|

市场调查报告书

商品编码

1687239

美国电动车 (EV) 充电:市场占有率分析、行业趋势和成长预测(2025-2030 年)US Electric Vehicle (EV) Charging Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

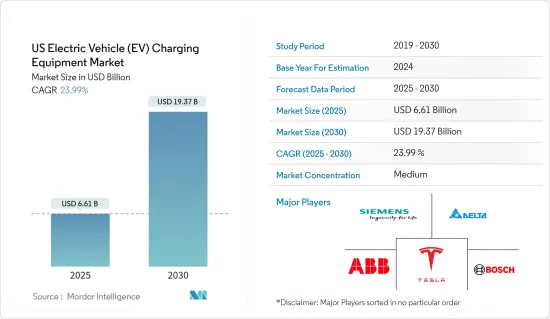

预计 2025 年美国电动车 (EV) 充电器市场规模为 66.1 亿美元,到 2030 年将达到 193.7 亿美元,预测期内(2025-2030 年)的复合年增长率为 23.99%。

关键亮点

- 从中期来看,预计国内电动车普及率不断提高以及电动车基础设施发展等因素将在预测期内推动充电器市场的发展。

- 然而,预计在预测期内,建立充电站的高安装和维护成本将阻碍市场成长。

- 预计在预测期内,对电动车的投资增加和电动车充电设备的技术进步将为美国电动车充电设备市场创造重大机会。

美国电动车充电器市场趋势

提高电动车在该国的普及率

- 电动车因其环保特性和成本效益而越来越受欢迎。然而,电动车车主最关心的问题之一是充电站的可用性。随着电动车使用量的增加,需要更多的充电设施和基础设施来满足需求。

- 随着电动车越来越受欢迎,对充电设备和相关基础设施的需求也日益增长。为了满足需求,政府和企业正在努力在停车场、购物中心和高速公路等公共区域安装充电站。此外,许多电动车车主在家中安装充电站供个人使用。

- 根据国际能源总署 (IEA) 的数据,预计 2022 年美国电动车销量将比 2021 年增长 55%,其中电池电动车 (BEV) 占主导地位。纯电动车销量成长 70%,达到约 80 万辆,这是继 2019-2020 年下滑之后连续第二年实现强劲增长。 PHEV 的销售也有所成长,但仅成长了 15%。

- 根据美国能源局科学办公室的数据,2023 年 12 月美国总合售出 141,055 辆插电式汽车(100,928 辆 BEV 和 40,127 辆 PHEV),比 2022 年 12 月的销量成长 42.4%。此外,2023年12月美国混合动力车销量为117,690辆(乘用车31,825辆,长续航型汽车85,865辆),较2022年12月成长70.3%。 2022年电动车总保有量将达300万辆,较2021年成长36%以上,占全球整体的10%。

- 2023年2月,根据拜登两党基础设施法案,该国宣布计划投资75亿美元用于电动车充电,投资100亿美元用于清洁交通,并投资超过70亿美元用于电动车电池组件、关键矿物和材料。

- 此外,汽车製造商和电池製造商计划在 37 个专用电动车电池製造工厂投资超过 500 亿美元。总设备容量将达到 654 吉瓦时,到 2030 年足以支援每年约 1,000 万辆轻型汽车,并为电动车的生产和销售提供支援。所有这些投资将有助于推动电动车在美国的普及。因此,预测期内对电动车充电设备和基础设施的需求将会上升。

- 因此,预计该国电动车的普及和投资不断增加将继续推动对电动车充电设备的需求,在预测期内仍将是一个有前景的市场。

电池电动车占据市场主导地位。

- 电池电动车(BEV)通常也称为配备马达的电动车。该车辆使用大型牵引电池组为马达提供动力。电动车需要插入墙上插座或称为电动车供电设备 (EVSE) 的充电设备。

- BEV 是全电动汽车,通常不含内燃机 (ICE)、燃料箱或排气管。推进力完全依靠电力。车辆的能量来自电池组,由电网充电。 BEV 是零排放汽车,不会产生传统汽油动力汽车产生的有害废气排放或空气污染风险。

- 电池电动车 (BEV) 在美国的普及正在加速,并正在改变汽车产业。在技术进步、政府支持和日益增强的环保意识的推动下,纯电动车已成为应对气候变迁挑战和减少对石化燃料依赖的有希望的解决方案。

- 近年来,美国电动车的普及率显着增加。电池技术的改进、更长的行驶里程以及充电基础设施的普及有助于克服最初的进入障碍。特斯拉、雪佛兰、日产和福特等汽车製造商透过提供价格实惠、吸引广大消费者的车型,在推广纯电动车方面发挥了重要作用。

- 2022年,美国将有99万辆新电动车註册,其中约80%将是纯电动车。根据国际能源总署 (IEA) 的数据,美国电池电动车 (BEV) 销量与 2021 年相比成长了 40%。

- 根据美国能源局的数据,公共可用的电动车充电站(1 级、2 级和直流快速)数量将从 2022 年的 143,729 个增加到 2023 年的 175,547 个。在 2023 年可用的 175,547 个充电站中,约 137,795 个为慢速充电站,其余 37,752 个为快速充电站。近年来,日本公共快速充电站的比例大幅增加。预计预测期内同样的趋势仍将持续。

- 随着科技的不断发展,美国电动车的未来前景光明。汽车製造商和美国政府正在大力投资研发,以提高电池效率、降低成本并提高整体车辆性能。

- 例如,2022 年第三季度,该国在电动车和电池製造方面投资约 2,100 亿美元。特斯拉预计将加大投资,在2022年至2024年期间每年在美国和德国投资60亿至80亿美元。此外,汽车製造商和电池製造商计划在全国投资540亿美元建设37个电动车电池製造工厂。预计到 2030 年,这些工厂每年将生产 654 吉瓦时 (GWh) 的电动车电池容量。这种情况预计将对纯电动车製造业产生正面影响。

- 此外,自动驾驶技术和Vehicle-to-Grid整合的出现进一步增加了纯电动车彻底改变交通运输产业的潜力。这增加了对电动车充电设备的需求。

美国电动车充电产业概况

美国电动车充电器市场减少了一半。市场的主要企业(不分先后顺序)包括 ABB 有限公司、罗伯特博世有限公司、台达电子股份有限公司、西门子股份公司和特斯拉公司。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究范围

- 市场定义

- 调查前提

第二章执行摘要

第三章调查方法

第四章 市场概述

- 介绍

- 2029 年市场规模与需求预测

- 近期趋势和发展

- 政府法规和政策

- 市场动态

- 驱动程式

- 电动车普及及相关投资增加

- 政府支持政策和倡议

- 限制因素

- 安装电动车充电站的高成本

- 驱动程式

- 供应链分析

- PESTLE分析

第五章市场区隔

- 汽车模型

- 纯电动车(BEV)

- 插电式混合动力汽车(PHEV)

- 混合动力电动车(HEV)

- 应用

- 家庭充电

- 职场充电

- 公共充电

- 充电类型

- 交流充电(1 级和 2 级)

- 直流充电

第六章 竞争格局

- 併购、合资、合作与协议

- 主要企业策略

- 公司简介

- ABB Ltd.

- Robert Bosch GmbH

- ChargePoint Inc.

- Enphase Energy, Inc.

- Delta Electronics Inc.

- Powercharge

- Siemens AG

- Tesla Inc.

- KOSTAL Automobil Elektrik GmbH & Co. KG.

- Webasto SE

- 市场排名分析

第七章 市场机会与未来趋势

- 电动车充电技术进步

简介目录

Product Code: 56960

The US Electric Vehicle Charging Equipment Market size is estimated at USD 6.61 billion in 2025, and is expected to reach USD 19.37 billion by 2030, at a CAGR of 23.99% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors like the growing adoption of electric vehicles in the country and the development of electric vehicle infrastructure are expected to drive the charging equipment market during the forecast period.

- On the other hand, high installation costs associated with setting up charging stations and maintenance costs are expected to hinder the market's growth during the forecast period.

- Nevertheless, increasing investments in EVs and technological advancements in EV charging Equipment are expected to provide significant opportunities for the US electric vehicle (EV) charging equipment market during the forecast period.

US Electric Vehicle (EV) Charging Equipment Market Trends

Increasing Adoption of Electric Vehicles in the Country

- Electric vehicles (EVs) became increasingly popular due to their eco-friendly nature and cost-effective benefits. However, one of the main concerns for EV owners is the availability of charging stations. As the usage of electric vehicles increases, more charging equipment and infrastructures are required to fulfill the need.

- As the adoption of electric vehicles increases, the need for charging devices and relevant infrastructure is expanding. To meet the demand, the government and companies work on installing more charging stations in public areas such as parking lots, malls, and highways. Many electric vehicle owners also install charging stations in their homes for personal use.

- According to the International Energy Agency (IEA), in the United States, electric car sales increased by 55% in 2022 relative to 2021, led by battery electric vehicles (BEV). Sales of BEVs increased by 70%, reaching nearly 800,000 and confirming a second consecutive year of solid growth after the 2019-2020 dip. Sales of PHEVs also grew, albeit by only 15%.

- According to the United States Department of Energy Office of Science, a total of 141,055 plug-in vehicles (100,928 BEVs and 40,127 PHEVs) were sold during December 2023 in the United States, up 42.4% from the sales in December 2022. Also, In December 2023, 117,690 HEVs (31,825 cars and 85,865 LTs) were sold in the United States, up 70.3% from the sales in December 2022. The total stock of electric cars stood at 3 million in 2022, recording more than a 36% increase compared to 2021, accounting for 10% of the global total.

- In February 2023, Under Biden's Bipartisan Infrastructure Law, the country announced its plan to invest USD 7.5 billion in electric vehicle charging, USD 10 billion in clean transportation, and over USD 7 billion in electric vehicle (EV) battery components, critical minerals, and materials.

- Furthermore, the automakers and battery makers plan to spend over USD 50 billion across 37 dedicated EV battery manufacturing facilities. At total capacity, the facilities could produce 654 GWh in capacity, which is enough to support about 10 million light-duty vehicles annually by 2030 to support their electric vehicle manufacturing and sales. All these investments are likely to boost the adoption of EVs across the United States. It, in turn, is driving the need for EV charging devices and infrastructures over the forecast period.

- Hence, the increasing adoption of electric vehicles (EVs) and investments in the country are expected to continue accelerating the demand for EV charging equipment and hold a promising market over the forecast period.

Battery Electric Vehicles to Dominate the market.

- Battery electric vehicles (BEVs) are also commonly referred to as electric vehicles with an electric motor. The vehicle uses a large traction battery pack to power the electric motor. The EV must be plugged into a wall outlet or charging equipment called electric vehicle supply equipment (EVSE).

- BEVs are fully electric vehicles and typically do not include an internal combustion engine (ICE), fuel tank, or exhaust pipe. They rely only on electricity for propulsion. The vehicle's energy comes from the battery pack, which is recharged from the grid. BEVs are zero-emission vehicles, as they do not generate any harmful tailpipe emissions or air pollution hazards caused by traditional gasoline-powered vehicles.

- The United States is transforming the automotive industry as battery electric vehicles (BEVs) gain momentum and popularity. With technological advancements, government support, and increasing environmental concerns, BEVs emerged as a promising solution to address the challenges of climate change and reduce reliance on fossil fuels.

- In recent years, the adoption of battery-electric vehicles in the United States grew significantly. Improved battery technology, extended driving ranges, and a surge in charging infrastructure helped overcome the initial entry barriers. Automakers like Tesla, Chevrolet, Nissan, and Ford played instrumental roles in popularizing BEVs, offering affordable models that appeal to a broader range of consumers.

- In 2022, the United States registered 990,000 new electric cars, of which about 80% were BEVs, and witnessed a rise of 70% compared to 2021. According to the International Energy Agency (IEA), battery electric vehicle (BEV) sales increased by 40% in the United States relative to 2021.

- According to the United States Department of Energy, the number of publicly available electric vehicle charging points (Level 1, Level 2, and DC Fast) grew from 143,729 in 2022 to 175,547 in 2023. Of the 175,547 charging points in 2023, around 137,795 were slow charging points, and the rest 37,752 were fast charging points. The share of publicly available fast charging points witnessed significant growth in the country in recent years. It is expected to continue the same trend during the forecast period.

- As technology continues to evolve, the future of battery-electric vehicles in the United States looks promising. Automakers, along with the United States government, are investing heavily in research and development to improve battery efficiency, reduce costs, and enhance overall vehicle performance.

- For instance, in Q3 2022, the country invested nearly USD 210 billion in EV and battery manufacturing. The investment is expected to increase, with Tesla including USD 6-8 billion annually in the United States and Germany between 2022 and 2024. Further, automakers and battery makers also planned to spend USD 54 billion across 37 EV battery manufacturing facilities across the country. These facilities are expected to produce 654 gigawatt hours (GWh) of EV battery capacity annually by 2030. Such a scenario is expected with a positive impact on the BEV manufacturing industry.

- Moreover, the emergence of autonomous driving technology and vehicle-to-grid integration further adds to the potential of BEVs to revolutionize the transportation sector. It is thereby driving the demand for charging equipment for battery electric vehicles.

US Electric Vehicle (EV) Charging Equipment Industry Overview

The US electric vehicle (EV) charging equipment market is semi-fragmented. Some of the key players in the market (not in any particular order) include ABB Ltd, Robert Bosch GmbH, Delta Electronics Inc., Siemens AG, and Tesla Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Adoption of Electric Vehicles and Related Investments

- 4.5.1.2 Supportive Government Policies And Initiatives

- 4.5.2 Restraints

- 4.5.2.1 High Cost Of Setting Up Ev Charging Stations

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 PESTLE Analysis

5 MARKET SEGMENTATION

- 5.1 Vehicle Type

- 5.1.1 Battery Electric Vehicle (BEV)

- 5.1.2 Plug-in Hybrid Electric Vehicle (PHEV)

- 5.1.3 Hybrid Electric Vehicle (HEV)

- 5.2 Application

- 5.2.1 Home Charging

- 5.2.2 Workplace Charging

- 5.2.3 Public Charging

- 5.3 Charging Type

- 5.3.1 AC Charging (Level 1 and Level 2)

- 5.3.2 DC Charging

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 ABB Ltd.

- 6.3.2 Robert Bosch GmbH

- 6.3.3 ChargePoint Inc.

- 6.3.4 Enphase Energy, Inc.

- 6.3.5 Delta Electronics Inc.

- 6.3.6 Powercharge

- 6.3.7 Siemens AG

- 6.3.8 Tesla Inc.

- 6.3.9 KOSTAL Automobil Elektrik GmbH & Co. KG.

- 6.3.10 Webasto SE

- 6.4 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements in the EV Charging Equipment

02-2729-4219

+886-2-2729-4219

下一代电动车充电网路市场预测:至2034年-全球分析(按充电器类型、输出功率、连接器类型、车辆型号、安装类型、连接方式、应用、最终用户和地区划分)

下一代电动车充电网路市场预测:至2034年-全球分析(按充电器类型、输出功率、连接器类型、车辆型号、安装类型、连接方式、应用、最终用户和地区划分) 电动车充电站市场(含广告看板):依广告形式、充电器类型、安装位置、网路类型和最终用户划分,全球预测,2026-2032年电动车充电主动滤波器按充电站类型、滤波器配置、额定输出功率和最终用户划分,全球预测,2026-2032年电动车充电滤波器市场按滤波器类型、滤波器拓扑结构、额定电流、应用和最终用户划分-全球预测,2026-2032年电动车智慧充电控制器市场:按充电等级、模式、通讯技术、交付方式、车辆类型、应用和最终用户划分-2026-2032年全球预测

电动车充电站市场(含广告看板):依广告形式、充电器类型、安装位置、网路类型和最终用户划分,全球预测,2026-2032年电动车充电主动滤波器按充电站类型、滤波器配置、额定输出功率和最终用户划分,全球预测,2026-2032年电动车充电滤波器市场按滤波器类型、滤波器拓扑结构、额定电流、应用和最终用户划分-全球预测,2026-2032年电动车智慧充电控制器市场:按充电等级、模式、通讯技术、交付方式、车辆类型、应用和最终用户划分-2026-2032年全球预测 日本电动车充电设备市场占有率分析、产业趋势及统计、成长预测(2026-2031)

日本电动车充电设备市场占有率分析、产业趋势及统计、成长预测(2026-2031) 日本电动车充电设备市场规模、份额、趋势及预测(按充电站、最终用途和地区划分,2026-2034年)电动汽车家用充电套件市场预测至2032年:按充电器类型、连接器类型、车辆类型、安装类型、分销管道、应用和地区分類的全球分析

日本电动车充电设备市场规模、份额、趋势及预测(按充电站、最终用途和地区划分,2026-2034年)电动汽车家用充电套件市场预测至2032年:按充电器类型、连接器类型、车辆类型、安装类型、分销管道、应用和地区分類的全球分析 智慧电动汽车充电网路市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)超快速电动车充电(350kW+)系统市场机会、成长驱动因素、产业趋势分析及2025-2034年预测

智慧电动汽车充电网路市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)超快速电动车充电(350kW+)系统市场机会、成长驱动因素、产业趋势分析及2025-2034年预测

▼