|

市场调查报告书

商品编码

1687940

电线电缆:市场占有率分析、产业趋势与统计、成长预测(2025-2030)Wire And Cable - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

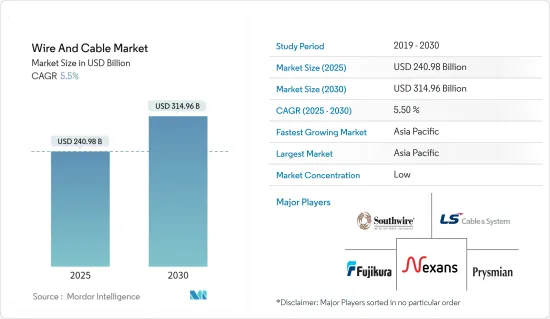

电线电缆市场规模预计在 2025 年为 2,409.8 亿美元,预计到 2030 年将达到 3,149.6 亿美元,预测期内(2025-2030 年)的复合年增长率为 5.5%。

可再生能源产量的增加、智慧电网技术蕴藏量的不断增长以及世界各国政府为升级输配电系统所做的努力是推动市场扩张的一些因素。近年来,随着内容和云端供应商试图吸引更多客户并提供频宽密集型服务,海底基础设施变得越来越受欢迎。该海底电缆预计使用寿命为25年。

关键亮点

- 电缆製造商也大幅提高耐火电缆的生产能力,以满足日益增长的建筑产品需求。耐火电缆旨在限制火焰蔓延。他们还用一块布来阻挡释放的烟雾和其他有毒气体。这种电线专为商业建筑、大型住宅和製造设备布线而设计。提供耐火电缆的主要企业包括 Nexans、TPC Wire & Cable Corp.、Prysmian Group、Cavicel 和 Cleveland Cable。

- 2022 年 7 月,随着云端服务供应商寻求更快的网路连接,美国通讯基础设施供应商开通了连接英国和欧洲大陆的宙斯海底路线。海底电缆承载着几乎所有的网路资料流量。包括 Alphabet 旗下的Google和 Meta 在内的多家科技公司也正在投资建造海底电缆。电讯连接器允许透过电子或电气方式远距传输各种资料。连接器安装在提供资料传输和电话服务的通讯电缆的末端。对连接和互联网接入的不断增长的需求正在积极推动市场成长。对更快的互联网速度和更好的连接性的日益增长的需求最终将需要强大而高效的有线连接,而光纤技术可以满足这一需求。连接器有助于保护光纤,从而推动市场成长。

- 5G网路应用正在快速发展,IT连接器系统发挥关键作用。不断增长的讯号频率、资料速率、封装密度和讯号完整性要求正在推动对高性能、高品质基板对板互连解决方案的需求。

- 对于电缆製造商来说,开发中国家日益增长的连接需求带来了巨大的商业前景。然而,市场成长也伴随着一些营运挑战,例如铺设光纤电缆。

- COVID-19 疫情对所研究的市场产生了重大影响,多个部署电线电缆的终端用户产业面临许多挑战。新冠疫情在美国和欧洲的蔓延,迫使通讯监管机构延后5G频谱竞标。例如在葡萄牙,沃达丰、NOS和MEO必须等待700MHz、1800MHz、900MHz、2.6GHz、2.1GHz和3.6GHz等各个频段的频谱权。

电线电缆市场趋势

光纤电缆正在快速成长

- 光纤电缆覆盖本地电话线路之间的远距,是网路系统的骨干。其他系统使用者包括有线电视服务、办公大楼、大学校园、工业工厂和电力公司。光纤电缆长度在 984.2 英尺至 24.8 英里之间,最大传输距离为 9,328 英里。光纤电缆不易受到干扰。

- 支持全球推广 5G 的政府计划正在推动市场成长。例如,欧盟委员会很早就认识到5G网路的重要性,并建立了官民合作关係关係,共同开发和研究5G技术。因此,欧盟委员会宣布透过其「地平线 2020」计画提供超过 7 亿英镑的公共资金,支持在欧洲推广 5G。

- 在工业4.0中,光纤网路实现了传统工业的通讯网路升级,实现了工业资料通讯,以及高速M2M/M2S网路的即时监控。因此,光纤电缆製造商正专注于提高产量,以满足全球市场对光纤宽频 (FTTH) 和 5G 服务日益增长的需求。

- 根据 GSMA 预测,到 2030 年,波湾合作理事会(GCC) 成员国巴林、科威特、阿曼、卡达、沙乌地阿拉伯和阿拉伯联合大公国的 5G 普及率将成为全球最高的地区。近年来,随着云端和内容提供者试图吸引更多用户并提供更可靠、频宽密集型的服务,海底基础设施变得越来越受欢迎。

- 根据Telegeography通报,截至2023年,全球投入使用的海底电缆长度约140万公里。这些电缆用于短远距的资料传输。例如,连接爱尔兰和英国的CeltixConnect海底电缆长131公里。亚美通道采用全长2万公里的海底电缆。海底电缆的成长趋势正在吸引投资者并振兴光纤网路。

亚太地区占市场主导地位

- 亚太地区在上年度占据了最大的市场占有率,由于各个地区的发展,预计在预测期内将以最高的复合年增长率增长。例如,根据中国国家统计局的数据,2023年4月通讯业业务总量约为人民币1,540亿元(约21.63兆美元),比去年同期成长18%。电讯流量的增加可能会鼓励电讯建立新的电讯塔,从而推动研究市场的需求。

- 中国市场向可再生能源的扩张正在推动该地区太阳能板的建设,预计这将相应推动所研究的市场。例如,2022年12月,中国三峡新能源开始在内蒙古库布其沙漠建设其提案的16GW大型企划的第一期1GW工程。一旦建成,这个大型设施将能够产生 8GW 的太阳能、4GW 的风能和 4GW 的改良煤电。

- 日本不断增长的能源需求和智慧电网的引入是推动市场扩张的主要因素。由于许多行业对持续供电的需求不断增加,发电、配电和输电在各个地方都在扩大,导致低压电缆的使用量增加。

- 由于政府的「全民住宅」计划和新住宅的建设,印度低压电缆市场预计将很快出现显着增长。低压架空线路可能由玻璃或陶瓷绝缘层包覆的裸导体或架空捆绑电缆系统组成,通常用于将住宅和小型商业客户与电力设施连接起来。

- 其他亚洲国家正大力投资加强海底电缆网路的连通性,从而促进市场成长。

电线电缆产业概况

电线电缆市场竞争激烈。市场的主要企业包括 Nexans、LS Cable & System Limited、Prysmian SpA、Southwire Company LLC、Fujikura、Furukawa Electric、Leoni、Belden Incorporated、TE Connectivity 和 Wilms Group。在预测期内,公司正在建立多种伙伴关係并投资于新产品的推出,以增加市场占有率并获得竞争。

2023 年 5 月,耐吉森旗下公司 LibanCables 开始在其 Nahr Ibrahim工业设施扩建 600kW尖峰时段太阳能光电系统,采用全球第一个 500kW 货柜式电池解决方案,使总尖峰时段容量达到 1.2MW。该计划将使 LibanCables 用太阳能发电面板替换其六台发电机中的两台,从而每年减少 1,500 吨温室气体排放(相当于 750 辆汽车)。

2023 年 4 月,管理瑞士电网的国营公司 Swissgrid 与耐吉森合作,在日内瓦-科因特林机场南侧埋设超高压 (VHV) 架空输电线路。以地下电缆取代架空电线将释放大日内瓦地区用于城市发展的大片土地。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- 评估主要宏观经济趋势的影响

第五章市场动态

- 市场驱动因素

- 建筑业需求增加

- 继续部署智慧电网基础设施

- 扩大通讯产业的应用

- 市场问题

- 安装成本高且相关复杂性

- 原物料价格波动

第六章市场区隔

- 按电缆类型

- 低压能源

- 电源线

- 光纤电缆

- 讯号/控制电缆

- 其他电缆

- 按行业

- 建筑(住宅和商业)

- 通讯(IT/通讯)

- 电力基础设施(能源与电力、汽车)

- 其他最终用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 其他亚太地区

- 拉丁美洲

- 中东和非洲

- 北美洲

第七章竞争格局

- 公司简介

- Nexans

- Cable & System Limited

- Prysmian SpA

- Southwire Company LLC

- Fujikura Limited

- Furukawa Electric Co., Ltd

- Leoni AG

- Belden Incorporated

- TE Connectivity

- British Cables Company(Wilms Group)

- TELE-FONIKA Kable SA

- Amphenol Corporation

- NKT A/S

- CommScope Holding Company, Inc.

- Corning Incorporated

- Waskonig & Walter

- Shanghai Shenghua Group

- Hengton Optic-Electric

第八章投资分析

第九章:市场的未来

The Wire And Cable Market size is estimated at USD 240.98 billion in 2025, and is expected to reach USD 314.96 billion by 2030, at a CAGR of 5.5% during the forecast period (2025-2030).

The growing renewable energy production, increasing reserves in smart grid technology, and government initiatives globally for upgrading distribution and transmission systems are responsible for market proliferation. In the past few years, content and cloud providers have attempted to attract more customers and offer bandwidth-intensive services, increasing submarine infrastructure popularity. The lifespan of a submarine cable is expected to be 25 years.

Key Highlights

- Cable manufacturing companies are also significantly increasing fire-resistant cable production capacities to keep pace with the increasing need for construction products. Fire-resistant cables are designed to limit the propagation of flames. They have a sheet to determine the smoke and other toxic gases released. Such wires are designed for commercial buildings and wiring in large residential and manufacturing units. The major players offering fire-resistant cables include Nexans, TPC Wire & Cable Corp., Prysmian Group, Cavicel, Cleveland Cable, and others.

- In July 2022, US communications infrastructure provider launched the Zeus subsea route connecting the United Kingdom and continental Europe as cloud service providers desire faster internet connection. Undersea cables transmit almost all internet data traffic. Numerous technology companies, including Alphabet's Google and Meta, have also invested in building subsea cables. Using telecom connectors, extensive data can be transmitted over long distances via electronic or electrical means. They could be seen at the end of telecom cables that transmit data and offer telephony services. Growing demand for connectivity and internet access positively drives the market's growth. The growing need for higher internet speed and better connectivity eventually requires robust and efficient cable connectivity, which fiber optic technology fulfills. The connectors help protect optic fiber, positively boosting the market's growth.

- 5G network applications are rapidly gaining momentum, and IT connector systems play a crucial role. Due to ever-higher signal frequencies, data rates, packing density, and signal integrity requirements, the need for high-performance and high-quality board-to-board connection solutions is also growing.

- The growing demand for connectivity in developing nations for cable producers presents significant business prospects. Yet factors such as installing fiber optic cables provide several operational difficulties for market growth.

- The COVID-19 pandemic had a remarkable impact on the market studied, with several end-user industries that deploy wire and cables facing several difficulties. The spread of COVID-19 across the United States and Europe has forced telecom regulators to postpone 5G spectrum auctions. For instance, in Portugal, Vodafone, NOS, and MEO had to wait for frequency rights in various frequency bands such as 700 MHz, 1800 MHz, 900 MHz, 2.6 GHz, 2.1 GHz, and 3.6 GHz bands.

Wires and Cables Market Trends

Fiber Optic Cable to Witness Major Growth

- Fiber-optic cable spans long distances between local phones and provides the backbone for network systems. Other system users include cable television services, office buildings, university campuses, industrial plants, and electric utility companies. Fiber cables travel between 984.2 feet and 24.8 miles, while the maximum transmission distance is 9,328. Fiber optic cables are less susceptible to interference.

- The government programs to support 5G deployment across the globe drive market growth. For instance, the European Commission recognized the importance of the 5G network early and established a public-private partnership to develop and research 5G technology. As a result, the European Commission announced public funding of over GBP 700 million to support 5G deployment across Europe through the Horizon 2020 Program.

- In Industry 4.0, the fiber optic cable network enables the upgrade of telecom networks, industrial data communication, and real-time monitoring in traditional industries with high-speed M2M/M2S networks. Thus, manufacturers of optical fiber cable focus on improving production to keep up with the growing demand for fiber-to-the-home (FTTH) broadband and power 5G services in the global market.

- According to GSMA, the Gulf Cooperation Council (GCC) states of Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates are forecast to have the highest 5G adoption rates of any region worldwide in 2030. In the past few years, cloud and content providers have attempted to attract more users and offer reliable bandwidth-intensive services, increasing submarine infrastructure popularity.

- According to Telegeography, as of 2023, nearly 1.4 million km of submarine cable are in service worldwide. These cables are used for short and long-range data transmission. For instance, the submarine CeltixConnect cable connecting Ireland and the United Kingdom is 131 km. A 20,000 km long submarine cable is used in the Asia America Gateway. The growing trend of submarine cables attracts investors and fuels the optic fiber network.

Asia Pacific to Dominate the Market

- Asia-Pacific held the largest market share in the previous year and is expected to register the highest CAGR over the forecast period due to various regional developments. For instance, according to the National Bureau of Statistics of China, the Chinese telecommunications industry's business volume was roughly CNY 154 billion (USD 21.63 trillion) in April 2023, an 18% rise over the same period the previous year. The rise in telecom business volume would push telecom players to establish new telecom towers, driving the demand for the studied market.

- China's development toward renewable energy is pushing the construction of solar panels in the region, which would proportionately drive the market studied. For instance, in December 2022, China's Three Gorges New Energy began construction on the first 1 GW phase of a proposed 16 GW mega-project in Inner Mongolia's Kubuqi Desert. The gigantic facility, when completed, would feature 8 GW of solar, 4 GW of wind, and 4 GW of improved coal capacity.

- Rising energy demand and implementing smart grid networks in Japan are the primary drivers driving market expansion. The increasing demand for continuous power supply in many industries has expanded power generation, distribution, and transmission across various locations, resulting in greater use of LV cables.

- India's low-voltage cable market is expected to see significant growth shortly due to the government's Housing For All plan and the construction of new residential buildings. Low voltage overhead lines, which may use bare conductors carried on glass or ceramic insulators or an aerial bundled cable system, are often used to connect a residential or small commercial customer and the utility.

- Several other Asian countries are investing heavily to strengthen connectivity through undersea cable networks, thus boosting the market's growth.

Wires and Cables Industry Overview

The Wire and Cable Market is very competitive. Some of the significant players in the market are Nexans, LS Cable & System Limited, Prysmian S.p.A, Southwire Company LLC, Fujikura Limited, Furukawa Electric Co., Ltd, Leoni, Belden Incorporated, TE Connectivity, Wilms Group, among others. The companies are increasing the market share by forming multiple partnerships and investing in introducing new products, earning a competitive edge during the forecast period.

In May 2023, LibanCables, a Nexans company, launched the extension of its 600kW peak solar power system at its NahrIbrahim industrial facility, leading to a total output power of 1.2 MW at peak with a first-of-its-kind 500kW containerized battery solution. The project will allow LibanCables to reduce greenhouse gas emissions by 1,500 tons per year, equivalent to the weight of 750 cars, by replacing two of its six electric generators with photovoltaic panels.

In April 2023, Swissgrid, the national company in charge of Switzerland's electricity transmission grid, partnered with Nexans to bury the Very High Voltage (VHV) overhead power lines along the southern side of the Geneva-Cointrin airport. Replacing the overhead cables with underground cables will free up large tracts of land destined for urban development in the greater Geneva area.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 An Assessment of the Impact of Key Macroeconomic Trends

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand from the Construction Sector

- 5.1.2 Ongoing Deployment of Smart Grid Infrastructure

- 5.1.3 Growing Adoption in the Telecommunications Industry

- 5.2 Market Challenges

- 5.2.1 High Cost of Installation and Associated Complexities

- 5.2.2 Fluctuating Raw Material Prices

6 MARKET SEGMENTATION

- 6.1 By Cable Type

- 6.1.1 Low Voltage Energy

- 6.1.2 Power Cable

- 6.1.3 Fiber Optic Cable

- 6.1.4 Signal and Control Cable

- 6.1.5 Other Cable Types

- 6.2 By End-user Vertical

- 6.2.1 Construction (Residential & Commercial)

- 6.2.2 Telecommunications (IT & Telecom)

- 6.2.3 Power Infrastructure (Energy & Power, Automotive)

- 6.2.4 Others End-user Verticals

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 Rest of Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Nexans

- 7.1.2 Cable & System Limited

- 7.1.3 Prysmian S.p.A

- 7.1.4 Southwire Company LLC

- 7.1.5 Fujikura Limited

- 7.1.6 Furukawa Electric Co., Ltd

- 7.1.7 Leoni AG

- 7.1.8 Belden Incorporated

- 7.1.9 TE Connectivity

- 7.1.10 British Cables Company (Wilms Group)

- 7.1.11 TELE-FONIKA Kable S.A.

- 7.1.12 Amphenol Corporation

- 7.1.13 NKT A/S

- 7.1.14 CommScope Holding Company, Inc.

- 7.1.15 Corning Incorporated

- 7.1.16 Waskonig & Walter

- 7.1.17 Shanghai Shenghua Group

- 7.1.18 Hengton Optic-Electric

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

光纤地线市场(按光纤数量、光纤模式和应用)—2025-2032 年全球预测电线电缆市场按类型、材料类型、电压类型、安装类型、分销管道和最终用户划分 - 2025-2032 年全球预测

光纤地线市场(按光纤数量、光纤模式和应用)—2025-2032 年全球预测电线电缆市场按类型、材料类型、电压类型、安装类型、分销管道和最终用户划分 - 2025-2032 年全球预测 2025年全球微管电缆市场报告

2025年全球微管电缆市场报告 2032 年电线电缆材料市场预测:按电缆类型、应用、最终用户和地区进行的全球分析2025年全球电线电缆市场报告2025年全球电缆市场报告2025年全球铝电缆市场报告URD 电缆市场按类型、安装类型、额定电压、导体材料、销售管道和应用划分 - 2025-2030 年全球预测微管电缆市场(按产品类型、材料、部署类型、直径和应用)—2025-2030 年全球预测

2032 年电线电缆材料市场预测:按电缆类型、应用、最终用户和地区进行的全球分析2025年全球电线电缆市场报告2025年全球电缆市场报告2025年全球铝电缆市场报告URD 电缆市场按类型、安装类型、额定电压、导体材料、销售管道和应用划分 - 2025-2030 年全球预测微管电缆市场(按产品类型、材料、部署类型、直径和应用)—2025-2030 年全球预测 全球陶瓷电缆市场

全球陶瓷电缆市场