|

市场调查报告书

商品编码

1689929

运动复合材料:市场占有率分析、行业趋势和成长预测(2025-2030 年)Sports Composites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

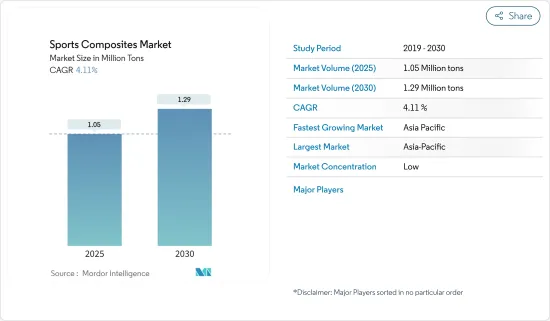

预计 2025 年运动复合材料市场规模为 105 万吨,2030 年将达到 129 万吨,预测期间(2025-2030 年)的复合年增长率为 4.11%。

2020 年,COVID-19 疫情对市场造成了影响,全国停工、製造活动和供应链中断、全球范围内的生产暂停。然而,情况在 2021 年开始復苏,市场在预测期内恢復成长轨迹。

主要亮点

- 对轻型、高性能运动器材的需求不断增加以及高尔夫行业的不断发展是预测期内推动市场发展的主要因素。

- 另一方面,碳纤维製造成本高造成的不利条件阻碍了市场的成长。

- 新能源复合材料在运动装备领域的应用不断扩大,可望为市场带来新的成长机会。

- 预计预测期内亚太地区将主导全球运动复合材料市场。

运动复合材料市场趋势

滑雪和单板滑雪的需求不断增长

- 碳纤维在滑雪板和滑雪板製造中的应用已相当广泛,涵盖越野滑雪、竞赛滑雪、自由骑行和滑雪登山等所有类别。

- 这种现象为滑雪板的技术特性带来了多种优势。但由于时尚和製造商的营销策略,也存在夸张的情况。

- 碳纤维在滑雪板和滑雪板製造(尤其是滑雪登山)中的成功应用是由于其优良的特性:品质轻且滑雪板较宽(脚下超过 100 毫米)。

- 利用纤维增强塑胶(FRP)的内部黏合效应,开发出一种采用异向性层设计的新型滑雪板技术。该研究涉及由三种替代材料(即碳纤维、玻璃纤维和亚麻纤维增强复合材料)製成的滑雪板的技术、经济和环境评估。

- 在这种情况下,材料选择和纤维排列角度都会从成本、环境和技术三个分析维度显着影响所得 FRP 的刚度。

- 从环境角度来看,天然纤维是最永续的选择,从经济角度来看,玻璃纤维是最好的,从技术角度来看,碳纤维是最好的。因此,对于任何製造商而言,在做出决策之前,每个分析项目的重要性都至关重要。

- 美国和加拿大是滑雪板和滑雪板製造复合材料的主要消费国,因为这些材料在气候较温暖的国家的使用有限。

- 预计所有这些因素将有助于确定预测期内全球对复合材料的需求。

亚太地区占市场主导地位

- 预计预测期内亚太地区将主导全球运动复合材料市场。

- 由于竞争激烈、媒体赞助和社会认可度不断提高,体育产业正在经历快速成长。

- 中国已成为运动服装、配件和鞋类的一个有吸引力的市场。由于人事费用上升,跨国公司正在将业务迁往中国以外。然而,运动服和运动服的需求量很大。

- 根据国际贸易局预测,2024年,中国运动服饰市场规模将达到828亿美元,年增率为11%。

- 中国将于2023年举办2022年亚运。根据亚奥理事会(OCA)介绍,亚运会将于2023年9月23日至10月8日在杭州举行。亚运会通常会吸引来自全部区域的10,000多名运动员参赛。

- 此外,在印度,根据印度青年事务和体育部的数据,印度政府透过「Khelo India」计画在2021-22年用于体育的支出将达到83.9亿印度卢比(1.1亿美元)。此类支出和体育规划可能会支持学习市场的需求。

- 印度2021-22年自行车及零件资料总额为343.3亿印度卢比(4.6亿美元),2021-22年进口资料为187.64亿印度卢比(2.51亿美元)。

- 因此,近年来对高尔夫球桿、曲棍球棒、球拍、自行车等运动器材的需求不断增加,预计将进一步推动该地区研究市场的需求。

运动复合材料产业概况

全球运动复合材料市场较为分散。主要公司包括东丽、西格里碳素、三菱化学碳纤维及复合材料、Rockwest复合材料及Excel复合材料。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 对轻量、高性能运动用品的需求不断增加

- 高尔夫产业的成长

- 限制因素

- 碳纤维製造成本高

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔

- 类型

- 玻璃纤维增强

- 碳纤维增强

- 其他类型

- 树脂类型

- 环氧树脂

- 聚氨酯

- 其他树脂类型

- 应用

- 高尔夫球桿

- 曲棍球棒

- 球拍

- 自行车

- 滑雪和单板滑雪

- 其他用途

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章竞争格局

- 併购、合资、合作与协议

- 市场排名分析

- 主要企业策略

- 公司简介

- Celanese Corporation

- Dexcraft

- EPSILON Composite

- Exel Composites

- Mitsubishi Chemical Carbon Fiber and Composites Inc.

- Rockman

- Rock West Composites

- SGL Carbon

- Toray Industries Inc.

- Topkey

第七章 市场机会与未来趋势

- 新能源复合材料在体育用品的应用

The Sports Composites Market size is estimated at 1.05 million tons in 2025, and is expected to reach 1.29 million tons by 2030, at a CAGR of 4.11% during the forecast period (2025-2030).

Due to the COVID-19 outbreak, nationwide lockdowns around the globe, disruption in manufacturing activities and supply chains, and production halts impacted the market in 2020. However, the conditions started recovering in 2021, restoring the market's growth trajectory during the forecast period.

Key Highlights

- The major factor driving the market studied is the increasing demand for lightweight and high-performance sports equipment and the growing golf industry during the forecast period.

- On the flip side, unfavorable conditions arising due to the high manufacturing cost of carbon fibers hinder the market's growth.

- The growing application of new energy composites in sports equipment will likely provide new growth opportunities for the market.

- Asia-Pacific region is expected to dominate the global sports composites market during the forecast period.

Sports Composites Market Trends

Increasing Demand for Skis and Snowboards

- The use of carbon fibers in the construction of skis and snowboards has spread considerably in all categories, including piste skiing, race, freeride, and ski mountaineering.

- This phenomenon has led to some advantages in the technical characteristics of the skis. However, there have also been some exaggerations, largely due to fashion and the marketing policies of manufacturers.

- The appropriate use of carbon fibers in the construction of skis and snowboards, especially for ski mountaineering, is owing to its excellent characteristics with a contained mass and even wider skis (over 100 mm under the foot).

- A new snowboard technology was developed using an anisotropic layer design, taking advantage of the internal coupling effects of fiber-reinforced plastics (FRP). This work deals with the technical, economic, and environmental evaluation of a snowboard made of three alternative materials, namely carbon, glass, and flax fiber-reinforced composites.

- In this case, both the material choice and the fiber placement angles significantly impact the stiffness of the resulting FRP in the three dimensions of analysis: cost, environmental, and technical.

- The natural fiber is the most sustainable option environmentally, glass fiber is the best economically, and carbon fiber is the best in terms of technical performance. Therefore, the importance attributed to each dimension of analysis is essential for any manufacturer before making the decision.

- Owing to its limited usage in warmer countries, the United States and Canada are the primary consumers of composites for manufacturing skis and snowboards.

- All such factors are expected to help determine the global demand for composites over the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific region is expected to dominate the global sports composites market during the forecast period.

- The sports industry has been growing significantly due to high competition, media sponsorships, and increased social awareness.

- China has been an attractive market for athletic apparel, accessories, and footwear. Multinational companies are shifting their operations outside China due to rising labor costs. However, the country has a high demand for sportswear and activewear.

- According to the International Trade Administration, the Chinese sportswear market is expected to reach USD 82.8 billion by 2024, growing at an annual rate of 11%.

- China will host the 2022 Asian Games in 2023. The games will take place in Hangzhou from September 23 to October 8, 2023, as per the Olympic Council of Asia (OCA). The Asian Games generally attract more than 10,000 athletes across the region.

- Moreover, in India, according to the Ministry of Youth Affairs and Sports, the expenditure on sports by the Indian government in FY 2021-22 accounted for INR 8.39 billion (USD 0.11 billion) through the Khelo India scheme. Such expenditures and sports schemes are likely to support the demand for the market studied.

- India's total export data of bicycles and parts in 2021-2022 was INR 34,330 million ( USD 460 million), and the total import data in 2021-2022 was INR 18,764 million (USD 251 million).

- Therefore, the demand for sports equipment, such as golf shafts, hockey sticks, rackets, and bicycles, is expected to grow in recent times, further boosting the demand for the market studied in the region.

Sports Composites Industry Overview

The global sports composites market is fragmented in nature. The major companies are Toray Industries Inc., SGL Carbon, Mitsubishi Chemical Carbon Fiber and Composites Inc., Rock West Composites, and Exel Composites, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Lightweight and High-Performance Sports Equipment

- 4.1.2 Growing Golf Industry

- 4.2 Restraints

- 4.2.1 High Manufacturing Cost of Carbon Fibers

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Glass-Fibre Reinforced

- 5.1.2 Carbon-Fibre Reinforced

- 5.1.3 Other Types

- 5.2 Resin Type

- 5.2.1 Epoxy

- 5.2.2 Polyurethane

- 5.2.3 Other Resin Types

- 5.3 Applications

- 5.3.1 Golf Shafts

- 5.3.2 Hockey Sticks

- 5.3.3 Rackets

- 5.3.4 Bicycles

- 5.3.5 Skis and Snowboards

- 5.3.6 Other Applications

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Celanese Corporation

- 6.4.2 Dexcraft

- 6.4.3 EPSILON Composite

- 6.4.4 Exel Composites

- 6.4.5 Mitsubishi Chemical Carbon Fiber and Composites Inc.

- 6.4.6 Rockman

- 6.4.7 Rock West Composites

- 6.4.8 SGL Carbon

- 6.4.9 Toray Industries Inc.

- 6.4.10 Topkey

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Application of New Energy Composites in Sports Equipment