|

市场调查报告书

商品编码

1687814

碳化钙-市场占有率分析、产业趋势与统计、成长预测(2025-2030)Calcium Carbide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

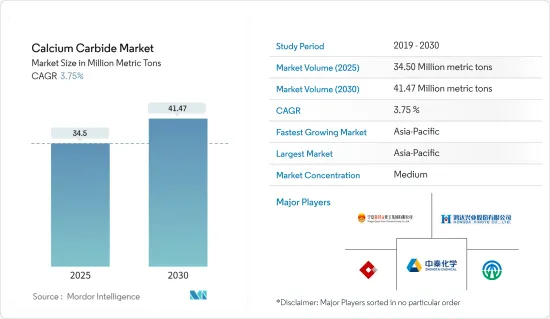

预计 2025 年碳化钙市场规模将达到 3,450 万吨,预计到 2030 年将达到 4,147 万吨,预测期内(2025-2030 年)的复合年增长率为 3.75%。

COVID-19 对受访市场产生了负面影响。疫情期间,汽车製造活动因封锁而暂时停止,导致碳化钙消费量下降。然而,限制解除后市场恢復良好。由于化工、冶金、食品等终端用户产业对碳化钙的消费量增加,市场出现明显復苏。

化学製造需求的不断增长和全球钢铁产量的上升正在推动所研究市场的成长。然而,碳化钙对健康的不利影响和严格的环境法规可能会阻碍市场成长。

扩大乙炔及其衍生物的下游应用可以为所研究的市场带来机会。

亚太地区占据市场主导地位,中国是世界上最大的碳化钙生产国和消费国。预计亚太地区在预测期内的复合年增长率最高。

碳化钙市场趋势

化工产业占市场主导地位

- 碳化钙是合成有机化学和工业化学中的关键组成部分。碳化钙是乙炔的主要来源之一,广泛应用于化学工业。乙炔是一种非常有用的碳氢化合物,因为其三键中蕴含着能量。

- 乙炔最常见的用途之一是作为生产氯乙烯、乙酸和丙烯腈的原料。 PVC 用于各种纤维、薄膜、电缆和片材配方,在建筑和汽车领域有着广泛的应用。

- 乙炔生产的另一种产品是氢氧化钙,它有多种用途。其最广泛的用途是石化燃料发电厂产生的排放,以去除硫化合物,防止其排放到大气中。化学製造商使用氢氧化钙来中和废弃物,地方政府则用它来处理污水。

- 根据BASF2023发布的报告,预计全球化学品产量年增将从2023年的2.2%上升至与前一年同期比较的2.7%。

- 在美国,2022 年化学品产量增加了 2.3%。然而,2021 年与天气相关的生产损失起了主要作用。同时,预计2022年南美产量将成长2.6%,略低于上年(成长3.6%)。

- 同样,在欧洲,法国化学工业的化学品和化学产品总销售额仅次于德国。法国在化学工业研发投入方面排名世界第六,每年投入约21亿美元。

- 在南美,巴西化学工业协会(Abiquim)为化学工业提出了短期、中期和长期提案,以帮助降低成本、提高竞争力、改善监管和促进投资。该提案的目标是到2030年将化学工业在该国GDP的份额提高到2,312亿美元。

- 碳化钙也主要用于生产氰胺基化钙,用作肥料。根据国际肥料工业协会预测,到2022年,东亚将成为全球化肥产能最高的地区,占全球产量的31%以上。其次是东欧和中亚,占17%。

- 根据中东通讯引述埃及化肥出口委员会的声明称,埃及化肥出口额预计将从 2021 年的 73.3 亿美元增长 23%,至 2022 年的 86.2 亿美元。化学工业占埃及非石油出口总额的24%。

- 因此,这些因素和趋势可能会影响未来几年全球碳化钙市场的成长。

亚太地区可望主导市场

- 亚太地区约占全球碳化钙需求的94%。中国是世界上最大的碳化钙生产国和消费国,化学、冶金、食品等终端用户产业的需求日益增长。

- 此外,由于蕴藏量庞大以及对VCM(氯乙烯单体)、VAM(醋酸乙烯单体)和乙炔法生产BDO(丁二醇)的需求不断增长,碳化钙的消费量也在增加。

- 中国是最大的煤炭消费量。除了用于发电之外,中国长期以来也利用煤炭生产化学品。自 19 世纪下半叶以来,煤焦油主要用于染料工业的芳香族化合物和特殊化合物的合成。

- 最近,碳化钙已被用来将煤转化为乙炔。这导致丙烯腈 (ACN)、氯乙烯单体 (VCM)、1,4-丁二醇 (BDO) 和丙烯酸 (AA) 的产量增加。中国计划扩建约 10 个丙烯腈产能,到 2026 年总产能将达到约 223 万吨/年。

- 此外,中国也是世界上最大的钢铁生产国。 2023年粗钢产量为10.191亿吨。 2023 年 9 月,中国钢铁製造商乌兰浩特钢铁在其位于内蒙古(中国北方的一个自治区)的工厂运作了一座新的高炉。该高炉容量为1,200立方米,预计年产铁113万吨。预计钢铁产量的上升将推动用于燃烧和清洗用途的乙炔气的需求。此外,碳化钙也用于生产低碳钢。碳化钙在钢铁工业中扮演重要角色。主要用于钢铁生产过程中的脱硫工艺。

- 此外,日本是该地区第二大碳化钙消费国。日本化学工业由少数知名公司主导,这些公司通常高度多元化,并经常与其他公司建立合作关係。根据德国化学工业委员会(VCI)预测,2022年日本化学工业销售额预计将达到约2,272.6亿欧元(2,466.3亿美元)。日本化学工业销售额位居亚洲第二,仅次于中国。

- 乙炔是由碳化钙(CaC2)与水(H2O)反应生成的。预计到2022年,日本化学工业溶解乙炔产量将下降至8,110吨,低于2014年的10920吨,是观察期间该产业的最低产量。值得注意的是,近年来该行业的产量一直在下降。

- 东南亚国协的硬质合金消费量也在增加。越南和印尼分别是全球第12大和第15大粗钢生产国,产能分别为1,900万吨和1,600万吨。

- 根据世界钢铁协会的报告,预计2023年印尼粗钢产量将增加2.8%,达到约1600万吨,而2022年为1560万吨。印尼钢铁业的积极成长得益于政府在智慧供需理念下,从上游到下游优先发展钢铁业的管理努力。

- 因此,预计上述因素将在未来几年对市场产生重大影响。

碳化钙产业概况

碳化钙市场部分分散,顶级公司之间为扩大市场占有率展开激烈竞争。市场主要企业(排名不分先后)包括新疆天业(集团)、新疆中泰化工、宏达兴业、中盐内蒙古化工、宁夏金裕源化工集团等。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 全球钢铁业需求旺盛

- 化学製造需求增加

- 限制因素

- 碳化钙对健康的不良影响

- 严格的环境法规

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔

- 应用

- 乙炔气

- 氰胺基化钙

- 还原剂和脱水剂

- 脱硫脱氧剂

- 其他用途

- 最终用户产业

- 化学品

- 冶金

- 食物

- 其他最终用户产业

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 世界其他地区

- 亚太地区

第六章竞争格局

- 併购、合资、合作与协议

- 市场占有率(%)分析

- 主要企业策略

- 公司简介

- Alzchem Group AG

- American Elements

- Carbide Industries LLC

- China Salt Inner Mongolia Chemical Co. Ltd

- DCM Shriram

- Denka Company Limited

- Hongda Xingye Co. Ltd

- Inner Mongolia Baiyanhu Chemical Co. Ltd

- Merck KGaA(Sigma-Aldrich)

- NGO Chemical Group Ltd

- Ningxia Jinyuyuan Chemical Group Co. Ltd

- Ningxia Yinglite Chemical Co. Ltd

- Xiahuayuan Xuguang Chemical Co. Ltd

- Xinjiang Tianye(Group)Co. Ltd

- Xinjiang Zhongtai Chemical Co. Ltd

第七章 市场机会与未来趋势

- 乙炔及其衍生物下游用途的成长

The Calcium Carbide Market size is estimated at 34.50 million metric tons in 2025, and is expected to reach 41.47 million metric tons by 2030, at a CAGR of 3.75% during the forecast period (2025-2030).

COVID-19 negatively impacted the market studied. During the pandemic, automotive manufacturing activities were stopped temporarily due to the lockdown, thereby decreasing the consumption of calcium carbide. However, the market recovered well after the restrictions were lifted. The market recovered significantly, owing to the rise in consumption of calcium carbide in chemicals, metallurgy, food, and other end-user industries.

The increasing demand for chemical production and rising steel production worldwide are driving the growth of the market studied. However, the detrimental health effects of calcium carbide and stringent environmental regulations may hinder market growth.

Growing downstream applications of acetylene and its derivatives can act as an opportunity for the market studied.

Asia-Pacific dominated the market, with China being the largest producer and consumer of calcium carbide globally. During the forecast period, Asia-Pacific is expected to record the highest CAGR.

Calcium Carbide Market Trends

Chemical Industry to Dominate the Market

- Calcium carbide is one of the primary building blocks in synthetic organic and industrial chemistry. It is one of the major sources of acetylene, which is extensively used in the chemical industry. Acetylene is an extremely useful hydrocarbon due to the energy that is locked up in its triple bond.

- One of the most common applications of acetylene is its use as a raw material for manufacturing vinyl chloride, acetic acid, and acrylonitrile. Vinyl chloride is used in the formulation of various fibers, films, cables, sheets, etc., and it has numerous applications in the construction and automotive sectors.

- The co-product of acetylene production is calcium hydroxide, which has several uses. It is most widely used in the process of scrubbing stack gases from fossil fuel-based power plants to remove sulfur compounds before they are released into the air. Chemical manufacturers use calcium hydroxide to neutralize their waste streams, while municipalities use it to treat sewage water.

- According to a report published by BASF 2023, global chemical production is expected to increase to 2.7% in 2024 from 2.2% in 2023, thus increasing year-on-year.

- In the United States, chemical production increased by 2.3% in 2022. However, the underlying impact of weather-related production losses in 2021 played a major role. Meanwhile, production in South America grew at 2.6% in 2022, slightly slower than the previous year (+3.6%).

- Similarly, in Europe, the French chemical industry is the second-largest in total sales of chemicals and chemical products after Germany. France ranks sixth among all countries in terms of R&D investments in the chemical industry, spending around USD 2.1 billion annually.

- In South America, the Brazilian Chemical Industry Association, Abiquim, introduced a set of short-, medium-, and long-term proposals for the chemical industry, which may help reduce cost, increase competitiveness, improve regulatory aspects, and increase investment. This proposal aims to increase the share of the chemical sector in the country's GDP to USD 231.2 billion by 2030.

- Calcium carbide is also majorly used in the production of calcium cyanamide, which is used as a fertilizer. As per the International Fertilizer Industry Association, in 2022, East Asia recorded the highest fertilizer production capacity worldwide, accounting for more than 31% of production. Eastern Europe and Central Asia followed, with a share of 17%.

- Moreover, according to the Middle East News Agency (MENA), citing a statement by the Egyptian Fertilizer Export Council, Egypt's chemical fertilizer exports were expected to increase by 23% from USD 7.33 billion in 2021 to USD 8.62 billion in 2022. The chemical sector accounted for 24% of Egypt's total non-oil exports.

- So, these factors and trends can affect the growth of the global calcium carbide market over the next few years.

Asia-Pacific is Expected to Dominate the Market

- Asia-Pacific accounts for around 94% of the global demand for calcium carbide. China is the world's largest producer and consumer of calcium carbide, with increased demand from end-user industries such as chemicals, metallurgy, and food.

- Moreover, because of its large reserves and growing demand for VCM (vinyl chloride monomer), VAM (vinyl acetate monomer), and BDO (butanediol) from acetylene, the consumption of calcium carbide is increasing.

- China records the largest consumption of coal. Not only has it been used for power generation, but the Chinese have been using coal for chemical production for a long time. Since the late 19th century, coal tar has been used to synthesize aromatics and special chemical compounds, primarily for the dye industry.

- Lately, the country has been using calcium carbide to convert coal to acetylene. This has led to the increased production of acrylonitrile (ACN), vinyl chloride monomer (VCM), 1,4-butanediol (BDO), and acrylic acid (AA). China has around ten planned additions to acrylonitrile capacity, with a total capacity of about 2.23 million tonnes per annum (Mtpa) by 2026.

- Additionally, China is by far the largest steel producer globally. In 2023, the county produced 1,019.1 million tons of crude steel. The second largest, India, had a production of a mere 140.2 Mt. Moreover, in September 2023, Chinese steel company Ulanhot Steel launched a new blast furnace at a plant in Inner Mongolia (an autonomous region in Northern China). The blast furnace capacity of 1.2 thousand cubic meters is estimated at 1.13 million tons of iron per year. The increasing steel production is expected to increase the demand for acetylene gas for flame-cutting and cleansing purposes. Additionally, calcium carbide is used in the production of low-carbon steel. Calcium carbide plays a vital role in the steel industry. It is primarily utilized in the desulfurization process during steel production.

- Moreover, Japan is the second largest consumer of calcium carbide in the region. The Japanese chemical industry is dominated by a few prominent companies, which are usually highly diversified and often form alliances with other companies. According to the German Chemical Industry Association, VCI, in 2022, the sales value of the chemical industry in Japan amounted to approximately EUR 227.26 billion (USD 246.63 billion). Following China, the Japanese chemical industry had the second-largest sales value in Asia.

- The reaction of calcium carbide (CaC2) with water (H2O) is used to produce acetylene. The production volume of dissolved acetylene in the chemical industry in Japan decreased to 8.11 thousand tons in 2022. The production volume has declined since 2014, when it amounted to 10.92 thousand tons. This marked the lowest production quantity in this industry during the observed period. Notably, this industry's production quantity decreased over the last few years.

- ASEAN countries are also witnessing an increased consumption of calcium carbide. Vietnam and Indonesia were the 12th and 15th largest crude steel producers globally, with a production capacity of 19 million tonnes and 16 million tonnes.

- As per the World Steel Association report, Indonesia produced around 16 million tons of crude steel in 2023, compared to 15.6 million tons in 2022, registering a growth of 2.8%. The positive growth of the steel industry in Indonesia was due to control efforts carried out by the government in the country, with the concept of smart supply demand, which was executed by prioritizing the national steel industry from the upstream sector to the downstream sector.

- Therefore, the aforementioned factors are expected to have a significant impact on the market in the coming years.

Calcium Carbide Industry Overview

The market studied is partially fragmented, with intense competition among the top players to increase their shares in the market. Some of the key players in the market (not in a particular order) include Xinjiang Tianye (Group) Co. Ltd, Xinjiang Zhongtai Chemical Co. Ltd, Hongda Xingye Co. Ltd, China Salt Inner Mongolia Chemical Co. Ltd, and Ningxia Jinyuyuan Chemical Group Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Favorable Demand from Steel Industry Across the World

- 4.1.2 Increase in Demand for Chemical Production

- 4.2 Restraints

- 4.2.1 Detrimental Effect of Calcium Carbide on Health

- 4.2.2 Stringent Environmental Regulations

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Application

- 5.1.1 Acetylene Gas

- 5.1.2 Calcium Cyanamide

- 5.1.3 Reducing and Dehydrating Agent

- 5.1.4 Desulfurizing and Deoxidizing Agent

- 5.1.5 Other Applications

- 5.2 End-user Industry

- 5.2.1 Chemicals

- 5.2.2 Metallurgy

- 5.2.3 Food

- 5.2.4 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Rest of North America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 Rest of the World

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Alzchem Group AG

- 6.4.2 American Elements

- 6.4.3 Carbide Industries LLC

- 6.4.4 China Salt Inner Mongolia Chemical Co. Ltd

- 6.4.5 DCM Shriram

- 6.4.6 Denka Company Limited

- 6.4.7 Hongda Xingye Co. Ltd

- 6.4.8 Inner Mongolia Baiyanhu Chemical Co. Ltd

- 6.4.9 Merck KGaA (Sigma-Aldrich)

- 6.4.10 NGO Chemical Group Ltd

- 6.4.11 Ningxia Jinyuyuan Chemical Group Co. Ltd

- 6.4.12 Ningxia Yinglite Chemical Co. Ltd

- 6.4.13 Xiahuayuan Xuguang Chemical Co. Ltd

- 6.4.14 Xinjiang Tianye (Group) Co. Ltd

- 6.4.15 Xinjiang Zhongtai Chemical Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Downstream Applications of Acetylene and Its Derivatives

全球碳化钙市场(按产品类型、应用、最终用途和分销管道)预测 2025-2032

全球碳化钙市场(按产品类型、应用、最终用途和分销管道)预测 2025-2032 2025年碳化钙全球市场报告

2025年碳化钙全球市场报告 全球碳化钙市场需求、预测分析(2018-2034)

全球碳化钙市场需求、预测分析(2018-2034) 全球电石市场研究报告-产业分析、规模、份额、成长、趋势与预测 2025 年至 2033 年

全球电石市场研究报告-产业分析、规模、份额、成长、趋势与预测 2025 年至 2033 年 碳化钙市场规模、份额、成长分析(按形状、等级、应用、地区)- 产业预测,2024-2031 年全球碳化钙市场:未来预测(2025-2030)

碳化钙市场规模、份额、成长分析(按形状、等级、应用、地区)- 产业预测,2024-2031 年全球碳化钙市场:未来预测(2025-2030) 全球碳化钙市场规模、份额、趋势分析报告,按最终用户、按应用、按地区、展望和预测,2023-2030 年

全球碳化钙市场规模、份额、趋势分析报告,按最终用户、按应用、按地区、展望和预测,2023-2030 年 电石市场(应用:脱硫剂、乙炔气、还原剂、氰氨化钙、化学中间体等)-全球产业分析、规模、份额、成长、趋势和预测,2023-2031

电石市场(应用:脱硫剂、乙炔气、还原剂、氰氨化钙、化学中间体等)-全球产业分析、规模、份额、成长、趋势和预测,2023-2031