|

市场调查报告书

商品编码

1689788

核能发电-市场占有率分析、产业趋势与统计、成长预测(2025-2030)Nuclear Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

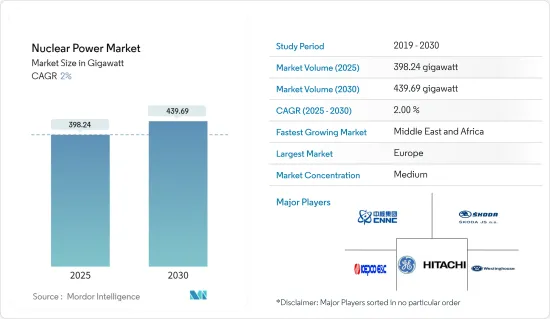

预计 2025 年核能发电市场规模为 398.24 吉瓦,到 2030 年将达到 439.69 吉瓦,预测期内(2025-2030 年)的复合年增长率为 2%。

关键亮点

- 从中期来看,市场成长受到核能发电的可能性的推动,因为与石化燃料相比,核能发电产生的二氧化碳排放较少。

- 然而,建立核能发电厂的高初始成本以及可再生能源等替代能源的可用性可能会在预测期内抑制市场成长。

- 世界各国都在进行第四代核能技术研发,推动安全、技术、经济、先进的小型模组核子反应炉。因此,未来市场可能会提供多种商业机会。

- 由于中国和印度的核能份额庞大,预计预测期内亚太地区的核能发电市场将显着成长。

核能发电市场趋势

能源领域预计将主导市场

- 核能以质子和中子的形式从原子核或原子核中释放出来。核能是由核分裂(原子核分裂成几个独立的部分)或核融合(原子核的聚变)所产生的。当今世界,核分裂产生电能,核融合技术正处于研发阶段,以产生电能。截至 2022 年,全球核能发电发电量约为 2,679 TWh,而 2021 年约为 2,802 TWh。

- 核能发电厂能够长时间连续运行,提供稳定的电力供应。这对于满足已开发国家和开发中国家日益增长的能源需求至关重要。

- 此外,这一能源领域为全球减缓气候变迁的努力做出了重大贡献。核能发电在运作过程中几乎不排放温室气体,是减少二氧化碳和其他有害空气污染物的重要工具。

- 根据2022年世界能源统计评论,核能总发电量与2021年相比下降了近4.4%,但2013年至2022年的年增长率约为1%。

- 此外,即将开工的核能发电厂计划预计将在预测期内增加发电能力。例如,2023年4月,据印度核能部称,印度政府授予在印度五个不同邦建立10座核子反应炉的许可证和财政核准。

- 这些核子反应炉每座容量为 700 兆瓦,是以舰队形式建造的本土加压重水反应器。将建造这些核子反应炉的邦包括卡纳塔克邦、哈里亚纳邦、中央邦和拉贾斯坦邦。

- 此外,印度已进入三阶段核能计画的第二阶段。 2024 年 3 月,印度首批自主建造的快滋生式反应炉(500 Mwe)之一在清奈约 70 公里的卡尔帕卡姆开始运作。

- 因此,鑑于上述情况,预计能源部门将在预测期内主导核能发电市场。

亚太地区预计将经历强劲成长

- 与北美和欧洲多年来核能发电装置容量成长受限不同,亚太地区的一些国家正在规划和建造新的核能发电厂,以满足日益增长的绿能需求。

- 例如,中国正致力于创新主导成长、低碳发展、城乡一体化、深化社会包容和人口老化。 「十四五」规划强调高品质绿色发展,高度重视创新作为现代化发展的基础。在第一个「十三五」成果的基础上,我们计画降低经济体的碳强度,在2030年实现二氧化碳排放达到高峰。

- 此外,根据2021年3月发布的《第十四个五年规划(2021-2025年)》草案,政府计划在2025年底将核能发电容量提高到7,000万千瓦。

- 此外,中国国家能源局(NEA)正在考虑在未来十年提高国家清洁能源计画的目标。国家能源局提案,到2030年,中国40%的电力应来自核能和可再生,目标是2030年核能发电装置容量达到120-150吉瓦。

- 印度政府致力于扩大核能发电能力,以满足该国日益增长的电力需求。印度政府预计,到2031年,该国核能发电量将达到约2,250万千瓦。

- 根据印度中央电力局(CEA)预测,2024年1月,印度核能发电厂将达到748万千瓦,包括23座核子反应炉和7座在建核子反应炉,总合装置容量为5398万千瓦。

- 根据永续能源政策研究所 (ISEP) 的数据,核能发电量在 2014 年最初降至零,但此后有所回升,占 2019 年发电量的 6.5%。然而,2020 年这一比例下降到 4.3%,然后在 2021 年上升到 5.9%,然后在 2022 年再次下降到 4.8%。

- 因此,由于上述因素,预计亚太地区在预测期内将出现显着的市场成长。

核能发电业概况

核能发电市场是半静态的。市场的主要企业(不分先后顺序)包括通用电气日立核能公司、西屋电气公司、韩国电力工程建设公司、斯柯达 JS AS 和中国核工业集团公司。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究范围

- 市场定义

- 调查前提

第二章执行摘要

第三章调查方法

第四章 市场概述

- 介绍

- 装置容量及2029年预测

- 近期趋势和发展

- 政府法规和政策

- 市场动态

- 驱动程式

- 清洁能源需求不断成长

- 有利措施延长植物寿命

- 限制因素

- 来自可再生能源的激烈竞争

- 事故和成本效益的不确定性

- 驱动程式

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章市场区隔

- 按用途(定性分析)

- 活力

- 防御

- 其他的

- 核子反应炉类型

- 压水式反应炉/加压重水核子反应炉

- 沸水式反应炉

- 高温反应炉

- 液态金属快滋生反应器

- 其他核子反应炉

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 英国

- 俄罗斯

- 法国

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 伊朗

- 其他中东和非洲地区

- 北美洲

第六章 竞争格局

- 合併、收购、合资、合作和协议

- 主要企业策略

- 公司简介

- Electricite de France SA(EDF)

- GE-Hitachi Nuclear Energy Inc.

- Westinghouse Electric Company LLC

- Duke Energy Corporation

- SKODA JS AS

- China National Nuclear Corporation

- Bilfinger SE

- BWX Technologies Inc.

- Doosan Enerbility Co. Ltd

- Mitsubishi Heavy Industries Ltd

- Bechtel Group Inc.

- Japan Atomic Power Company

- Rosatom State Atomic Energy Corporation

- KEPCO Engineering & Construction

- 市场排名/份额(%)分析

第七章 市场机会与未来趋势

- 先进小型模组化反应堆

简介目录

Product Code: 68252

The Nuclear Power Market size is estimated at 398.24 gigawatt in 2025, and is expected to reach 439.69 gigawatt by 2030, at a CAGR of 2% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the ability of nuclear energy to generate electricity with lower carbon emissions compared to fossil fuels have been driving the market's growth over the medium term.

- On the other hand, the high initial cost of setting up a nuclear power plant and the availability of alternative power generation sources, such as renewable energy, is likely to restrain the market's growth during the forecast period.

- Nevertheless, nations worldwide are researching and developing generation IV nuclear energy technologies to promote safety, technical, economic, and advanced small modular reactors. This, in turn, is likely to create several future opportunities for the market.

- Asia-Pacific is expected to witness significant growth in the nuclear power market during the forecast period, owing to its substantial share of nuclear energy in China and India.

Nuclear Power Market Trends

Energy Segment Expected to Dominate the Market

- Nuclear energy is released from the nucleus or the core of an atom of protons and neutrons. Nuclear energy can be produced either in nuclear fission (when the nuclei of atoms split into several parts) or by fusion (when nuclei fuse). In today's world, nuclear fission produces electricity, while nuclear fusion technology produces power in the research and development (R&D) phase. As of 2022, the global nuclear power generation was about 2,679 TWh compared to around 2,802 TWh in 2021.

- Nuclear power plants can operate continuously for extended periods, providing a consistent supply of electricity, which is crucial in meeting the increasing energy demands of industrialized and developing nations.

- Furthermore, the energy segment contributes significantly to global efforts to mitigate climate change. Nuclear power generates virtually no greenhouse gas emissions during operation, making it a vital tool for reducing carbon dioxide and other harmful atmospheric pollutants.

- According to the Statistical Review of World Energy in 2022, the total electricity generated through nuclear energy was down by almost 4.4% compared to 2021 but recorded an annual growth rate of almost 1% between 2013 and 2022.

- Moreover, with the upcoming nuclear energy power plant projects, the generation capacity is expected to increase during the forecast period. For instance, in April 2023, according to the Atomic Energy Ministry, the Indian government granted authorization and financial approval for establishing ten nuclear reactors in five different states throughout India.

- With a capacity of 700 MW each, these reactors will be indigenous pressurized heavy water reactors constructed in fleet mode. The states where these reactors are scheduled to be set up include Karnataka, Haryana, Madhya Pradesh, and Rajasthan.

- Moreover, India entered the second stage of the country's three-stage nuclear program. In March 2024, the country commenced one of its first indigenous fast-breeder reactors (500 Mwe) in Kalpakkam, around 70 km from Chennai.

- Therefore, the energy segment is expected to dominate the nuclear power market during the forecast period due to the abovementioned points.

Asia-Pacific Expected to Witness Significant Growth

- In contrast to North America and Europe, where growth in nuclear electricity generating capacity has been limited for many years, several countries in Asia-Pacific are planning and building new nuclear power plants to meet their increasing demand for clean electricity.

- For instance, China focuses on innovation-driven growth, low-carbon development, integrating urban and rural areas with deeper social inclusion, and population aging. The 14th Five-Year Plan highlights high-quality green development, emphasizing innovation as the basis for modern development. By capitalizing on the accomplishments of the 13th Plan, the country intends to reduce the economy's carbon intensity and peak carbon dioxide emissions by 2030.

- Further, according to a draft of the 14th Five-Year Plan (2021-2025) released in March 2021, the government intends to reach 70 GW of nuclear capacity by the end of 2025.

- Furthermore, China's National Energy Administration (NEA) is examining the possibility of increasing the ambition of the country's clean energy programs this decade. The NEA proposes that China obtain 40% of its electricity from nuclear and renewable sources by 2030 and set its nuclear capacity target to 120-150 GW by 2030.

- The Indian government is dedicated to growing its nuclear power generation capacity to meet the increasing electricity demand in the country. According to the Indian government, the country's nuclear capacity is expected to reach about 22.5 GW by 2031.

- As per the Central Electricity Authority (CEA), India had 7.48 GW of nuclear power plants in India till January 2024, with 23 nuclear reactors and seven reactors with a combined capacity of 5,398 MWe under the construction stage.

- According to the Institute for Sustainable Energy Policies (ISEP), electricity generation initially dropped to zero for nuclear power in 2014 but witnessed a resurgence, accounting for 6.5% of electricity generation in 2019. However, it decreased to 4.3% in 2020, increased to 5.9% in 2021, and then declined again to 4.8% in 2022.

- Therefore, owing to the above factors, Asia-Pacific is expected to witness significant market growth during the forecast period.

Nuclear Power Industry Overview

The nuclear power market is semi-consolidated. Some of the major players in the market (in no particular order) include GE-Hitachi Nuclear Energy Inc., Westinghouse Electric Company LLC, KEPCO Engineering & Construction, SKODA JS AS, and China National Nuclear Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Installed Capacity and Forecast, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increase in Demand for Clean Energy

- 4.5.1.2 Plant Lifetime Extensions With Favorable Policies

- 4.5.2 Restraints

- 4.5.2.1 Intense Competition From Renewable Energy Sources

- 4.5.2.2 Accidents and Uncertainty over the Cost Effectiveness

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Application (Qualitative Analysis)

- 5.1.1 Energy

- 5.1.2 Defense

- 5.1.3 Other Applications

- 5.2 By Reactor Type

- 5.2.1 Pressurized Water Reactor and Pressurized Heavy Water Reactor

- 5.2.2 Boiling Water Reactor

- 5.2.3 High-temperature Gas-cooled Reactor

- 5.2.4 Liquid-metal Fast-breeder Reactor

- 5.2.5 Other Reactor Types

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 Russia

- 5.3.2.4 France

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 South Africa

- 5.3.5.4 Iran

- 5.3.5.5 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Electricite de France SA (EDF)

- 6.3.2 GE-Hitachi Nuclear Energy Inc.

- 6.3.3 Westinghouse Electric Company LLC

- 6.3.4 Duke Energy Corporation

- 6.3.5 SKODA JS AS

- 6.3.6 China National Nuclear Corporation

- 6.3.7 Bilfinger SE

- 6.3.8 BWX Technologies Inc.

- 6.3.9 Doosan Enerbility Co. Ltd

- 6.3.10 Mitsubishi Heavy Industries Ltd

- 6.3.11 Bechtel Group Inc.

- 6.3.12 Japan Atomic Power Company

- 6.3.13 Rosatom State Atomic Energy Corporation

- 6.3.14 KEPCO Engineering & Construction

- 6.4 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advanced Small Modular Reactors

02-2729-4219

+886-2-2729-4219

全球先进核子技术市场(2026-2045)

全球先进核子技术市场(2026-2045) 2032年先进核能市场预测:按核子反应炉类型、燃料类型、技术、应用、最终用户和地区分類的全球分析

2032年先进核能市场预测:按核子反应炉类型、燃料类型、技术、应用、最终用户和地区分類的全球分析 2025年全球核能发电市场报告

2025年全球核能发电市场报告 全球核能市场

全球核能市场 核能发电感测器市场 - 预测 2025-20302025年核能营运、燃料和仪器全球市场报告

核能发电感测器市场 - 预测 2025-20302025年核能营运、燃料和仪器全球市场报告 核电市场-全球产业规模、份额、趋势、机会及预测(细分、按应用、按反应器类型、按地区、按竞争,2020-2030 年)

核电市场-全球产业规模、份额、趋势、机会及预测(细分、按应用、按反应器类型、按地区、按竞争,2020-2030 年) 按核子反应炉类型、应用和地区分類的核能发电市场

按核子反应炉类型、应用和地区分類的核能发电市场 核能市场规模、份额和成长分析(按类型、燃料、应用和地区)- 产业预测,2025-2032 年核电厂服务市场 - 全球产业规模、份额、趋势、机会和预测,按电站类型、服务、地区和竞争细分,2019-2029F

核能市场规模、份额和成长分析(按类型、燃料、应用和地区)- 产业预测,2025-2032 年核电厂服务市场 - 全球产业规模、份额、趋势、机会和预测,按电站类型、服务、地区和竞争细分,2019-2029F

▼