|

市场调查报告书

商品编码

1687914

MEMS-市场占有率分析、产业趋势与统计、成长预测(2025-2030)MEMS - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

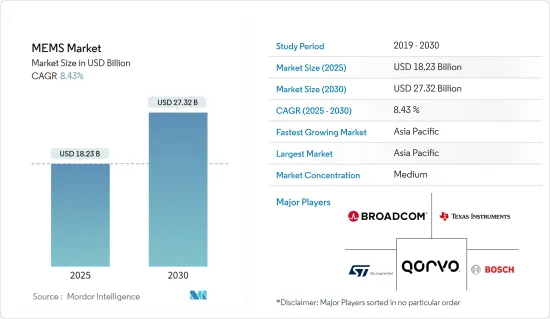

预计 2025 年 MEMS 市场规模为 182.3 亿美元,到 2030 年将达到 273.2 亿美元,预测期内(2025-2030 年)的复合年增长率为 8.43%。

由于从汽车到家用电子电器等各种应用对 MEMS 的需求不断增加,MEMS 领域正在经历快速成长。

关键亮点

- 电子机械系统 (MEMS) 感测器因其在准确性、可靠性和电子设备小型化方面的优势,近年来获得了极大的普及。推动 MEMS 市场发展的关键因素是工业自动化以及对小型化消费性设备(如穿戴式装置和物联网连网型设备)的需求。

- 全球对物联网设备的需求不断增长,推动了 MEMS 在这些设备中的采用率。结合小型化的趋势,连网型设备也将受益。根据思科系统公司预测,2022年,连网型设备数量预计将达到11.05亿台,领先市场。

- 此外,预计未来几年工业对物联网的需求将超过对连网型设备的需求,所需的连网型设备数量将非常庞大,工业领域的采用率也将不断上升。根据 GSMA 预测,到 2025 年,连网工业设备的数量预计将超过连网消费设备的数量。在 2021 年国际消费电子展 (CES) 上,TDK 公司推出了一系列用于工业应用的 MEMS 平台和感测器。

- 然而,市场面临着产品生产和缺乏标准化製造流程的挑战。考虑到汽车产业使用的感测器的介面设计,MEMS 会产生微小的电容变化。这必须精确且准确地完成,从而延长製造产品的前置作业时间并略微抵消市场成长。

- 消费和汽车应用中的持续感测器化、医疗和工业终端市场以及相关应用的进步是推动市场成长的关键因素。 MEMS 感测器的空前需求促使许多 MEMS 製造商投资新的生产设施。例如,博世已宣布计划在 2022 年投资超过 4 亿欧元(4.2607 亿美元),扩建其位于德国德勒斯登和罗伊特林根的晶圆厂以及位于马来西亚槟城的半导体业务。作为投资的一部分,该公司将分两个阶段在罗伊特林根新增总合超过 4,000平方公尺的无尘室空间,现有无尘室面积为 35,000平方公尺。第一期工程已完工,新增200毫米晶圆生产面积1,000平方公尺,总合达11,500平方公尺。

- 除此之外,COVID-19 加速了以患者为中心的医疗方法的步伐,增加了对远端患者监护,包括远端医疗、照护现场设备和穿戴式装置。人们对能够追踪患者体温和血压的可穿戴设备的需求日益增长。这一趋势为穿戴式装置市场以及压力、惯性、麦克风和热电堆等整合式 MEMS 感测器创造了新的机会。

MEMS市场趋势

消费性电子应用领域预计将占据主要市场占有率

- MEMS 技术已经改进了几项重要的通讯、医疗和生物技术应用,但其在家用电子电器中的应用对未来的发展具有巨大的潜力。 MEMS 广泛应用于从智慧型手机到其他消费品等各种各样的产品中,并渗透到人们的日常生活中。

- 由于MEMS在高频下电气性能的提高,MEMS被广泛应用于智慧型手机、穿戴式装置和其他电子设备。由于消费电子领域的兴趣从传统感测器转向 MEMS 技术,预计市场将会成长。作为MEMS的主要技术驱动力,以智慧型手机为代表的家用电子电器正逐步取代汽车应用。

- 加速计和陀螺仪是智慧型手机中最突出的两种 MEMS(微电子机械系统)应用。智慧型手机中多种用于各种感测器和致动器应用的晶片的普及是 MEMS 市场爆炸式增长的主要驱动力之一。由于智慧型手机销售和商业机会的增加,预计预测期内行动装置的 MEMS 市场将大幅扩张。

- 例如,根据爱立信移动2022年第四季的报告,到2022年第四季度,全球行动用户普及率将达到106%。该公司本季净增加3,900万用户,使2022年第四季的行动用户总数超过84亿人。预计 MEMS 设备的需求将会上升,为供应商提供各种机会以扩大市场占有率并满足智慧型手机对 MEMS 日益增长的需求。

- 智慧型手机使用由 MEMS 感测器支援的光学影像稳定 (OIS) 和电子影像稳定 (EIS)。预计这些广泛的功能和创新能力将在预测期内推动对 MEMS 感测器的需求,尤其是用于智慧型行动装置的感测器。

- 光学影像稳定、投影显示和指纹认证技术等技术的进步和发展对 MEMS 感测器设计产生了重大影响。技术趋势、消费者偏好和其他因素是影响家用电子电器和智慧设备电子产业发展的关键。这些模式正在推动对小型化 MEMS 感测器的需求。

亚太地区预计将占据主要市场占有率

- 亚太地区很可能主导 MEMS 市场。由于主要家用电子电器製造商进入该领域,电子机械系统 (MEMS) 市场正在不断扩大。预计智慧型手机的普及率不断提高、5G 的广泛应用以及众多终端用户行业的进步将推动市场的发展。

- 中国、韩国、日本、印度等是亚太地区的主要国家。亚太地区是MEMS感测器技术的庞大市场。该地区主导着其他终端用户行业以及全球半导体製造业的许多製造子部门行业。中国等国家正在向市场供应低成本产品。

- 例如,许多中国MEMS感测器公司,如美新半导体和深迪科技,正大力投资物联网(IoT)。中国政府将汽车产业(包括汽车零件产业)视为最重要的产业之一。中国政府预计,到2025年,中国的汽车产量将达到3,500万辆。这将使汽车产业成为中国MEMS感测器最突出的应用领域之一。中国最近指示汽车製造商到 2030 年销售的电动车 (EV) 数量比传统汽车多 40%。随着汽车行业的这些进步,MEMS 技术预计将变得越来越受欢迎。

- 随着中国汽车市场向更高水准的自动驾驶发展,对安全性和环保驾驶的要求不断提高,预计压力 MEMS 将继续成长。中国的六项法规预计将推动各种应用的发展,包括柴油微粒过滤器、汽油微粒过滤器、蒸发排放控制系统、废气再循环和轮胎压力监测系统。

- 此外,由于医疗保健领域的进步,预计亚太地区在预测期内将显着增长。政府支持医疗设备和设备市场的计画和政策,以及对研究和创新设施的投资增加,都促进了这一成长。

MEMS产业概况

MEMS 市场细分程度适中,主要企业包括 Broadcom Inc.、Robert Bosch GmBH、意法半导体 NV、德州仪器公司和 Qorvo Inc.。市场参与企业正在采用联盟和收购等策略来加强其产品供应并获得可持续的竞争优势。

- 2023年5月 - SPEA与共进微电子签章策略伙伴关係,可望加强中国当地MEMS测试与校准业务的发展。该协议将 GJM 领先的製造服务和品管能力与 SPEA 的世界级检测技术和专业知识相结合,预计将加速两家公司在中国快速成长的 MEMS 领域的成长。

- 2023 年 6 月 - Rogue Valley Microdevices 宣布已在佛罗里达州收购一座 50,000 平方英尺的商业建筑,用于其第二家微製造工厂。该空间将重新配置为无尘室和办公空间,预计将于 2025 年生产首批 MEMS 设备。扩展到棕榈湾将使该公司能够提高供应链弹性并增加产量。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- 产业价值链分析

- COVID-19 市场影响

第五章市场动态

- 市场驱动因素

- 物联网在半导体领域的日益普及

- 智慧家用电子电器需求不断成长

- 工业和家庭越来越多地采用自动化

- 市场挑战/限制

- 高度复杂的製造流程和严苛的周期时间

- MEMS 缺乏标准化製造工艺

第六章市场区隔

- 按类型

- RF MEMS

- 振盪器

- 微流体

- 环境MEMS

- 光学MEMS

- MEMS麦克风

- 惯性MEMS

- 压力MEMS

- 嗜热

- 微测辐射热计

- 喷墨头

- 加速计

- 陀螺仪

- 其他的

- 按应用

- 车

- 医疗保健

- 工业的

- 家用电子电器

- 电讯

- 航太与国防

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第七章竞争格局

- 相对定位

- MEMS供应商的相对定位

- MEMS代工厂的相对定位

- 公司简介

- Broadcom Inc.

- Robert Bosch GmBH

- STMicroelectronics NV

- Texas Instruments Inc.

- Qorvo Inc.

- Infineon Technologies AG

- Knowles Electronics LLC(Knowles Corporation)

- TDK Corporation

- NXP Semiconductors NV

- Panasonic Corporation

- GoerTek Inc.

第八章投资分析

第九章:市场的未来

The MEMS Market size is estimated at USD 18.23 billion in 2025, and is expected to reach USD 27.32 billion by 2030, at a CAGR of 8.43% during the forecast period (2025-2030).

The MEMS sector is witnessing rapid growth due to the increasing demand for MEMS in multiple applications, from automotive to consumer electronics.

Key Highlights

- Microelectromechanical system (MEMS) sensors have gained significant traction over recent years due to advantages such as accuracy, reliability, and the scope for making smaller electronic devices. Among the significant factors driving the MEMS market are industrial automation and the demand for miniaturized consumer devices, such as wearables and IoT-connected devices.

- The increasing demand for IoT devices worldwide is spearheading the adoption rate of MEMS in these devices; when coupled with the miniaturization trend, the connected devices benefit as well. According to Cisco Systems, the number of connected is expected to reach 1,105 million by 2022, thus driving the market.

- Further, industrial demand for IoT is expected to eclipse the demand for consumer-connected devices over the coming years, with the sheer number of connected devices required and adoption in the industrial space on the rise. By 2025, industrial-connected devices are expected to be more in number than consumer-connected devices, according to GSMA. At CES 2021, TDK Corp. announced the availability of its range of MEMS platforms and sensors for industrial applications.

- However, the market faces challenges in product production and a lack of a standardized fabrication process. Considering the sensor interface design used in the automotive industry, the MEMS produces capacitance changes of tiny magnitudes. This must be addressed with precision and accuracy, increasing the lead time to manufacture the products and slightly offsetting the market's growth.

- Continuous sensorization of both consumer and automotive applications and advances in the medical and industrial end markets and associated applications are important factors contributing to the market growth. Owing to the unprecedented demand for MEMS sensors, many MEMS players are currently investing in new production fabs. For instance, Bosch announced plans to invest more than EUR 400 million (USD 426.07 million) in 2022 in expanding its wafer fabs in Dresden and Reutlingen, Germany, and its semiconductor operations in Penang, Malaysia. As part of the investment, a total of more than 4,000 square meters will be added to the current 35,000 square meters of clean-room space in Reutlingen, in two stages. The first stage, which involved adding 1,000 square meters of production area for 200-millimeter wafers to bring the total to 11,500 square meters, has already been completed.

- In additoin to this, COVID-19 has also accelerated the pace towards a more patient-centric approach and increased the need for remote patient monitoring, including telehealth, point-of-care devices, and wearables. There is a growing demand for wearables owing to their ability to track peoples' temperature and blood pressure. This trend has created new opportunities in the wearables market, as well as for integrated MEMS sensors, such as pressure, inertial, microphones, thermopiles, etc.

Micro-Electro-Mechanical System Market Trends

Consumer Electronics Application Segment is Expected to Hold Significant Market Share

- MEMS technology has improved several crucial communication and medical biotechnology applications, but its use in consumer electronics holds great promise for future advancements. MEMS has ingrained itself into people's daily lives by appearing in various products, from smartphones to other consumer goods.

- MEMS is widely used in smartphones, wearable devices, and other electronic devices due to its improved electrical performance at high frequencies. As the consumer electronics sector shifts its attention away from conventional sensors and toward MEMS technology, the market is anticipated to grow in popularity. As the main technology driver for MEMS, consumer electronics, driven by smartphones, gradually replaced automotive applications.

- Accelerometers and gyroscopes are two of the most well-known MEMS (micro-electro-mechanical systems) applications found in smartphones. The proliferation of multiple chips for various sensor and actuator applications in smartphones is one of the main drivers of the MEMS market's explosive growth. During the forecast period, MEMS for mobile devices is anticipated to expand significantly due to rising smartphone sales and business opportunities.

- For instance, global mobile subscription penetration was 106percent by Q4 2022, according to the Ericsson Mobility report for the fourth quarter of 2022. With a net addition of 39 million subscriptions during the quarter, the total number of mobile subscriptions surpassed 8.4 billion in Q4 2022. Such developments are anticipated to increase demand for MEMS devices and provide vendors with various business opportunities to increase their market share and meet the demand for MEMS in smartphones.

- Smartphones use optical image stabilization (OIS) and electronic image stabilization (EIS), enabled by MEMS sensors. During the forecast period, these broad features and innovative functions will likely augment the demand for MEMS sensors, especially for use in smart mobile devices.

- The advancement and evolution of technologies like optical image stabilization, projection displays, fingerprint technology, and others have significantly influenced the designs of MEMS sensors. Technology trends, consumer preferences, and other factors are significant in shaping developments in the electronics industry for consumer electronics and smart devices. These patterns are driving the demand for MEMS sensor miniaturization.

Asia Pacific is Expected to Hold Significant Market Share

- Asia Pacific is likely to dominate the MEMS market. The micro-electro-mechanical system (MEMS) market is expanding due to the presence of major consumer electronics manufacturers in this area. The market is anticipated to be driven by increasing smartphone penetration, 5G penetration, and advancements across numerous end-user industries.

- China, South Korea, Japan, and India, among others, are major Asian-Pacific countries. Asia-Pacific is a massive marketplace for MEMS sensor technologies. The area dominates many manufacturing subsectors of other end-user industries and the global semiconductor manufacturing sector. Nations like China are supplying low-cost goods to the market.

- For instance, many Chinese MEMS sensor firms, including MEMSIC Semiconductor, Senodia Technologies, and others, are investing heavily in the Internet of Things (IoT). The Chinese government views its automotive industry, including the auto parts sector, as one of its most prominent industries. The Central Government expects China's automobile output to reach 35 million units by 2025. This is intended to make the automotive sector one of the most prominent uses of MEMS sensors in China. China recently instructed automakers to sell 40percent more electric vehicles (EVs) than conventional vehicles by 2030. As a result of these advancements in the automotive industry, MEMS technology will become increasingly in demand.

- In the Chinese automotive market, pressure MEMS are expected to continue to grow due to the evolution towards increased autonomy levels that demand enhanced safety and greener driving. China 6 regulations are expected to boost various applications like diesel particulate filters and particulate gasoline filters, evaporative emissions control systems, exhaust gas recirculation, and tire pressure monitoring systems.

- Moreover, due to advancements in the healthcare sector, the Asia Pacific region is anticipated to grow significantly during the forecast period. Government programs and policies supporting the markets for healthcare equipment and devices, increasing investments in research and innovation facilities, and other factors contribute to this growth.

Micro-Electro-Mechanical System Industry Overview

The MEMS market is moderately fragmented with the presence of significant players like Broadcom Inc., Robert Bosch GmBH, STMicroelectronics NV, Texas Instruments Inc., and Qorvo Inc. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- May 2023 - SPEA and GongJin Microelectronics have entered into a strategic partnership that is expected to strengthen the development of their MEMS testing and calibration business in the Mainland China territory. The agreement brings together GJM's leading manufacturing services and quality management capabilities with SPEA's world-class testing technologies and expertise and is expected to accelerate growth for both companies in the fast-growing MEMS field in China.

- June 2023 - Rogue Valley Microdevices announced its acquisition of a 50,000 sqft commercial building in Florida to serve as its second microfabrication facility. The space will be reconfigured for a cleanroom and office space, with initial production of its first MEMS devices slated for 2025. The company's expansion to Palm Bay will aid it in increasing supply-chain resilience and to boost production volume.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Popularity of IoT in Semiconductors

- 5.1.2 Increasing Demand for Smart Consumer Electronics

- 5.1.3 Increasing Adoption of Automation in Industries and Homes

- 5.2 Market Challenges/ Restraints

- 5.2.1 Highly Complex Manufacturing Process and Demanding Cycle Time

- 5.2.2 Lack of Standardized Fabrication Process for MEMS

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 RF MEMS

- 6.1.2 Oscillators

- 6.1.3 Microfluidics

- 6.1.4 Environmental MEMS

- 6.1.5 Optical MEMS

- 6.1.6 MEMS Microphones

- 6.1.7 Inertial MEMS

- 6.1.8 Pressure MEMS

- 6.1.9 Thermophiles

- 6.1.10 Microbolometers

- 6.1.11 Inkjet Heads

- 6.1.12 Accelerometers

- 6.1.13 Gyroscopes

- 6.1.14 Other Types

- 6.2 By Application

- 6.2.1 Automotive

- 6.2.2 Healthcare

- 6.2.3 Industrial

- 6.2.4 Consumer Electronics

- 6.2.5 Telecom

- 6.2.6 Aerospace and Defense

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Relative Positioning

- 7.1.1 Relative Positioning of MEMS Vendors

- 7.1.2 Relative Positioning of MEMS Foundries

- 7.2 Company Profiles

- 7.2.1 Broadcom Inc.

- 7.2.2 Robert Bosch GmBH

- 7.2.3 STMicroelectronics NV

- 7.2.4 Texas Instruments Inc.

- 7.2.5 Qorvo Inc.

- 7.2.6 Infineon Technologies AG

- 7.2.7 Knowles Electronics LLC (Knowles Corporation)

- 7.2.8 TDK Corporation

- 7.2.9 NXP Semiconductors NV

- 7.2.10 Panasonic Corporation

- 7.2.11 GoerTek Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

奈米机电系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

奈米机电系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 2025年MEMS(电子机械系统)全球市场报告2025年电子机械系统(MEMS)振盪器全球市场报告2025年电子机械(MEM)系统扬声器全球市场报告

2025年MEMS(电子机械系统)全球市场报告2025年电子机械系统(MEMS)振盪器全球市场报告2025年电子机械(MEM)系统扬声器全球市场报告 电子机械系统市场(按设备类型、製造材料、最终用户和分销管道)—2025-2030 年全球预测全球行动装置MEMS市场

电子机械系统市场(按设备类型、製造材料、最终用户和分销管道)—2025-2030 年全球预测全球行动装置MEMS市场 全球电子机械系统 (MEMS) 市场(至 2030 年)按感测器类型(惯性感测器、压力感测器、环境感测器、光学感测器)、致动器类型(光学、微流体、喷墨头、高频)、产业和地区划分电子机械系统 (MEMS) 振盪器全球市场机会与策略(至 2034 年)电子机械系统市场:2034 年的机会与策略微製造设备市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

全球电子机械系统 (MEMS) 市场(至 2030 年)按感测器类型(惯性感测器、压力感测器、环境感测器、光学感测器)、致动器类型(光学、微流体、喷墨头、高频)、产业和地区划分电子机械系统 (MEMS) 振盪器全球市场机会与策略(至 2034 年)电子机械系统市场:2034 年的机会与策略微製造设备市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测