|

市场调查报告书

商品编码

1687364

包装黏合剂:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)Packaging Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

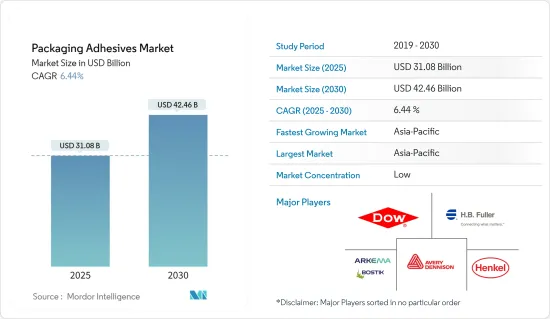

预计 2025 年包装黏合剂市场规模为 310.8 亿美元,到 2030 年将达到 424.6 亿美元,预测期内(2025-2030 年)的复合年增长率为 6.44%。

2020 年市场受到新冠疫情的轻微影响。新冠疫情限制了外出用餐,导致家庭烹饪增加。因此,果汁、水、软性饮料和酒精饮料的产值大幅下降,但这在很大程度上被麵粉、乳製品、保健食品和方便性或已调理食品的成长所抵消。

主要亮点

- 推动市场成长的因素是食品和饮料行业需求的不断增长、食品安全意识的不断增强以及对污染风险的避免。

- 另一方面,对黏合剂製造中使用的各种原材料的法规的影响可能会阻碍市场成长。

- 然而,电子商务的快速成长可能为市场提供进一步的成长机会。

- 亚太地区占据了最大的市场份额,预计在预测期内将继续占据市场主导地位。

包装胶合剂市场趋势

软包装应用将达到最高成长率

- 受消费者偏好转向新颖、美观的包装、易用性、永续性和认真的环保原则的推动,软包装正在经历巨大的成长。

- 软包装贴合黏剂有多种技术、黏度和固态浓度可供选择。常用的贴合黏剂有四种基本类型:水基、溶剂基、反应性 100%固态(无溶剂)液体和热熔性。

- 软包装中使用的溶剂型黏合剂通常是双组分聚氨酯贴合黏剂。它们设计用于干式层压工艺。

- 软包装也是VAE胶黏剂最重要的应用类型。此外,由于其柔韧性、防潮性以及对基材的优异附着力,层压应用也是一个主要类别。

- 美国、中国和印度等国家的人口不断增长,加上食品需求的增加,推动了全球对软包装的需求。

- 根据美国软包装协会(FPA)预测,到2020年底,美国软包装产业的年总销售额将超过356亿美元。软包装产业包括零售和机构食品和非食品产品、医疗和药品、工业用品、零售购物袋等的包装。美国食品业是软包装最大的细分市场。

- 此外,包装黏合剂也用于茅屋起司软包装膜,用于密封纸板品脱、塑胶容器和食品托盘,包括乳製品,如优酪乳、酸奶油等。

- 预计 2022 年全球食品业的收益将达到 8.8 兆美元。预计 2022 年至 2027 年期间市场复合年增长率为 4.79%。

- 因此,食品业需求增加和软包装成长等上述因素可能会在预测期内推动包装黏合剂的市场需求。

亚太地区占市场主导地位

- 由于中国、日本和印度等国家的需求旺盛,亚太地区目前占据包装黏合剂市场的最大份额。

- 随着人均收入的提高以及电子商务巨头的崛起,中国已成为包装胶合剂的主要消费国。

- 根据中国国家统计局的数据,2020年社会消费品零售总额为39,1980.7亿元人民币(5,5323.1亿美元),2021年将增长至44,8234亿元人民币(6,2216.6亿美元),从而推动了消费品包装和运输活动中的胶合消费。

- 此外,中国是世界上最大的食品产业之一。由于微波炉、零食和冷冻食品等食品领域的客製化包装增加以及出口增加,预计该国在预测期内将呈现持续成长。预计未来包装黏合剂的使用量将会增加。

- 此外,食品业是印度包装黏合剂的最大消费者之一。包装黏合剂的主要终端使用者包括药品、个人保健产品和家用电器。这些最终用户群体不断增长的需求正在创造巨大的市场成长潜力。

- 印度的包装产业也在快速发展。它是印度经济的第五大产业,也是当今印度成长最快的产业之一。随着电子商务的兴起,印度包装产业蓬勃发展,成为成长最强劲的产业之一。

- 根据印度包装协会(IIP)的数据,过去十年印度的包装消费量增加了 200%,从人均每年 4.3 公斤(pppa)增加到人均每年 8.6 公斤(pppa)。

- 因此,由于上述因素,预计亚太地区将在预测期内占据市场主导地位。

包装胶合剂产业概况

包装黏合剂市场较为分散,没有一家企业能够占据全球市场的较大份额。全球公司都高度重视研发和合作开发新技术,以保持其在市场上的地位和立足点。市场的主要企业包括汉高股份公司、HB Fuller、陶氏、阿科玛(博斯蒂克)和艾利丹尼森公司。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 食品和饮料行业的需求不断增长

- 提高食品安全意识

- 限制因素

- 严格的政府法规

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔

- 依技术

- 水性

- 溶剂型

- 热熔胶

- 按应用

- 软包装

- 折迭式盒/纸箱

- 密封

- 标籤和胶带

- 其他的

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚国协

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章竞争格局

- 併购、合资、合作与协议

- 市场排名分析

- 主要企业策略

- 公司简介

- 3M

- Arkema Group(Bostik)

- AVERY DENNISON CORPORATION

- Ashland

- Dow

- Henkel AG & Co. KGaA

- HB Fuller Company

- Jowat SE

- Paramelt RMC BV

- Wacker Chemie AG

第七章 市场机会与未来趋势

- 电子商务产业快速成长

The Packaging Adhesives Market size is estimated at USD 31.08 billion in 2025, and is expected to reach USD 42.46 billion by 2030, at a CAGR of 6.44% during the forecast period (2025-2030).

The market was marginally impacted by COVID-19 in 2020. The COVID-19 pandemic limited dining out and led to increases in home cooking. With that, significant drops in the production values of juices, water, soft drinks, and alcoholic beverages were nearly offset by growth in wheat flour, dairy, health foods, and convenience or ready-to-eat foods.

Key Highlights

- The factors driving the growth of the market studied are the growing demand from the food and beverage industry, increasing awareness about food safety , and avoiding risks of contamination.

- On the flip side, the impact of regulations on various raw materials to be used for manufacturing adhesives may hinder the market's growth.

- However, the rapid growth in e-commerce will further provide opportunities for the market to grow.

- Asia-Pacific accounted for the highest share of the market, and it is likely to continue dominating the market during the forecast period.

Packaging Adhesives Market Trends

Flexible Packaging Application to Witness the Highest Growth Rate

- Flexible packaging is growing at an impressive rate, driven by consumer preferences shifting toward new attractive packages, ease of use, sustainability, and conscientious environmental ideals.

- Laminating adhesives for flexible packaging are available in various technologies, viscosities, and solids concentrations. There are four basic categories of laminating adhesives that are commonly used. These are waterborne, solvent-based, reactive 100% solid (solventless) liquid, and hot melt.

- Solvent-based adhesives used in flexible packaging are generally two-component polyurethane laminating adhesives. These are designed for use in the dry lamination process.

- Flexible packaging is also the most significant application type for VAE adhesives. Another large category is laminating applications due to their flexibility, moisture resistance, and superior substrate adhesion.

- With the growing population in countries such as the United States, China, and India, the requirement for food is increasing, thus resulting in increased demand for flexible packaging worldwide.

- According to the Flexible Packaging Association (FPA), the total US flexible packaging industry registered more than USD 35.6 billion in annual sales by the end of 2020. The flexible packaging industry includes packaging for retail and institutional food and non-food, medical and pharmaceutical, industrial materials, and retail shopping bags, among others. The US food industry is the largest segment for flexible packaging.

- Furthermore, packaging adhesives are also used in lidding films, which are a type of flexible packaging film commonly made by using foils, paper, polyester, polyethylene, and others generally used to seal paperboard pints, plastic containers, and trays for food items, including dairy products such as cottage cheese, sour cream, and others.

- The food industry worldwide is estimated to generate a revenue of USD 8.8 trillion in 2022. The market is expected to register a CAGR of 4.79% during 2022-2027.

- Hence, the factors above, such as increasing demand from the food industry and growing flexible packaging, will likely boost the market demand for packaging adhesives during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific currently accounts for the highest share of the packaging adhesives market, owing to the high demand from countries like China, Japan, India, etc.

- China is the leading country in the consumption of packaging adhesives due to growing per capita income, coupled with rising e-commerce giants in the country.

- According to the National Bureau of Statistics of China, the total retail sales revenue of consumer goods accounted for CNY 39,198.07 billion (~ USD 5532.31 billion) in 2020, which rose to CNY 44,082.34 billion (~ USD 6221.66 billion) in 2021, thereby enhancing the consumption of adhesives from consumer goods packaging and shipping activities.

- Additionally, China has one of the largest food industries globally. The country is expected to witness consistent growth during the forecast period due to the rise of customized packaging in the food segment, like microwave, snack, and frozen foods, and increasing exports. The use of packaging adhesives is expected to increase in the future.

- Furthermore, In India, the food industry is among the largest consumers of packaging adhesives. Some key end-user sectors of packaging adhesives include pharmaceuticals, personal care products, consumer electronics, etc. Increasing demand from these end-user segments is creating a huge market growth potential.

- In India, the packaging industry is also increasing at a rapid rate. It is the fifth-largest sector in India's economy and is currently one of the fastest and highest-growing sectors in the country. Amid the e-commerce surge, the Indian packaging industry is witnessing steep growth and is one of the strongest growing segments.

- According to the Indian Institute of Packaging (IIP), packaging consumption in India increased by 200% in the past decade, from 4.3 kgs per person per annum (pppa) to 8.6 kgs pppa.

- Hence, owing to the above-mentioned factors, Asia-Pacific is likely to dominate the market studied during the forecast period.

Packaging Adhesives Industry Overview

The packaging adhesives market is fragmented, as no major company holds a significant share of the global market. Global companies are significantly focusing on R&D and collaborations to develop new technologies to maintain their market presence and foothold. Some of the key players in the market include Henkel AG & Co. KGaA, H.B. Fuller, Dow, Arkema (Bostik), and Avery Dennison Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from the Food and Beverage Industry

- 4.1.2 Increasing Awareness for Food Safety

- 4.2 Restraints

- 4.2.1 Strict Government Regulations

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Technology

- 5.1.1 Water-based

- 5.1.2 Solvent-based

- 5.1.3 Hot-melt

- 5.2 By Application

- 5.2.1 Flexible Packaging

- 5.2.2 Folding Boxes and Cartons

- 5.2.3 Sealing

- 5.2.4 Labels and Tapes

- 5.2.5 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Arkema Group (Bostik)

- 6.4.3 AVERY DENNISON CORPORATION

- 6.4.4 Ashland

- 6.4.5 Dow

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 H.B. Fuller Company

- 6.4.8 Jowat SE

- 6.4.9 Paramelt RMC B.V.

- 6.4.10 Wacker Chemie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rapid Growth of the E-commerce Industry

包装胶合剂市场-全球产业规模、份额、趋势、机会及预测,依技术、树脂、应用、地区及竞争细分,2020-2030 年

包装胶合剂市场-全球产业规模、份额、趋势、机会及预测,依技术、树脂、应用、地区及竞争细分,2020-2030 年 2025-2033年包装胶合剂市场报告(按类型、基材类型、包装类型、最终用途行业和地区)

2025-2033年包装胶合剂市场报告(按类型、基材类型、包装类型、最终用途行业和地区) 全球包装黏合剂市场未来展望(至2030年)

全球包装黏合剂市场未来展望(至2030年) 包装黏合剂市场规模、份额、成长分析(按树脂、技术和地区)—2025-2032 年产业预测

包装黏合剂市场规模、份额、成长分析(按树脂、技术和地区)—2025-2032 年产业预测 2025年包装黏合剂全球市场报告

2025年包装黏合剂全球市场报告 包装黏合剂市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

包装黏合剂市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 包装黏剂市场报告:2030 年趋势、预测与竞争分析

包装黏剂市场报告:2030 年趋势、预测与竞争分析 包装黏合剂市场:2024-2031年全球产业分析、规模、占有率、成长、趋势、预测全球包装黏合剂市场 2024-2031

包装黏合剂市场:2024-2031年全球产业分析、规模、占有率、成长、趋势、预测全球包装黏合剂市场 2024-2031 到 2030 年包装黏剂市场预测:按产品类型、原材料类型、包装类型、黏剂化学、技术、应用、最终用户和地区进行的全球分析

到 2030 年包装黏剂市场预测:按产品类型、原材料类型、包装类型、黏剂化学、技术、应用、最终用户和地区进行的全球分析