|

市场调查报告书

商品编码

1689790

地板胶合剂:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Floor Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

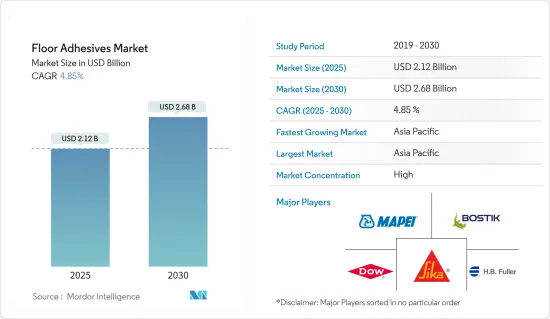

地板胶合剂市场规模预计在 2025 年为 21.2 亿美元,预计到 2030 年将达到 26.8 亿美元,预测期内(2025-2030 年)的复合年增长率为 4.85%。

主要亮点

- 全球建设产业的快速成长以及地板胶合剂的多功能性、安全性和易用性预计将推动市场成长。

- 另一方面,VOC排放对健康的不利影响可能会阻碍市场成长。

- 对生物基地板黏合剂的需求不断增加可能会带来机会。

- 亚太地区占据全球市场主导地位,其中最大的消费国是中国、印度和日本。

地板胶合剂市场趋势

住宅终端用户行业细分市场的需求不断增长

- 瓷砖和石材黏合剂是住宅终端用户行业领域最常用的黏合剂类型。此外,住宅市场是所研究市场中规模最大且成长最快的市场。

- 中产阶级人口的成长加上可支配收入的增加,推动了中产阶级住宅市场的扩大,从而增加了地板胶合剂的使用。

- 根据世界银行的数据,全球建筑业的价值将从 2020 年的 22.36 兆美元增加到 2021 年的 27.18 兆美元。

- 预计最高成长将来自亚太地区,主要受中国和印度住宅建筑市场扩张的推动。预计到2030年,这两个地区将占全球中阶的43.3%以上。印度政府已将住宅的GST税从12%降至5%。这项减税措施可能扩大中阶住宅建设市场。

- 此外,2021 年 10 月,圣保罗州住宅协会 (Secovi-SP) 记录巴西圣保罗住宅销售量为 5,555 套。由于消费者在住宅方面的支出增加,这一数字可能还会增加。此外,巴西独户住宅的趋势可能会支持未来的住宅建设产业的发展。

- 由于联邦住宅补贴大幅削减,以及疫情引发深度经济衰退,墨西哥住宅开工量和库存水准已跌至十年来的最低水准。社会住宅计画(Programa de 住宅 Social)的预算在 2021 年增加了 179%,达到 2 亿美元,以支持建筑支出。此外,便捷的融资设施和优惠的房屋抵押贷款制度预计将有利于该国的住宅建设。

- 经济适用住宅领域一直在稳步增长,这主要归功于政府努力为都市区贫困阶级提供经济适用住宅。

- 与其他类型的住宅相比,廉价住宅建造中地板胶的消费量相对较低。世界各国都为来自其他国家的难民提供庇护。因此,政府为难民提供临时或永久的廉价住宅。

亚太地区占市场主导地位

- 亚太地区占据全球市场占有率。随着中国、印度和东南亚国协等国家的建设活动日益增多,该地区的地板胶合剂消费量也增加。

- 儘管中国政府努力实现经济结构调整,更加重视服务业,但还是推出了大规模建设计画,其中包括为未来十年内2.5亿人迁入新的特大城市做准备。

- 根据中国国家统计局的数据,中国建筑市场规模将从 2020 年的 23.27 兆元(3.34 兆美元)成长至 2021 年的 25.92 兆元(3.72 兆美元)。

- 中国是全球最大的建筑市场,占全球建筑投资的20%。预计到2030年,中国将在建筑上投入约13兆美元。中国正在推动和推动持续都市化进程,目标到2030年都市化率达70%。

- 受政府对基础设施计划兴趣增加以及住宅和商业领域需求预计快速復苏的推动,建筑业预计将在 22 财年增长 10.7%。因此,预计该国建设活动的扩张将增加对地板胶合剂的需求。

- 印度政府实施的各项政策,如智慧城市计划和2022年全民住宅,预计将为低迷的建设产业提供急需的提振。此外,近期的《房地产法》、商品及服务税和房地产投资信託基金等政策改革预计将减少核准延迟并在未来几年加强建筑业。

- 韩国统计局的资料显示,由于国际需求强劲,2021年韩国建筑商赢得的建筑订单增加了两位数。韩国统计局称,2021年国内外建筑公司接到的建筑订单总额达2,459亿美元,比2020年增加了31兆韩元。

地板胶合剂产业概况

全球地板胶合剂市场部分整合。主要参与者包括西卡集团 (Sika AG)、马贝集团 (MAPEI SpA)、阿科玛集团 (Bostik SA)、HB Fuller Company 和陶氏化学 (Dow)。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 快速成长的全球建设产业

- 地板胶合剂用途广泛、安全且使用方便

- 限制因素

- VOC排放对健康的不利影响

- 其他阻碍因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场区隔

- 树脂类型

- 环氧树脂

- 聚氨酯

- 丙烯酸纤维

- 乙烯基塑料

- 其他树脂类型

- 科技

- 水性

- 溶剂型

- 其他技术

- 应用

- 磁砖和石材

- 地毯

- 木头

- 层压板

- 弹性地板

- 其他用途

- 最终用户产业

- 住宅

- 商业

- 工业的

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作、协议

- 市场排名分析

- 主要企业策略

- 公司简介

- 3M

- Arkema Group(Bostik SA)

- Ashland

- Dow

- Forbo Holding AG

- HB Fuller Company

- Henkel AG & Co. KGaA

- Jowat SE

- LATICRETE International Inc.

- MAPEI SpA

- Pidilite Industries Limited

- Sika AG

- Tesa SE

第七章 市场机会与未来趋势

- 生物基地板胶黏剂的需求不断增加

简介目录

Product Code: 68260

The Floor Adhesives Market size is estimated at USD 2.12 billion in 2025, and is expected to reach USD 2.68 billion by 2030, at a CAGR of 4.85% during the forecast period (2025-2030).

Key Highlights

- The rapidly growing global construction industry and the versatility, safety, and ease of application of floor adhesives, are likely to drive market growth.

- On the flip side, hazardous health effects due to VOC emissions may hinder the market's growth.

- Increasing demand for bio-based floor adhesives will likely act as an opportunity.

- Asia-Pacific dominates the global market, with the largest consumption coming from China, India, and Japan.

Floor Adhesives Market Trends

Increasing Demand from Residential End-user Industry Segment

- Tile and stone adhesives are the most commonly used adhesive type in the residential end-user segment. Additionally, the residential segment is the largest and fastest-growing segment in the market studied.

- The rising middle-class population, coupled with the increasing disposable incomes, has facilitated an expansion in the middle-class housing segment, thereby increasing the use of flooring adhesives.

- According to the World Bank, the value of the global construction industry has increased from USD 22.36 trillion in 2020 to USD 27.18 in 2021.

- The highest growth is expected to be registered in the Asia-Pacific region, owing to China and India's expanding housing construction markets. These two regions are expected to represent over 43.3% of the global middle class by 2030. The Government of India reduced the GST taxes for housing from 12% to 5%. This tax redemption may increase the construction market for middle-class housing.

- Furthermore, in October 2021, Sao Paulo State Housing Union (Secovi-SP) recorded 5,555 new residential units sold in Sao Paulo, Brazil. The number is likely to rise, owing to the increase in consumer spending on residential housing units. Moreover, the growing trend for single-family housing in Brazil is likely support the residential construction industry in the upcoming period.

- Mexico's housing starts and inventory levels reached a 10-year low due to a sharp cut in the federal housing subsidy program and the pandemic that triggered a severe recession. The Programa de Vivienda Social, or social housing program, had a budget increase of 179% to USD 200 million in 2021, thus, supporting construction spending. Moreover, accessible loan facilities and favorable mortgage schemes are expected to benefit residential construction in the country.

- The low-cost housing segment is rising steadily, primarily due to government initiatives to provide affordable housing to the poor in urban and rural regions.

- The consumption of flooring adhesives in constructing low-cost houses is comparatively less than other types of houses. Various countries across the world are providing shelter to refugees from other countries. Hence, governments offer temporary or permanent low-cost housing to refugees.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region dominates the global floor adhesives market share. With growing construction activities in countries such as China, India, and ASEAN Countries, the consumption of floor adhesives is increasing in the region.

- The Chinese government has rolled out massive construction plans, including making provisions for the movement of 250 million people to its new megacities, over the next ten years, despite efforts to rebalance its economy to a more service-oriented form.

- The National Bureau of Statistics of China reports that the market for construction works in China increased from CNY 23.27 trillion (USD 3.34 trillion) in 2020 to CNY 25.92 trillion (USD 3.72 trillion) in 2021.

- The country has the largest construction market in the world, encompassing 20% of all construction investments globally. China is expected to spend nearly USD 13 trillion on buildings by 2030. China is promoting and undergoing a process of continuous urbanization, with a target rate of 70% for 2030.

- Because of the government's increased attention to infrastructure projects and the predicted rapid rebound in demand for both residential and commercial segments, the construction sector was expected to grow by 10.7% in FY22. Hence, the growing construction activities in the country are expected to increase the demand for floor adhesives.

- Various policies implemented by the Indian government, such as Smart City projects, Housing for All by 2022, etc., are expected to bring the needed impetus to the slowing construction industry. Moreover, recent policy reforms, such as the Real Estate Act, GST, and REITs, are expected to reduce approval delays and strengthen the construction sector over the next few years.

- According to statistical office data, construction orders won by South Korean builders in 2021 increased by double digits due to robust international demand. According to Statistics Korea, construction orders collected by local builders both at home and overseas totaled USD 245.9 billion in 2021, up by 31 trillion won from 2020.

Floor Adhesives Industry Overview

The global floor adhesives market is partially consolidated. The major players include Sika AG, MAPEI S.p.A, Arkema Group (Bostik SA), HB Fuller Company, and Dow.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rapidly Growing Global Construction Industry

- 4.1.2 Versatility, Safety, and Ease of Application of Floor Adhesives

- 4.2 Restraints

- 4.2.1 Hazardous Health Effects Due to VOC Emissions

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Resin Type

- 5.1.1 Epoxy

- 5.1.2 Polyurethane

- 5.1.3 Acrylic

- 5.1.4 Vinyl

- 5.1.5 Other Resin Types

- 5.2 Technology

- 5.2.1 Water-borne

- 5.2.2 Solvent-borne

- 5.2.3 Other Technologies

- 5.3 Application

- 5.3.1 Tile & Stone

- 5.3.2 Carpet

- 5.3.3 Wood

- 5.3.4 Laminate

- 5.3.5 Resilent Flooring

- 5.3.6 Other Applications

- 5.4 End-user Industry

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.4.3 Industrial

- 5.5 Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Arkema Group (Bostik SA)

- 6.4.3 Ashland

- 6.4.4 Dow

- 6.4.5 Forbo Holding AG

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Jowat SE

- 6.4.9 LATICRETE International Inc.

- 6.4.10 MAPEI SpA

- 6.4.11 Pidilite Industries Limited

- 6.4.12 Sika AG

- 6.4.13 Tesa SE

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand for Bio-based Floor Adhesives

02-2729-4219

+886-2-2729-4219

地板黏合剂市场:类型、技术、销售管道、应用和最终用途 - 2026-2032年全球市场预测

地板黏合剂市场:类型、技术、销售管道、应用和最终用途 - 2026-2032年全球市场预测 全球地板黏合剂市场规模、份额、趋势和成长分析报告(2026-2034)

全球地板黏合剂市场规模、份额、趋势和成长分析报告(2026-2034) 2026年全球地板黏合剂市场报告

2026年全球地板黏合剂市场报告 地板黏合剂市场规模、份额和成长分析(按树脂类型、技术、应用、最终用户和地区划分)—2026-2033年产业预测

地板黏合剂市场规模、份额和成长分析(按树脂类型、技术、应用、最终用户和地区划分)—2026-2033年产业预测 地板黏合剂市场-全球产业规模、份额、趋势、机会和预测,按树脂类型、技术、应用、地区和竞争格局划分,2020-2030年预测

地板黏合剂市场-全球产业规模、份额、趋势、机会和预测,按树脂类型、技术、应用、地区和竞争格局划分,2020-2030年预测 亚太地板树脂:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

亚太地板树脂:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年) 2024-2028年全球地板胶市场

2024-2028年全球地板胶市场