United Kingdom

- 6.3.2.3 France

- 6.3.3 Asia

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.3.4 South Korea

- 6.3.3.5 Australia and New Zealand

- 6.3.4 Middle East and Africa

- 6.3.4.1 United Arab Emirates

- 6.3.4.2 Saudi Arabia

- 6.3.4.3 Israel

- 6.3.5 Latin America

- 6.3.5.1 Brazil

- 6.3.5.2 Argentina

- 6.3.5.3 Mexico

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Texas Instruments Incorporated

- 7.1.2 Panasonic Corporation

- 7.1.3 Bosch Sensortec GmbH

- 7.1.4 Knowles Electronics

- 7.1.5 Honeywell International Inc.

- 7.1.6 TE Connectivity Ltd

- 7.1.7 Analog Devices Inc

- 7.1.8 General Electric Co.

- 7.1.9 AMS osram AG

- 7.1.10 STMicroelectronics NV

- 7.1.11 Infineon Technologies AG

- 7.1.12 NXP Semiconductors NV

- 7.1.13 InvenSense, Inc. (TDK Corporation)