|

市场调查报告书

商品编码

1687321

离子交换树脂:市场占有率分析、产业趋势与统计、成长预测(2025-2030)Ion Exchange Resin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

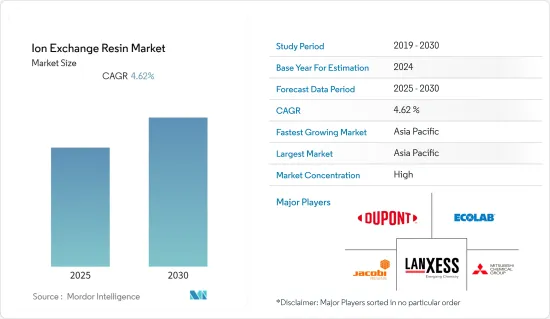

预计预测期内离子交换树脂市场将以 4.62% 的复合年增长率成长。

市场受到了 COVID-19 的负面影响。疫情导致许多国家采取封锁措施,以遏止病毒传播。许多企业和工厂关闭,扰乱了全球供应链,影响了全球的生产、交货时间和产品销售。目前,市场正在从新冠疫情中復苏并经历显着成长。

主要亮点

- 中期推动市场成长的主要因素是水处理行业的成长以及电子和製药行业对超纯水的需求不断增长。

- 然而,离子交换树脂的细菌污染可能会阻碍市场成长。

- 预计燃料电池需求的不断增长将为市场提供成长机会。

- 亚太地区占据市场主导地位,其中中国和印度是最大的消费国。此外,预计亚太地区在预测期内将实现最快的成长率。

离子交换树脂市场趋势

水处理领域正在推动市场

- 离子交换树脂通常用作水处理剂,去除水中的微量金属离子、有机化合物和污染物。

- 由于对淡水资源的强劲需求,水处理应用近年来有所增加。在污水处理厂中,水循环利用是一个多步骤的过程。离子交换处理流程通常用于软化水或海水淡化。它也用于在脱碱、去离子和消毒等过程中去除水中的其他物质。它们适用于工业和市政应用。

- 近年来,离子交换树脂在饮用水中的应用越来越多。专用树脂用于处理各种污染物,包括高氯酸盐和铀。

- 还有许多树脂专门用于去除硝酸盐和高氯酸盐,例如强碱/强阴离子树脂。还有树脂珠可用于软化水。

- 树脂材料的交换容量是有限的。随着使用时间的延长,各个替换部位将会变得满满的。当离子交换不再可行时,必须重新充电或再生树脂以使其恢復到原始状态。用于此目的的物质包括氯化钠、盐酸、硫酸和氢氧化钠。

- 废再生剂是该过程剩余的主要物质。这包括所有去除的离子以及总溶解固态含量高的过量再生剂。该再生剂可以在市政污水处理厂进行处理,但排放可能需要监测。

- 离子交换在水处理中的有效性可能会受到矿物结垢、表面堵塞和其他导致树脂污染的问题的限制。过滤或添加化学物质等预处理步骤有助于减少或防止这些问题。

- 德国拥有欧洲最大的工业污水处理市场,约有3,000座处理厂。每年有超过9.2亿立方公尺的工业污水在国内处理后再排放到环境中。

- 由于美国和其他国家的饮料和製药业对处理水的需求很高,北美用水和污水处理市场也正在快速成长。湖岸污水处理厂扩建计划4,300 万美元,涉及在加拿大安大略省开发一座污水处理厂。预计建设将于 2021 年第四季开始,并于 2023 年第二季完工。该计划旨在解决该地区的污水和污水处理需求。该计划预计将使加工能力提高70%。

- 由于全球对水处理的需求不断增加,预计整个预测期内对离子交换树脂的需求将会成长。

亚太地区占市场主导地位

- 预计预测期内亚太地区将主导全球离子交换树脂市场。

- 中国出口离子交换树脂主要到美国,是世界上最大的出口国。在中国,水处理应用对离子交换树脂的需求正在快速成长。食品饮料、化学、製药和电力行业对更纯净、更清洁的树脂的需求不断增加,以及公司对技术、研发的投资正在推动市场成长。

- 在亚太地区,中国是最大的用水国。全国有水质净化厂10113座,处理95%城镇和30%农村地区的污水。此外,中国计划在2021年至2025年期间新建或维修8万公里污水收集管网,增加污水处理能力2,000万立方公尺/日。

- 在「十四五」规划中,中国发布了废水再利用的新指南,要求提高废水再利用的比例。到2025年,25%的废弃物必须回收。

- 此外,印度是世界上最大的水消耗国之一,每年需要约 7,400 亿立方公尺的水来满足其需求。然而,地下水的枯竭和用水需求的增加增加了该国对处理水的依赖。

- 在韩国,2023 年 2 月,SK offplant Co. 宣布透过在地化生产超纯水核心技术,扩大其在水产业的投资组合。该公司已与专门从事膜製造和加工的韩国公司Sepratek签署了研发协议,投资其超纯水(UPW)核心技术。

- 预计上述因素将在预测期内推动亚太地区对离子交换树脂的需求。

离子交换树脂产业概况

离子交换树脂市场正在整合,主要企业占据全球市场占有率。市场上一些知名的参与者包括杜邦、朗盛、艺康、三菱化学公司和雅可比碳集团。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 电子和製药业对超纯水的需求不断增加

- 污水处理产业的成长

- 其他驱动因素

- 限制因素

- 离子交换树脂的细菌污染

- 其他限制因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔

- 按类型

- 通用树脂

- 特殊树脂

- 按应用

- 製药

- 饮食

- 水处理

- 采矿和冶金

- 化学处理

- 力量

- 其他的

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚国协

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章竞争格局

- 併购、合资、合作与协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- Anhui Samsung Resin Co. Ltd

- Bio-rad Laboratories Inc.

- Doshion Polyscience Pvt. Ltd

- Dupont

- Ecolab

- Eichrom Technologies Llc

- Evoqua Water Technologies Llc

- Ion Exchange(India)Ltd

- Jacobi Carbons Group

- Lanxess

- Mitsubishi Chemical Corporation

- Novasep

- Protech Water India

- Pure Resin Co. Ltd

- Resintech Inc.

- Samyang Corporation

- Sunresin New Materials Co. Ltd

- Suqing Group

- Suzhou Bojie Resin Technology Co. Ltd

- Thermax Limited

第七章 市场机会与未来趋势

- 燃料电池需求不断成长

The Ion Exchange Resin Market is expected to register a CAGR of 4.62% during the forecast period.

The market was negatively impacted due to COVID-19. Owing to the pandemic, several countries worldwide went into lockdown to curb the spread of the virus. The shutdown of numerous companies and factories disrupted worldwide supply networks and harmed global production, delivery schedules, and product sales. Currently, the market recovered from the COVID-19 pandemic and is increasing significantly.

Key Highlights

- Over the medium term, the major factors driving the market's growth are the growing water treatment industry and the increasing demand for ultra-pure water from the electronics or pharmaceutical industry.

- Conversely, bacterial contamination caused by ion exchange resins will likely hinder the studied market's growth.

- Growing demand for fuel cells is expected to offer growth opportunities to the market studied.

- Asia-Pacific dominated the market, with the largest consumption coming from China and India. Also, Asia-Pacific will likely register the fastest growth rate during the forecast period.

Ion Exchange Resin Market Trends

Water Treatment Segment to Drive the Market

- Ion exchange resins are commonly used as a water treatment agent to remove trace metal ions, organic compounds, and pollutants from water.

- Water treatment applications are increasing lately, owing to the strong demand for freshwater resources. Water recycling is a multi-stage process in wastewater treatment plants. The ion exchange treatment process is commonly used for water softening or demineralization. It is also used for removing other substances from water in processes such as de-alkalization, de-ionization, and disinfection. These are used for both industrial and municipal purposes.

- Recently, ion exchange resins is increasingly used to create drinking water. Specialized resins are designed to treat various contaminants, including perchlorate and uranium.

- Many resins, such as strong base/strong anion resin, are designed to remove nitrates and perchlorate. There are also resin beads that can be used for water softening.

- Resin materials contain a finite exchange capacity. Each of the individual exchange sites will become full with prolonged use. When it is impossible to exchange ions, the resin must be recharged or regenerated to restore it to its initial condition. The substances used for this include sodium chloride, hydrochloric acid, sulfuric acid, or sodium hydroxide.

- The spent regenerant is the primary substance remaining from the process. It contains not only all the ions removed but also extra regenerations with high total dissolved solids. It can be treated in a municipal wastewater facility, while discharges may require monitoring.

- The efficacy of ion exchange for water treatment can be limited by mineral scaling, surface clogging, and other issues contributing to resin fouling. Pretreatment processes such as filtration or adding chemicals can help reduce or prevent these issues.

- Germany includes Europe's largest industrial wastewater treatment market, with almost 3,000 treatment plants. Over 920 million cubic meters of industrial wastewater are treated annually in the country before being discharged to the outside environment.

- The North American water and wastewater treatment market is also rapidly growing due to the high demand for treated water from the beverage and pharmaceutical industries in countries such as the United States. Expansion of the Lakeshore Wastewater Treatment Plant, a USD 43 million project, entails the development of a wastewater treatment plant in Ontario, Canada. Construction began in Q4 2021 and is expected to complete in Q2 2023. The project aims to address the region's wastewater and sewage needs. The project is expected to increase the capacity by 70%.

- With the increasing need for water treatment globally, the demand for ion exchange resins is projected to grow through the forecast period.

Asia-pacific to Dominate the Market

- Asia-Pacific is expected to dominate the global ion exchange resin market during the forecast period.

- China exports ion exchange resin mainly to the United States and is the largest exporter globally. In China, the demand for ion exchange resins for the applications in water treatment applications is growing at a fast pace. The increasing demand for purer and cleaner resins for usage in food and beverages, chemical, pharmaceutical, and power industries and companies investing in technology and R&D shall augment the market growth.

- In the Asia-Pacific region, China is the largest water consumer country. It contains 10,113 water treatment plants that treat wastewater for 95% of municipalities and 30% of rural areas. Moreover, China plans to build or renovate 80,000 km of sewage collection pipeline networks and increase sewage treatment capacity by 20 million cubic meters/day between 2021-2025.

- In the 14th Five-year Plan, China published new guidelines for wastewater reuse, which mandated increasing the proportion of sewage. It must be treated to reuse standards to 25% by 2025.

- Furthermore, India is among the largest water consumers in the world and needs around 740 billion cubic meters of water per year to meet the demand. However, depleting groundwater and increasing water demand are driving the dependency on water treatment in the country.

- In South Korea, in February 2023, SK Ecoplant Co. announced the expansion of its portfolio in the water industry through localizing core technology to produce ultrapure water. The company signed an R&D agreement with Sepratek, a Korean company specializing in membrane manufacturing and processes, to invest in core technologies for ultrapure water (UPW).

- The above factors are expected to drive the demand for Ion-exchange resins in the Asia-Pacific region during the forecast period.

Ion Exchange Resin Industry Overview

The ion exchange resin market is consolidated, with top players accounting for a major global market share. Some prominent players in the market include DuPont, LANXESS, Ecolab, Mitsubishi Chemical Corporation, and Jacobi Carbons Group, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand For Ultra Pure Water From Electronics Or Pharmaceutical Industry

- 4.1.2 Growing Wastewater Treatment Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Bacterial Contamination Caused by Ion Exchange Resins

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Commodity Resins

- 5.1.2 Specialty Resins

- 5.2 Application

- 5.2.1 Pharmaceutical

- 5.2.2 Food and Beverage

- 5.2.3 Water Treatment

- 5.2.4 Mining and Metallurgy

- 5.2.5 Chemical Processing

- 5.2.6 Power

- 5.2.7 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Anhui Samsung Resin Co. Ltd

- 6.4.2 Bio-rad Laboratories Inc.

- 6.4.3 Doshion Polyscience Pvt. Ltd

- 6.4.4 Dupont

- 6.4.5 Ecolab

- 6.4.6 Eichrom Technologies Llc

- 6.4.7 Evoqua Water Technologies Llc

- 6.4.8 Ion Exchange (India) Ltd

- 6.4.9 Jacobi Carbons Group

- 6.4.10 Lanxess

- 6.4.11 Mitsubishi Chemical Corporation

- 6.4.12 Novasep

- 6.4.13 Protech Water India

- 6.4.14 Pure Resin Co. Ltd

- 6.4.15 Resintech Inc.

- 6.4.16 Samyang Corporation

- 6.4.17 Sunresin New Materials Co. Ltd

- 6.4.18 Suqing Group

- 6.4.19 Suzhou Bojie Resin Technology Co. Ltd

- 6.4.20 Thermax Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Demand For Fuel Cells

离子交换树脂市场(按产品类型、原料基础、功能和应用)—2025-2030 年全球预测

离子交换树脂市场(按产品类型、原料基础、功能和应用)—2025-2030 年全球预测 阳离子和阴离子交换树脂市场报告:趋势、预测和竞争分析(至 2031 年)

阳离子和阴离子交换树脂市场报告:趋势、预测和竞争分析(至 2031 年) 全球半导体离子交换树脂市场 -市场占有率和排名、总收入、需求预测(2025-2031)

全球半导体离子交换树脂市场 -市场占有率和排名、总收入、需求预测(2025-2031) 离子交换树脂市场规模、份额、趋势分析报告:依产品、最终用途、地区、细分市场预测,2025-2030

离子交换树脂市场规模、份额、趋势分析报告:依产品、最终用途、地区、细分市场预测,2025-2030 离子交换树脂市场:依产品类型、应用和地区划分

离子交换树脂市场:依产品类型、应用和地区划分 离子交换树脂市场规模、份额、趋势及预测(按类型、应用和地区),2025 年至 2033 年

离子交换树脂市场规模、份额、趋势及预测(按类型、应用和地区),2025 年至 2033 年 离子交换树脂市场规模、份额和成长分析(按产品类型、应用、最终用途和地区)- 产业预测 2025-20322030 年离子交换树脂市场预测:按类型、应用、最终用户和地区分類的全球分析阴离子树脂市场:按类型、应用分类 - 2025-2030 年全球预测

离子交换树脂市场规模、份额和成长分析(按产品类型、应用、最终用途和地区)- 产业预测 2025-20322030 年离子交换树脂市场预测:按类型、应用、最终用户和地区分類的全球分析阴离子树脂市场:按类型、应用分类 - 2025-2030 年全球预测 全球矿用离子交换树脂市场,2024-2028

全球矿用离子交换树脂市场,2024-2028