|

市场调查报告书

商品编码

1689768

丁腈橡胶 (NBR):市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Nitrile Butadiene Rubber (NBR) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

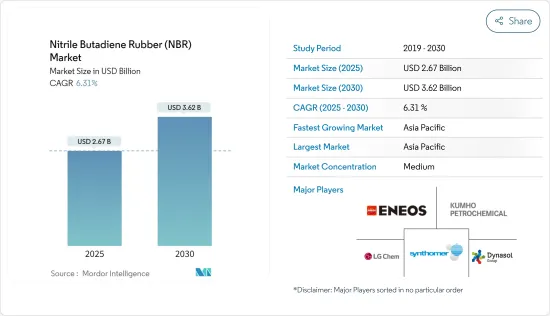

预计 2025 年丁腈橡胶 (NBR) 市场规模为 26.7 亿美元,到 2030 年将达到 36.2 亿美元,预测期内(2025-2030 年)的复合年增长率为 6.31%。

COVID-19 阻碍了丁腈橡胶市场的发展。疫情扰乱了全球供应链,影响了 NBR 製造商的原材料供应、物流和製造业务。然而,疫情过后人们对卫生和安全的持续关注,导致对 NBR 手套和其他医疗相关应用的需求持续存在。

主要亮点

- 预计推动丁腈橡胶 (NBR) 市场发展的因素包括汽车工业以及新兴市场的工业和基础设施发展计划对丁腈橡胶的需求增加。

- 然而,替代材料的可用性和原材料价格的波动预计会阻碍丁腈橡胶市场的成长。

- 可再生能源领域以及医疗保健及医疗设备对丁腈橡胶的需求不断增加,预计将在未来几年为市场参与者提供各种机会。

- 亚太地区在全球丁腈橡胶市场占据主导地位,其中消费量最高的国家是中国、印度和东南亚国协。

丁腈橡胶(NBR)市场趋势

汽车和运输业占据市场主导地位

- NBR 广泛用于製造汽车软管和管材,例如燃油管、散热器软管、煞车软管等。 NBR 对石油基流体、劣化和臭氧的耐受性使其非常适合这些要求苛刻的应用。

- NBR的高拉伸强度和耐磨性使其成为运输业使用的正时带、风扇带和输送机等汽车皮带的理想材料。

- NBR 出色的耐用性和耐化学性使其成为工业车辆、重型卡车和施工机械中的密封件、垫圈和其他部件的热门选择。

- 根据国际汽车工业组织(OICA)发布的最新预测,2023年全球汽车产量将达到93,546,599辆,较2021年成长17%。

- 根据国际能源总署(IEA)发布的估计,美国电动车销量将从2022年的100万辆增加到2023年的160万辆。

- 此外,根据国际能源总署发布的估计,欧洲电动车销量将从2022年的270万辆增加到2023年的340万辆。

- 根据印度品牌股权基金会(IBEF)的估计,印度民航业在过去三年中已成为该国成长最快的产业之一。预计 2023 年印度航空运输量将达到 3.2728 亿架飞机,而 2022 年则为 1.8889 亿架。

- 预测期内,丁腈橡胶 (NBR) 的需求预计会受到所有这些因素的影响。

亚太地区占市场主导地位

- 亚太地区是中国、日本、韩国和印度等主要汽车製造地的所在地。这些国家的汽车工业蓬勃发展,推动了对 NBR 的需求,NBR 广泛应用于密封件、垫圈、软管、皮带等各种汽车零件。

- 根据国际汽车工业组织(OICA)发布的资料,到2023年,中国汽车产量将达到30,160,966辆,高于2022年的27,020,615辆。

- 中国、印度和东南亚等国家的快速都市化和基础设施发展计划正在增加对施工机械、重型车辆和运输系统的需求。 NBR 广泛用于製造这些行业的零件,促进了市场的成长。

- 根据印度品牌股权基金会(IBEF)发布的估计,印度在基础建设方面的投资已使其成为价值26兆美元的经济体。印度政府已推出国家基础设施管道(NIP)计划,以促进基础设施产业的发展。

- 亚太地区,特别是中国、日本和韩国,拥有几家主要的 NBR 製造商和生产设施。该成熟的製造地确保了 NBR 的可靠供应,以满足该地区日益增长的需求。

- 所有这些因素,再加上亚太地区其他新兴经济体的消费不断增长,正在推动该地区的市场成长。

丁腈橡胶(NBR)产业概况

丁腈橡胶(NBR)市场部分整合。主要参与者包括锦湖石油化学、Synthomer PLC、LG Chem、ENEOS Materials Corporation 和 Dynasol Group。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 不断扩张的汽车产业

- 工业和基础设施发展计划

- 限制因素

- 替代材料的可用性

- 原物料价格波动

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场区隔

- 应用

- 黏合剂和密封剂

- 皮带和电缆

- 手套

- 软管

- 垫圈和 O 型环

- 其他用途(消费品)

- 最终用户产业

- 汽车与运输

- 建筑和施工

- 工业

- 医疗

- 其他终端用户产业(石油和天然气、航太)

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 越南

- 印尼

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 西班牙

- 土耳其

- 俄罗斯

- 北欧的

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 埃及

- 卡达

- 阿拉伯聯合大公国

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- Apcotex

- ARLANXEO

- China Petrochemical Corporation(Sinopec)

- Dynasol Group

- ENEOS Materials Corporation

- KUMHO PETROCHEMICAL

- Lanxess

- LG Chem

- SIBUR

- Synthomer PLC

- Synthos

- TSRC

- Versalis SpA

- ZEON CORPORATION

第七章 市场机会与未来趋势

- 可再生能源领域的需求不断增长

- 医疗保健和医疗设备需求增加

The Nitrile Butadiene Rubber Market size is estimated at USD 2.67 billion in 2025, and is expected to reach USD 3.62 billion by 2030, at a CAGR of 6.31% during the forecast period (2025-2030).

COVID-19 hampered the nitrile butadiene rubber market. The pandemic disrupted the global supply chains, impacting the availability of raw materials, logistics, and manufacturing operations for NBR producers. However, the continued focus on hygiene and safety post-pandemic led to sustained demand for NBR gloves and other medical-related applications.

Key Highlights

- The increasing demand for nitrile butadiene rubber from the expanding automotive industry and from the industrial and infrastructure development projects are factors that are expected to drive the nitrile butadiene rubber market.

- However, the availability of substitute materials and fluctuating raw material prices are expected to hinder the growth of nitrile butadiene rubber market.

- The increasing demand for nitrile butadiene rubber from renewable energy sector and healthcare and medical devices are expected to provide various opportunities to the market players in the upcoming peroiod.

- The Asia-Pacific region dominates the nitrile butadiene rubber market globally, with the largest consumption from countries such as China, India, and ASEAN Countries.

Nitrile Butadiene Rubber (NBR) Market Trends

Automotive and Transportation Sector Dominates the Market

- NBR is extensively used in the manufacturing of hoses and tubing for automotive applications, including fuel lines, radiator hoses, and brake hoses. Its resistance to petroleum-based fluids, aging, and ozone makes it suitable for these demanding applications.

- NBR's high tensile strength and resistance to abrasion make it an ideal material for automotive belts, such as timing belts, fan belts, and conveyor belts used in the transportation industry.

- The exceptional durability and chemical resistance of NBR makes it a preferred choice for seals, gaskets, and other components in industrial vehicles, heavy-duty trucks, and construction equipment.

- According to the latest estimates published by the International Organization of Motor Vehicle Manufacturers (OICA), in 2023, global production of motor vehicles stood at 93,546,599 units, a 17% increase from that in 2021.

- According to the estimate released by the International Energy Agency (IEA), the sales of electric vehicles increased from 1.0 million units in 2022 to 1.6 million units in 2023 in the United States.

- In addition, the sales of electric vehicles also increased from 2.7 million in 2022 to 3.4 million units in 2023 in Europe, according to the estimate released by the IEA.

- According to an estimate published by the Indian Brand Equity Foundation (IBEF), the civil aviation industry in India has emerged as one of the fastest-growing industries in the country in the last three years. The air traffic movement in India stood at 327.28 million in Financial Year 2023 compared to 188.89 million in 2022.

- The demand for nitrile butadiene rubber (NBR) is anticipated to be affected by all of these factors over the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is home to major automotive manufacturing hubs, including China, Japan, South Korea, and India. The thriving automotive industry in these countries drives the demand for NBR, which is extensively used in various automotive components, including seals, gaskets, hoses, and belts.

- According to the data released by the International Organization of Motor Vehicle Manufacturers (OICA), in China, 30,160,966 units of vehicles were produced in 2023, which increased from 27,020615 units in 2022.

- Rapid urbanization and infrastructure development projects in countries like China, India, and Southeast Asian nations have led to an increase in the need for construction equipment, heavy-duty vehicles, and transportation systems. NBR is widely used in the manufacturing of components for these industries, contributing to its market growth.

- According to the estimate released by the Indian Brand Equity Foundation (IBEF), the investment in infrastructure development in India has helped India become an economy of USD 26 trillion. The government of India has launched the National Infrastructure Pipeline (NIP) to augment the growth of the infrastructure sector.

- Several major NBR manufacturers and production facilities are located in the Asia-Pacific region, particularly in countries like China, Japan, and South Korea. This established manufacturing base ensures a reliable supply of NBR to meet the region's growing demand.

- All such factors, coupled with the increasing consumption from other emerging economies of the Asia-Pacific region, are driving the market's growth in the region.

Nitrile Butadiene Rubber (NBR) Industry Overview

The nitrile butadiene rubber market is partially consolidated. Some of the major players include KUMHO PETROCHEMICAL, Synthomer PLC, LG Chem, ENEOS Materials Corporation, and Dynasol Group, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Expanding Automotive Industry

- 4.1.2 Industrial and Infrastructure Development Projects

- 4.2 Restraints

- 4.2.1 Availability of Substitute Materials

- 4.2.2 Fluctuating Raw Material Prices

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Application

- 5.1.1 Adhesives and Sealants

- 5.1.2 Belts and Cables

- 5.1.3 Gloves

- 5.1.4 Hoses

- 5.1.5 Gaskets and O-Rings

- 5.1.6 Other Applications (Consumer Goods)

- 5.2 End-user Industry

- 5.2.1 Automotive and Transportation

- 5.2.2 Building and Construction

- 5.2.3 Industrial

- 5.2.4 Medical

- 5.2.5 Other End-user Industries (Oil and Gas, Aerospace)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Vietnam

- 5.3.1.8 Indonesia

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 Turkey

- 5.3.3.7 Russia

- 5.3.3.8 NORDIC

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Egypt

- 5.3.5.5 Qatar

- 5.3.5.6 UAE

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Apcotex

- 6.4.2 ARLANXEO

- 6.4.3 China Petrochemical Corporation (Sinopec)

- 6.4.4 Dynasol Group

- 6.4.5 ENEOS Materials Corporation

- 6.4.6 KUMHO PETROCHEMICAL

- 6.4.7 Lanxess

- 6.4.8 LG Chem

- 6.4.9 SIBUR

- 6.4.10 Synthomer PLC

- 6.4.11 Synthos

- 6.4.12 TSRC

- 6.4.13 Versalis S.p.A.

- 6.4.14 ZEON CORPORATION

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand from Renewable Energy Sector

- 7.2 Increasing Demand from Healthcare and Medical Devices

丁腈橡胶粉市场分析及预测(至2035年):类型、产品类型、应用、形态、材料类型、製程、最终用户、技术、功能

丁腈橡胶粉市场分析及预测(至2035年):类型、产品类型、应用、形态、材料类型、製程、最终用户、技术、功能 全球快速硫化丁腈橡胶市场规模、份额、趋势和成长分析报告(2026-2034)

全球快速硫化丁腈橡胶市场规模、份额、趋势和成长分析报告(2026-2034) 丙烯腈丁二烯乳胶市场按应用、终端用户产业、类型、等级、形态和销售管道-2026-2032年全球预测

丙烯腈丁二烯乳胶市场按应用、终端用户产业、类型、等级、形态和销售管道-2026-2032年全球预测 丁腈橡胶市场规模、份额及成长分析(按产品类型、终端用户产业及地区划分)-2026-2033年产业预测丁腈橡胶市场按等级、聚合方法、形态、分销管道和应用划分-2025-2032年全球预测

丁腈橡胶市场规模、份额及成长分析(按产品类型、终端用户产业及地区划分)-2026-2033年产业预测丁腈橡胶市场按等级、聚合方法、形态、分销管道和应用划分-2025-2032年全球预测 全球丁腈橡胶乳胶市场全球丁腈橡胶粉红市场全球特种丁腈橡胶市场全球快速固化丁腈橡胶市场全球氢化丁腈橡胶市场

全球丁腈橡胶乳胶市场全球丁腈橡胶粉红市场全球特种丁腈橡胶市场全球快速固化丁腈橡胶市场全球氢化丁腈橡胶市场