|

市场调查报告书

商品编码

1689945

3D 列印长丝:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)3D Printing Filament - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

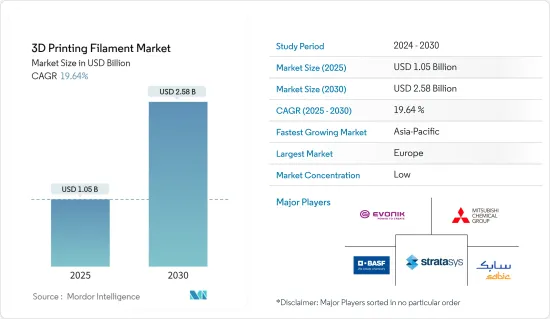

3D 列印线材市场规模预计在 2025 年为 10.5 亿美元,预计到 2030 年将达到 25.8 亿美元,预测期内(2025-2030 年)的复合年增长率为 19.64%。

COVID-19 疫情导致全球停工、製造活动和供应链中断以及生产停顿,所有这些都对 2020 年的市场产生了负面影响。不过,预计情况将在 2021-2022 年开始好转,预计市场在预测期内将与前一年同期比较增。

主要亮点

- 3D 列印长丝在製造应用中的使用日益增多,以及与 3D 列印相关的大规模定制,预计将在预测期内推动市场成长。

- 相反,3D 列印所需的高资本投入可能会阻碍市场成长。

- 医疗产业3D列印的技术创新和3D列印材料的进步可能成为未来市场值得研究的成长机会。

- 预计预测期内欧洲将占据市场主导地位,占据最大的市场占有率。

3D 列印线材市场趋势

医疗和牙科领域的需求增加可能会推动市场成长

- 医疗和牙科行业是3D列印长丝的主要使用者。它约占 3D 列印长丝总应用量的 30-35%。

- 使用各种细丝的 3D 列印技术已经能够创建组织和类器官、手术器械、针对特定患者的手术模型以及用于医疗和牙科应用的自订假体。这些3D列印物品为行业的进步和发展做出了巨大贡献。

- 3D 列印生产的医疗设备包括整形外科和颅骨植入、手术器械、牙冠等牙齿修復体以及外部假体。

- 2023 年 3 月,Invibio 扩大了其植入级 PEEK-OPTIMA 聚合物的选择范围,增加了专为医疗设备熔融长丝增材製造而设计的长丝。

- 2022年8月,3D陶瓷列印公司Lithoz报告称,由于其产品订单增加,今年上半年是该公司历史上最强劲的半年。该公司为各种医疗、牙科和工业应用提供各种陶瓷 3D 列印机。

- 由于上述因素,预计预测期内该行业将快速成长。

欧洲主导市场

- 以国内生产毛额计算,德国是欧洲最大的经济体。德国、英国和法国是世界上成长最快的经济体之一。

- 截至 2023 年 10 月,欧洲国内生产总值) 平均约有 11% 用于医疗保健,人均医疗技术支出约为 312 欧元(337 美元)。

- 根据MedTech Europe统计,欧洲拥有超过33,000家医疗技术公司。其中最多的是德国,其次是义大利、英国、法国和瑞士。中小型企业(SME)约占医疗科技产业的 95%。

- 德国航太工业在全国拥有2,300多家企业,其中最大的集中在德国北部。德国有许多飞机内装零件和材料的生产基地,主要分布在巴伐利亚州、不来梅州、巴登-符腾堡州和梅克伦堡-前波莫瑞州。

- 根据英国国际贸易部统计,英国电子产业每年为当地经济贡献160亿英镑(约195.3亿美元)。目前,该国占据欧洲电子设计产业 40% 的份额。目前该行业的专业知识重点关注积体电路 (IC)、RFID、光电子和电子元件。

- 法国是空中巴士、赛峰集团、巴西航空工业公司和达赫-索卡塔等製造商的主要製造地,因此其飞机製造和组装业务近期有所增加。

- 此外,根据 Air & Cosmos-International 报道,根据最新的军事规划法 (LPM),法国预计将在 2024 年至 2030 年期间在国防支出上花费 4,130 亿欧元(4,471.3 亿美元)。这很可能在未来大幅促进该国 3D 列印长丝的消费。

- 预计所有上述因素都将推动该地区对 3D 列印长丝的需求。

3D 列印耗材产业概况

3D列印线材市场高度分散,少数几家大公司占据了相当一部分市场份额。该市场的主要企业(不分先后顺序)包括 Stratasys Ltd、SABIC、 BASF SE、Evonik Industries AG 和三菱化学。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 扩大在製造业的应用

- 利用 3D 列印实现大规模客製化

- 限制因素

- 3D 列印製程的资本投入要求较高

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场区隔

- 类型

- 金属

- 钛

- 防锈的

- 其他金属

- 塑胶

- 聚对苯二甲酸乙二醇酯(PET)

- 聚乳酸(PLA)

- 丙烯腈丁二烯苯乙烯 (ABS)

- 尼龙

- 其他塑料

- 陶瓷

- 其他类型

- 金属

- 应用

- 航太和国防

- 车

- 医疗/牙科

- 电子产品

- 其他用途

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 越南

- 印尼

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧的

- 土耳其

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 奈及利亚

- 卡达

- 埃及

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- BASF SE

- Covestro Ag

- DOW

- DSM

- Evonik Industries Ag

- Keene Village Plastics

- Mitsubishi Chemical Corporation

- SABIC

- Solvay

- Shenzhen Esun Industrial Co. Ltd

- Stratasys

第七章 市场机会与未来趋势

- 医疗产业的 3D 列印创新

- 3D 列印材料的进步

The 3D Printing Filament Market size is estimated at USD 1.05 billion in 2025, and is expected to reach USD 2.58 billion by 2030, at a CAGR of 19.64% during the forecast period (2025-2030).

The COVID-19 outbreak caused nationwide lockdowns across the world, disruption in manufacturing activities and supply chains, and production halts, all of which had a negative impact on the market in 2020. However, conditions began to improve in 2021-2022, and the market is expected to grow year-on-year during the forecast period.

Key Highlights

- The growing usage of 3D printing filaments in manufacturing applications, along with mass customization associated with 3D printing, is expected to drive the market growth during the forecast period.

- Conversely, high capital investment requirements in 3D printing may hinder the market's growth.

- 3D printing innovation in the medical industry and advancements in 3D printing materials may act as growth opportunities for the market studied in the future.

- Europe is expected to dominate the market with the largest market share during the forecast period.

3D Printing Filament Market Trends

Increased Demand from the Medical and Dental Segment May Facilitate Market Growth

- The medical and dental industry is the leading industry that uses 3D printing filaments. It contributes to around 30-35% of the total applications of 3D printing filaments.

- 3D printing technology using different filaments allowed the creation of tissues and organoids, surgical tools, patient-specific surgical models, and custom-made prosthetics as applications in the medical and dental industry. These 3D-printed objects significantly contribute to the advancement and development of the industry.

- Medical devices produced by 3D printing include orthopedic and cranial implants, surgical instruments, dental restorations such as crowns, and external prosthetics.

- In March 2023, Invibio broadened its selection of implantable-grade PEEK-OPTIMA polymers by adding a filament specifically designed for fused filament additive manufacturing of medical devices.

- In August 2022, Lithoz, a 3D ceramic printing company, reported the first half of the year as the most successful in its history due to the increased order of its products. The company offers a wide range of ceramic 3D printers for various medical, dental, and industrial applications.

- Owing to all the above-mentioned factors, this segment is expected to grow rapidly in the market studied over the forecast period.

Europe to Dominate the Market

- Germany is the largest economy in Europe in terms of GDP. Germany, the United Kingdom, and France are among the fastest-emerging economies globally.

- As of October 2023, an average of approximately 11% of Europe's gross domestic product (GDP) was spent on healthcare, and expenditure on medical technology per capita was around EUR 312 (USD 337).

- According to MedTech Europe, over 33,000 medical technology companies are present in Europe. Most of them are located in Germany, followed by Italy, the United Kingdom, France, and Switzerland. Small and medium-sized companies (SMEs) make up around 95% of the medical technology industry.

- The German aerospace industry includes more than 2,300 firms located across the country, with Northern Germany recording the highest concentration of firms. The country hosts many production bases for aircraft interior components and materials, largely in Bavaria, Bremen, Baden-Wurttemberg, and Mecklenburg-Vorpommern.

- According to the Department for International Trade, the electronics industry in the United Kingdom contributes GBP 16 billion (~USD 19.53 billion) each year to the local economy. The country currently holds 40% of the share in the available electronics design industry in Europe. Current expertise within the industry is focused on integrated circuits (ICs), RFIDs, optoelectronics, and electronic components.

- France has been witnessing an increase in aircraft manufacturing and assembly operations in recent times as it is a major manufacturing base for manufacturers such as Airbus, Safran, Embraer, and Daher-Socata.

- Moreover, according to Air & Cosmos-International, France is expected to spend EUR 413 billion (USD 447.13 billion) on defense between 2024 and 2030 under its latest military programming law (LPM). This can substantially boost the country's consumption of 3D printing filament in the future.

- All the factors mentioned above are expected to boost the demand for 3D printing filament in the region.

3D Printing Filament Industry Overview

The 3D printing filament market is highly fragmented, with a few major players dominating a significant portion. Some of the major companies (not in any particular order) operating in the market include Stratasys Ltd, SABIC, BASF SE, Evonik Industries AG, and Mitsubishi Chemical Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Usage in Manufacturing Applications

- 4.1.2 Mass Customization Associated with 3D Printing

- 4.2 Restraints

- 4.2.1 High Capital Investment Requirement in 3D Printing Process

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Metals

- 5.1.1.1 Titanium

- 5.1.1.2 Stainless Steel

- 5.1.1.3 Other Metals

- 5.1.2 Plastics

- 5.1.2.1 Polyethylene Terephthalate (PET)

- 5.1.2.2 Polylactic Acid (PLA)

- 5.1.2.3 Acrylonitrile Butadiene Styrene (ABS)

- 5.1.2.4 Nylon

- 5.1.2.5 Other Plastics

- 5.1.3 Ceramics

- 5.1.4 Other Types

- 5.1.1 Metals

- 5.2 Application

- 5.2.1 Aerospace and Defense

- 5.2.2 Automotive

- 5.2.3 Medical and Dental

- 5.2.4 Electronics

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Vietnam

- 5.3.1.8 Indonesia

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC

- 5.3.3.8 Turkey

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Qatar

- 5.3.5.6 Egypt

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 Covestro Ag

- 6.4.3 DOW

- 6.4.4 DSM

- 6.4.5 Evonik Industries Ag

- 6.4.6 Keene Village Plastics

- 6.4.7 Mitsubishi Chemical Corporation

- 6.4.8 SABIC

- 6.4.9 Solvay

- 6.4.10 Shenzhen Esun Industrial Co. Ltd

- 6.4.11 Stratasys

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 3D Printing Innovation in the Medical Industry

- 7.2 Advancements in 3D Printing Materials

可回收3D列印耗材市场规模、份额及趋势分析报告:依产品、应用、地区及细分市场预测(2025-2033年)

可回收3D列印耗材市场规模、份额及趋势分析报告:依产品、应用、地区及细分市场预测(2025-2033年) 3D列印耗材市场-2025-2030年预测

3D列印耗材市场-2025-2030年预测 3D列印耗材市场:依材料类型、技术、终端用户产业、应用及通路划分-2025-2032年全球预测

3D列印耗材市场:依材料类型、技术、终端用户产业、应用及通路划分-2025-2032年全球预测 3D列印长丝市场:按类型、材料类型、应用和地区

3D列印长丝市场:按类型、材料类型、应用和地区 PVA 3D 列印长丝市场报告:2031 年趋势、预测与竞争分析

PVA 3D 列印长丝市场报告:2031 年趋势、预测与竞争分析 全球 3D 列印长丝市场(按类型、最终用途产业和地区划分)- 预测至 2030 年

全球 3D 列印长丝市场(按类型、最终用途产业和地区划分)- 预测至 2030 年 可回收 3D 列印长丝市场分析及预测至 2033 年:按类型、产品、服务、技术、应用、材料类型、製程、最终用户、安装类型和解决方案全球柔性长丝3D列印材料市场:预测(2025-2030)

可回收 3D 列印长丝市场分析及预测至 2033 年:按类型、产品、服务、技术、应用、材料类型、製程、最终用户、安装类型和解决方案全球柔性长丝3D列印材料市场:预测(2025-2030)