|

市场调查报告书

商品编码

1689815

水产养殖:市场占有率分析、产业趋势与统计、成长预测(2025-2030)Aquaponics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

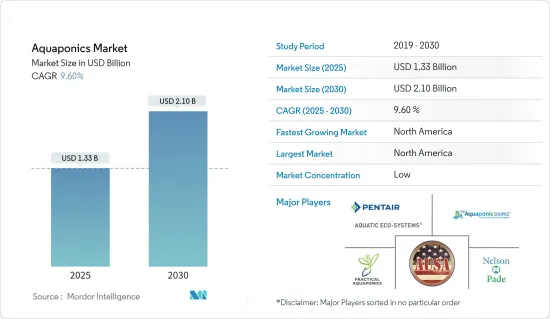

预计 2025 年水产养殖市场规模为 13.3 亿美元,到 2030 年将达到 21 亿美元,预测期内(2025-2030 年)的复合年增长率为 9.6%。

COVID-19 疫情对水产养殖市场供应链产生了重大影响。疫情期间供应链中断导致农民大量养殖活鱼和其他水生物种,对农民的成本、支出和风险造成不利影响。

2021年,北美占据了水产养殖市场的最大份额。美国在该地区占比最大,其次是加拿大。水产养殖业是该地区规模虽小但发展迅速的产业,与多家教育和研究机构以及私人公司建立了合作伙伴关係。这一因素在建立和提高水产养殖农场的知名度方面发挥了关键作用。儘管 Superior Fresh 和 Ouroboros Farms 等农场处于商业性水产养殖生产的前沿,但该地区尚未实现水产养殖作物的大规模生产。

水产养殖市场趋势

有机农产品需求旺盛推动市场

由于水产养殖不使用任何合成肥料或作物保护化学品,且鱼类废物是植物的主要营养物质,因此对有机种植作物的需求潜力很大,这使其成为新兴水产养殖农场和水产养殖系统提供者尚未开发的领域。有机贸易协会报告称,2018 年有机水果和蔬菜的销售额成长 5.6%,达到 174 亿美元,高于去年的 164.2 亿美元。因此,美国已成为有机种植水果和蔬菜的主要市场之一。此外,欧洲是世界上有机农地面积最大的国家之一,其中西班牙占最大份额,有机种植面积达 2,246,475.0 公顷。由于水产养殖在有机农产品产业中占有重要地位,欧洲资助的 COST 行动 FA1305「欧盟水产养殖中心 - 为欧盟实现全面永续鱼类和蔬菜生产」加强了研究人员和私人公司之间的网络。因此,预计预测期内对有机农产品的需求将推动全球水产养殖产业的发展。

北美占据市场主导地位

儘管水产养殖在北美仍是一个小产业,但预计未来几年将呈指数级增长。 2014 年,威斯康辛大学史蒂文斯分校和 Nelson and Pade Aquaponics 公司达成官民合作关係(PPP),并建立了 Aquaponics研发中心,作为威斯康辛大学系统经济发展激励基金的一部分。此类倡议对于提高当地人对水产养殖等永续农业选择的认识发挥着至关重要的作用。此外,水产养殖有望协助重组美国水产养殖业。威斯康辛州的水产养殖场数量最近从 2,300 个增加到 2,800 个,根据 2018 年美国水产养殖大会的透露,500 个新农场中有 300 个是水产养殖场。目前,美国每年消费的水产品有80.0%以上依赖进口。该国水产养殖场的兴起可能有助于逐步减少鱼贝类进口。

鱼菜共生产业概览

水产养殖市场高度细分,主要是由于市场不断发展的特性。一些最活跃的水产养殖农场包括 Superior Fresh、Ouroboros Farms、Garden City Aquaponics Inc.、BIGH、Deep Water Farms 和 Madhavi Farms。一些主要企业包括 Pentair Aquatic Eco-System Inc. (PAES)、Nelson & Pade Aquaponics、Practical Aquaponics、Aquaponics USA 和 The Aquaponic Source。由于市场仍在扩大,新兴企业正在製定产品推出和产能扩张策略,以抢占相当大的市场占有率份额。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概览

- 市场驱动因素

- 市场限制

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

第五章市场区隔

- 进阶系统

- 媒体挤满了床

- 恆流

- 潮流(洪水和排水)

- 营养膜技术(NFT)

- 筏式或深海养殖(DWC)

- 媒体挤满了床

- 设施类型

- 聚乙烯或玻璃温室

- 室内垂直农场

- 其他设施类型

- 鱼类

- 吴郭鱼

- 鲶鱼

- 鲤鱼

- 鳟鱼

- 观赏鱼

- 其他鱼类

- 地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 北美其他地区

- 欧洲

- 英国

- 法国

- 德国

- 义大利

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 马来西亚

- 印尼

- 澳洲

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 非洲

- 南非

- 其他非洲国家

- 北美洲

第六章 竞争格局

- 最受欢迎的策略

- 水产养殖投入品供应商

- 水产养殖农场

- 市场占有率分析

- 水产养殖投入品供应商

- 水产养殖农场

- 公司简介 – 鱼菜共生投入品供应商

- Pentair Aquatic Eco-System Inc.(PAES)

- Nelson & Pade Aquaponics

- Practical Aquaponics

- Aquaponics USA

- The Aquaponic Source

- 公司简介 - 鱼菜共生农场

- Superior Fresh

- Ouroboros Farms

- Garden City Aquaponics Inc.

- BIGH

- Deep Water Farms

- Madhavi Farms

- ECF Farm Berlin

第七章 市场机会与未来趋势

第八章 COVID-19 市场影响评估

The Aquaponics Market size is estimated at USD 1.33 billion in 2025, and is expected to reach USD 2.10 billion by 2030, at a CAGR of 9.6% during the forecast period (2025-2030).

The COVID-19 pandemic majorly impacted the supply chain of the aquaponics market. Supply chain disruptions amid the pandemic led farmers to rear many live fishes and other aquatic species, which negatively impacted the farmers' cost, expenditure, and risk.

In 2021, North America occupied the largest share in the aquaponics market. The United States contributed the largest share in the region, followed by Canada. Aquaponic is a small but rapidly growing industry in the region, with several partnerships among educational and research institutions and private companies. This factor played a pivotal role in establishing and increasing awareness about aquaponic farms. However, mass-scale production of aquaponic crops is yet to take form in the region, although farms such as Superior Fresh and Ouroboros Farms are at the forefront of commercial aquaponics production.

Aquaponics Market Trends

Substantial Demand for Organic Produce Driving the Market

As aquaponics are free from chemical fertilizers and crop protection chemicals, with fish waste serving as the prime nutrients for plants, the demand for organically grown crops holds high potential and an untapped space for emerging aquaponic farms and aquaponic system providers. As reported by the Organic Trade Association, sales of organic fruits and vegetables rose by 5.6% to USD 17.40 billion in 2018 from USD 16.42 billion in the previous year. Thus, the United States became one of the leading markets for organically grown fruits and vegetables. Moreover, Europe holds one of the largest organic farmland areas globally, with Spain accounting for the largest share with 2,246,475.0 ha of the area under organic farming. As a result of the underlying scope for aquaponic farming in the organic produce industry, the European-funded COST Action FA1305, 'The European Union Aquaponics Hub-Realising Sustainable Integrated Fish and Vegetable Production for the EU', strengthened the network between researchers and private players. Therefore, the demand for organically grown produce is expected to drive the global aquaponics industry during the forecast period.

North America Dominates the Market

Although still a small industry in North America, aquaponic farming is expected to witness exponential growth in the coming years. In 2014, the University of Wisconsin - Stevens Point and Nelson and Pade Aquaponics entered a Public-Private Partnership (PPP) to establish an Aquaponics Innovation Center as part of the UW-System Economic Development Incentive Grant. Such initiatives have played a pivotal role in raising awareness about sustainable farming alternatives, such as aquaponics, in the region. Additionally, aquaponics is expected to help rebuild the aquaculture industry in the United States. In Wisconsin, the number of aquaculture farms recently rose from 2,300 to 2,800, with 300 out of the 500 new farms being aquaponic farms, as revealed at the Aquaculture America Conference in 2018. Currently, the United States imports more than 80.0% of the seafood it consumes annually. The rising number of aquaponic farms in the country may help it reduce its seafood import over time.

Aquaponics Industry Overview

The aquaponics market is highly fragmented, primarily due to the evolving nature of the market. Some of the most active aquaponic farms are Superior Fresh, Ouroboros Farms, Garden City Aquaponics Inc., BIGH, Deep Water Farms, and Madhavi Farms. Some major aquaponic input providers are Pentair Aquatic Eco-System Inc. (PAES), Nelson & Pade Aquaponics, Practical Aquaponics, Aquaponics USA, and The Aquaponic Source. As the market is still expanding, emerging players are strategizing product launches and capacity expansions to secure a substantial share in the market studied.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Growing System

- 5.1.1 Media Filled Beds

- 5.1.1.1 Constant Flow

- 5.1.1.2 Ebb and Flow (Flood and Drain)

- 5.1.2 Nutrient Film Technique (NFT)

- 5.1.3 Raft or Deep Water Culture (DWC)

- 5.1.1 Media Filled Beds

- 5.2 Facility Type

- 5.2.1 Poly or Glass Greenhouses

- 5.2.2 Indoor Vertical Farms

- 5.2.3 Other Facility Types

- 5.3 Fish Type

- 5.3.1 Tilapia

- 5.3.2 Catfish

- 5.3.3 Carp

- 5.3.4 Trout

- 5.3.5 Ornamental Fish

- 5.3.6 Other Fish Types

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 France

- 5.4.2.3 Germany

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Malaysia

- 5.4.3.4 Indonesia

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.1.1 Aquaponics Input Providers

- 6.1.2 Aquaponic Farms

- 6.2 Market Share Analysis

- 6.2.1 Aquaponics Input Providers

- 6.2.2 Aquaponic Farms

- 6.3 Company Profiles - Aquaponics Input Providers

- 6.3.1 Pentair Aquatic Eco-System Inc. (PAES)

- 6.3.2 Nelson & Pade Aquaponics

- 6.3.3 Practical Aquaponics

- 6.3.4 Aquaponics USA

- 6.3.5 The Aquaponic Source

- 6.4 Company Profile - Aquaponic Farms

- 6.4.1 Superior Fresh

- 6.4.2 Ouroboros Farms

- 6.4.3 Garden City Aquaponics Inc.

- 6.4.4 BIGH

- 6.4.5 Deep Water Farms

- 6.4.6 Madhavi Farms

- 6.4.7 ECF Farm Berlin

7 MARKET OPPORTUNITITES AND FUTURE TRENDS

8 AN ASSESSMENT OF COVID-19 IMPACT ON THE MARKET

水耕市场:2026-2032年全球市场预测(依鱼类、系统类型、安装地点、销售管道及应用划分)

水耕市场:2026-2032年全球市场预测(依鱼类、系统类型、安装地点、销售管道及应用划分) 2026年全球鱼菜共生市场报告

2026年全球鱼菜共生市场报告 水耕市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测

水耕市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测 水耕市场商机、成长要素、产业趋势分析及2026-2035年预测。全球海洋水族设备市场(按设备类型、服务类型、技术、最终用户和分销管道划分)预测(2026-2032年)

水耕市场商机、成长要素、产业趋势分析及2026-2035年预测。全球海洋水族设备市场(按设备类型、服务类型、技术、最终用户和分销管道划分)预测(2026-2032年) 水产养殖市场:全球产业分析、规模、份额、成长、趋势与预测(2025-2032)

水产养殖市场:全球产业分析、规模、份额、成长、趋势与预测(2025-2032) 鱼菜共生市场-全球产业规模、份额、趋势、机会及预测,依设备、方法(基于介质、营养膜技术和深水养殖)、应用、区域和竞争细分,2020-2030 年预测全球水产养殖市场:2025-2030 年预测

鱼菜共生市场-全球产业规模、份额、趋势、机会及预测,依设备、方法(基于介质、营养膜技术和深水养殖)、应用、区域和竞争细分,2020-2030 年预测全球水产养殖市场:2025-2030 年预测 2032 年全球鱼菜共生市场预测:按系统类型、设备类型、产品、组件、营运规模、应用和地区划分

2032 年全球鱼菜共生市场预测:按系统类型、设备类型、产品、组件、营运规模、应用和地区划分 2034 年水产养殖市场分析及预测:类型、产品、服务、技术、组件、应用、形式、材料类型、最终用户、设备

2034 年水产养殖市场分析及预测:类型、产品、服务、技术、组件、应用、形式、材料类型、最终用户、设备