|

市场调查报告书

商品编码

1687898

C-RAN:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)C-RAN - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

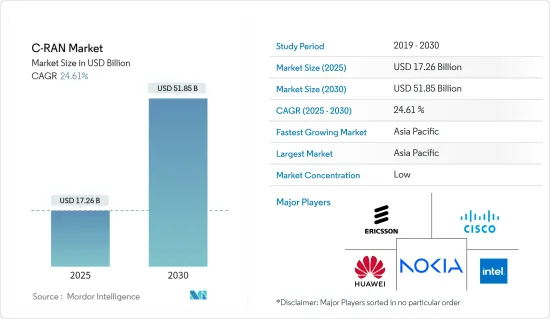

2025 年 C-RAN 市场规模预计为 172.6 亿美元,预计到 2030 年将达到 518.5 亿美元,预测期内(2025-2030 年)的复合年增长率为 24.61%。

在预计预测期内,资本支出的激增和营运支出的下降将推动云端无线接取网路市场的发展。此外,无线和通讯技术的不断升级将提高4G和5G的可及性,为市场成长提供光明前景。

主要亮点

- 5G 技术的不断进步也在推动 Cloud RAN 市场的发展方面发挥关键作用。 5G网路需要更高的容量、更低的延迟和更佳的网路效能,这与C-RAN架构提供的功能非常契合。 C-RAN 支援具有集中处理和先进无线资源管理的 5G 网路部署,可协助营运商充分发挥 5G 技术的潜力,提供卓越的使用者体验。

- 此外,行动通讯业者RAN 网路预计将向云端基础的RAN 解决方案大幅发展。现实中,Cloud RAN将需要与拥有自己专用基频的Classic RAN共存于网路中,因此大多数营运商在迈向6G的道路上将采用混合策略。

- 物联网 (IoT) 正在推动各个领域的连网型设备的发展,包括智慧城市、医疗保健、农业和製造业。 5G网路正在建置中,旨在同时连接数十亿台物联网设备,实现大规模连接。 5G 网路得益于其 C-RAN 架构,具有更高的扩充性和灵活性,可实现物联网应用的无缝整合。 C-RAN 透过提供动态资源配置来满足不断变化的连接需求、实现软体定义网路 (SDN) 的理念以及集中管理业务,从而简化了物联网流量管理。

- C-RAN可以显着降低维护和部署无线网路的成本。透过整合基频处理的用途,C-RAN 消除了每个基地台对专用硬体的需求,从而减少了设备需求。此外,透过使用SDN(软体定义网路)和虚拟技术,可以更有效地利用资源,有望进一步降低成本。

- 我们这个快速发展的互联互通的世界正在推动对无线通讯的需求。从智慧型手机到智慧家庭、自动驾驶汽车到工业物联网设备,对安全、高速无线网路的需求从未如此强烈。此外,随着网路连线需求的成长,频谱稀缺的挑战也随之增加,这意味着可用于传输行动资料的无线电频率数量有限。

云端无线接取网路市场趋势

5G将成为成长最快的网路类型

- C-RAN 将透过降低硬体和营运成本,使营运商能够更经济高效地部署 5G 网路。随着高速行动连线的需求不断增长,尤其是物联网设备、自动驾驶汽车、扩增实境和其他新兴技术的普及,5G C-RAN 市场预计将在未来几年大幅成长。

- 5G固定无线存取的日益普及可能会在预测期内推动市场的发展。图表显示,分析显示5G连接数将达到惊人的53亿,从而促进市场成长率。

- 按地区划分,北美在全球占有主要份额。 5G技术正在被广泛采用,尤其是在云端无线接取网路(C-RAN)市场。 C-RAN 利用云端运算来集中和虚拟基频功能,提供灵活性和扩充性。

- 5G的高资料速率、低延迟和海量连接能力使其非常适合C-RAN部署,从而提高网路效能并支援物联网和扩增实境等先进服务。 5G和C-RAN的结合将推动整个北美通讯业的创新和效率。

- 2023 年 12 月,AT&T 宣布计画成为美国领先的商业规模开放无线接取网路(Open RAN) 部署供应商。透过与爱立信合作,这项产业倡议将加速通讯业的发展,并有助于建立更强大的网路基础设施供应商和供应商生态系统。 AT&T 和爱立信对 Open RAN 部署的多年共同承诺正值 5G 创新週期的关键时刻。

亚太地区预计将经历最快成长

- 推动中国 C-RAN 市场发展的因素有几个,首先中国拥有华为、中兴等多家主要企业,其次中国拥有蓬勃发展的 C-RAN 生态系统。随着中国积极部署5G网络,C-RAN被视为实现高效网络效能和支援多样化5G用例的关键技术。

- 在中国,5G行动网路的广泛部署将支援许多不同类型的服务,包括医疗保健、汽车、物流、能源和公共。网路切片可以实现可编程的网路实例,以满足各个使用案例、用户类型和应用程式的要求。

- 从网路类型来看,5G网路成长速度显着。这种成长归因于多种因素,包括对高速连接、软体定义网路、虚拟、技术进步和产业协作的需求不断增加。日本政府最近一直在寻求透过支援开放无线存取网路 (RAN) 技术来促进安全 5G通讯网路的部署。

- 其他亚太地区通讯业者正在积极采用 C-RAN 结构和网路虚拟来应对不断上升的部署成本。近年来,随着区域通讯业者寻求健康的经营模式以及设备供应商尝试重组以更好地适应其业务,融合无线接取网路的重要性日益增加。印度、韩国和马来西亚等国家正在开发 C-RAN 架构,以有效满足不断增长的客户需求。

云端无线接取网路产业概览

云端无线接取网路市场较为分散,竞争对手之间的竞争非常激烈,策略联盟显着增加。来自买家的需求正在推动现有企业投资解决方案并保留合约。市场的主要企业包括思科系统公司、诺基亚公司、华为科技公司、爱立信公司和英特尔公司。

- 2023 年 10 月,诺基亚和 Elisa 宣布他们已经完成了业界首次使用内联加速的 Cloud RAN 试验。此次试验在芬兰 Elisa 总部进行,利用了该公司的商用 5G 独立 RAN 和 5G Core。此试验主要基于诺基亚的 anyRAN 方法,旨在确保 Cloud RAN 与专用 RAN 相比功能丰富、节能高效且效能优异。透过内联第 1 层 (L1) 加速,可以确保上述每个方面,并可以灵活地在 x86 和基于 ARM 的生态系统之间进行选择。

- 2023年9月,爱立信与Google扩大了与Google云端的合作,在Google分散式云端(GDC)上开发爱立信的Cloud RAN解决方案。爱立信表示,在 GDC 上开发爱立信 Cloud RAN 的伙伴关係旨在提供整合自动化和编配,利用 AI/ML 为通讯服务供应商带来利益。合作伙伴在位于加拿大渥太华的爱立信OpenLab的即时网路上运行此解决方案,并成功展示了爱立信vDU(虚拟分散式单元)和vCU(虚拟中央单元)在GDC Edge上的完整实作。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 市场驱动因素与限制因素简介

- 市场驱动因素

- 各个终端使用者群体对 5G 趋势的需求不断增加

- 需要降低4G-5G网路使用的硬体设备成本

- 市场限制

- 网路扩展所需频宽不足,加上监管限制

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 购买者/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 技术简介

- 云端虚拟

- 集中式 RAN

第五章 市场区隔

- 按组件

- 解决方案

- 服务

- 专业的

- 託管

- 依网路类型

- 5G

- 4G

- LTE

- 3G(EDGE)

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 其他亚太地区

- 拉丁美洲

- 中东和非洲

- 北美洲

第六章 竞争格局

- 公司简介

- Cisco System Inc.

- Nokia Corporation

- Huawei Technologies Co. Ltd

- Telefonaktiebolaget LM Ericsson

- Intel Corporation

- Fujitsu Limited

- Mavenir Systems Inc.

- Artiza Networks Inc.

第七章投资分析

第 8 章:市场的未来

The C-RAN Market size is estimated at USD 17.26 billion in 2025, and is expected to reach USD 51.85 billion by 2030, at a CAGR of 24.61% during the forecast period (2025-2030).

The rapid increase in capital expenditure and reduction in operational spending is expected to drive the Cloud Radio Access Network Market over the forecasted years. Also, the increasing upgrade in wireless and telecommunication technology improves 4G and 5G accessibility, thereby imposing a positive outlook on market growth.

Key Highlights

- The constant advancements in 5G technology also play a key role in driving the Cloud RAN market. 5G networks require increased capacity, low latency, and enhanced network performance, which align well with the abilities offered by C-RAN architecture. C-RAN enables the deployment of 5G networks with its centralized processing and progressive radio resource management, allowing operators to unlock the complete potential of 5G technology and provide a superior user experience.

- Furthermore, mobile operator RAN networks are expected to evolve significantly toward Cloud-based RAN solutions. In practice, most operators will adopt a hybrid strategy during the journey toward 6G simply because Cloud RAN will have to co-exist in the network with Classic RAN with a purpose-built baseband.

- The Internet of Things (IoT) is driving the development of connected devices across different sectors, such as smart cities, healthcare, agriculture, and manufacturing. To connect billions of IoT devices at once, 5G networks are being built, enabling massive connectivity. 5G networks are made more scalable and flexible by C-RAN architecture, which makes it likely to integrate IoT applications with them seamlessly. C-RAN provides dynamic resource provision to meet changing connectivity needs and rationalizes IoT traffic management by putting software-defined networking (SDN) ideas into practice and centralizing management operations.

- C-RAN can significantly decrease the cost of maintaining and deploying a wireless network. By consolidating the baseband processing purposes, C-RAN removes the requirement for dedicated hardware at each base station, decreasing the need for equipment. In addition, using software-defined networking (SDN) and virtualization technologies enables more efficient utilization of resources, further reducing costs.

- The demand for wireless communication is rising in a rapidly connected world. The need for a secure and fast wireless network has never been more critical, from smartphones to smart homes, from autonomous cars to Industrial Internet of Things devices. The challenge of spectrum scarcity, the limited number of radio frequencies that can be used to transmit mobile data, also increases with increasing demand for Internet connectivity.

Cloud Radio Access Network Market Trends

5G to be the Fastest Growing Network Type

- C-RAN enables operators to deploy 5G networks more cost-effectively by reducing hardware and operational costs, along with demand for high-speed mobile connectivity continues to rise, especially with the proliferation of IoT devices and emerging technologies like autonomous vehicles and augmented reality, the market for 5G C-RAN is expected to grow significantly in the coming years.

- The rise in adopting 5G fixed wireless access would drive the studied market over the forecasted period. The graph indicates that the 5G connections are analyzed to reach a notable 5.3 billion subscriptions, thereby contributing to the market growth rate.

- By geography, the North American region has a substantial share globally. 5G technology is widely adopted, particularly in the Cloud Radio Access Network (C-RAN) market. C-RAN leverages cloud computing to centralize and virtualize baseband processing functions, offering flexibility and scalability.

- With 5G's high data rates, low latency, and massive connectivity capabilities, it is well-suited to C-RAN deployments, enhancing network performance and enabling advanced services like IoT and augmented reality. This combination of 5G and C-RAN drives innovation and efficiency in the telecommunications industry across North America.

- In December 2023, AT&T announced plans to be a key provider in the United States in commercial-scale open radio access network (Open RAN) deployment. In collaboration with Ericsson, this industry move will further the telecommunications industry efforts and help build a more robust ecosystem of network infrastructure providers and suppliers. AT&T's and Ericsson's multiyear joint commitment to Open RAN deployment comes at a pivotal moment in the 5G innovation cycle.

Asia-Pacific is Expected to Register the Fastest Growth

- Several factors drive the C-RAN market in China as the country has a thriving domestic C-RAN ecosystem with several significant players, such as Huawei and ZTE. China is aggressively deploying 5G networks, and C-RAN is considered a key technology to allow efficient network performance and support diverse 5G use cases.

- In China, the widespread adoption of 5G mobile networks is supporting various service types, such as healthcare, automotive, logistics, energy, and public safety. Network slicing enables programmable network instances that match the requirements of individual use cases, subscriber types, and applications.

- By network type, the 5G network is growing at a considerable rate. This growth is attributed to several factors, including increased demand for high-speed connectivity, software-defined networking, virtualization, technological advancements, and industry collaboration. The Japanese government has been trying significantly to promote the deployment of secure 5G telecommunications networks in recent years by supporting open radio access network (RAN) technology, which can further accommodate better vendor flexibility when building those networks.

- Operators in the Rest of Asia-Pacific region are actively embracing C-RAN structure and network virtualization to tackle increasing deployment costs. Centralized radio access networks have gained increased significance in recent years as regional operators seek sound business models and equipment vendors try to reshape the landscape to suit their businesses. Countries such as India, South Korea, and Malaysia are developing C-RAN architectures to cater to growing customer demands effectively.

Cloud Radio Access Network Industry Overview

The cloud radio access network market is fragmented, and the intensity of competitive rivalry is high due to the significant growth in strategic collaborations. The demand from the buyers has actively led the incumbents to invest in solutions and keep the contracts intact; some of the key players in the market are Cisco Systems Inc., Nokia Corporation, Huawei Technologies Co. Ltd, Telefonaktiebolaget LM Ericsson, and Intel Corporation.

- In October 2023, Nokia and Elisa declared that they had completed the industry's first trial of Cloud RAN, which was powered by In-Line acceleration. The successful trial occurred at Elisa's headquarters in Finland, where it utilized its commercial 5G Standalone RAN and 5G Core. The trial mainly builds on Nokia's anyRAN approach, which was established to ensure the feature richness, energy efficiency, and high performance of Cloud RAN compared to purpose-built RAN. Using In-Line layer 1 (L1) acceleration ensures each of these aspects while allowing flexibility to select between x86 and ARM-based ecosystems.

- In September 2023, Ericsson and Google expanded their partnership with Google Cloud to develop an Ericsson Cloud RAN solution on Google Distributed Cloud (GDC). As per Ericsson, the partnership to develop an Ericsson Cloud RAN on GDC aims to offer integrated automation and orchestration and leverage AI /ML for communications service providers to benefit from. The partners successfully demonstrated the complete implementation of the Ericsson vDU (virtualized distributed unit) and vCU (virtualized central unit) on GDC Edge, running the solution on a live network in the Ericsson Open Lab in Ottawa, Canada.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Introduction to Market Drivers and Restraints

- 4.3 Market Drivers

- 4.3.1 Rising Demand of 5G Trend Across Various End-user Segment

- 4.3.2 Need to Eliminate the Cost of Hardware Equipment Used in 4G-5G Network

- 4.4 Market Restraints

- 4.4.1 Scarce Spectrum Availability for Network Expansion When Combined With Regulatory Limits

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Technology Snapshot

- 4.6.1 Cloud-Virtualization

- 4.6.2 Centralized-RAN

5 MARKET SEGMENTATION

- 5.1 By Components

- 5.1.1 Solution

- 5.1.2 Services

- 5.1.2.1 Professional

- 5.1.2.2 Managed

- 5.2 By Network Type

- 5.2.1 5G

- 5.2.2 4G

- 5.2.3 LTE

- 5.2.4 3G (EDGE)

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.5 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Cisco System Inc.

- 6.1.2 Nokia Corporation

- 6.1.3 Huawei Technologies Co. Ltd

- 6.1.4 Telefonaktiebolaget LM Ericsson

- 6.1.5 Intel Corporation

- 6.1.6 Fujitsu Limited

- 6.1.7 Mavenir Systems Inc.

- 6.1.8 Artiza Networks Inc.

7 INVESTMENT ANALYSIS

8 FUTURE OF THE MARKET

云端无线接取网路市场(按组件、部署类型和最终用户)-全球预测,2025-2032

云端无线接取网路市场(按组件、部署类型和最终用户)-全球预测,2025-2032 云端无线接取网路(C-RAN) 市场分析及预测(至 2034 年):类型、产品、服务、技术、元件、应用、部署、最终用户和功能

云端无线接取网路(C-RAN) 市场分析及预测(至 2034 年):类型、产品、服务、技术、元件、应用、部署、最终用户和功能 全球云端化无线存取网路(C-RAN) 市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测全球云端无线接取网路市场规模(按技术、网路类型、部署区域、区域范围和预测)

全球云端化无线存取网路(C-RAN) 市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测全球云端无线接取网路市场规模(按技术、网路类型、部署区域、区域范围和预测) 2025年云端无线接取网路全球市场报告C-RAN 市场规模、份额、趋势分析报告:按元件、按网路类型、按架构类型、按部署模型、按地区、按细分市场、预测,2025-2030 年

2025年云端无线接取网路全球市场报告C-RAN 市场规模、份额、趋势分析报告:按元件、按网路类型、按架构类型、按部署模型、按地区、按细分市场、预测,2025-2030 年 宏蜂窝无线电单元/主动天线单元(RU/AAU)供应商全球市场占有率分析(2022-2023)(第6版)

宏蜂窝无线电单元/主动天线单元(RU/AAU)供应商全球市场占有率分析(2022-2023)(第6版) 宏蜂窝无线电单元/主动天线单元(RU/AAU)全球市场分析与预测(2024-2028)(第6版)

宏蜂窝无线电单元/主动天线单元(RU/AAU)全球市场分析与预测(2024-2028)(第6版) 云端无线存取网路(C-RAN) 市场、份额、市场规模、趋势、产业分析报告:按组件、按网路类型、按部署、按最终用户、按地区、按细分市场、预测,2024-2032年

云端无线存取网路(C-RAN) 市场、份额、市场规模、趋势、产业分析报告:按组件、按网路类型、按部署、按最终用户、按地区、按细分市场、预测,2024-2032年