|

市场调查报告书

商品编码

1689766

化学机械平坦化(CMP)浆料:市场占有率分析、产业趋势与成长预测(2025-2030)Chemical Mechanical Planarization (CMP) Slurry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

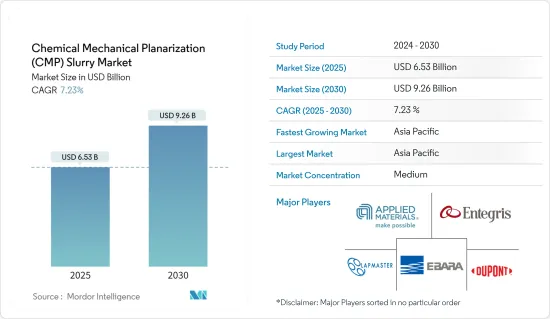

化学机械平坦化浆料市场规模预计在 2025 年为 65.3 亿美元,预计到 2030 年将达到 92.6 亿美元,预测期内(2025-2030 年)的复合年增长率为 7.23%。

关键亮点

- 由于製造技术和半导体製程的进步提高了半导体产品的性能,预计 CMP 市场在预测期内将实现稳步成长。市场成长的动力来自于製造商为实现产品创新而加大对半导体晶圆製造材料的投资。

- 化学机械抛光或平坦化(CMP)使粗糙的表面变得平整,并在半导体製造中提供许多好处。 CMP 可在一次操作中实现整个晶圆的均匀平整度。 CMP 用途广泛,可以平坦化从金属到氧化膜的各种材料,并且通常可以同时处理多种材料。

- CMP 解决方案透过提供均匀的平坦化和减少晶圆表面的缺陷,在实现高产量比率方面发挥关键作用。透过开发具有成本效益的 CMP 浆料,製造商可以优化其生产流程并显着降低成本。 CMP 可应用于光学、光电、资料储存、医疗设备等领域。 CMP应用领域的扩展将为CMP解决方案製造商创造新的市场机会,进一步推动市场成长。

- 各种 CMP 製程对精确製程控制和减少缺陷的严格要求影响着装置性能、产量比率和批量製造挑战。此外,磨料的复杂性也推动 CMP 耗材的创新。新耗材的品管正在扩大,影响製程窗口和生产线,减缓全球 CMP 设备和耗材製造的速度。

- 疫情过后,由于汽车、家用电子电器和医疗产品销售的成长,对积体电路的需求激增。例如,根据WSTS预测,2024年全球IC市场销售额将达到约4,870亿美元。

化学机械平坦化(CMP)浆料市场趋势

预测期内,积体电路将占据最大的市场占有率

- 对更高功能和更小电子设备的需求不断增长,刺激了市场对高密度嵌入式 IC 和 VLSI 的需求,为 CMP 设备和耗材创造了成长机会。化学机械平坦化(CMP)是半导体产业中的重要製程。 CMP 製程对于积体电路和储存盘的製造至关重要,因为它可以透过化学反应和机械力的结合有效地去除表面材料。

- 此外,随着超大规模积体电路(VLSI)的出现,数十万个电晶体现在可以整合到单一硅半导体微晶片上。这项工艺可实现小型化、高性能和多功能化。然而,挑战在于将许多组件装入有限的空间并尽量减少错误。这增加了彻底清除安装表面碎屑的需要,强调了化学机械抛光在积体电路製造中的重要性。预计这将有助于市场与全球积体电路製造业同步成长。

- 美国、台湾、韩国、中国等国家是半导体晶片的主要生产国。消费和投资也对市场成长做出了重大贡献。 CMP已成为半导体製造商生产积体电路(IC)的标准製造流程。预计物联网、汽车和 5G 等市场对各种组件的采用率不断提高将在预测期内推动对 CMP 设备的需求。

- 在半导体製造商、政府和其他国际组织的投资活动的支持下,市场正在取得重大发展,透过最大限度地减少对少数国家半导体供应链的依赖来加强全球半导体生态系统,这将推动对 CMP 市场的需求,因为抛光製程在全球积体电路製造中的应用。

- 例如,马来西亚计划于2024年4月建成东南亚最大的积体电路设计园区,以促进国内半导体设计、原型设计和製造。马来西亚政府将提供多项奖励,包括税收优惠、办公空间补贴和免签证费,以吸引高科技公司和投资者入驻该工厂,支持该国的积体电路製造生态系统,并为 CMP 市场创造成长机会。

- CMP 製程还包括一个化学成分,可以有针对性地去除特定材料。与纯机械抛光相比,CMP 可最大限度地减少表面缺陷,并使得光刻製程能够应用于 IC 製造。

- 预计未来几年全球半导体销售额的成长将推动 CMP 市场的需求。根据SIA统计,2024年1月全球半导体销售额达476.3亿美元,较去年同期成长60多亿美元。

亚太地区实现强劲成长

- 亚太地区是全球许多半导体製造工厂的所在地,其中包括台积电和三星电子等大公司。台湾是全球晶圆代工领域的领导者,在半导体价值链中扮演关键角色。在政府措施的支持下,该地区的半导体产业正经历显着成长,推动市场扩张。

- 亚太地区的半导体销售额逐年成长,预计将推动CMP市场的需求。根据WSTS预测,该地区的半导体销售额预计将在2024年和2025年大幅成长。 2023年,该地区的销售额预计将达到2,899.9亿美元,到2024年将增至3,408.7亿美元,到2025年将增至3,829.6亿美元。 WSTS预测,对积体电路、分立元件和其他半导体的需求增加预计将推动与前一年同期比较和2025年分别大幅成长17.5%和12.3%。预计此类发展将推动CMP市场的需求。

- 由于三星和 SK 海力士等大公司的存在以及半导体业务的巨大增长,韩国等国家成为 CMP 技术需求的主要推动力。 2024年1月,韩国政府宣布投资约4,700亿美元建立全球最大半导体丛集的策略。这个雄心勃勃的计划将在未来 23 年内展开,并将与 SK Hynix 合作在京畿道建造一个大型生产基地。随着 SK Hynix 等公司的投资不断增加,CMP 市场的需求预计也将上升。

- 2024 年 3 月,东进半导体开始向 SK 海力士供应用于高频宽记忆体 (HBM) 生产的化学机械抛光 (CMP) 浆料。此浆料在晶圆製造的CMP过程中对平滑表面起着重要作用。具体来说,氧化物浆料用于平坦化绝缘层,而金属浆料用于平坦化金属电路。该协议将终止 Soulbrain 在韩国对 HBM 製造材料的独家权利。预计此类市场发展将推动未来几年的市场成长。

- 此外,由于中国地区拥有强大的半导体製造能力,预计市场将显着成长。中国是半导体製造市场的主要企业,在该地区拥有大量工厂。根据WSTS报告,2024年1月中国半导体销售额将达147.6亿美元。这一数字较2023年1月的116.6亿美元有显着成长。在美国战争等地缘政治紧张局势加剧的背景下,该地区正在进行大规模投资以促进国内生产。

化学机械平坦化(CMP)浆料产业概述

化学机械平坦化 (CMP) 浆料市场以半固体为主,主要参与者包括应用材料公司、Entegris 公司、Ebara 公司、Lapmaster Wolters GmbH 和杜邦。该市场的参与企业正在采取合作和收购等策略来加强其产品供应并获得可持续的竞争优势。

- 2024 年 5 月:杜邦宣布一项策略性倡议,将公司拆分为三个营业单位,并将每个实体公开上市。该计划将把电子和水资源部门在免税的基础上分离,新成立的「新杜邦」将成为多元化的工业参与企业。分离后,电子和水资源部门将作为独立营业单位运作,使每个部门更加专注和灵活。杜邦预计这三家公司都将拥有强劲的资产负债表、有吸引力的财务状况和良好的成长前景。该公司计划在未来 18 至 24 个月内完成这些分离工作。

- 2023 年 12 月:Entegris Inc. 在京畿道安山汉阳大学 ERICA 校区开设了韩国技术中心。该中心旨在将 Entegris 的多种能力集中到一起。该中心的策略定位是促进与涉及先进逻辑、DRAM、3D NAND半导体和其他技术的客户进行更深入的合作。具体来说,该中心将成为薄膜沉积、化学机械平坦化(CMP)和先进湿蚀刻製程的知识中心。也将安装先进的分析工具,以增强 Entegris 为韩国客户提供服务的能力。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 消费者议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 技术简介

第五章市场动态

- 市场驱动因素

- 半导体小型化需求日益增长

- Mems 和 Nems 的应用成长推动 CMP 市场成长

- 市场问题

- 製造复杂性

第六章市场区隔

- 按类型

- CMP设备

- CMP耗材

- 泥

- 垫片

- 垫片调理剂

- 其他的

- 按应用

- 复合半导体

- 积体电路

- 微机电系统与奈米机电系统

- 其他的

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

第七章竞争格局

- 公司简介

- Applied Materials Inc.

- Entegris Inc.

- Ebara Corporation

- Lapmaster Wolters Gmbh

- Dupont De Nemours Inc.

- Fujimi Incorporated

- Revasum Inc.

- Resonac Holdings Corporation(Showa Denko Materials)

- Okamoto Corporation

- Fujifilm Corporation(Fujifilm Holdings Corporation)

- Tokyo Seimitsu Co. Ltd(Accretech Create Corp.)

第八章投资分析

第九章 市场机会与未来趋势

The Chemical Mechanical Planarization Slurry Market size is estimated at USD 6.53 billion in 2025, and is expected to reach USD 9.26 billion by 2030, at a CAGR of 7.23% during the forecast period (2025-2030).

Key Highlights

- The CMP market is expected to grow steadily during the forecast period due to technological advancements in fabrication and semiconductor processes to enhance the performance of semiconductor products. Manufacturers' increasing investment in semiconductor wafer fabrication materials for product innovation drives the market's growth.

- Chemical mechanical polishing or planarization (CMP) flattens rough surfaces and offers numerous benefits in semiconductor manufacturing. It enables manufacturers to achieve uniform flatness across the entire wafer in a single operation. CMP is versatile and capable of planarizing various materials, from metals to oxide films, often handling multiple materials simultaneously.

- CMP solutions play a vital role in achieving higher yields by ensuring uniform planarization and reducing defects on the wafer surface. Developing cost-effective CMP slurries also helps manufacturers optimize their production processes, significantly saving costs. CMP is utilized in optics, photonics, data storage, and medical devices. This expansion of CMP applications creates new market opportunities for CMP solutions manufacturers, further driving the market's growth.

- The stringent requirements of precise process control and defect reduction in various CMP processes affected device performance, yield, and challenges in high-volume manufacturing. Additionally, the complexity of polished materials drives the innovation of CMP consumables. The quality control of new consumables grows, impacting the process window and production line and lowering the manufacturing of CMP equipment and consumables worldwide.

- Post-pandemic, the demand for IC has surged due to increased automotive, consumer electronics, and healthcare sales. For instance, according to WSTS, the global IC market reached around USD 487 billion in revenue in 2024.

Chemical Mechanical Planarization (CMP) Slurry Market Trends

Integrated Circuits Occupied the Largest Market Share During the Forecast Period

- The increasing demand for electronic devices and the high functionalities required in them, in line with the growth of miniaturized electronic devices, are fueling the demand for highly dense embedded ICs and VLSIs in the market, which would create a growth opportunity for CMP devices and consumables. Chemical mechanical polishing (CMP) is a pivotal process in the semiconductor industry. It effectively eliminates surface materials by combining chemical reactions with mechanical forces, making the need for the CMP process instrumental in producing integrated circuits and memory disks.

- Additionally, the emergence of very large-scale integration (VLSI) involves embedding hundreds of thousands of transistors onto a single silicon semiconductor microchip. This process leads to heightened miniaturization, enhanced performance, and improved functionality. However, the challenge lies in fitting more components into a limited space, fueling a lesser margin of error. It raises the need to ensure the total removal of debris from mounting surfaces, supporting the importance of chemical mechanical polishing in IC manufacturing. It would help the market grow in line with the development of IC manufacturing worldwide.

- Countries such as the United States, Taiwan, Korea, and China, among others, are some of the major producers of semiconductor chips. They also contribute significantly to the market's growth in terms of consumption and investments. CMP has become a standard manufacturing process semiconductor manufacturers use to fabricate integrated circuits (IC). The growing adoption of various components in markets like IoT, automotive, and 5G is expected to drive the demand for CMP equipment over the forecast period.

- The market has been registering a significant development supported by the investment activities by the semiconductor manufacturer, government, and other international agencies to strengthen the semiconductor ecosystems worldwide by minimizing the dependency of limited countries for the semiconductor supply chain, which would fuel the demand for the CMP market due to the applications of polishing process in the manufacturing of ICs worldwide.

- For instance, in April 2024, Malaysia planned to build the most extensive integrated circuit design park in Southeast Asia to promote domestic semiconductor design, prototyping, and manufacturing. The Malaysian government would offer several incentives, including tax breaks, office space subsidies, and visa exemption fees, to attract tech companies and investors to the facility, supporting the IC manufacturing ecosystem in the country and creating a growth opportunity for the CMP market.

- The chemical component in the CMP process allows for the targeted removal of specific materials. Compared to purely mechanical polishing, CMP minimizes surface defects and enables the lithography steps to be applied in IC manufacturing, which shows the demand for CMP equipment and consumables in the market.

- The growing semiconductor sales globally over the years are expected to drive the demand for the CMP market. According to SIA, in January 2024, global semiconductor sales reached USD 47.63 billion, marking an increase of over USD 6 billion from the previous year's for the same month.

Asia-Pacific to Register Major Growth

- The Asia-Pacific region holds a significant number of global semiconductor manufacturing facilities, with major players like TSMC and Samsung Electronics. Taiwan is the leading country globally for foundries and plays a crucial role in the semiconductor value chain. Supported by government initiatives, the semiconductor industry in the region is experiencing significant growth, driving market expansion.

- The growing semiconductor sales across the APAC region over the years are expected to drive the demand for the CMP market. According to WSTS, the region's semiconductor sales are expected to significantly increase in 2024 and 2025. In 2023, the region reported a revenue of USD 289.99 billion in sales, which is expected to increase to USD 340.87 billion in 2024 and USD 382.96 billion in 2025. WSTS reports that a significant increase, such as 17.5% YoY growth in 2024 and 12.3% YoY in 2025, is expected due to the growing demand for integrated circuits, discrete and other semiconductors. Such developments are expected to drive the demand for the CMP market.

- Countries like South Korea are significantly driving the demand for CMP technology due to its extensive growth in the semiconductor business with the presence of significant companies like Samsung, SK Hynix, and others. The South Korean government unveiled its strategy in January 2024 to dedicate around USD 470 billion towards establishing the world's largest semiconductor cluster. This ambitious project is set to unfold over the next 23 years and will entail the construction of a substantial production complex in Gyeonggi Province in partnership with SK Hynix. With the growing investments by companies like SK Hynix, the demand for the CMP market is expected to rise.

- In March 2024, Dongjin Semichem initiated the provision of a chemical mechanical polishing (CMP) slurry to SK Hynix for the production of high bandwidth memory (HBM). This slurry plays a crucial role in the CMP process during wafer fabrication by smoothing out the surface. Specifically, oxide slurry is utilized to flatten insulating layers, while metal slurry is employed to flatten metal circuits. This agreement marks the end of Soulbrain's monopoly on the material for HBM production in South Korea. Such developments are expected to drive the market's growth in the coming years.

- Moreover, due to its extensive semiconductor manufacturing capabilities, the market is also expected to witness significant growth in the Chinese region. China stands as a major player in the semiconductor production market, boasting the presence of numerous fabs in the area. As reported by WSTS, semiconductor sales in China hit USD 14.76 billion in January 2024. This figure marks a notable rise from January 2023, when sales in China amounted to USD 11.66 billion. With the growing geopolitical tensions, such as the US-China war, the region is investing significantly in boosting its domestic production.

Chemical Mechanical Planarization (CMP) Slurry Industry Overview

The chemical mechanical planarization market is semi-consolidated with the presence of major players like Applied Materials Inc., Entegris Inc., Ebara Corporation, Lapmaster Wolters GmbH, and Dupont De Nemours Inc. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- May 2024: DuPont unveiled a strategic initiative to divide itself into three separate entities, each to be publicly traded. The plan entails executing tax-free separations of its Electronics and Water divisions, with the newly formed 'New DuPont' emerging as a diversified industrial player. Post separation, electronics, and water will operate as independent entities, poised to leverage enhanced focus and agility within their sectors. DuPont anticipates that all three companies will boast robust balance sheets, enticing financial standings, and promising growth prospects. The company aims to finalize these separations within the next 18 to 24 months.

- December 2023:- Entegris Inc. unveiled its Korea Technology Center at the Hanyang University ERICA campus in Ansan-si, Gyeonggi-do. The center, designed as a focal point, aims to streamline Entegris' diverse capabilities under one roof. This setup is strategically positioned to foster deeper collaboration with clients involved in technologies like advanced logic, DRAM, and 3D NAND semiconductors. Specifically, the center will serve as a knowledge hub for deposition, chemical mechanical planarization (CMP), and advanced wet etch processes. It will also house sophisticated analytical tools, bolstering Entegris' ability to cater to its Korean clientele.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Technology Snapshot

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Need for Miniaturization of Semiconductors

- 5.1.2 Increasing use of Mems and Nems is Fueling the Growth of the CMP Market

- 5.2 Market Challenges

- 5.2.1 Complexity Regarding Manufacturing

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 CMP Equipment

- 6.1.2 CMP Consumable

- 6.1.2.1 Slurry

- 6.1.2.2 Pad

- 6.1.2.3 Pad Conditioner

- 6.1.2.4 Other Consumable Types

- 6.2 By Application

- 6.2.1 Compound Semiconductors

- 6.2.2 Integrated Circuits

- 6.2.3 Mems and Nems

- 6.2.4 Other Applications

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Applied Materials Inc.

- 7.1.2 Entegris Inc.

- 7.1.3 Ebara Corporation

- 7.1.4 Lapmaster Wolters Gmbh

- 7.1.5 Dupont De Nemours Inc.

- 7.1.6 Fujimi Incorporated

- 7.1.7 Revasum Inc.

- 7.1.8 Resonac Holdings Corporation (Showa Denko Materials)

- 7.1.9 Okamoto Corporation

- 7.1.10 Fujifilm Corporation (Fujifilm Holdings Corporation)

- 7.1.11 Tokyo Seimitsu Co. Ltd (Accretech Create Corp.)

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

半导体用CMP材料市场:按类型、应用、通路和最终用户划分-2026年至2032年全球预测晶圆CMP材料市场按产品类型、晶圆尺寸、颗粒尺寸、应用和最终用途产业划分-2026-2032年全球预测

半导体用CMP材料市场:按类型、应用、通路和最终用户划分-2026年至2032年全球预测晶圆CMP材料市场按产品类型、晶圆尺寸、颗粒尺寸、应用和最终用途产业划分-2026-2032年全球预测 湿式工作台市场:按类型、应用和地区划分

湿式工作台市场:按类型、应用和地区划分 2025年化学机械抛光(CMP)浆料和垫片全球市场报告

2025年化学机械抛光(CMP)浆料和垫片全球市场报告 机械式和电子式引信:全球市场份额和排名、总销售额和需求预测(2025-2031 年)化学机械平坦化市场按组件、晶圆尺寸和应用划分 - 全球预测 2025-2032

机械式和电子式引信:全球市场份额和排名、总销售额和需求预测(2025-2031 年)化学机械平坦化市场按组件、晶圆尺寸和应用划分 - 全球预测 2025-2032 全球半导体晶圆 CMP 固定环市场 - 市场份额和排名、总收入和需求预测(2025-2031 年)2025年化学机械平坦化全球市场报告

全球半导体晶圆 CMP 固定环市场 - 市场份额和排名、总收入和需求预测(2025-2031 年)2025年化学机械平坦化全球市场报告 半导体 CMP 材料市场(按产品类型、按应用、按最终用户、按国家和地区)-2025 年至 2032 年全球产业分析、市场规模、市场份额及预测

半导体 CMP 材料市场(按产品类型、按应用、按最终用户、按国家和地区)-2025 年至 2032 年全球产业分析、市场规模、市场份额及预测 全球牙齿维持器市场:市场规模、份额和趋势分析(2025-2031 年)

全球牙齿维持器市场:市场规模、份额和趋势分析(2025-2031 年)