|

市场调查报告书

商品编码

1687272

电源管理积体电路(PMIC) -市场占有率分析、产业趋势与统计、成长预测(2025-2030)Power Management Integrated Circuit (PMIC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

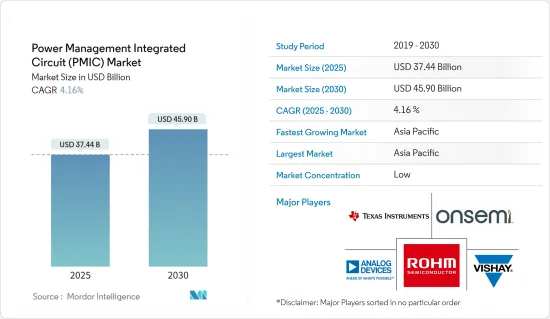

电源管理积体电路市场规模预计在 2025 年为 374.4 亿美元,预计到 2030 年将达到 459 亿美元,预测期内(2025-2030 年)的复合年增长率为 4.16%。

这种增长很大程度上是由于每个电子元件都需要控制和供电,无论所需电压或最终应用如何。随着主要企业寻求透过开发新製程、封装和电路设计技术来突破功率界限以提供适合应用的设备,市场正在获得发展动力。电源管理IC在提高功率密度、延长电池寿命、减少电磁干扰、维护电源和讯号完整性以及维护高压条件下的安全性方面的效用越来越大。

关键亮点

- 从功率密度因素开始,随着功率需求的增加,基板面积和高度正在成为限制因素。为了使他们的产品与众不同,电源设计人员在他们的应用中加入更多的电路,同时提高效率并改善热性能。此外,在电池供电系统中,需要在空载或轻载条件下实现高效率,这为调节输出同时严格保持超低电流的电源解决方案铺平了道路。

- 电磁干扰 (EMI) 是电子系统中越来越重要的要求,尤其是在汽车和工业等新应用中。因此,开发低 EMI IC 可以显着缩短开发週期,同时减少基板面积和解决方案成本。监控、调节和处理电力链讯号的能力对于最大限度地提高系统效能和可靠性至关重要。高度精密系统需要低噪音、精确的参考和低噪音、低涟波的电源轨。因此,迫切需要先进的电源管理 IC 来提高精度并最大限度地减少失真。

- 电源管理积体电路是电子设备中的关键元件,旨在实现电源管理效率。然而,在PMIC设计过程中,设计人员经常面临从功率损耗到温度控管的多重挑战,这些挑战会影响电子设备的效率和效能。预计这些因素将阻碍市场成长。

- 此外,汽车领域对电源管理IC也前景看好。这是由 ADAS 的引入和汽车电气化推动的,并得到了蓬勃发展的地区和新兴国家的大力支持。

- 此外,电动车已成为道路运输脱碳的关键技术,道路运输占全球能源相关排放的 15% 以上。近年来,电动车销量呈指数级增长,续航里程不断增加,车型种类不断丰富,性能不断提升。乘用电动车越来越受欢迎,国际能源总署预测,2023 年销售的新车中 18% 将是电动车。欧洲、中国和美国仍然是主要的电动车市场。

电源管理积体电路(PMIC)市场趋势

汽车作为终端用户产业正在快速成长

- 汽车是本研究市场中主要的终端使用者之一。汽车及其製造业的进步也推动了对更小、更节能的设备的需求。汽车产量的增加和汽车先进功能的增加是推动汽车领域对电源管理 IC 需求的关键因素。

- 汽车应用的电源需要高可靠性、高效率和各种安全功能。对宽电压输入、多相电源、汽车安全完整性等级 (ASIL) 支援以及高功率系统晶片(SoC) 全系统能源的需求不断增长,推动了汽车领域对电源管理积体电路 (PMIC) 的需求。高级驾驶辅助系统 (ADAS),包括摄影机和雷达技术、资讯娱乐和丛集系统、主动安全功能、车身电子和照明控制、电动、混合动力和动力传动系统传动系统等,是 PMIC 的一些主要应用领域。

- 考虑到汽车行业日益增长的需求,供应商定期推出创新解决方案,以支持所研究市场的成长。例如,2022年3月,运动控制和节能係统感测和电源解决方案供应商Allegro MicroSystems Inc.出货了第30亿个马达驱动器积体电路(IC),展现了其运动控制业务的实力。

- 近年来,随着全球环境问题日益严重,消费者意识不断增强,政府监管不断加强,电动车产业经历了显着增长。例如,根据国际能源总署(IEA)的预测,2022年全球道路上将有约2,590万辆电动车。同年,纯电动车在插电式电动车的比例约为69.5%。

- 此外,根据国际能源总署的预测,2023 年插电式电动车 (PEV) 的销量将达到 1,370 万辆左右。随着对插电式轻型电动车的需求持续成长,研究市场在预测期内可能会出现更高的需求。

亚太地区占市场主导地位

- 由于消费性电子产品销售不断增长、政府推动电子产品製造业发展的倡议、多家公司的存在以及对其他行业的投资,亚太市场预计将扩大。

- 由于主要半导体製造商的存在、消费性电子市场的快速扩张以及智慧型设备的日益普及,亚太地区成为电源管理 IC 市场的焦点。区域市场的主要企业包括中国、印度、韩国和日本,这些国家在半导体产业取得了重大进展。由于先进电子设备的普及,该地区占有相当大的市场占有率。

- 此外,5G 网路的引入和该地区通讯领域投资的增加预计将推动 PMIC 市场的发展。根据台湾网路资讯中心的调查,19% 的台湾受访者将在 2022 年使用 5G,较 2020 年的 2% 大幅成长。如此快速的普及预计将推动该地区通讯业的蓬勃发展,从而大幅增加对强大晶片的需求以及对 OSTA 服务的需求。

- 根据 GSMA 预测,到 2030 年底,亚太地区的 5G 连线数预计将达到约 14 亿。这一增长预计将受到 5G 设备平均成本下降、许多国家网路快速扩张以及主要政府的共同努力的推动。此外,5G领域的进步也促进了市场扩张。根据韩国科学、资讯通信技术和通讯部报告,截至2023年2月,韩国5G用户数为2,913万,较2021年2月的1,366万大幅成长113%。

- 此外,印度、中国和日本等国家汽车产业的崛起预计将进一步刺激市场需求。例如,中国汽车产业正在快速扩张,在全球汽车产业的地位日益重要。中国是率先采用电动车的国家之一,电动车正变得越来越受欢迎。 2022年,中国乘用车市场资讯联席会报告称,由于政府奖励和油气价格上涨导致消费者放弃耗油车型,中国电动车和插电式汽车销量为567万辆。电动汽车产业预计将推动对汽车电源管理解决方案的快速需求,从而推动对 PMIC 设备的需求。

电源管理积体电路(PMIC)市场概况

电源管理积体电路 (PMIC) 市场高度分散,主要企业包括德州仪器公司、安森美半导体元件有限责任公司 (onsemi)、ADI 公司、ROHM 和 Vishay Intertechnology Inc.。市场主要企业正在积极推行各种策略,包括联盟和收购,以加强产品系列建立可持续的竞争优势。

2023 年 4 月,德州仪器 (TI) 发布了有关其最新产品 SimpleLink 系列 Wi-Fi 6伴同性积体电路 (IC) 的重要公告。这些 IC 专为在高密度或高温环境下运作的应用而设计,可承受高达 1050°C 的温度。 TI 新 CC33xx 系列的初始成员包括仅支援 Wi-Fi 6 连接的选项,以及支援 Wi-Fi 6 和低功耗蓝牙 5.3 连接的选项,全部整合到单一 IC 中。这种创新解决方案在与微控制器单元 (MCU) 或处理器连接时,可透过可靠的射频效能实现安全的物联网连接,特别是在电网基础设施、医疗和楼宇自动化等工业领域。

2023 年 5 月,Semiconductor Components LLC(Onsemi)宣布与 Vitseco Technologies 建立战略合作伙伴关係,旨在加强其 SiC(碳化硅)技术能力。两家公司签署了一份为期10年、价值19亿美元的长期供应协议,主要集中在SiC产品。根据协议,Vitseco 将向 Onsemi 投资 2.5 亿美元,用于购买专门用于 SiC 晶圆製造、晶锭生长和外延製程的新设备。这项策略性倡议旨在确保未来稳定、强大的碳化硅生产能力,使两家公司能够满足不断增长的市场需求。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业价值链/供应链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

- 宏观趋势如何影响市场

第五章市场动态

- 市场驱动因素

- 节能电池供电设备的需求不断增加

- 汽车领域的电气化趋势

- 市场限制

- 高功率应用中的设计复杂性与效能限制

第六章市场区隔

- 按产品

- 电压稳压器

- 马达控制IC

- 电池管理IC

- 多通道PMIC

- 更多产品

- 按最终用户

- 汽车

- 家用电子电器

- 工业的

- 通讯设备

- 计算

- 其他的

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

第七章竞争格局

- 公司简介

- Texas Instruments Incorporated

- Semiconductor Components Industries LLC(Onsemi)

- Analog Devices Inc.

- ROHM Co. Ltd

- Vishay Intertechnology Inc.

- NXP Semiconductors NV

- Infineon Technologies AG

- Qualcomm Incorporated

- Renesas Electronic Corporation

- STMicroelectronics NV

第八章投资分析

第九章:市场的未来

The Power Management Integrated Circuit Market size is estimated at USD 37.44 billion in 2025, and is expected to reach USD 45.90 billion by 2030, at a CAGR of 4.16% during the forecast period (2025-2030).

This growth is largely owing to the fact that every electronic component needs to be controlled and powered, irrespective of the required voltage or the final application. The market has been gaining momentum as major players have been looking toward pushing the limits of power by developing new processes, packaging, and circuit design technologies for delivering suitable devices as per the application. Power management IC has been gaining usability in enhancing power density, extending battery life, reducing electromagnetic interference, preserving power and signal integrity, and maintaining safety in the presence of high voltages.

Key Highlights

- Starting with the power density factor, the board area and height are becoming limiting factors as power demands increase. Power designers are squeezing more circuitry into their applications to differentiate their products while also increasing efficiency and enhancing thermal performance. Moreover, in battery-operated systems, the need to achieve high efficiency at no or light-load conditions has been paving the way for power solutions to regulate the output while maintaining ultra-low supply current tightly.

- Electromagnetic interference (EMI) is a key requirement of increasing importance in electronic systems, especially in new applications such as automotive and industrial. Thus, designing for low EMI IC can save significant development cycle times while also reducing board area and solution cost. The ability to monitor, condition, and process signals in the power chain is critical in order to maximize system performance and reliability. High-precision systems require accurate low-noise references, as well as supply rails with low noise and ripple. Thus, advanced power management ICs are significantly required for increased accuracy and minimum distortion.

- Power management integrated circuits are crucial components in electronic devices and are designed to achieve efficiency in power management. However, in the PMIC design process, designers often face multiple challenges ranging from power losses to thermal management, affecting the electronic device's efficiency and performance. Such factors are expected to hinder the growth of the market.

- Furthermore, the automotive segment is also promising for the power management IC, driven by the introduction of ADAS as well as the electrification of vehicles, which are largely gaining support from strong regional and developing countries.

- In addition to this, electric vehicles have evolved as the key technology to decarbonize road transport, a sector that accounts for over 15% of global energy-related emissions. Recent years have observed exponential growth in the sale of EVs, together with improved range, wider model availability, and increased performance. Passenger electric cars are gaining popularity, and IEA estimates that 18% of new cars sold in 2023 will be electric. Europe, China, and the United States remain the leading electric vehicle markets.

Power Management Integrated Circuit (PMIC) Market Trends

Automotive to be the Fastest Growing End-user Industry

- The automotive is one of the significant end users of the market studied. The advancement in automotive and its manufacturing is also driving the need for compact, power-efficient devices. The growing automotive production and the addition of advanced features in the automotive are some of the major factors driving the demand for power management ICs in the automotive sector.

- Power in automotive applications demands high reliability, efficiency, and different safety functionality. The growing need for broad voltage input or multiphase power, support for automotive safety integrity level (ASIL), or full-system energy for high-powered system-on-chips (SoCs) is fueling the demand for power management integrated circuits (PMICs) in the automotive sector. Advanced driver assistance systems (ADAS) encompassing camera and radar technologies, infotainment and cluster systems, active safety features, body electronics and lighting control, as well as electric, hybrid, and powertrain systems, represent some of the significant scopes for PMIC applications.

- Considering the growing demand from the automobile industry, vendors are launching innovative solutions regularly, which is supporting the growth of the market studied. For instance, in March 2022, Allegro MicroSystems Inc., a provider of motion control and energy-efficient systems sensing and power solutions, shipped the three billionth motor driver integrated circuit (IC), demonstrating the strength of its motion control business.

- In recent years, the electric vehicle industry has witnessed remarkable growth, driven by growing consumer awareness and supporting government regulations as global environmental concerns rise. For instance, according to the International Energy Agency (IEA), there were approximately 25.9 million electric vehicles worldwide in 2022. All-electric vehicles accounted for about 69.5% of plug-in electric vehicles that year.

- Furthermore, according to IEA, It is estimated that 2023 saw plug-in electric light vehicle (PEV) sales of around 13.7 million units. As the demand for EVs in the plug-in light vehicles continues to grow, the studied market will witness a higher demand during the forecast period.

Asia-Pacific to Dominate the Market

- The market in Asia-Pacific is expected to increase owing to rising consumer electronics sales, government initiatives to boost electronics manufacturing, the presence of several companies, and investments in other industries.

- The Asia-Pacific region has gained prominence in the Power Management IC Market, owing to the presence of major semiconductor manufacturers, the rapid expansion of consumer electronics markets, and the growing adoption of smart devices. Key players in the region's market include China, India, South Korea, and Japan, which have made significant strides in the semiconductor industry. The region commands a substantial market share due to the widespread adoption of advanced electronic devices.

- Moreover, the region's adoption of the 5G network and the rising investments in the telecom sector are expected to drive the market for PMICs. According to a survey conducted by the Taiwan Network Information Center, in 2022, 19% of Taiwanese respondents have availed themselves of 5G, a significant increase from 2% in 2020. This rapid adoption is anticipated to fuel the telecom industry in the region, resulting in a substantial demand for potent chips, thereby necessitating OSTA services.

- As per the GSMA, the Asia-Pacific region is projected to witness approximately 1.4 billion 5G connections by the conclusion of 2030. This growth is expected to be propelled by a decline in the average cost of 5G devices, swift network expansion in numerous nations, and concerted efforts by prominent governments. Furthermore, the 5G domain advancements have also contributed to market expansion. The Ministry of Science and ICT has reported that as of February 2023, the nation has 29.13 million 5G subscribers, indicating a 113% surge compared to 13.66 million 5G subscribers in February 2021.

- Moreover, the rising region's automotive sector across various countries like India, China, Japan, and others is expected to drive the demand for the market further. For instance, The automotive industry in China is expanding rapidly, and the region is assuming a more prominent position in the global auto industry. China is among the leading nations in adopting electric vehicles, which are gaining popularity. In 2022, the China Passenger Car Association reported that 5.67 million EVs and plug-ins were sold in China as consumers shifted from gas-guzzling models due to government incentives and elevated oil prices. The EV industry is expected to drive a rapid increase in demand for car power management solutions, thereby driving the need for PMIC devices.

Power Management Integrated Circuit (PMIC) Market Overview

The power management integrated circuit (IC) market is characterized by a high degree of fragmentation, featuring prominent players like Texas Instruments Incorporated, Semiconductor Components LLC (onsemi), Analog Devices Inc., ROHM Co. Ltd, and Vishay Intertechnology Inc. These key players in the market are actively pursuing various strategies, including partnerships and acquisitions, to enhance their product portfolios and establish sustainable competitive advantages.

In April 2023, Texas Instruments made a significant announcement regarding its latest offering, the SimpleLink family of Wi-Fi 6 companion integrated circuits (ICs). These ICs are designed to cater to applications operating in high-density or high-temperature environments, with the capability to withstand temperatures up to 1050C. The initial products within TI's new CC33xx family encompass options for Wi-Fi 6 connectivity alone, as well as Wi-Fi 6 paired with Bluetooth Low Energy 5.3 connectivity, all integrated into a single IC. This innovative solution facilitates a secure IoT connection with dependable RF performance when interfacing with a microcontroller unit (MCU) or processor, particularly in industrial sectors like grid infrastructure, medical, and building automation.

In May 2023, Semiconductor Components LLC (onsemi) announced a strategic partnership with Vitseco Technologies aimed at bolstering SiC (Silicon Carbide) technology capacity expansion. The two companies have entered into a substantial 10-year long-term supply agreement valued at USD 1.9 billion, primarily centered on SiC products. Under the terms of this agreement, Vitseco will inject USD 250 million in investment to Onsemi for the acquisition of new equipment dedicated to SiC wafer production, boule growth, and epitaxy processes. This strategic move is intended to secure a stable and robust SiC capacity for the future, ensuring both companies are well-positioned to meet growing market demands.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Value Chain/Supply Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitutes

- 4.4 Impact of Macro Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand for Energy-efficient Battery-powered Devices

- 5.1.2 Electrification Trend in the Automotive Sector

- 5.2 Market Restraints

- 5.2.1 Design Complexity and Performance Limitations in High-power Applications

6 MARKET SEGMENTATION

- 6.1 By Product

- 6.1.1 Voltage Regulators

- 6.1.2 Motor Control ICs

- 6.1.3 Battery Management ICs

- 6.1.4 Multi-channel PMIC

- 6.1.5 Other Products

- 6.2 By End-User

- 6.2.1 Automotive

- 6.2.2 Consumer Electronics

- 6.2.3 Industrial

- 6.2.4 Communication

- 6.2.5 Computing

- 6.2.6 Other End-Users

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Texas Instruments Incorporated

- 7.1.2 Semiconductor Components Industries LLC (Onsemi)

- 7.1.3 Analog Devices Inc.

- 7.1.4 ROHM Co. Ltd

- 7.1.5 Vishay Intertechnology Inc.

- 7.1.6 NXP Semiconductors N.V.

- 7.1.7 Infineon Technologies AG

- 7.1.8 Qualcomm Incorporated

- 7.1.9 Renesas Electronic Corporation

- 7.1.10 STMicroelectronics N.V.