|

市场调查报告书

商品编码

1689722

永续包装:市场占有率分析、行业趋势和统计数据、成长预测(2025-2030 年)Sustainable Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

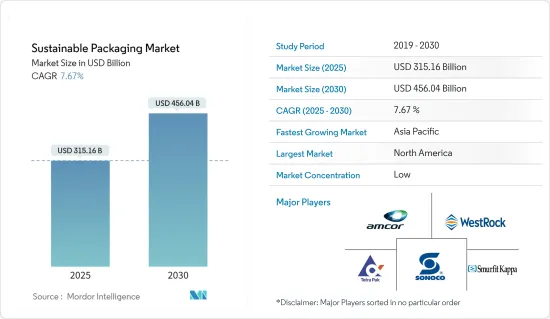

永续包装市场规模预计在 2025 年为 3,151.6 亿美元,预计到 2030 年将达到 4,560.4 亿美元,预测期内(2025-2030 年)的复合年增长率为 7.67%。

关键亮点

- 永续包装涉及开发和使用增强永续性的包装解决方案。他们严重依赖生命週期评估和清单来指导决策并最大限度地减少环境影响。

- 近年来,消费者对永续性的兴趣显着增加。循环经济的兴起进一步凸显了永续包装的重要性。为了回应民众对包装废弃物(尤其是一次性塑胶)的担忧,世界各国政府正在製定严格的法规,以遏制环境破坏并改善废弃物管理。

- 法国、德国和英国等国家处于领先地位,它们不仅在欧盟内部实施了强有力的回收措施,而且还采用了生产者延伸责任制(EPR)。在亚洲,泰国从2020年1月1日起在全国范围内禁止在主要商店使用一次性塑胶袋,最终目标是减少塑胶污染。

- 根据海洋保护协会的统计,每年有 800 万吨塑胶进入海洋,而目前海洋中的塑胶总量约为 1.5 亿吨。这是一个严重的问题。换个角度来看,这就相当于一年内每分钟向海洋中倾倒一辆纽约市垃圾车的塑胶。调查显示,2025年是环保包装的关键一年,超过40%的受访者计画采用创新、永续的包装技术。公司越来越多地转向循环经济,使用可堆肥和生物分解性的材料,并重新设计包装以减少废弃物。

- 然而,既不可回收又生物分解的塑胶包装的使用正在增加,加剧了我们的碳排放。作为回应,亚马逊、谷歌和利乐等大公司都设定了实现净零碳排放的雄心勃勃的目标,预计此举将需要大量的资本投入。

永续包装市场的趋势

再生包装占据了大部分市场份额

- 消费者对永续产品的需求不断增长,推动了再生包装的成长。随着环保意识的增强,消费者正在积极寻找优先考虑永续性,尤其是在包装选择方面。这种消费者转变促使各领域的企业转向再生包装,以满足消费者的期望并增强企业的社会责任。同时,回收技术的进步正在简化回收材料与包装的结合,使製造商更具成本效益,进一步推动市场成长。

- 全球政府和监管机构在再生包装市场的扩张中发挥着至关重要的作用。他们制定了严格的法规和政策,重点是控制塑胶废弃物和促进回收。特别是,欧盟循环经济行动计画等措施以及美国和加拿大等国家减少塑胶废弃物的授权正在引导企业投资永续包装。这些指令不仅要求使用再生材料,还鼓励包装设计和材料科学的创新,旨在提高可回收性并最大限度地减少对环境的影响。

- 回收过程中的技术进步对于再生包装市场的成长至关重要。化学回收等创新技术将塑胶分解成其原始单体,为包装中的高品质再生材料铺平了道路。这些进步解决了传统机械回收的局限性,例如材料劣化和某些塑胶的可回收性有限。随着技术的不断进步,再生包装的品质和功效正在提高,预计将进一步刺激市场需求。

- 企业越来越意识到回收包装的经济效益。透过采用再生材料,公司可以减少对原始资源的依赖,降低生产成本并为供应链中断做好准备。此外,采用再生包装的品牌不仅能引起有环保意识的消费者的共鸣,还能使自己与竞争对手区分开来,并增加吸引力。因此,包装领域的大小企业都在大力投资再生包装解决方案,支持市场强劲的成长轨迹。

亚太地区:预计市场将大幅成长

- 中国各大电商和宅配服务都在积极致力于减少包装材料。例如,顺丰速运推出可回收包装箱,每个包装箱可回收约10次。顺丰速运已在全国各大城市部署超过10万个包装箱,其中包括一线城市和多个二线城市。其主要用途是取代传统的纸盒和塑胶袋,减少发泡块和胶带的使用。顺丰强调,这些努力符合推动中国永续物流发展的目标。该公司还投资研发,以创造更耐用、更环保的包装解决方案,确保其使用的材料能够承受重复使用,而不会损害内容物的安全性和完整性。

- 印度中产阶级的崛起、有组织的零售业的快速扩张、出口的成长以及电子商务产业的蓬勃发展都为所研究市场的成长铺平了道路。但这种成长需要环保包装,以确保一流的品质,同时最大限度地减少对环境的影响。因此,企业采用永续包装方式正成为重中之重。越来越多的公司开始使用生物分解性的材料,减少塑胶的使用,并引入创新设计以最大程度地减少废弃物。此外,政府法规和消费者意识正在推动向更环保的包装解决方案转变,许多公司设定了雄心勃勃的永续性目标以满足这些新标准。

- Capgemini SA最近的一项研究深入探讨了永续性和不断变化的消费行为。调查显示,79% 的消费者正在改变他们的购买模式,主要是出于社会责任、整体性和环境的考量。值得注意的是,53% 的消费者和 57% 的 18-24 岁年轻人被不太知名的品牌所吸引,因为它们是环保的。此外,超过一半的受访者(52%)表示对优先考虑永续性的公司有情感连结。调查也强调,消费者愿意为永续包装的产品支付溢价,显示市场对环保产品的需求强劲。适应这些偏好的品牌可以避免将市场占有率拱手让给更有环保意识的竞争对手。

- 该地区的主要企业处于创新的前沿,推动着永续包装市场的成长。这些创新包括开发植物来源塑胶等新材料、先进的回收技术和智慧包装解决方案,以延长产品保质期,同时减少对环境的影响。产业领袖、新兴企业和研究机构之间的合作努力也正在培养包装产业持续改进和永续性的文化。

永续包装产业概览

永续包装市场高度分散,主要企业包括 Amcor Limited、TetraPak International SA、WestRock Company、Smurfit Kappa Group PLC 和 Sonoco Products Company。

- 2024年5月,安姆可与化妆品主要企业雅芳宣布在中国推出雅芳沐浴凝胶黑裙沐浴露填充用装Amplima Plus。这项策略性倡议旨在减少碳排放和水消费量。

- 2024年3月,提供印刷包装解决方案的全球公司TOPPAN推出了基于双轴延伸聚丙烯(BOPP)的阻隔膜“GL-SP”,彻底改变了永续包装。该新产品加入了 GL BARRIER 系列,该系列以其透明沉淀阻隔膜而闻名,拥有世界领先的市场份额。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业价值链分析

- 产业吸引力波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 竞争对手之间的竞争强度

- 替代品的威胁

- 评估微观经济因素对产业的影响

第五章市场动态

- 市场驱动因素

- 政府推动永续包装的倡议

- 缩小包装尺寸

- 消费者偏好转向可回收和环保材料

- 市场限制

- 製造工厂产能限制

- 原料高成本

第六章市场区隔

- 按工艺

- 可重复使用的包装

- 可降解包装

- 再生包装

- 依材料类型

- 玻璃

- 塑胶

- 金属

- 纸

- 按最终用户

- 製药和医疗

- 化妆品和个人护理

- 饮食

- 其他的

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第七章竞争格局

- 公司简介

- Amcor Limited

- Westrock Company

- TetraPak International SA

- Sonoco Products Company

- Smurfit Kappa Group PLC

- Sealed Air Corporation

- Mondi PLC

- Huhtamaki OYJ

- BASF SE

- Ardagh Group SA

- Ball Corporation

- Crown Holdings Inc.

- DS Smith PLC

- Genpak LLC

- International Paper Company

第八章投资分析

第九章 市场展望

The Sustainable Packaging Market size is estimated at USD 315.16 billion in 2025, and is expected to reach USD 456.04 billion by 2030, at a CAGR of 7.67% during the forecast period (2025-2030).

Key Highlights

- Sustainable packaging involves developing and utilizing packaging solutions that enhance sustainability. It relies heavily on life cycle assessments and inventories to guide decisions and minimize environmental impact.

- In recent years, consumer interest in sustainability has surged significantly. The rise of circular economics has further underscored the importance of sustainable packaging. Governments worldwide, responding to public concerns over packaging waste, particularly single-use plastics, are enacting stringent regulations to curb environmental harm and bolster waste management.

- Leading the charge, countries like France, Germany, and the United Kingdom are not only enforcing robust recycling measures within the European Union but are also adopting extended producer responsibilities (EPRs). In Asia, Thailand implemented a nationwide ban on single-use plastic bags in major stores starting January 1, 2020, with the ultimate goal of reducing plastic pollution.

- According to the Ocean Conservancy statistics, 8 million metric tons of plastic enter the oceans annually, adding to the estimated 150 million metric tons already present. This is a critical issue. To put this in perspective, it is akin to dumping a New York City garbage truck's load of plastic into the ocean every minute for a year. The survey identifies 2025 as a pivotal year for eco-friendly packaging, with over 40% of respondents planning to adopt innovative and sustainable packaging techniques. Companies are increasingly pivoting toward a circular economy, utilizing compostable materials and biodegradables and rethinking container designs to reduce waste.

- However, the use of non-recyclable, non-biodegradable plastic packaging is on the rise, exacerbating carbon emissions. In response, major corporations like Amazon, Google, and Tetrapak are setting ambitious targets, aiming for net-zero carbon emissions, a move expected to entail significant capital investments.

Sustainable Packaging Market Trends

The Recycled Packaging Segment to Hold Significant Share in Market

- Increasing consumer demand for sustainable products is driving the growth of recycled packaging. As environmental awareness rises, consumers are actively seeking brands that prioritize sustainability, particularly in their packaging choices. This consumer shift is compelling companies across sectors to pivot toward recycled packaging, aligning with both consumer expectations and bolstering their corporate social responsibility standings. Simultaneously, advancements in recycling technologies are streamlining the incorporation of recycled materials into packaging, enhancing cost-effectiveness for manufacturers, and further amplifying market growth.

- Global governments and regulatory bodies are pivotal in expanding the recycled packaging market. They are enacting stringent regulations and policies, with a primary focus on curbing plastic waste and promoting recycling. Notably, initiatives like the European Union's Circular Economy Action Plan and plastic waste reduction mandates in countries like the United States and Canada are nudging companies toward sustainable packaging investments. These directives not only mandate the use of recycled materials but also foster innovation in packaging design and material science, aiming to bolster recyclability and minimize environmental footprints.

- Technological strides in recycling processes are pivotal for the growth of the recycled packaging market. Innovations like chemical recycling, which breaks down plastics into their original monomers, are paving the way for high-quality recycled materials in packaging. These advancements are addressing limitations seen in traditional mechanical recycling, like material degradation and the restricted recyclability of certain plastics. With ongoing technological evolution, the quality and efficacy of recycled packaging are poised to elevate, further stoking market demand.

- Businesses are increasingly recognizing the economic merits of recycled packaging. By embracing recycled materials, companies can diminish their dependence on virgin resources, trim production costs, and buffer themselves against supply chain disruptions. Moreover, brands adopting recycled packaging not only resonate with environmentally conscious consumers but also carve out a distinct niche from their competitors, bolstering their market appeal. Consequently, both major players and smaller enterprises in the packaging realm are channeling substantial investments into recycled packaging solutions, underpinning the market's robust growth trajectory.

Asia-Pacific Expected to Register Significant Market Growth

- Chinese e-commerce giants and express delivery services are actively cutting down on packaging materials. For example, SF Express introduced recyclable packaging boxes, each capable of being recycled approximately ten times. In major cities, including first-tier and several second-tier ones, the company deployed over 100,000 of these boxes. Its primary aim is to replace traditional paper boxes and plastic bags, thereby reducing the usage of foam blocks and tape. SF Express emphasized that these efforts align with China's push for sustainable logistics growth. The company has also invested in research and development to create more durable and eco-friendly packaging solutions, ensuring that the materials used can withstand multiple cycles of use without compromising the safety and integrity of the contents.

- The rise of India's middle class, the rapid expansion of organized retail, increasing exports, and the booming e-commerce industry are all paving the way for the growth of the market studied. This growth, however, necessitates environmentally friendly packaging that ensures top-notch quality with minimal environmental repercussions. Consequently, the adoption of sustainable packaging practices by companies is gaining paramount importance. Companies are increasingly focusing on biodegradable materials, reducing plastic usage, and implementing innovative designs that minimize waste. Additionally, government regulations and consumer awareness are driving the shift toward greener packaging solutions, with many firms setting ambitious sustainability targets to meet these new standards.

- A recent survey by Capgemini delved into sustainability and changing consumer behavior. It revealed that 79% of consumers are altering their buying patterns, primarily driven by social responsibility, inclusivity, and environmental concerns. Notably, 53% of all consumers and a significant 57% of those aged 18 to 24 are gravitating toward lesser-known brands due to their eco-friendliness. Moreover, over half (52%) of respondents expressed an emotional connection with businesses prioritizing sustainability. The survey also highlighted that consumers are willing to pay a premium for sustainably packaged products, indicating a strong market demand for eco-friendly options. Brands that adapt to these preferences avoid losing market share to more environmentally conscious competitors.

- Key players in the region are spearheading innovations, propelling the growth of the sustainable packaging market. These innovations include the development of new materials such as plant-based plastics, advanced recycling technologies, and smart packaging solutions that enhance product shelf life while reducing environmental impact. Collaborative efforts between industry leaders, startups, and research institutions are also fostering a culture of continuous improvement and sustainability in the packaging industry.

Sustainable Packaging Industry Overview

The sustainable packaging market exhibits a high degree of fragmentation, with prominent players such as Amcor Limited, TetraPak International SA, WestRock Company, Smurfit Kappa Group PLC, and Sonoco Products Company. These companies are actively engaged in developing innovative and eco-friendly packaging solutions to meet the growing demand for sustainable practices. They invest significantly in research and development to enhance the recyclability and biodegradability of their products, striving to reduce the environmental impact of packaging materials. Additionally, these key players often collaborate with other stakeholders in the supply chain to encourage sustainability and adhere to stringent regulatory standards.

- May 2024: Amcor and AVON, a leading cosmetics company, announced the launch of the AmPrima Plus refill pouch for AVON's Little Black Dress shower gels in China. This strategic initiative aims to reduce both carbon footprint and water consumption.

- March 2024: TOPPAN, a global player in printing and packaging solutions, revolutionized sustainable packaging with the launch of GL-SP, a barrier film utilizing biaxially oriented polypropylene (BOPP) as the substrate. This new product has been added to the GL BARRIER series, renowned for its transparent vapor-deposited barrier films, which hold a leading share in the global market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness: Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitute Products

- 4.4 Assessment of the Impact of Microeconomic Factors on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Government Initiatives Toward Sustainable Packaging

- 5.1.2 Downsizing of Packaging

- 5.1.3 Shift in Consumer Preferences Toward Recyclable and Eco-friendly Materials

- 5.2 Market Restraints

- 5.2.1 Capacity Constraint of Manufacturing Plants

- 5.2.2 High Cost of Raw Materials

6 MARKET SEGMENTATION

- 6.1 By Process

- 6.1.1 Reusable Packaging

- 6.1.2 Degradable Packaging

- 6.1.3 Recycled Packaging

- 6.2 By Material Type

- 6.2.1 Glass

- 6.2.2 Plastic

- 6.2.3 Metal

- 6.2.4 Paper

- 6.3 By End User

- 6.3.1 Pharmaceutical and Healthcare

- 6.3.2 Cosmetics and Personal Care

- 6.3.3 Food and Beverage

- 6.3.4 Other End Users

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor Limited

- 7.1.2 Westrock Company

- 7.1.3 TetraPak International SA

- 7.1.4 Sonoco Products Company

- 7.1.5 Smurfit Kappa Group PLC

- 7.1.6 Sealed Air Corporation

- 7.1.7 Mondi PLC

- 7.1.8 Huhtamaki OYJ

- 7.1.9 BASF SE

- 7.1.10 Ardagh Group SA

- 7.1.11 Ball Corporation

- 7.1.12 Crown Holdings Inc.

- 7.1.13 DS Smith PLC

- 7.1.14 Genpak LLC

- 7.1.15 International Paper Company

8 INVESTMENT ANALYSIS

9 MARKET OUTLOOK

永续包装市场(按材料、永续性类型、应用和分销管道)—2025-2032 年全球预测

永续包装市场(按材料、永续性类型、应用和分销管道)—2025-2032 年全球预测 零废弃包装市场-全球产业规模、份额、趋势、机会与预测,依材料、类型、配销通路、应用、地区和竞争细分,2020-2030 年

零废弃包装市场-全球产业规模、份额、趋势、机会与预测,依材料、类型、配销通路、应用、地区和竞争细分,2020-2030 年 2025年全球环保包装市场报告

2025年全球环保包装市场报告 永续塑胶包装市场规模、份额及成长分析(按包装类型、製程、应用和地区)-产业预测,2025-2032

永续塑胶包装市场规模、份额及成长分析(按包装类型、製程、应用和地区)-产业预测,2025-2032 2032 年永续包装市场预测:按材料类型、包装类型、工艺、功能、分销管道、应用和地区进行的全球分析

2032 年永续包装市场预测:按材料类型、包装类型、工艺、功能、分销管道、应用和地区进行的全球分析 全球永续塑胶包装市场

全球永续塑胶包装市场 纸币的生命週期(~2030年)2025年永续塑胶包装全球市场报告全球零废弃物包装市场

纸币的生命週期(~2030年)2025年永续塑胶包装全球市场报告全球零废弃物包装市场 永续产品和服务开启新市场:供应商、营运商和云端服务供应商的机会

永续产品和服务开启新市场:供应商、营运商和云端服务供应商的机会