|

市场调查报告书

商品编码

1687960

电子竞技 -市场占有率分析、产业趋势与统计、成长预测(2025-2030)eSports - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

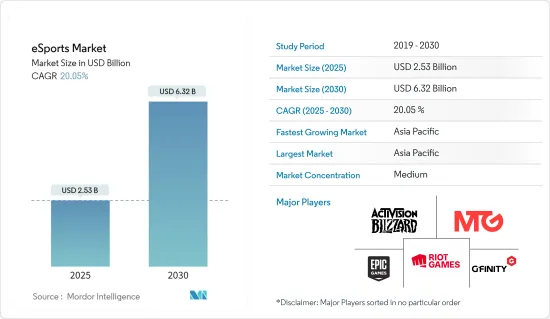

预计 2025 年电竞市场规模为 25.3 亿美元,到 2030 年将达到 63.2 亿美元,预测期内(2025-2030 年)的复合年增长率为 20.05%。

全球数百万人正在关注提供数百万美元奖金的竞技电子游戏。休閒游戏玩家赚取七位数的薪水、获得串流媒体服务的重磅商业代言以及出现在实况活动中已不再罕见。电子竞技市场目前仍处于早期阶段,但随着观众人数的增加,预计未来将成为一个巨大的市场。

关键亮点

- 市场成长要素包括游戏直播的兴起、大量投资、不断增长的观众群、参与活动以及联赛基础设施的发展。随着产业专业化程度的提高,影响者、游戏玩家、活动策划者和游戏开发者的利润前景一片光明,市场也从中受益。

- 大多数电竞观众和参与企业都是千禧世代。因此,电子竞技发行商透过个人化游戏体验并在主机、个人电脑和手机等不同平台上提供游戏来瞄准这一人群。例如,截至 2018 年 4 月,游戏《要塞英雄》在各个平台上创造了 2.96 亿美元的收益,收益了任何其他重要的主机或 PC 游戏的单年收入。透过这种方式,生态系统中增加新的游戏玩家有望吸引更多的电竞观众,并在长期内创造更多的收益。

- 此外,一些旨在为整个体育运动提供管治的组织也应运而生。例如,世界电子竞技协会(WESA)和电子竞技诚信联盟等组织与电子竞技相关人员合作,保护比赛的完整性并调查任何作弊行为,包括比赛操纵。因此,预计这将为市场带来积极的前景并促进其成长。

- 然而,缺乏支持性基础设施和对体育的认识是预测期内阻碍市场成长的一些因素。

- COVID-19 疫情影响了人类生活的各个方面和许多商业领域。由于 COVID-19,许多联赛和锦标赛被重新安排或取消。由于体育场馆关闭,一些组织者在网上举办活动。由于 COVID-19,8% 的实况活动被推迟,53% 的活动转移到虚拟平台,26% 的活动被重新安排,13% 的活动按计划进行。在所有这些条件下,市场在 2020 年实现了一定成长。

电竞市场趋势

广告成为电竞最大的收入来源

- 广告收入包括针对电竞观众的广告收益,包括线上平台直播、电竞比赛随选节目或电竞电视上显示的广告。

- 当今全球最受欢迎的电子游戏包括 Dota 2、Fortnite、英雄联盟、反恐精英和全球攻势。守望先锋、全球攻势等。电子游戏产业已经从娱乐业发展成为可行的职业。观众对电竞比赛的兴趣非常高,它吸引了包括名人和全球品牌在内的投资者的赞助。

- 过去几年,观众和粉丝数量稳步增长,带来了新的成长机会和增加的投资。由于生态系统在多个子行业提供各种投资机会,近年来该领域的投资显着成长。一级市场咨询来自传统创业投资公司、策略投资者和私募股权。

- 俄亥俄州立大学、麻萨诸塞州贝克尔学院和维吉尼亚州雪兰多大学均提供电竞学位课程。此外,美国 100 多所高中还举办电竞比赛和传统足球等其他比赛。与其他几所学校一样,加州大学欧文分校也为其排名前六名的球员提供奖学金,以帮助扩大其计画。

- 因此,预计所有上述因素都将在预测期内为电竞市场的收益广告部分做出贡献。

亚太地区可望主导市场

- 在亚太地区,由于电子竞技在年轻人中的流行以及政府对市场成长的支持,预计中国将在电竞市场中占据主要市场占有率。

- 例如,中国杭州市计划在 2022 年建成 14 个电竞设施,预计投资额高达 154.5 亿元(22.2 亿美元)。这项投资预计将使杭州成为全球电竞中心。

- 此外,杭州将于2022年举办亚运会,电子竞技可望成为正式比赛项目。透过这项投资,中国可望抢占大量市场占有率。

- 此外,电竞产业的主要参与企业腾讯控股有限公司总部位于中国,透过开发诸如大获成功的《王者荣耀》等游戏,在中国电竞的崛起中发挥了重要作用。腾讯控股有限公司计划在中国扩大《英雄联盟》和《王者荣耀》等热门成人游戏的锦标赛,吸引来自世界各地的参与企业和观众。

- 腾讯天美电竞中心总经理张小龙在腾讯全球电竞高峰会上宣布,2022年王者荣耀世界冠军杯(KCC)的总奖金池为1000万美元(820万欧元)。张解释说,从2022年起,来自中国KPL和其他海外的16支球队将参加该赛事。

- 本次比赛将创下行动电竞领域最高奖金池纪录,标誌着该产业的重大发展。作为全球最盈利的游戏之一,《王者荣耀》及其开发商腾讯天美工作室已经明确表示了他们的电竞意图。

- 因此,预计增加对中国电子竞技的投资将推动中国市场的发展。

电竞产业概览

电子竞技市场尚处于早期阶段,因此竞争较少。看到电竞联盟的受欢迎程度,各公司纷纷进入市场以获得竞争优势并扩大其地理影响力。此外,这些公司为提高其在不同地区的知名度而采取的策略包括组织新的体育联盟、建立合作伙伴关係、合併、收购等。主要参与企业包括 Modern Times Group、Activision Blizzard Inc.、RIoT Games Inc. 和腾讯控股有限公司。最近的趋势如下:

- 2022 年 4 月-SK Telecom 与韩国电竞协会 (KeSPA) 签署为期三年的赞助合约。根据该协议,SK Telecom 将成为 KeSPA 的官方赞助商,并可能在即将举行的亚运会上担任韩国电竞队伍的教练。预计与市场相关的多项措施和创新技术将在预期期内推动进一步成长。

- 2022 年 3 月 - Rooter Sports Technologies Private Limited 购买 Sky Esports 所有智慧财产权的媒体版权,期限为一年。南亚领先的电竞赛事组织者 Sky Esports 拥有该智慧财产权。媒体版权将使 Rooter Sports 能够在印度以多种语言转播比赛,包括英语、印地语、孟加拉语、卡纳达语、泰米尔语、马拉雅拉姆语和泰卢固语。这些併购预计将扩大媒体版权部门。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 调查结果和先决条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概览

- 采用市场驱动因素与限制因素

- 市场驱动因素

- 电子游戏日益普及

- 人们对电子竞技的认识不断提高

- 市场限制

- 盗版、法律限制以及游戏交易过程中的诈欺问题

- 产业价值链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章:电竞市场现状

- 各国电竞参与状况

- 电竞爱好者最爱的 10 款游戏

- 收视率和奖金排名前十名的联赛

第六章市场区隔

- 按收益模式

- 媒体权利

- 广告和赞助

- 商品和门票

- 其他的

- 透过串流媒体平台

- Twitch

- YouTube

- 其他串流媒体平台(斗鱼和哈鱼)

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 其他欧洲国家

- 中国

- 亚太地区(不包括中国)

- 日本

- 印度

- 韩国

- 其他亚太地区

- 拉丁美洲

- 中东和非洲

- 北美洲

第七章竞争格局

- 公司简介

- Modern Times Group

- Activision Blizzard Inc

- Electronic Arts Inc

- RIoT Games Inc.(Tencent Holdings Ltd)

- Epic Games Inc.

- Gfinity PLC

- Faceit

- Capcom Co. Ltd

- Valve Corporation

第八章 市场机会与未来趋势

第九章投资分析

The eSports Market size is estimated at USD 2.53 billion in 2025, and is expected to reach USD 6.32 billion by 2030, at a CAGR of 20.05% during the forecast period (2025-2030).

Millions of people worldwide are increasingly interested in competitive video gaming, which offers millions of dollars in prize money. It is no longer uncommon for casual gamers to command seven-figure wages, receive significant business endorsements from streaming services, and appear at live events. Although the eSports market is still in its initial stage, and with the growing viewership, it is expected that it may offer strong potential to capitalize on the market in the future.

Key Highlights

- The market growth factors are an increase in the live streaming of games, significant investments, growing audience reach, engagement activities, and infrastructure for league competitions. The market benefits from the lucrative prospects made possible by the industry's increasing professionalization for influencers, gamers, event planners, and game developers.

- The majority of the audience and the players of eSports are the Millenials. Thus, the publishers of eSports are targeting this customer base by personalizing the gameplay experience and offering the game on different platforms such as console, PC, and mobile. For instance, as of April 2018, the Fortnite game generated USD 296 million in revenue across platforms, which was more annual than any significant console or PC game. Thus, with the new gamers in the ecosystem, it is expected to attract more eSports audiences, generating more revenue over time.

- Moreover, organizations are emerging for governance to make the entire sports organized. For instance, associations such as the World esports Association (WESA) and Esports Integrity Coalition are working with esports stakeholders to protect the integrity of competition and investigate all forms of cheating, including match manipulation. Hence, this is expected to have a positive outlook on the market and is expected to complement the growth of the market.

- However, on the flip, lack of supportive infrastructure and awareness about sports are a few factors hindering market growth during the forecast period.

- The COVID-19 pandemic impacted many aspects of human life and numerous business sectors. Due to COVID-19, numerous leagues and tournaments were rescheduled or abandoned. As the stadiums were closed, some organizers held the event online. In COVID-19, 8% of live events were postponed, 53% were shifted to virtual platforms, 26% were rescheduled, and 13% were held as planned. Under all of these conditions, the market increased somewhat in 2020.

esports Market Trends

Advertising to be the Largest Sources of eSports Revenue

- The advertising comprises the revenue generated from the advertisements targeting esports viewers, including ads shown during live streams on online platforms, on video-on-demand content of esports matches, or esports TV.

- The top video games globally now include Dota2, Fortnite, League of Legends, Counter-Strike: Overwatch, and Global Offensive. The video game industry has developed from a pastime to a viable job path. Due to the huge amount of interest in esports competitions among spectators, investors, including celebrities and global brands, are becoming sponsors.

- The number of viewers and fans has grown steadily over the past few years, opening up new growth opportunities and increasing investment. Investments in this area have advanced significantly in recent years thanks to the ecosystem, which offers a variety of investment opportunities across several subsectors. The key market draw is traditional venture capital firms, strategic investors, and private equity.

- The esports degree program is offered by Ohio State University, Becker College in Massachusetts, and Shenandoah University in Virginia. Additionally, esports competitions and other games like conventional soccer are being held in more than 100 high schools around the United States. The University of California Irvine offers scholarships to the top 6 players, as are several other institutions, to boost the program's expansion.

- Hence, all the above factors are expected to contribute to the advertising segment for generating revenue for the eSports market in the forecasted period.

Asia-Pacific is expected to dominate the Market

- In the Asian-pacific region, China is anticipated to hold a significant market share in the eSports market owing to the popularity of esports among the youth and supportive government support for the market's growth.

- For instance, Hangzhou ( a city in China) could plan to build 14 esports facilities before 2022, and it is expected to invest up to CNY 15.45 billion (USD 2.22 billion). This investment is expected to make it the esports capital of the world.

- Moreover, Hangzhou will host Asian Games in 2022, where esports is expected to be an official medal event. With its investments, China is expected to hold a significant market share.

- Furthermore, Tencent Holdings Limited, a significant player in the eSports industry, is headquartered in China and played an influential role in the increase of eSports in China by developing games like "Honor of Kings," which was a huge success. Tencent Holdings Limited plans to expand tournaments for hugely popular games like "League of Legends" and "Honor of Kings in China, " which will attract global players and viewers.

- The prize pool for the 2022 Honor of Kings World Champion Cup (KCC) will be USD 10 million (EUR 8.2 million), according to Allan Zhang, general manager of Tencent TiMi Esports Center, who announced during the Tencent Global Esports Summit. Zhang explained that 16 teams from the King Pro League (KPL) in China and other international locations would participate in the competition after 2022.

- The competition will set a new record for the largest prize pool in mobile esports, which is a significant development for the industry. The honor of Kings and its developer Tencent's TiMi Studio have made their intentions for esports clear as one of the most lucrative games globally.

- Hence, the increasing investment in eSports in the country is expected to augment the China market.

esports Industry Overview

The eSports market is at its initial stage; thus, it is a little competitive. Although seeing the popularity of the eSports leagues, companies are entering the market to gain a competitive advantage and expand their geographical presence. Furthermore, these companies' strategies to increase their visibility across different geographic locations include organizing new sports leagues, partnerships, mergers, and acquisitions. Some significant players are Modern Times Group, Activision Blizzard Inc., and Riot Games Inc. (Tencent Holdings Ltd), amongst others. A few recent developments are:

- April 2022 - SK Telecom and the Korean Esports Association (KeSPA) have a three-year sponsorship agreement. As a result of the arrangement, SK Telecom is now KeSPA's official sponsor and may coach the Korean esports team for forthcoming Asian tournaments. During the anticipated term, several market-related efforts and innovations are expected to fuel additional growth.

- March 2022 - Rooter Sports Technologies Private Limited purchased Sky Esports' media rights for all of its intellectual property for a year. The top esports event organizer in South Asia, Sky Esports, owns its intellectual properties. With media rights, Rooter Sports may broadcast matches in India in several languages, including English, Hindi, Bengali, Kannada, Tamil, Malayalam, and Telugu. These M&A operations are anticipated to boost the media rights segment's expansion during the expected term.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables and Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Introduction to Market Drivers and Restraints

- 4.3 Market Drivers

- 4.3.1 Increasing Popularity of Video Games

- 4.3.2 Growing Awareness about eSports

- 4.4 Market Restraints

- 4.4.1 Issues Such as Piracy, Laws and Regulations, and Concerns Relating to Fraud During Gaming Transactions

- 4.5 Industry Value Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 ESPORTS MARKET LANDSCAPE

- 5.1 Esports Engagement by Country

- 5.2 Top 10 Games Played by eSports Fans

- 5.3 Top 10 Leagues, By Viewership, By Prize Money

6 MARKET SEGMENTATION

- 6.1 By Revenue Model

- 6.1.1 Media Rights

- 6.1.2 Advertising and Sponsorships

- 6.1.3 Merchandise and Tickets

- 6.1.4 Other Revenue Models

- 6.2 By Streaming Platform

- 6.2.1 Twitch

- 6.2.2 YouTube

- 6.2.3 Other Streaming Platforms ( DouYu and Hayu )

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.1.3 Rest of North America

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 United Kingdom

- 6.3.2.3 France

- 6.3.2.4 Rest of Europe

- 6.3.3 China

- 6.3.4 Asia-Pacific ( excluding China)

- 6.3.4.1 Japan

- 6.3.4.2 India

- 6.3.4.3 South Korea

- 6.3.4.4 Rest of Asia-Pacific

- 6.3.5 Latin America

- 6.3.6 Middle East & Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Modern Times Group

- 7.1.2 Activision Blizzard Inc

- 7.1.3 Electronic Arts Inc

- 7.1.4 Riot Games Inc. ( Tencent Holdings Ltd)

- 7.1.5 Epic Games Inc.

- 7.1.6 Gfinity PLC

- 7.1.7 Faceit

- 7.1.8 Capcom Co. Ltd

- 7.1.9 Valve Corporation

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

9 INVESTMENT ANALYSIS

2025 年至 2033 年电竞市场规模、份额、趋势及预测(依收入模式、平台、游戏及地区)

2025 年至 2033 年电竞市场规模、份额、趋势及预测(依收入模式、平台、游戏及地区) 2025年全球电竞市场报告

2025年全球电竞市场报告 电子竞技市场 - 全球产业规模、份额、趋势、机会和预测,按收入来源、受众类型、设备、地区和竞争细分,2020-2030 年预测2025年全球电竞内容创作市场报告

电子竞技市场 - 全球产业规模、份额、趋势、机会和预测,按收入来源、受众类型、设备、地区和竞争细分,2020-2030 年预测2025年全球电竞内容创作市场报告 电竞的全球市场:种类·收益来源·各地区 (~2032年)

电竞的全球市场:种类·收益来源·各地区 (~2032年) 电子竞技市场 (~2035年):串流类型·游戏种类·设备类型·串流平台·收益源·各地区的产业趋势与全球预测

电子竞技市场 (~2035年):串流类型·游戏种类·设备类型·串流平台·收益源·各地区的产业趋势与全球预测 电子竞技市场分析与预测(2034 年):类型、产品、服务、技术、组件、应用、设备、最终用户、模式、阶段2032 年电竞市场预测:按收益来源、游戏类型、受众类型、平台、锦标赛和地区进行的全球分析全球电竞市场:市场规模、份额、趋势分析(按收益来源、串流媒体和地区)、细分市场预测(2025-2030 年)

电子竞技市场分析与预测(2034 年):类型、产品、服务、技术、组件、应用、设备、最终用户、模式、阶段2032 年电竞市场预测:按收益来源、游戏类型、受众类型、平台、锦标赛和地区进行的全球分析全球电竞市场:市场规模、份额、趋势分析(按收益来源、串流媒体和地区)、细分市场预测(2025-2030 年) 电子竞技市场:2025-2030 年全球预测(按产品、游戏类型、串流类型和收益模式)

电子竞技市场:2025-2030 年全球预测(按产品、游戏类型、串流类型和收益模式)