|

市场调查报告书

商品编码

1689934

聚乙烯亚胺:市场占有率分析、产业趋势与统计、成长预测(2025-2030)Polyethyleneimine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

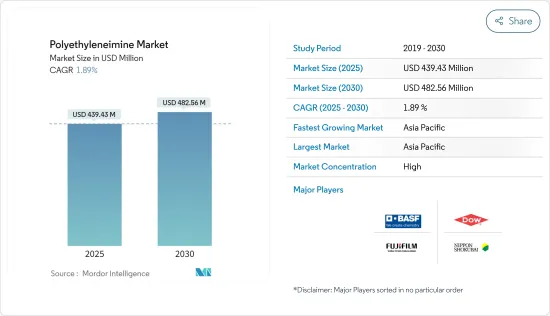

聚乙烯亚胺市场规模预计在 2025 年为 4.3943 亿美元,预计到 2030 年将达到 4.8256 亿美元,预测期内(2025-2030 年)的复合年增长率为 1.89%。

COVID-19 对市场产生了负面影响。不过,市场已达到疫情前的水平,预计在预测期内将稳定成长。

主要亮点

- 推动市场发展的首要因素是清洁剂和水处理化学品应用的需求不断增加,以及对黏合剂和密封剂的使用量不断增加。

- 另一方面,严格的环境法规阻碍了市场成长。

- 聚乙烯亚胺-奈米二氧化硅复合材料的发展以及个人护理和化妆品行业的快速扩张等因素预计将为市场提供各种成长机会。

- 亚太地区占全球市场主导地位,其中中国和印度的消费量最大。

聚乙烯亚胺市场趋势

黏合剂和密封剂领域占据市场主导地位

- 聚乙烯亚胺 (PEI) 广泛应用于黏合剂和密封剂。在黏合剂行业中,它被用作层压中的黏合促进剂。它也用于包装膜的水性底漆。

- 聚乙烯亚胺长期以来一直被用作包装工业中挤压涂布的底漆。特别是,它用于将聚乙烯粘合到纸张等纤维素基材上。在实践中,使用的是水或水和酒精的稀释溶液。

- 包装产业是全球最大的黏合剂消费产业。预计这一趋势将在预测期内持续下去,这主要是由于食品和饮料行业对包装应用的强劲需求。

- 黏合剂是包装行业最常用的黏合机制之一。聚乙烯亚胺基黏合剂主要用于冷冻食品包装。这推动了包装行业对黏合剂的需求,从而促进了市场的发展。

- 根据标普全球的数据,2021 年印度国内黏合剂和密封剂市场价值为 1,340 亿至 1,360 亿印度卢比(18.1 亿至 18.3 亿美元)。印度黏合剂和密封剂市场分为两个部分。工业领域面向包装、鞋类、油漆、汽车等 B2B 产业。零售领域面向家具/木工、建筑施工、工艺品、电气配件等行业。

- 电子业使用黏合剂进行各种应用,包括三防胶、端子电极保护和表面黏着型元件的黏合。电子产业是印度成长最快的产业之一,根据印度电子和资讯技术部的数据,预计 2021 年市场规模将达到 4.95 兆至 5.0 兆印度卢比(669.5 亿至 676.2 亿美元)。

- 由于上述因素,黏合剂和密封剂领域很可能在预测期内占据市场主导地位。

亚太地区占市场主导地位

- 由于聚乙烯亚胺在清洁剂、黏合剂、水处理化学品、化妆品和造纸等领域的广泛应用,预计亚太地区将在预测期内占据聚乙烯亚胺市场的主导地位。

- 聚乙烯亚胺在纸浆和造纸生产中用作湿强度剂。中国、印度和东南亚的造纸和纸浆工业的成长可能会继续成为市场驱动因素。

- 中国是油墨生产成长最快的国家之一。中国的油墨产业由国际油墨製造商和国内企业组成,例如与T&K Toka合资的杭州东华油墨和与东洋油墨合资的天津东洋油墨,它们都是中国主要的跨国油墨供应商。此外,DIC、坂田INX、盛威科、富林特集团、Hubergroup等主要油墨製造商也在中国设有製造工厂。叶氏化工的子公司紫荆油墨化工有限公司是国内最大的油墨製造商。

- 由于消费者习惯的改变和对家庭卫生的日益重视,中国对清洁剂和工业清洗产品的需求很高。新冠疫情导致中国市场对清洁剂和工业清洗产品的需求大幅增加。 2020年清洁剂和清洗剂的销量增加了10倍。 2021年,销量成长了400-500%。

- 肥皂製造是印度快速消费品产业最古老的产业之一,占消费品产业的 50% 以上。最近的数据显示,全国约有500万个肥皂零售店,其中375万个位于农村地区。

- 印度和丹麦在哥本哈根举行的 2022 年世界水大会和展览会上发布了一份关于「印度都市废水情景」的白皮书。 2021年,印度都市区污水产生量为72,368 MLD,而污水处理能力仅31,841 MLD。印度政府正在根据去年宣布的「清洁印度计画 2.0」(SBM2.0)努力提高污水处理能力。预计这将对水处理领域的聚乙烯亚胺产生巨大的需求。

- 由于其成长潜力,製造商正在投资印度黏合剂产业。因此,预计新建工厂和产能扩张将增加该国对聚乙烯亚胺的需求。例如,2021年12月,西卡宣布计划在印度普纳开设一个新的技术中心和高品质黏合剂和密封剂製造工厂。

- 因此,由于这些因素,预计亚太地区将主导整个市场。

聚乙烯亚胺产业概况

聚乙烯亚胺市场高度整合,有国际和国内参与者参与。主要企业(排名不分先后)包括BASF公司、日本触媒、陶氏化学、富士胶片和光纯化学株式会社。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 清洁剂和水处理化学品应用的需求不断增加

- 扩大在黏合剂和密封剂的应用

- 限制因素

- 严格的环境法规

- 其他的

- 价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔

- 按类型

- 线性

- 分支类型

- 按应用

- 清洁剂

- 黏合剂和密封剂

- 水处理化学品

- 化妆品

- 纸

- 涂料、油墨、染料

- 其他的

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 市场排名分析

- 主要企业策略

- 公司简介

- BASF SE

- Dow

- FUJIFILM Wako Pure Chemical Corporation

- Gongbike New Material Technology(Shanghai)Co. Ltd

- NIPPON SHOKUBAI Co. Ltd

- Polysciences, Inc.

- SERVA Electrophoresis GmbH

- Shanghai Holdenchem Co.

- WUHAN BRIGHT CHEMICAL Co. Ltd

第七章 市场机会与未来趋势

- 聚乙烯亚胺-奈米二氧化硅复合材料的研发

- 个人护理和化妆品行业的快速扩张

The Polyethyleneimine Market size is estimated at USD 439.43 million in 2025, and is expected to reach USD 482.56 million by 2030, at a CAGR of 1.89% during the forecast period (2025-2030).

The impact of COVID-19 on the market was negative. However, the market has reached pre-pandemic levels and is expected to grow steadily during the forecast period.

Key Highlights

- The major factors driving the market are the increasing demand from applications in detergents and water treatment chemicals and the growing usage in adhesives and sealants.

- On the flip side, stringent environmental regulations are hindering the growth of the market.

- Factors such as the development of polyethyleneimine-nano silica composites and the rapidly expanding personal care and cosmetics industry are expected to offer various growth opportunities for the market.

- Asia-Pacific dominates the market worldwide, with the largest consumption coming from China and India.

Polyethyleneimine Market Trends

Adhesives and Sealants Segment to Dominate the Market

- Polyethyleneimine (PEI) is used for a wide range of adhesive and sealant applications. It is used for laminations in the adhesives industry as an adhesion promoter. It is also used in water-based primers for packaging films.

- Polyethyleneimine has been used for some time as an extrusion coating primer in the packaging industry. It has particularly found use in bonding polyethylene to paper and other cellulosic substrates. In practice, it is applied with diluted water or water-alcohol solutions.

- The packaging industry is the largest consumer of adhesives globally. This trend is estimated to continue during the forecast period, primarily due to the robust demand for packaging applications in the food and beverage sector.

- Adhesives are one of the most common bonding mechanisms used in the packaging industry. Polyethyleneimine-based adhesives are used majorly in the packaging of frozen food products. This factor boosts the demand for adhesives in the packaging industry, thus driving the market studied.

- According to S&P Global, India's domestic adhesives and sealants market is INR 134-136 billion (~USD 1.81-1.83 billion) in fiscal year 2021. Indian adhesives and sealant market is divided into two segment. The industrial segment caters to B2B industries such as packaging, footwear, paints, automotive, etc. The retail segment caters to industries such as furniture/woodwork, building construction, arts and craft, electrical fittings, etc.

- The electronics industry uses adhesives for various applications, including conformal coatings, protecting terminal electrodes, bonding of surface mount devices, among many others. The electronics industry is one of the fastest-growing industries in India and, as per the Ministry of Electronics and IT, the market size of the industry is INR 4,950-5,000 billion (~ USD 66.95-67.62 billion) as of fiscal 2021.

- Based on the above-mentioned factors, the adhesive and sealants segment is likely to dominate the market during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific is expected to dominate the market for polyethyleneimine during the forecast period, as polyethyleneimine is strongly used in applications, such as detergents, adhesives, water treatment chemicals, cosmetics, and paper, in the region.

- Polyethyleneimine is used as a wet strengthening agent in pulp and paper manufacturing. The growing paper and pulp industry in China, India, and Southeast Asia may continue to act as a driver for the market studied.

- China is one of the fastest-growing countries in terms of ink production. The country's ink industry is a mix of international ink manufacturers and domestic players, including Hangzhou TOKA Ink, a JV with T&K Toka, and Tianjin Toyo Ink Co. Ltd, a JV with Toyo Ink, which are the leading multi-national ink suppliers in China. DIC, Sakata INX, Siegwerk, Flint Group, Hubergroup, and other major ink companies also have manufacturing plants in China. The Bauhinia Variegata Ink & Chemicals, a subsidiary of Yip's Chemical, is the largest domestic ink producer in the country.

- The detergents and industrial cleaning agents are gaining demand in China due to changing consumer habits and growing attention toward hygiene at home. Due to the COVID-19 pandemic, the Chinese market witnessed a huge rise in demand for detergent and industrial cleaning agents. The sales revenue for detergents and cleaning agents witnessed a ten-fold growth in 2020. In 2021, the sales grew by 400-500%.

- Soap manufacturing is one of the oldest industries operating in the FMCG sector in India, accounting for more than 50% of the consumer goods sector. As per recent data, there are approximately five million retail outlets selling soaps in the country, of which 3.75 million operate in rural areas.

- India and Denmark together launched a whitepaper recently on 'Urban Wastewater Scenario in India' at World Water Congress and Exhibition 2022 in Copenhagen. In 2021 India's sewage generation was 72,368 MLD in urban centres, whereas the installed sewage treatment capacity was only 31,841 MLD. The government is trying to increase the sewage treatment capacity under the government Swachh Bharat Mission 2.0 (SBM 2.0), which was announced last year. This is expected to create a huge demand for polyethyleneimine in water treatment.

- The manufacturers have been investing in the Indian adhesives industry due to its growth potential. Thus, new plants and capacity expansions in the pipeline are projected to increase the demand for polyethyleneimine in the country. For instance, in December 2021, Sika announced its plans to open a new technology center and manufacturing plant for high-quality adhesives and sealants in Pune, India.

- Thus, such factors are expected to help the Asia-Pacific region dominate the overall market.

Polyethyleneimine Industry Overview

The polyethyleneimine market is highly consolidated with the presence of international and domestic players. The major companies (in no particular order) include BASF SE, Nippon Shokubai Co. Ltd, Dow, and FUJIFILM Wako Pure Chemical Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Drivers

- 4.1.1 Increasing Demand from Applications in Detergents and Water Treatment Chemicals

- 4.1.2 Growing Usage in Adhesive and Sealant Applications

- 4.2 Restraints

- 4.2.1 Stringent Environment Regulations

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 Market Segmentation (Market Size in Revenue)

- 5.1 Type

- 5.1.1 Linear

- 5.1.2 Branched

- 5.2 Application

- 5.2.1 Detergents

- 5.2.2 Adhesives and Sealants

- 5.2.3 Water Treatment Chemicals

- 5.2.4 Cosmetics

- 5.2.5 Paper

- 5.2.6 Coatings, Inks, and Dyes

- 5.2.7 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Ranking Analysis

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BASF SE

- 6.3.2 Dow

- 6.3.3 FUJIFILM Wako Pure Chemical Corporation

- 6.3.4 Gongbike New Material Technology (Shanghai) Co. Ltd

- 6.3.5 NIPPON SHOKUBAI Co. Ltd

- 6.3.6 Polysciences, Inc.

- 6.3.7 SERVA Electrophoresis GmbH

- 6.3.8 Shanghai Holdenchem Co.

- 6.3.9 WUHAN BRIGHT CHEMICAL Co. Ltd

7 Market Opportunities and Future Trends

- 7.1 Development of Polyethyleneimine-nano Silica Composites

- 7.2 Rapidly Expanding Personal Care and Cosmetics Industry