|

市场调查报告书

商品编码

1687346

氨:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)Ammonia - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

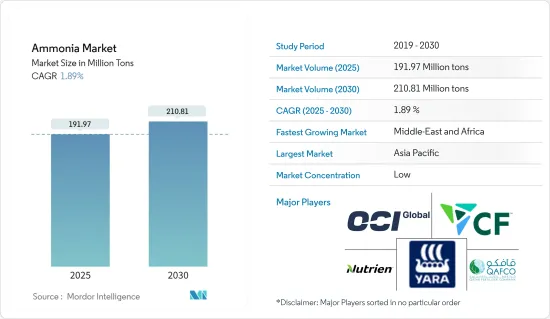

预计2025年氨市场规模为1.9197亿吨,2030年将达2.1081亿吨,预测期间(2025-2030年)复合年增长率为1.89%。

在 COVID-19 疫情期间,全球氨市场受到负面影响,农业、纺织、采矿业和其他终端用户产业受到严重影响。然而,行业内製药业的成长正在改善,预计这将有助于市场发展。目前,氨市场正在从疫情中復苏并经历强劲成长。

主要亮点

- 短期内,预化肥行业的大量使用和炸药製造中氨的使用量的增加将在预测期内推动市场成长。

- 然而,浓氨的危害可能会阻碍市场成长。

- 然而,预计 2024 年至 2029 年期间氨作为冷媒的使用和绿色氨的日益普及将为市场带来机会。

- 预计亚太地区将占据市场主导地位,并在 2024 年至 2029 年期间实现最高的复合年增长率。

氨市场趋势

农业可望主导市场

- 据世界经济论坛称,氨对农业和全球食品供应链至关重要。氨也被视为未来能源来源。

- 氨与大气中的氮结合,吸收的氮用于作物的主要养分,然后用于生产氮肥。氨作为肥料生产中不可或缺的原料,可以改善作物健康,并长期维持并提高土壤肥力。

- 根据联合国预测,世界人口将持续成长,到2050年将达到90亿。届时,预计相同土地面积上的粮食生产需求将增加60%。实现粮食安全需要以可负担的价格获得充足的、营养丰富的食物。这可以透过使用优化肥料来实现。

- 此外,美国是三大肥料成分的主要进口国之一。主要肥料成分生产国为中国、俄罗斯、加拿大和摩洛哥。 2023年3月,美国农业部(USDA)宣布了前两轮新津贴计划,旨在创新扩大47个州和两个地区的国内化肥生产能力。美国也宣布,已收到来自350多家独立公司的30亿美元申请,凸显国内化肥产业的强劲復苏。

- 此外,美国农业部宣布首轮津贴2900万美元。这些津贴可能有助于独立公司增加美国製造的化肥的产量并促进良性竞争。

- 2023年3月,CBH集团宣布开设新的奎那那化肥厂,将为西澳的粮食种植者带来巨大利益。该计划标誌着 CBH 液体肥料业务的开始,并将使其颗粒肥料生产能力提高 15,000。新设施的储存容量为 32,000 吨尿素硝酸铵 (UAN) 和 55,000 吨颗粒散装肥料。

- 因此,预计所有上述因素将在 2024-2029 年期间推动农业产业对氨的需求。

亚太地区预计将主导市场

- 由于中国、印度和日本等国家氨消费量庞大,亚太地区在氨市场占据主导地位。

- 中国是世界上最大的氨生产国和消费国。根据美国地质调查局 (USGS) 的数据,2023 年美国生产了 4,300 万吨氨。由于氨在农业领域(包括化肥、纺织、製药和采矿)的用途日益广泛,美国对氨的需求也在增加。

- 中国约占全球整体面积的7%,养活了全球22%的人口。该国是多种作物的最大生产国,包括水稻、棉花和马铃薯。因此,大规模的农业活动导致用作肥料的氨的需求激增。

- 此外,印度是严重依赖农业的经济体之一。超过55%的人口仍以农业为生。据化肥部称,2023财年的尿素产量将达到约2,800万吨,而上年度的产量为2,572万吨。印度的尿素产量正在上升。

- 纺织业也受益于氨的功能。液态氨在鞣製上的使用十分广泛,就像染料在纺织品染色中的使用一样。液氨在合成纤维的发展中扮演重要角色。氨溶液可以使织物着色达到几乎任何颜色。

- 日本在纺织品生产方面有着悠久的传统,是最大的技术纺织品生产国之一。为了在充斥着来自中国和其他新兴国家的廉价纺织产品的全球市场中保持竞争力,日本纺织业正在转型成为专门生产技术先进的智慧纺织产品的产业。合成蜘蛛丝和穿戴式健康监测器等创新是日本纺织业差异化努力的一部分。

- 此外,根据印度品牌股权基金会的数据,2023年4月至2023年10月,印度纺织品和服装出口(包括手工艺品)额为211.5亿美元。预计到 2025-26 年将达到 1900 亿美元。

- 因此,预计所有上述因素将导致 2024-2029 年期间氨市场需求增加。

合成氨产业展望

氨市场高度分散。主要参与者(不分先后顺序)包括 CF Industries Holdings Inc.、Yara、Nutrien Ltd.、OCI 和卡达化肥公司 (QAFCO)。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 肥料工业中的多种应用

- 火药製造的使用增加

- 限制因素

- 浓缩形式的危险

- 价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔

- 按类型

- 液体

- 气体

- 按最终用户产业

- 农业

- 纤维

- 矿业

- 製药

- 《冷冻》

- 其他终端用户产业(食品和饮料、橡胶、水处理、石油、纸浆和造纸业)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章竞争格局

- 併购、合资、合作与协议

- 市场占有率(%)分析

- 主要企业策略

- 公司简介

- BASF SE

- CF Industries Holdings Inc.

- Chambal Fertilisers and Chemicals Limited

- CSBP

- Eurochem Group

- Group DF(Ostchem)

- IFFCO

- Jsc Togliattiazot

- Koch Fertilizer LLC

- Nutrien Ltd

- OCI

- PT Pupuk Sriwidjaja Palembang(Pusri)

- Qatar Fertiliser Company(QAFCO)

- Rashtriya Chemicals And Fertilizers Limited

- SABIC

- Yara

第七章 市场机会与未来趋势

- 使用氨作为冷媒

- 扩大绿色氨的应用

The Ammonia Market size is estimated at 191.97 million tons in 2025, and is expected to reach 210.81 million tons by 2030, at a CAGR of 1.89% during the forecast period (2025-2030).

During the COVID-19 pandemic, there was a negative impact on the ammonia market globally as agriculture, textile, mining, and other end-user industries were significantly affected. However, growth in the pharmaceutical segment is improving in the industry, and this is expected to assist in market development. Currently, the ammonia market has recovered from the pandemic and is growing significantly.

Key Highlights

- In the short term, abundant use in the fertilizer industry and ammonia's increasing usage for the production of explosives are projected to fuel the market's growth during the forecast period.

- However, the hazardous effects of ammonia in its concentrated form are likely to hinder the growth of the market.

- Nevertheless, the use of ammonia as a refrigerant and the growing adoption of green ammonia are likely to act as opportunities for the market between 2024 and 2029.

- Asia-Pacific is expected to dominate the market and is likely to witness the highest CAGR from 2024 to 2029.

Ammonia Market Trends

The Agriculture Industry is Expected to Dominate the Market

- According to the World Economic Forum, ammonia is vital in agriculture and the global food supply chain. Ammonia has also been recognized as a future energy source for clean hydrogen.

- Ammonia binds nitrogen from the atmosphere and produces the primary crop nutrients using the absorbed nitrogen, which is then used to produce nitrogen fertilizers. As an essential raw material for fertilizer production, ammonia improves crop health and, in the long run, maintains and even increases soil fertility.

- According to the United Nations, the world population continues to grow and will reach 9 billion by 2050. By then, on the same land area, the demand for food production is expected to increase by 60%. Achieving food security requires the availability of sufficient, nutritious food at affordable prices. This can be achieved through the use of optimized fertilizers.

- Additionally, the United States is among the top importers of the three major fertilizer ingredients. Major producers of the main fertilizer components include China, Russia, Canada, and Morocco. In March 2023, the US Department of Agriculture (USDA) announced the first two rounds of a new grant program to expand innovative production for domestic fertilizer production capacity in 47 states and two territories. The USDA further announced that it received USD 3 billion in applications from more than 350 independent companies, thus highlighting significant recovery in the country's fertilizer industry.

- Furthermore, the USDA also announced its first USD 29 million grant offering in the first round. The subsidy will help independent companies increase their production of American-made fertilizers and encourage healthy competition.

- In March 2023, CBH Group announced the opening of its new Kwinana Fertilizer Plant, which will benefit grain farmers in Western Australia significantly. The project marks the start of CBH's liquid fertilizer business, increasing its granular fertilizer production capacity by 15,000. The new facility has 32,000 tons of urea ammonium nitrate (UAN) storage capacity and 55,000 tons of granular bulk fertilizer.

- Therefore, all the aforementioned factors are expected to enhance the demand for ammonia from the agriculture industry between 2024 and 2029.

Asia-Pacific is Expected to Dominate the Market

- Asia-Pacific dominates the ammonia market owing to large consumption from countries such as China, India, and Japan.

- China is the largest producer and consumer of ammonia in the world. According to the US Geological Survey (USGS), the country produced 43 million metric tons of ammonia in 2023. The demand for ammonia in the country is rising due to increasing applications in the agriculture industry, such as fertilizers, textiles, pharmaceuticals, and mining.

- China accounts for approximately 7% of the overall agricultural acreage globally, thus feeding 22% of the world's population. The country is the largest producer of various crops, including rice, cotton, potatoes, and others. Hence, the demand for ammonia, which is used as a fertilizer, is rapidly increasing owing to the country's large-scale agricultural activities.

- Further, India is one of the economies that are largely dependent on agriculture. Agriculture is still the primary source of livelihood for more than 55% of the population. As per the Department of Fertilizers, in FY2023, about 28 million metric tons of urea were produced in India, which was 25.72 million metric tons in the previous year. Urea production in India presented an increasing trend.

- The textile industry also benefits from ammonia's capabilities. The use of liquid ammonia in tanning is widespread, as is the use of dyes in textile dyeing. Liquid ammonia plays an important role in the development of synthetic fabrics. The solution of ammonia enables fabric coloring to achieve almost any color.

- Japan has a long tradition in textile production and is one of the largest manufacturers of technical textiles. To remain competitive in the global market flooded with cheap textiles from China and other emerging countries, the Japanese textile industry is transforming into an industry that specializes in technological and smart textiles. Innovations such as synthetic spider silk and wearable health monitors are among the efforts to differentiate the Japanese textile industry.

- In addition, according to the Indian Brand Equity Foundation, India's textile and apparel exports (including handicrafts) from April 2023 to October 2023 stood at USD 21.15 billion. The industry is expected to reach USD 190 billion by 2025-26.

- Thus, all the above-mentioned factors are likely to provide the increasing demand for the ammonia market between 2024 and 2029.

Ammonia Industry Oveview

The ammonia market is highly fragmented in nature. The major players (not in any particular order) include CF Industries Holdings Inc., Yara, Nutrien Ltd, OCI, and Qatar Fertiliser Company (QAFCO).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Abundant Use in the Fertilizer Industry

- 4.1.2 Increasing Usage to Produce Explosives

- 4.2 Restraints

- 4.2.1 Hazardous Effects in its Concentrated Form

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Liquid

- 5.1.2 Gas

- 5.2 End-user Industry

- 5.2.1 Agriculture

- 5.2.2 Textiles

- 5.2.3 Mining

- 5.2.4 Pharmaceutical

- 5.2.5 Refrigeration

- 5.2.6 Other End-user Industries (Food and Beverage, Rubber, Water Treatment, Petroleum, and Pulp and Paper Industries)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 CF Industries Holdings Inc.

- 6.4.3 Chambal Fertilisers and Chemicals Limited

- 6.4.4 CSBP

- 6.4.5 Eurochem Group

- 6.4.6 Group DF (Ostchem)

- 6.4.7 IFFCO

- 6.4.8 Jsc Togliattiazot

- 6.4.9 Koch Fertilizer LLC

- 6.4.10 Nutrien Ltd

- 6.4.11 OCI

- 6.4.12 PT Pupuk Sriwidjaja Palembang (Pusri)

- 6.4.13 Qatar Fertiliser Company (QAFCO)

- 6.4.14 Rashtriya Chemicals And Fertilizers Limited

- 6.4.15 SABIC

- 6.4.16 Yara

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Use of Ammonia as a Refrigerant

- 7.2 Growing Adoption of Green Ammonia

全球预测:2025-2030 年氨市场(按类型、生产过程、水分含量类型、物理状态、纯度等级、应用、最终用途和分销管道)

全球预测:2025-2030 年氨市场(按类型、生产过程、水分含量类型、物理状态、纯度等级、应用、最终用途和分销管道) 2025年全球氨市场报告2025年蓝色氨全球市场报告

2025年全球氨市场报告2025年蓝色氨全球市场报告 2034 年氨市场分析及预测:类型、产品、应用、技术、最终用户、流程、组件、部署

2034 年氨市场分析及预测:类型、产品、应用、技术、最终用户、流程、组件、部署 氨市场-全球产业规模、份额、趋势、机会和预测,按形态(液体、气体、粉末)、按最终用户(农业、纺织、采矿、製药、冷冻等)、按地区和竞争情况划分,2020 年至 2030 年预测

氨市场-全球产业规模、份额、趋势、机会和预测,按形态(液体、气体、粉末)、按最终用户(农业、纺织、采矿、製药、冷冻等)、按地区和竞争情况划分,2020 年至 2030 年预测 氨(NH3)全球市场,2025-2029

氨(NH3)全球市场,2025-2029 日本氨市场报告(依实体形态、应用、最终用途产业和地区)2025-20332025 年至 2033 年氨市场规模、份额、趋势及预测(依实体形态、应用、最终用途产业及地区)

日本氨市场报告(依实体形态、应用、最终用途产业和地区)2025-20332025 年至 2033 年氨市场规模、份额、趋势及预测(依实体形态、应用、最终用途产业及地区) 按类型、应用、最终用途行业和地区分類的氨市场

按类型、应用、最终用途行业和地区分類的氨市场 全球氨市场研究报告-产业分析、规模、份额、成长、趋势与预测 2025 年至 2033 年

全球氨市场研究报告-产业分析、规模、份额、成长、趋势与预测 2025 年至 2033 年