|

市场调查报告书

商品编码

1687981

资料中心交换器:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Data Center Switch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

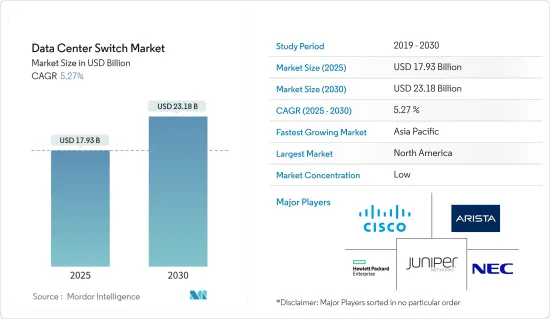

资料中心交换器市场规模预计在 2025 年为 179.3 亿美元,预计到 2030 年将达到 231.8 亿美元,预测期内(2025-2030 年)的复合年增长率为 5.27%。

由于云端运算、资料在地化以及 5G 和物联网等新技术的采用,全球资料中心投资正在增加。由于各种规模的企业需求不断变化、数百万台连网设备的不断创建以及每天透过网路产生的大量资料,资料中心正在激增。

主要亮点

- 要充分发挥人工智慧技术的潜力,需要额外的运算处理和决策流程。根据效能、容量、成本和其他方面,人工智慧处理和资料储存的位置可以从云端到内部资料中心再到网路外围。边缘运算预计将从连网型设备、创新产业和联网汽车中受益匪浅,并将对所考虑的市场产生重大影响。

- 核心交换机由于扩大了流量管理而提供了新的成长潜力。当 COVID-19 疫情迫使人们待在家里时,许多人转向 Netflix 等 OTT 服务来娱乐,而不是外出用餐或去看电影。在新冠疫情爆发的前三个月,Netflix 亚太区新增了 360 万名用户。为了处理大量传入流量同时保持串流服务的质量,Netflix 决定删除高频宽流并使用 Tor 减少流量。

- COVID-19疫情爆发,扰乱了资料中心建设供应链。与封锁相关的计划完工延迟,以及受灾特别严重的产业(如旅馆业和娱乐业)的收益减少,已经影响了建设活动和资料中心位置。

- 云端基础的业务流程的快速采用促使公司大量投资于资料管理解决方案来处理这些系统产生的大量资料。多重云端运算的成长推动了基于虚拟网路的伺服器取代传统的内部实体伺服器,这推动了资料中心格局的不断扩大以及对资料中心交换设备的需求不断增加。

- 然而,资料中心最大的开支之一仍然是电力。根据国际能源总署 (IEA) 的数据,资料中心消耗了全球全部电力的 1%。预计未来五年消费量将进一步增加。大部分能源消耗来自于运作伺服器所需的加热和冷却。再次,冷却过程会消耗大量的能源。

资料中心交换器市场趋势

核心交换器占据最大市场占有率

- 核心交换器必须优先于其他两台交换器。亚马逊和微软等拥有较大市场占有率的公司正在扩大其资料中心。随着资料中心的扩大,核心交换器的需求将呈指数级增长。

- 它必须有效率、可靠地处理不断增加的流量,并且具有较低且可预测的延迟。然而,vPC(虚拟连接埠通道)只能提供两个活动的平行上行链路,这使其在三层资料中心架构中受到频宽限制。三层设计的另一个问题是伺服器之间的延迟会根据所使用的流量路径而变化。例如,思科引入了一种称为跨网路脊叶架构的新资料中心设计来解决这些限制。事实证明,该设计可以提供高频宽、低延迟、无阻塞的伺服器到伺服器连线。

- Crore 交换器提供全面的设备选择,以满足各种资料中心的需求。 Crore 交换器支援为架顶式 (ToR)、脊叶式架构创建高效且可扩展的网路基础架构。此外,它还为特定使用案例提供专门的控制,例如用于高效能运算 (HPC) 的 SAN 和丛集。

- 云端处理技术在北美的使用正变得越来越普遍。例如,Facebook 的 Meta Platforms 去年宣布计划在美国爱达荷州投资 8 亿美元建造一个大型园区,以扩大其资料中心市场占有率。

- 资料中心功能的扩展预计将增加大部分 IT 设备的复杂性和互联互通性,从而推动对交换器和路由器等资料中心网路元件的需求,因为它们已成为超大规模基础设施的重要组成部分。超大规模IT基础设施供应商使用高效能核心交换器进行快速资料传输预计将推动资料中心交换器市场的成长。

北美有望实现显着成长

- 根据房地产专家世邦魏理仕(CBRE)统计,美国七大市场的资料中心租约较前几年成长了31%,较去年同期成长了50%,去年受疫情影响略有下降。北维吉尼亚是美国新资料中心容量的主要市场,占总量的60%以上。

- 主机託管资料中心的大部分需求来自云端服务供应商和社群媒体公司。此外,区块链技术、5G基础设施、虚拟实境社群和自动驾驶汽车技术等新技术的采用也在推动市场的发展。

- 亚特兰大最近已成为资料中心开发的另一个重要市场,并有来自企业供应商的新计画。 QTS资料中心两年前提交了提案在亚特兰大建立一个 110 万平方英尺资料中心的提案。根据「Project Granite」发布的蓝图,QTS 计划在约 36 英亩的土地上建造一个 230 万平方英尺的混合用途设施,其中将包括资料中心空间以及商业、零售和住宅空间。这些进步正在推动这些地区对资料中心交换设备的需求。

- 超融合将储存、处理和网路结合到单一系统中,从而降低了复杂性并提高了资料中心的扩充性。融合式基础架构平台的日益使用正在推动资料中心市场的发展。

- Patrinely Group 及其资金筹措合作伙伴 USAA Real Estate 去年向北维吉尼亚市场推出了一个新的资料中心开发平台 Corscale。该公司的首个计划是位于威廉王子县的盖恩斯维尔十字路口(Gainesville Crossing),这是一座发电容量为 300 兆瓦的综合设施,将包括五个资料中心,旨在为超大客户提供服务。

- 近年来,200GbE 和 400GbE 交换器连接埠在该地区也被广泛采用了。例如,惠普企业 (HPE) 去年和今年再次推出了专为现代资料中心设计的 32 连接埠 200GbE SN3700M 交换器。当配备基于 50G PAM-4 的 Spectrum-2 ASIC 时,此交换器可提供突破性的 8.33Bpps封包处理速度和高达 12.8Tb/s 的双向交换容量。

资料中心交换器产业概况

资料中心交换器市场竞争激烈,有几个主要参与者。然而,目前,市场市场占有率主要被少数几家大公司所占据。这些公司正在采取业务扩张、併购、合资、联盟、伙伴关係等多种策略,透过这些策略,这些市场参与者加强了其在业务中的地位。报告中介绍的关键市场参与者包括思科、Jupiter Networks、戴尔 EMC、Arista Networks、中兴通讯、惠普企业、Mellanox、华为和 Extreme Networks。

- 2023 年 9 月-Hyperscaler 选择 Arista 而非 Cisco 作为资料中心交换器。 Arista 专注于云端服务供应商,占其收入的一半以上。近年来,该公司也进军企业市场,努力实现「业务多元化」。

- 2023 年 4 月 - 为了提供下一代资料中心网路架构,Edgecore 推出了超高容量 400G 交换器。为了满足下一代资料中心和云端处理环境的需求并将基础网路架构提升到新的水平,EdgeCore 宣布推出超高容量 400G 交换器 DCS520。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 买家的议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 市场影响评估

- 技术简介

- 频宽

- 科技(乙太网路、光纤通道、InfiniBand)

第五章 市场动态

- 市场驱动因素

- 对云端运算和边缘运算服务的需求不断增加

- 资料中心本地化的政府法规

- 市场限制

- 资料中心营运成本高

第六章 市场细分

- 开关类型

- 核心交换机

- 分配交换机

- 存取交换机

- 地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 其他亚太地区

- 世界其他地区

- 北美洲

第七章 竞争格局

- 公司简介

- Cisco Systems, Inc.

- Arista Networks, Inc.

- Juniper Networks, Inc.

- Hewlett Packard Enterprise Development LP

- NEC Corporation

- Huawei Technologies Co., Ltd.

- H3C Holding Limited

- Lenovo Group Limited

- Extreme Networks Inc.

- Dell EMC

- Mellanox Technologies.

- Fortinet, Inc.

- ZTE Corporation

- Quanta Cloud Technology(QCT)

- D-Link Corporation

- Silicom Ltd. Connectivity Solutions

第八章投资分析

第九章 未来市场展望

The Data Center Switch Market size is estimated at USD 17.93 billion in 2025, and is expected to reach USD 23.18 billion by 2030, at a CAGR of 5.27% during the forecast period (2025-2030).

Global data center investments are rising because of adopting cloud computing, data localization, and emerging technologies like 5G and IoT. Data centers are fast gaining popularity because of the shifting needs of businesses of all sizes, the ongoing creation of millions of linked devices, and the daily volume of data generated via the Internet.

Key Highlights

- Additional computer processing and decision-making processes are needed to exploit AI technology's potential fully. Depending on aspects like performance, capacity, and cost, the location of AI processing and data storage may range from the cloud to on-premises data centers to the network's periphery. Edge computing, projected to tremendously benefit from connected devices, innovative industries, and connected cars, would significantly impact the market under examination.

- Core switches are experiencing new growth potential because of expanding traffic management. When the COVID-19 outbreak forced people to stay home, many turned to OTT services like Netflix for entertainment instead of going out to eat or to the movies. In the first three months of COVID-19, Netflix Asia-Pacific added 3.6 million new subscribers. Netflix decided to delete the highest bandwidth streams and cut traffic by tor to handle the high volume of incoming traffic while retaining the streaming service's quality.

- The COVID-19 outbreak messed up the supply chain for building the data center. Lockdown-related delays in project completion and a decline in revenue from particularly hard-hit industries, like hospitality and entertainment, impacted construction activity and data center entry locations.

- Due to the rapid adoption of cloud-based business processes, businesses have made significant investments in data management solutions to handle the massive volume of data produced by these systems. Virtual network-based servers are replacing conventional on-premises physical servers due to the growth of multi-cloud computing, which drives the global expansion of data centers and increases the demand for data center switching equipment.

- However, one of the most significant expenses for data centers is still electricity. According to the International Energy Agency, data centers consume 1% of all electricity worldwide. They will use it in the next five years. Most of this energy consumption is required to run the servers, which generate heating and cooling. Again, a lot of energy is used in the cooling process.

Data Center Switch Market Trends

Core Switches Holding the Largest Market Share

- Core switches must be given more priority than the other two switches. Companies with larger market shares, such as Amazon and Microsoft, are building additional data centers. The need for core switches will rise dramatically since data centers are expanding.

- The growing traffic must be handled effectively and reliably, with low and predictable latency. However, because vPC (virtual-port-channel) can only supply two active parallel uplinks, bandwidth becomes a constraint in a three-tier data center architecture. Another issue with a three-tier design is that server-to-server latency changes depending on the traffic path used. For Instance, Cisco introduced a new data center design known as the Clos network-based spine-and-leaf architecture to address these restrictions. This design has been demonstrated to provide a high-bandwidth, low-latency, nonblocking server-to-server connection.

- Crore Switches offer a comprehensive selection of devices to satisfy different data center requirements. Switches from their range allow clients to create effective and scalable network infrastructures for top-of-rack (ToR), spine, and leaf architectures. Additionally, offer specialized controls for particular use cases, including SANs or clusters for high-performance computing (HPC).

- In North America, cloud computing technology is becoming more widely used. For instance, Facebook Inc.'s Meta Platforms Inc. announced plans to increase its data center market share by investing USD 800 million in large-scale campuses in Idaho, United States, last year.

- The complexity and interconnectedness of many IT devices are expected to be improved by expanding data center capabilities, and the demand for data center networking components like switches and routers will be a crucial part of hyper-scale infrastructures. The use of high-performance core switches for quick data transfer by hyper-scale IT infrastructure providers will drive the growth of the data center switch market.

North America Expected to Register Significant Growth

- According to real estate expert CBRE, data center leasing in the top seven US markets was 31% greater than in the previous several years and 50% higher than the last year, which had slightly decreased owing to the pandemic. Northern Virginia was the leading market, with over 60% of the country's new data center capacity.

- Cloud service providers and social media firms account for most of the demand for colocation data centers. The market is also driven by adopting new technologies, including blockchain technology, 5G infrastructure, virtual reality communities, and autonomous car technology.

- With new projects from providers aiming at the enterprise sector, Atlanta has recently become another important market for data center development. To develop a 1.1 million square foot data center in Atlanta, QTS Data Centers submitted proposals the year before the current year. According to the designs in "Project Granite," QTS would create 2.3 million square feet of mixed-use space on around 36 acres of land, including data center space and commercial, retail, and residential land uses. These advances increase the need for data center switching devices in these areas.

- By fusing storage, processing, and networking into a single system, hyper-convergence reduces the complexity of data centers and improves scalability, which has begun to gain the attention of businesses in the North American region. An increase in the usage of a hyper-converged infrastructure platform is driving the market for data centers.

- The Patrinely Group and its financing partner, USAA Real Estate, introduced Corscale, a new data center development platform, to the Northern Virginia market last year. The company's first project is Gainesville Crossing, a 300-megawatt complex in Prince William County with five data centers designed for hyper-scale clients.

- In recent years, the region has also widely adopted the 200GbE and 400GbE switch ports. Hewlett Packard Enterprise (HPE), for instance, in the previous and current year, introduced the 32-port 200GbE SN3700M switch, which is designed specifically for the modern data center. The switch has a groundbreaking 8.33Bpps packet processing rate and a bidirectional switching capacity of up to 12.8Tb/s when powered by the 50G PAM-4-based Spectrum-2 ASIC.

Data Center Switch Industry Overview

The Data Centre Switch market is highly competitive and has several major players. However, few significant companies currently dominate the market regarding market share. The companies follow several strategies, including expansions, mergers & acquisitions, joint ventures, collaborations, partnerships, and others; these market players have strengthened their position in the business. The major market players interpreted in the report include Cisco, Jupiter Networks, Dell EMC, Arista Networks, ZTE, Hewlett Packard Enterprise, Mellanox, Huawei, Extreme Networks, etc.

- September 2023 - Hyperscalers have chosen Arista over Cisco for data center switches. Arista focuses on cloud service providers, representing over half of the vendor's revenue. In recent years, the networking company has also attempted to "diversify its business" by dipping its feet into the enterprise market.

- April 2023 - Edgecore launched the Ultra High-Capacity 400G Switch to provide the next-generation data center network architectures. To satisfy the demands of the next-generation data center and cloud computing environments and to bring a new level of basic network architecture, Edgecore announced the launch of the DCS520, an ultra-high capacity 400G switch.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Market

- 4.4 Technology Snapshot

- 4.4.1 Bandwidth

- 4.4.2 Technology (Ethernet, Fiber Channel, and InfiniBand)

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Augmented Demand for Cloud & Edge Computing Services

- 5.1.2 Government Regulations Regarding Localization of Data Centers

- 5.2 Market Restraints

- 5.2.1 High Data Center Operational Cost

6 MARKET SEGMENTATION

- 6.1 Switch Type

- 6.1.1 Core Switches

- 6.1.2 Distribution Switches

- 6.1.3 Access Switches

- 6.2 Geography

- 6.2.1 North America

- 6.2.1.1 Unites States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 Germany

- 6.2.2.3 France

- 6.2.2.4 Rest of Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 China

- 6.2.3.2 Japan

- 6.2.3.3 India

- 6.2.3.4 South Korea

- 6.2.3.5 Rest of Asia-Pacific

- 6.2.4 Rest of the World

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Cisco Systems, Inc.

- 7.1.2 Arista Networks, Inc.

- 7.1.3 Juniper Networks, Inc.

- 7.1.4 Hewlett Packard Enterprise Development LP

- 7.1.5 NEC Corporation

- 7.1.6 Huawei Technologies Co., Ltd.

- 7.1.7 H3C Holding Limited

- 7.1.8 Lenovo Group Limited

- 7.1.9 Extreme Networks Inc.

- 7.1.10 Dell EMC

- 7.1.11 Mellanox Technologies.

- 7.1.12 Fortinet, Inc.

- 7.1.13 ZTE Corporation

- 7.1.14 Quanta Cloud Technology (QCT)

- 7.1.15 D-Link Corporation

- 7.1.16 Silicom Ltd. Connectivity Solutions

8 INVESTMENT ANALYSIS

9 FUTURE MARKET OUTLOOK

资料中心交换器市场规模、份额和成长分析(按交换器类型、技术、最终用户、频宽和地区划分)—产业预测(2026-2033 年)

资料中心交换器市场规模、份额和成长分析(按交换器类型、技术、最终用户、频宽和地区划分)—产业预测(2026-2033 年) 资料中心交换器市场按类型、连接埠速度、拓扑结构、最终用户和应用划分-2025-2032 年全球预测

资料中心交换器市场按类型、连接埠速度、拓扑结构、最终用户和应用划分-2025-2032 年全球预测 全球人工智慧(AI)资料中心交换器市场

全球人工智慧(AI)资料中心交换器市场 资料中心交换器市场:全球产业分析、市场规模、份额、成长、趋势与未来预测(2025-2032)

资料中心交换器市场:全球产业分析、市场规模、份额、成长、趋势与未来预测(2025-2032) 2025-2029年全球资料中心交换器市场

2025-2029年全球资料中心交换器市场 2025 年至 2033 年资料中心交换器市场报告(按类型、频宽、技术、最终用户和地区)

2025 年至 2033 年资料中心交换器市场报告(按类型、频宽、技术、最终用户和地区) 资料中心交换器市场 - 全球产业规模、份额、趋势、机会和预测,按最终用户、产品类型、连接埠速度、交换器类型、地区和竞争细分,2019-2029F

资料中心交换器市场 - 全球产业规模、份额、趋势、机会和预测,按最终用户、产品类型、连接埠速度、交换器类型、地区和竞争细分,2019-2029F