|

市场调查报告书

商品编码

1689706

託管应用服务:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Managed Application Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

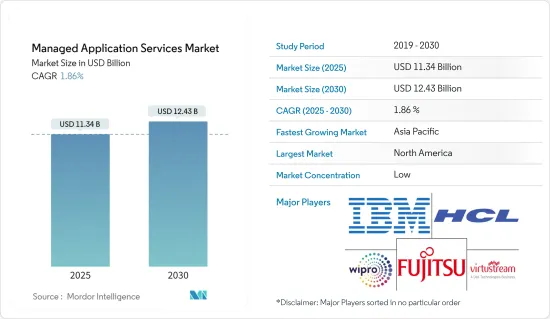

託管应用服务市场规模预计在 2025 年为 113.4 亿美元,预计到 2030 年将达到 124.3 亿美元,预测期内(2025-2030 年)的复合年增长率为 1.86%。

预测期内,对端到端应用程式託管服务的需求将会增加。託管应用程式服务可让您将某些 IT 需求外包给第三方服务提供者。企业无需花费时间实施、维护和升级 IT 相关应用程式即可降低成本、提高生产力并改善应用程式效能。预计在预测期内,智慧型手机设备的采用率和组织中物联网服务的采用率的增加将推动市场的发展。自 COVID-19 爆发以来,随着企业采用远距工作模式,对云端基础的解决方案的需求激增,但零售、製造、BFSI 等行业的收益在过去几年中大幅下降。

主要亮点

- 随着客户将工作负载转移到云端,云端原生架构(尤其是微服务)的使用正在增加。基于微服务的架构有助于提高可扩展性和速度,但在实施过程中也存在挑战。对于许多 Java 开发人员来说,Spring Boot 和 Spring Cloud 透过提供一个用于开发和部署微服务服务应用的强大、模式驱动的平台来帮助解决这些挑战。去年,为了更轻鬆地部署和管理 Spring Cloud 应用程序,微软与 Pivotal 合作创建了 Azure Spring Cloud。

- 最近,VSHN 宣布了 Project Syn。它是基于 Kubernetes 的任何基础设施上针对 DevOps 和应用程式运行的下一代开放原始码託管服务框架。 Project Syn 是一套预先整合的工具,用于在 Kubernetes 和云端中设定、更新备份、监控、回应和警报生产应用程式。透过容器、Kubernetes 和 GitOps,以完全自助服务和自动化的方式支援 DevOps。 Project Syn 很快就会成为一个开放原始码计划。它由多个元件组成,提供在 Kubernetes 上运作生产应用程式所需的功能并充当操作框架。

- 去年,AWS 宣布推出 Amazon Managed Apache Cassandra Service,这是一项可扩展、高可用且与 Apache Cassandra 相容的资料库服务,使用户能够使用自己的 Cassandra 应用程式程式码、Apache 2.0 许可的驱动程式和工具在 AWS 云端上运行 Cassandra 工作负载。使用託管 Cassandra 服务,无需设定、修补、管理伺服器,安装、维护或操作软体。表格会根据请求流量自动增加或缩小,提供几乎无限的吞吐量和储存空间。您可以使用 AWS Identity and Access Management (IAM) 管理对錶的访问,整合的日誌记录和监控有助于确保您的应用程式顺利运作。

- 近年来,由于新冠疫情引发的经济放缓,企业削减了技术投资,资讯科技支出呈下降趋势。不过,随着企业和政府机构继续对软体和IT服务进行投资,市场预计将趋于稳定。虽然短期计划被取消,但为服务供应商创造可观收益的託管应用服务产业也未能免受疫情的影响。最近,作为其 COVID-19 回应计画方案的一部分,XenonStack 为医疗保健、非政府组织、政府机构和其他直接参与救援工作的机构提供了三个月的免费託管 IT 支援、应用程式管理和云端迁移。

託管应用服务市场趋势

预计 IT 和通讯产业将占很大份额

- 由于各种技术的采用率高、BYOD 政策审查频率增加以及由于组织内资料的快速增长而对高端安全性的需求不断增长,IT 和通讯业已成为託管应用服务的关键市场。过去几年来,通讯业经历了显着的成长。在竞争激烈的市场中,电信业者不断面临以低成本提供创新服务以留住客户的压力。

- 根据最近的 SD-WAN 託管服务调查,64% 受调查的网路和 IT 经理计划在未来几年内增加 SD-WAN 託管服务。这是因为最终用户认为 SD-WAN 提供了更好的安全性、改进的云端应用程式效能和灵活的管理。这种需求促使IT和通讯服务供应商从第三方购买硬体、软体和网路的日常管理。许多 SD-WAN 託管服务供应商透过提供广泛的安全性来脱颖而出。

- 根据 Hazlecast Infinity Data 与英特尔合作发布的一份报告,IT 决策者认为云端应用程式效能 (40%) 是释放效益的最大机会,其中金融服务 (49%)、通讯(42%) 和电子商务 (40%) 在接受调查的行业中排名最高。然而,安全性(97%)和效能(90%)被认为是迁移到云端的最大挑战。

- 去年,Hazelcast 宣布在 Amazon Web Services (AWS) 上推出 Hazelcast Cloud Enterprise。它提供 Hazelcast 软体的低延迟部署作为託管服务,旨在提高云端基础的应用程式的效能、安全性和可管理性。 Hazelcast Cloud Enterprise 具有内建保护功能和与云端无关的架构,超越了现有商品云端资料储存服务的速度、规模、安全性和高可用性功能,适用于大规模企业部署。

预计北美将占很大份额

- 由于IT基础设施环境的变化,尤其是中小型企业 (SME) 对外包网路安全解决方案的持续关注,北美託管应用服务市场正在成长。例如,美国新兴 IT 供应製造商和分销商之一 Kpaul Properties LLC 聘请富士通用虚拟环境取代其实体伺服器。这使公司的成本降低了 15%,并将运转率提高了 95%。随着现代技术的快速发展和简化 IT 功能的需求,该地区越来越多的企业开始向 MSP 寻求最佳实践。

- 此外,加拿大对多重云端环境的采用和自动化的采用正在迅速增加。由于云端、行动和社交技术要求该地区的企业采取主动的IT安全方法,因此对于采用提供全方位安全控制层的强大託管服务的需求日益增长。整合通讯(UC) 即服务和相关的客服中心即服务市场为託管服务提供者提供了机会。新兴企业正在提供创新的云端基础的解决方案,这些解决方案只需极少的投资并且易于部署。

- 近日,美国託管云端处理公司Rackspace宣布,已同意收购亚马逊网路服务(AWS)合作伙伴网路(APN)首席咨询合作伙伴及AWS託管服务供应商Onika。此次收购将 Onika 的创新专业服务能力(包括策略咨询、架构、工程和应用开发)添加到 Rackspace 的产品组合中,并补充其现有的託管云端服务能力。 Rackspace 的混合云产品组合使企业能够利用从IT安全到软体开发等一系列技术增强功能。

- 印孚瑟斯公司去年在亚利桑那州凤凰城推出了 Infosys Live Enterprise Suite。该套件是一套全面的平台、解决方案和数位服务,可加速企业的数位转型之旅。透过 Infosys Polycloud 平台,使用者可以利用跨云端供应商的最佳创新来建立与云端无关的应用程式堆迭。该平台提供了一个抽象公共云端云和私有云端的背板,为整个企业的平台和应用服务工作负载的选择、配置、移动和管理提供了标准的介面和目录。

託管应用服务产业概况

託管应用服务市场竞争十分激烈,没有任何企业能独占主导地位。比赛的结果取决于公司的最佳特征:高品质、价格合理的服务。市场的一些主要参与者包括 IBM 公司、HCL Technologies Limited、WIPRO Limited 和富士通有限公司。市场的最新趋势包括:

- 2022 年 5 月-微软推出了一个名为「微软安全专家」的新託管服务类别。该服务为组织提供外部安全专家的协助,以协助威胁发现、侦测和回应活动。对于企业而言,该服务使现场安全团队能够在异地微软专家的协助下增强其能力。

- 2022 年 2 月-IBM 与 SAP(NYSE:SAP)合作,提供技术和咨询专业知识,协助受监管和非监管产业的客户采用混合云方法,并将关键任务工作负载从 SAP 解决方案迁移到云端。作为 RISE with an SAP 的一部分,IBM 是第一个提供云端基础设施和技术託管服务的合作伙伴。

- 此外,当客户考虑混合云策略时,他们需要一个安全可靠的云端环境来迁移其关键任务工作负载和应用程式。随着 IBM 推出针对 SAP 的 RISE 供应商选项,客户现在拥有了工具来加速将本机 SAP 软体工作负载迁移到 IBM Cloud,并以业界领先的安全功能为后盾。

- 此外,IBM 正在与 IBM 合作推出一项名为「BREAKTHROUGH with IBM for RISE with SAP」的新计画。该计划包括一系列解决方案和咨询服务,以加速和扩大您向 SAP S/4HANA Cloud 迈进的步伐。我们的解决方案和服务建立在灵活、可扩展的平台上,使用智慧工作流程来简化业务。我们提供一种参与模式来帮助您规划、执行和支援您的完整业务转型。它还为您提供了将 SAP 解决方案工作负载迁移到公有云的选项和灵活性,利用我们深厚的行业专业知识。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查结果

- 调查前提

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概况

- 市场驱动因素

- 端到端应用程式託管需求不断增长

- 改进并保护您的关键业务应用程式

- 提高应用程式基础架构的标准

- 市场限制

- 与应用程式资料相关的安全风险

- 价值链/供应链分析

- 波特五力分析

- 新进入者的威胁

- 购买者/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

- PESTLE分析

第五章 市场区隔

- 组织规模

- 中小型企业

- 大型企业

- 按最终用户产业

- BFSI

- 零售与电子商务

- 资讯科技和电信

- 製造业

- 卫生保健

- 地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 西班牙

- 其他欧洲国家

- 亚太地区

- 印度

- 中国

- 日本

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 其他中东地区

- 北美洲

第六章 竞争格局

- 供应商市场占有率

- 合併和收购

- 公司简介

- Fujitsu Limited

- IBM Corporation

- HCL Technologies Limited

- Wipro Limited

- VIRTUSTREAM INC.

- RACKSPACE INC.

- CenturyLink, Inc.

- DXC Technology Company

- BMC Software, INC.

- Mindtree Limited

- Unisys Corporation

第七章 市场机会与未来趋势

The Managed Application Services Market size is estimated at USD 11.34 billion in 2025, and is expected to reach USD 12.43 billion by 2030, at a CAGR of 1.86% during the forecast period (2025-2030).

Demand for end-to-end application hosting services will increase in the forecast period. The managed application services allow the organization to outsource specific IT requirements to a third-party service provider. The companies can reduce costs, boost productivity, and enhance application performance without spending time on implementation, maintenance, and upgradation of their IT-related application. The increase in the adoption of smartphone devices and the implementation of IoT services in the organization will drive the market in the forecast period. Since the outbreak of COVID-19, the demand for cloud-based solutions has seen significant growth owing to remote working models being adopted by enterprises; however, various industries such as retail, manufacturing, BFSI, and others have seen a significant slump in their revenues in the past years.

Key Highlights

- As customers have moved their workloads to the cloud, there is a growth in the usage of cloud-native architectures, particularly microservices. Microservice-based architectures help improve scalability and velocity, but implementing them can pose challenges. For many Java developers, Spring Boot and Spring Cloud have helped address these challenges, providing a robust platform with well-established patterns for developing and operating microservice applications. In the previous year, to help make it simpler to deploy and manage Spring Cloud applications, together with Pivotal, Microsoft created Azure Spring Cloud.

- Recently, VSHN announced Project Syn, the next generation Open Source managed services framework for DevOps and application operations on any infrastructure based on Kubernetes. Project Syn is a pre-integrated set of tools to provision, update backup, observe, and react or alert production applications on Kubernetes and in the cloud. It supports DevOps through complete self-service and automation with the help of containers, Kubernetes, and GitOps. Project Syn is about to become an Open Source project shortly. It consists of several components that bring the necessary features for running applications in production on Kubernetes, acting as an operations framework.

- During the previous year, AWS launched Amazon Managed Apache Cassandra Service, a scalable, highly available, and managed Apache Cassandra-compatible database service that enables the user to run the Cassandra workloads in the AWS Cloud utilizing the same Cassandra application code, Apache 2.0 licensed drivers, and tools that are used. With Managed Cassandra Service, there is no need to provision, patch, or manage servers and install, maintain, or operate the software. Tables could scale up and down automatically based on request traffic, with virtually unlimited throughput and storage. The user can manage access to the tables using AWS Identity and Access Management (IAM) and keep the applications running smoothly with integrated logging and monitoring.

- Information Technology spending in recent years is likely to fall as organizations trim investments in technology in the wake of the COVID-19 pandemic-led slowdown. However, enterprises and government agencies continue to invest in software and IT services, which is expected to stabilize the market. While short-term projects are getting stopped, the managed application services segment, which fetches significant revenue for service providers, has not been impacted by the outbreak. Recently, XenonStack offered a free 3-month Managed IT Support, Application Management, and Migration to the Cloud as part of their COVID-19 response plan program to anyone directly involved in relief initiatives like Healthcare, NGOs, and government bodies.

Managed Application Services Market Trends

IT and Telecom is Expected to Hold Major Share

- The IT and telecom sector is a significant market for managed application services due to the high rate of various technological adoptions, increased frequency of confirmation of the BYOD policy, and an increased need for high-end security due to the rapidly growing data among organizations. The telecom industry has observed extensive growth during the past few years. Telecommunication companies are constantly pressured to deliver innovative services at lower costs to retain their customers in the competitive market.

- According to the SD-WAN Managed Services recent survey, 64% of the surveyed network and IT managers plan to add an SD-WAN managed service in the upcoming years. This is because the end-users believe it will deliver better security, improved cloud application performance, and flexible management. This demand is encouraging IT and Telcom service providers to purchase hardware, software, and regular administration of their networks from a third party. Many SD-WAN-managed service providers are differentiating themselves with a wide range of security offerings.

- According to Hazlecast Infinity Data report in collaboration with Intel, IT decision-makers identified cloud application performance (40%) as the number one opportunity to unlock profits, with financial services (49%), telecommunications (42%), and e-commerce (40%) ranking it the highest among verticals surveyed. However, security (97%) and performance (90%) were the top challenges when migrating to the cloud.

- In the previous year, Hazelcast announced the availability of Hazelcast Cloud Enterprise on Amazon Web Services (AWS), a low-latency deployment of Hazelcast software as a managed service designed to improve the performance, security, and ease of management of cloud-based applications. Featuring built-in protection and a cloud-agnostic architecture, Hazelcast Cloud Enterprise exceeds the speed, scale, safety, and high availability capabilities of existing commoditized cloud data storage services for large-scale enterprise deployments.

North America is Expected to Hold Major Share

- The North American Managed Application Services market is growing due to the changing IT infrastructure landscape, especially in small and medium enterprises (SMEs), continually focusing on outsourcing cybersecurity solutions. For instance, Kpaul Properties LLC, one of the emerging manufacturers and distributors of IT supplies in the United States, onboarded FUJITSU to replace physical servers with a virtualized environment. This has reduced the company's cost by 15% and delivered 95% uptime. With the speedy acceleration of modern technology and the need for streamlined IT functions, an increasing number of businesses in the region find the best way to keep pace with MSP.

- Besides, Canada is witnessing a high rise in the application of multi-Cloud environments and increased adoption of automation. In the region, Cloud, mobile, and social technologies demand that businesses take a proactive approach toward IT security, thus boosting the demand for deploying robust managed services that would deliver in all security management layers. Unified Communications as a Service and related Contact Center as a Service market represent a business opportunity for managed service providers. This is because emerging players offer innovative cloud-based solutions, which require a minimum investment and are easy to deploy.

- Recently, Rackspace, an American-managed Cloud computing company, announced that it has agreed to acquire Onica, an Amazon Web Services (AWS) Partner Network (APN) Premier Consulting Partner and AWS Managed Service Provider. This acquisition brings Onica's innovative professional services capabilities, including strategic advisory, architecture, engineering, and application development, to the Rackspace portfolio, complementing its existing managed cloud services capabilities. Rackspace's hybrid cloud portfolio enables enterprises to leverage various technical enhancements, from IT security to software development.

- In the previous year, Infosys unveiled the Infosys Live Enterprise Suite in Phoenix, Arizona, a comprehensive set of platforms, solutions, and digital services that helps enterprises to accelerate their digital innovation journey. The user can embrace the best innovations across cloud providers and build a cloud-agnostic application stack through the Infosys Polycloud Platform. The platform provides a backplane that abstracts the public and private clouds, enabling a standard interface and catalog to select, provision, move and manage platform and application services workloads across the enterprise.

Managed Application Services Industry Overview

The competition within the managed application services market is high among the market players without any specific dominating player. The competition results are based on the enterprise's best features of high quality and services at a reasonable price. Some significant players in the market are IBM Corporation, HCL Technologies Limited, WIPRO Limited, Fujitsu Ltd., and others. Some of the recent trends in the market are as follows:

- May 2022 - Microsoft launched a new managed service category known as Microsoft Security Experts. The service provides organizations with assistance from external security experts who can perform threat hunting and managed detection and response tasks. For businesses, the service enables on-site security teams to supplement their capabilities with assistance from off-site Microsoft experts.

- February 2022 - IBM partnered with SAP (NYSE: SAP) to provide technology and consult experts to help clients embrace a hybrid cloud approach and migrate mission-critical workloads from SAP solutions to the cloud in regulated and non-regulated industries. As part of the RISE with an SAP offering, IBM is the first partner to provide cloud infrastructure and technical managed services.

- Moreover, as clients consider hybrid cloud strategies, moving the workloads and applications that are the backbone of their enterprise operations necessitates a highly secure and reliable cloud environment. With the launch of the IBM supplier option for RISE with SAP, clients have the tools to help accelerate the migration of their on-premise SAP software workloads to IBM Cloud, backed by industry-leading security capabilities.

- In addition, IBM is launching a new program called BREAKTHROUGH with IBM for RISE with SAP, which includes a portfolio of solutions and consulting services to help accelerate and amplify the journey to SAP S/4HANA Cloud. The solutions and services, built on a flexible and scalable platform, use intelligent workflows to streamline operations. They offer an engagement model that aids in the planning, execution, and support of holistic business transformation. Clients are also given the option and flexibility to migrate SAP solution workloads to the public cloud with the help of deep industry expertise.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased demand for end-to-end application hosting

- 4.2.2 The requirement to improve and secure critical business applications

- 4.2.3 Increase in the level of application infrastructure

- 4.3 Market Restraints

- 4.3.1 Security risks associated with application data

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Porters 5 Force Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 PESTLE Analysis

5 MARKET SEGMENTATION

- 5.1 Organization Size

- 5.1.1 Small & Medium-scale Enterprises

- 5.1.2 Large Enterprises

- 5.2 End-user Verticals

- 5.2.1 BFSI

- 5.2.2 Retail & E-Commerce

- 5.2.3 IT & Telecom

- 5.2.4 Manufacturing

- 5.2.5 Healthcare

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Rest of Asia Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.5 Middle East

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle East

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Mergers & Acquisitions

- 6.3 Company Profiles

- 6.3.1 Fujitsu Limited

- 6.3.2 IBM Corporation

- 6.3.3 HCL Technologies Limited

- 6.3.4 Wipro Limited

- 6.3.5 VIRTUSTREAM INC.

- 6.3.6 RACKSPACE INC.

- 6.3.7 CenturyLink, Inc.

- 6.3.8 DXC Technology Company

- 6.3.9 BMC Software, INC.

- 6.3.10 Mindtree Limited

- 6.3.11 Unisys Corporation