|

市场调查报告书

商品编码

1687830

资料中心机柜配电单元 (PDU):市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Data Center Rack Power Distribution Unit (PDU) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

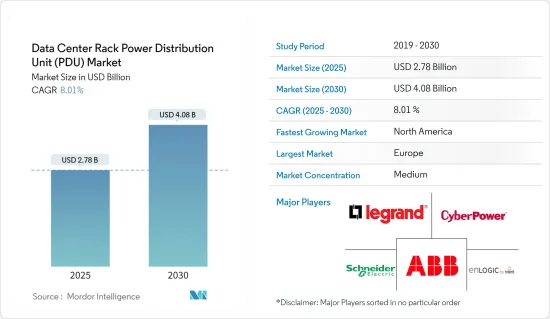

资料中心机柜配电单元(PDU)市场规模预计到 2025 年将达到 27.8 亿美元,到 2030 年将达到 40.8 亿美元,预测期内(2025-2030 年)的复合年增长率为 8.01%。

主要亮点

- 由于资料中心对高效电源管理解决方案的需求不断增加,资料中心机架 PDU 市场正在不断扩大。随着云端运算、数位化和资料驱动应用的快速发展,资料中心需要一致且扩充性的配电来支援其营运。资料中心机架 PDU 提供远端管理、即时监控和电力资源高效利用,以确保最佳效能并减少停机时间。

- 此外,人们对永续性、能源效率和成本节约的日益关注,推动了先进机架式 PDU 的采用,以便在现代资料中心基础设施中实现有效的电力使用监控和分配。

- 此外,资料中心温度的上升也推动了对冷却系统的需求,而与冷却设备相关的额外成本却在下降。然而,资料中心建筑的排气温度随着室内温度而上升。因此,必须使用额定为高环境温度的 PDU,以防止因过热而导致设备故障。由于这种背景,对耐热配电板的需求正在增加,并且预计整个预测期内资料中心机柜配电板市场将会成长。

- 硬体成本、基础设施价格和设备税使得运作资料中心的成本相对昂贵。这使得市场成长仅限于那些愿意承担建立资料中心的高昂成本的资源丰富的公司。此外,缺乏适当的监管合规性将影响市场并严重延迟企业采用主机託管。预计缺乏监管合规性将对未来五年的市场成长构成重大挑战。

资料中心机柜配电单元 (PDU) 的市场趋势

主机代管业务占据主要市场占有率

- 资料中心,尤其是主机託管资料中心的增加将对资料中心机架PDU市场产生正面影响。随着越来越多的企业选择将其IT基础设施集中安置在一起以利用成本节约、扩充性和共用资源,对支援这些设施的机架 PDU 的需求也可能会增加。

- 几十年来,机架配电单元 (PDU) 一直是资料中心配电架构的重要组成部分。在主机託管环境中,这些 PDU 为最终用户提供了多种好处,包括提高营运效率、增强 IT 设备的监控和安全性。

- 据Cloudscene称,截至2022年1月,美国共有2701个资料中心,德国共有487个资料中心。到 2024 年 2 月,德国将成为欧洲资料中心数量最多的国家,总合522 个资料中心。资料中心是一种容纳电脑系统并集中组织 IT业务的结构。

- 从资料中心数量来看,德国以456个资料中心位居第三,中国以443个资料中心位居第三。如此庞大的资料中心数量预计将导致PDU设备的成长。

- 过去十年来,主机託管业务取得了长足的发展,而资料中心在这一发展过程中发挥核心作用。对于许多企业(从小型到超大规模)来说,主机託管资料中心是一个有吸引力的解决方案,因为它们可以解决储存问题且无需前期成本。

- 减少整体 IT 支出的需求、对可扩展资料中心的需求不断增加以及资料中心的复杂性不断增加是主机託管业务成长的主要驱动力。

- 由于最终客户需要监控智慧电源分配单元 (PDU) 的能力以确保向所有 IT 设备供电,因此,具有从机架和设备层级监控和管理电源资料能力的智慧电源分配单元 (PDU) 越来越多地部署在主机託管中心。

- 主机託管资料中心营运商也越来越多地将这些智慧 PDU 与资料中心基础设施管理 (DCIM) 软体配对,以监控和追踪电力资料。该系统允许最终用户即时监控电力使用情况,并允许他们设定警报阈值来控制电力使用情况。这些技术进步正在推动所研究市场的需求。

预计北美将出现显着成长

- 该国正在迅速采用新技术。资料中心投资者正在寻找新的地点。全球5G网路的发展使得边缘资料中心在美国变得越来越重要。许多美国营运商已经开始投资这些设施,包括 EdgePresence、EdgeMicro 和 American Towers。

- 据Cisco称,美国的行动资料流程量随着时间的推移而显着增长,从2017年的每月1.26Exabyte增加到2022年的每月7.75Exabyte。而爱立信公司则表示,预计到2030年,这笔资料流将会成长两倍。要方便地连结如此大规模,必须确保低延迟和高频宽要求。因此,分散式云开始兴起。这刺激了日本资料中心对机架式PDU的需求。

- 此外,美国个人和组织的网路使用量正在迅速增长。中国是最大的资料中心营运市场,并且由于终端用户资料消费的增加而持续扩大。物联网的兴起推动了美国超大型资料中心市场的发展,推动了新设施的建设,以处理消费者和商业用户产生的Exabyte资料。

- 由于对高效资料中心的需求不断增长、努力提供环保资料中心解决方案以及该地区电力密度的显着提高,加拿大也在不断扩展和提供资料中心基础设施解决方案。这为资料中心机架PDU市场创造了庞大的商机。

- 资料中心机架 PDU 市场的成长与各市场参与者在国内投资资料中心推出与资料中心扩建直接相关。预计未来资料中心机架PDU市场将大幅成长。此外,农业、製造业和城市等活跃产业也越来越多地采用物联网平台,这也津贴了资料消耗的增加,从而刺激了加拿大对资料中心的需求。预计此类发展将在预测期内促进市场发展。

资料中心机柜配电单元 (PDU) 市场概览

资料中心机柜配电单元(PDU)市场的特点是产品种类多样且整合鬆散。然而,Schneider Electric、Enlogic、罗格朗、CyberPower Systems和ABB集团等知名供应商在不同地区被视为资料中心机架PDU供应商。

2023 年 6 月,坎普尔地铁选择了 ABB 印度的电气化解决方案,以确保安全、可靠且高品质的配电。 ABB 的最尖端科技在确保乘客无缝、舒适的通勤体验方面发挥关键作用。 ABB 印度公司对印度微系统公司的贡献包括为印度各地的 13 个地铁计划提供电气化解决方案。

2023年5月,罗格朗推出业界新一代智慧机架PDU,PRO4X和PX4。这些创新产品结合了 Raritan 和 Server Technologies 机架 PDU 迄今为止的最佳硬体和软体技术,同时引入了突破性的功能和一流的硬件,以增强可视性和安全性。值得注意的是,它是第一个估算设备和机柜层级的总谐波失真的机架 PDU,为资料中心营运商提供包括波形撷取功能在内的准确、全面的内部电能品质监控。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

- 主要市场研究结果

- 分析师对当前市场情势的评论

- 世界领先的主机託管和超大规模热点

第四章 市场动态与洞察

- 市场概况

- 市场驱动因素

- 超大规模资料中心投资持续推动智慧 PDU 安装需求

- 业界对软体定义资料中心的电力可用性和需求的要求

- 对边缘资料中心的需求

- 市场挑战

- 更新生命週期比资料中心寿命快

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争对手之间的竞争强度

- 替代品的威胁

- 市场机会

- 资料中心建置增加

- 资料中心 PDU 的演变符合流行格式

- 主要 PDU 基础设施部分分析 - 机架、地板、母线槽

第五章 市场区隔

- 按建筑

- 智慧型PDU

- 传统/基本 PDU

- 按应用

- 搭配

- 企业

- 云端基础

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 亚洲

- 中国

- 印度

- 日本

- 东南亚

- 拉丁美洲

- 中东和非洲

- 北美洲

第六章 竞争格局

- 公司简介

- Schneider Electric SE

- Enlogic by nVent

- Legrand

- Cyber Power Systems

- ABB Ltd

- Aten International Co. Ltd

- Vertiv Group Corp.

- Eaton

- Conteg Spol. SRO

- Rittal GmbH & Co. KG

第七章投资分析

第八章:未来市场展望

The Data Center Rack Power Distribution Unit Market size is estimated at USD 2.78 billion in 2025, and is expected to reach USD 4.08 billion by 2030, at a CAGR of 8.01% during the forecast period (2025-2030).

Key Highlights

- The data center rack PDU market is increasing due to the rising demand for efficient power management solutions in data centers. With the rapid development of cloud computing, digitalization, and data-driven applications, data centers need consistent and scalable power distribution to support their operations. Data center rack PDUs offer remote management, real-time monitoring, and efficient utilization of power resources that ensure optimal performance and lower downtime.

- Additionally, the increasing focus on sustainability, energy efficiency, and cost savings further drives the adoption of advanced rack PDUs, which enable effective power usage monitoring and distribution in modern data center infrastructures.

- Further, the need for cooling systems increases with rising temperatures in data centers, which lowers additional costs related to equipment cooling. However, the exhaust temperature is also growing along with the indoor temperature in data center buildings. Therefore, it is essential to use PDUs with high ambient temperature specifications to prevent equipment failures brought on by overheating. These previously mentioned elements have increased demand for high-rated power distribution units, which is anticipated to drive the growth of the data center rack power distribution unit market throughout the forecast period.

- Hardware costs, infrastructure prices, and taxes over equipment have been amounting to relatively expensive data center running costs. This has limited the market's growth to highly-resourced firms to absorb higher costs with the data center setups. Further, a lack of proper regulatory compliance will affect the market and greatly slow down the adoption of colocation among companies. Lack of regulatory compliance is expected to be a major challenge for the market's growth over the next five years.

Data Center Rack Power Distribution Unit (PDU) Market Trends

Colocation Segment Holds Significant Market Share

- The growth in the number of data centers, especially colocation data centers, positively impacts the data center rack PDU market. As more businesses choose to colocate their IT infrastructure to take advantage of cost savings, scalability, and shared resources, the demand for rack PDUs to support these facilities will likely increase.

- For decades, rack power distribution units (PDUs) have been an integral part of power distribution architectures in data centers. In the colocation environment, these PDUs provide the end customers with several benefits, such as enhanced operational efficiency, increased monitoring, and security of their IT equipment.

- According to Cloudscene, as of January 2022, there were 2,701 data centers in the United States and 487 in Germany. The United By February 2024, Germany had the highest number of data centers among all European countries, with a total of 522 facilities. Data centers are structures that store computer systems and consolidate an organization's collective IT operations.

- ranked third among countries in the number of data centers, with 456, while China recorded 443. Such a huge number of data centers is expected to create growth for PDU equipment.

- The colocation business has evolved significantly over the past ten years, with the role of the data center being central to that evolutionary process. Since its inception, colocation data centers have been an attractive solution to many small-scale and hyperscale players equally, as it allows organizations to address their storage issues without substantial upfront costs.

- The need to reduce the overall IT expenditure, the rising requirement for scalable data centers, and the growing data center complexities are the major drivers for the growth of the colocation business.

- Intelligent power distribution units (PDUs) that possess the ability to monitor and manage power data from the rack and device level are increasingly being deployed in the colocation centers, owing to the end customers' need to monitor the capability of PDUs to ensure the availability of power to all their IT equipment.

- Operators of colocation data centers are also increasingly deploying data center infrastructure management (DCIM) software to pair with these intelligent PDUs to monitor and track power data. This system also enables the end customers to monitor their power usage in real time and provides the ability to establish alarm thresholds to control the usage of power. Such advancements in technology are driving the demand for the market studied.

North America is Expected to Register Significant Growth

- Newer technologies are quickly adopted in the country. Investors in data centers are increasingly finding new locations. The worldwide development of 5G networks, of which the United States is one of the early adopters, has boosted the significance of edge data centers. Many American operators, including EdgePresence, EdgeMicro, and American Towers, have begun making investments in these facilities.

- According to Cisco Systems, the amount of mobile data traffic in the United States has grown significantly over time, from 1.26 exabytes of data traffic per month in 2017 to 7.75 exabytes per month by 2022. This data flow is anticipated to triple by 2030, according to Ericsson. In order to link such scale conveniently, low latency and high bandwidth requirements must be secured. As a result, the distributed cloud is starting to operate. Which has fueled the demand for data center rack PDUs in the country.

- Furthermore, Internet usage by individuals and organizations is rapidly increasing in the United States. The nation is the largest market for data center operations, and it is still expanding as a result of increased end-user data consumption. The market for US hyper-scale data centers is being significantly fueled by the rising IoT, which is encouraging the construction of new facilities to handle the exabytes of data generated by consumers and commercial users.

- Canada is also constantly expanding and offering more data center infrastructure solutions due to rising demand for efficient data centers, initiatives to provide environmentally friendly data center solutions, and a significant increase in power density in the region. Which has created significant opportunities for the data center rack PDU market.

- The growth of the data center rack PDU market is directly related to the launch of data centers and various market players investing in the data center expansion country. The data center rack PDU market is anticipated to flourish. Additionally, Augmented use of IoT platforms by variable sectors, such as agriculture, manufacturing, and cities, has subsidized the increasing data consumption, which has activated the demand for data centers in Canada. Such developments are also expected to aid the growth of the studied market during the forecast period.

Data Center Rack Power Distribution Unit (PDU) Market Overview

The data center rack PDU market features moderate consolidation with a diverse range of products available. However, prominent vendors such as Schneider Electric, Enlogic, Legrand, Cyber Power Systems, and ABB Group, among others, are highly preferred providers of data center rack PDUs across various regions.

In June 2023, the Kanpur Metro chose ABB India's Electrification solutions for ensuring safe, reliable, and high-quality power distribution. ABB's cutting-edge technology plays a pivotal role in ensuring a seamless and comfortable commuting experience for passengers. ABB India's contribution to the Indian Microsystems includes providing electrification solutions to 13 metro rail projects across India.

In May 2023, Legrand introduced the industry's next generation of intelligent rack PDUs, the PRO4X and PX4. These innovative products combine the best hardware and software technologies from previous Raritan and Server Technology rack PDUs while introducing groundbreaking features and top-tier hardware for enhanced visibility and security. Notably, they are the first rack PDUs to estimate total harmonic distortion at both the device and cabinet levels, offering data center operators precise and comprehensive internalized power quality monitoring, including waveform capture capabilities.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

- 3.1 Key Market Findings

- 3.2 Analyst Commentary on the Current Market Scenario

- 3.3 Key Colocation and Hyperscale Hotspots Worldwide

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Investments in Hyperscale DCs Continues to Spur Demand for Smart PDU Installations

- 4.2.2 Industry Mandates Related to Power Availability and Demand for Software-Defined Data Centers

- 4.2.3 Demand for Edge Data Centers

- 4.3 Market Challenges

- 4.3.1 Faster Refresh Life Cycle than Data Center Profitable Life Expectancy

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Intensity of Competitive Rivalry

- 4.4.5 Threat of Substitutes

- 4.5 Market Opportunities

- 4.5.1 Rise in Data Center Construction

- 4.6 Evolution of Data Center PDUs Along a Continuum

- 4.7 Analysis of the Major PDU Infrastructure Segments - Rack, Floor-based, and Busways

5 MARKET SEGMENTATION

- 5.1 By Construction

- 5.1.1 Smart PDU

- 5.1.2 Traditional/Basic PDU

- 5.2 By Application

- 5.2.1 Colocation

- 5.2.2 Enterprise

- 5.2.3 Cloud-Based

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.3 Asia

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Southeast Asia

- 5.3.4 Latin America

- 5.3.5 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Schneider Electric SE

- 6.1.2 Enlogic by nVent

- 6.1.3 Legrand

- 6.1.4 Cyber Power Systems

- 6.1.5 ABB Ltd

- 6.1.6 Aten International Co. Ltd

- 6.1.7 Vertiv Group Corp.

- 6.1.8 Eaton

- 6.1.9 Conteg Spol. S R O

- 6.1.10 Rittal GmbH & Co. KG

7 INVESTMENT ANALYSIS

8 FUTURE OUTLOOK OF THE MARKET

2026年全球资料中心机柜与机柜市场报告

2026年全球资料中心机柜与机柜市场报告 全球智慧机架式电源分配单元 (PDU) 市场预测至 2034 年:按 PDU 类型、功能、插座类型、资料中心类型、通讯介面、最终用户和地区划分

全球智慧机架式电源分配单元 (PDU) 市场预测至 2034 年:按 PDU 类型、功能、插座类型、资料中心类型、通讯介面、最终用户和地区划分 资料中心机柜配电单元市场 - 全球产业规模、份额、趋势、机会、预测:测量与监控、部署模式、功率容量、区域及竞争格局,2021-2031年

资料中心机柜配电单元市场 - 全球产业规模、份额、趋势、机会、预测:测量与监控、部署模式、功率容量、区域及竞争格局,2021-2031年 机架式伺服器市场 - 2026-2031 年预测机架式伺服器市场 - 全球产业规模、份额、趋势、机会和预测,按外形尺寸、价格范围、最终用户产业、地区和竞争格局划分,2021-2031 年预测

机架式伺服器市场 - 2026-2031 年预测机架式伺服器市场 - 全球产业规模、份额、趋势、机会和预测,按外形尺寸、价格范围、最终用户产业、地区和竞争格局划分,2021-2031 年预测 日本资料中心机架市场报告(按类型、机架单元、机架尺寸、框架尺寸、框架设计、服务、应用、最终用户和地区划分,2026-2034 年)

日本资料中心机架市场报告(按类型、机架单元、机架尺寸、框架尺寸、框架设计、服务、应用、最终用户和地区划分,2026-2034 年) 全球资料中心趋势(2026):机架式解决方案

全球资料中心趋势(2026):机架式解决方案 互联网资料中心(IDC)机柜:全球市场份额和排名、总收入和需求预测(2025-2031年)

互联网资料中心(IDC)机柜:全球市场份额和排名、总收入和需求预测(2025-2031年) IT 配电单元市场(按类型、额定功率、相位、安装类型和最终用户产业)—2025-2030 年全球预测ORV3 机架市场按产品类型、机架高度、组件、部署模型、应用和销售管道划分 - 2025-2030 年全球预测

IT 配电单元市场(按类型、额定功率、相位、安装类型和最终用户产业)—2025-2030 年全球预测ORV3 机架市场按产品类型、机架高度、组件、部署模型、应用和销售管道划分 - 2025-2030 年全球预测